- Home

- »

- Medical Devices

- »

-

Therapy Devices Market Size & Share Report, 2026-2033GVR Report cover

![Therapy Devices Market (2026 - 2033)Report]()

Therapy Devices Market (2026 - 2033)

Size, Share & Trends Analysis Report By Application (Pain Management, Rehabilitation & Physical Therapy, Respiratory Therapy), By End Use (Hospitals & Specialty Clinics, Rehabilitation Centers), By Region, And Segment Forecasts

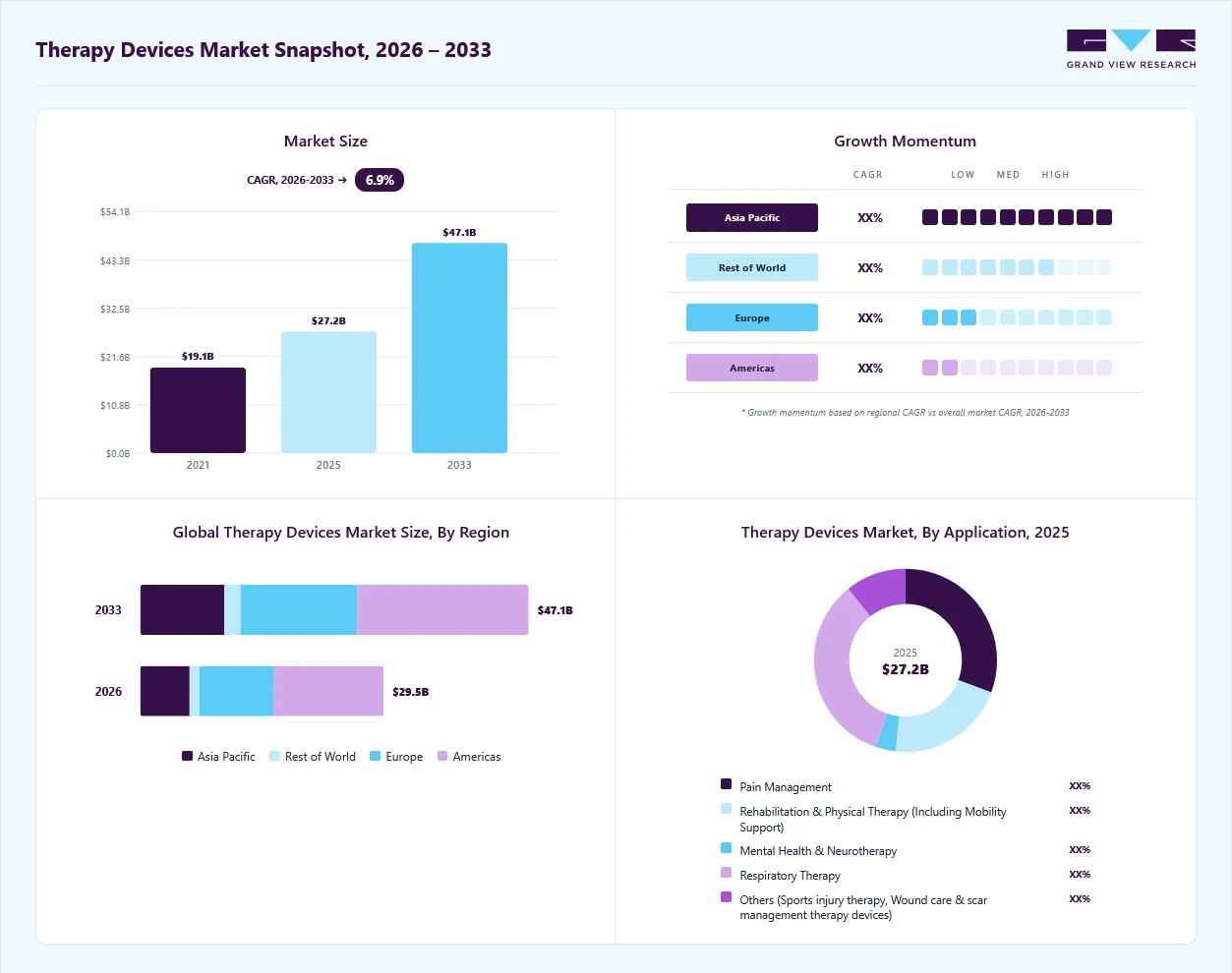

Market Size, 2025

$27.2BMarket Estimate, 2026

$29.5BMarket Forecast, 2033

$47.1BCAGR, 2026–2033

6.9%Therapy Devices Market Summary

The global therapy devices market size was valued at USD 27.2 billion in 2025 and is projected to grow from USD 29.5 billion in 2026 to USD 47.1 billion by 2033, at a CAGR of 6.9% from 2026 to 2033. The market in North America dominated with a revenue share of 45.5% in 2025. The growth is attributed to the growing burden of pain & musculoskeletal disorders and rising adoption of advanced neurotherapy and mental health solutions.

Key Market Trends & Insights

- By application: The respiratory therapy segment held the largest share in 2025.

- By end use: The hospitals segment held the largest share in 2025.

Regional Highlights

- Largest regional market: North America (45.5% revenue share, 2025)

- The therapy devices industry in the U.S. held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 27.2 Billion

- Estimated market size in 2026: USD 29.5 Billion

- Projected market size by 2033: USD 47.1 Billion

- CAGR (2026-2033): 6.9%

For instance, according to the report The State of Musculoskeletal Health 2024 published by the Versus Arthritis Organization, more than 10 million people in the UK have arthritis. In addition, around 27,000 adults are newly diagnosed with rheumatoid arthritis each year in the UK. The rise in chronic respiratory diseases and growing geriatric population further contribute to market growth. Moreover, growing shift towards home-based and self-administered therapy and supportive initiatives by government and private organizations drive market growth further.")

The increasing prevalence of chronic pain and musculoskeletal disorders is a significant driver for the market. This increasing prevalence is accelerating the demand for device-based, non-pharmacological therapies. Conditions such as arthritis, lower back pain, sports injuries, post-operative pain, and age-related mobility impairment require repetitive, localized, and long-term therapeutic intervention, optimally delivered through therapy devices rather than episodic drug treatment. This drives the adoption of electrical stimulation (TENS, NMES), ultrasound therapy, cryotherapy, thermotherapy, and laser therapy devices across clinical and home care settings. According to Hinge Health’s annual State of Musculoskeletal (MSK) Care Report, approximately 40% of adults in the U.S. are affected by MSK conditions.

Moreover, technological innovation in rehabilitation and physical therapy is a key factor driving market growth. Advanced therapy devices now integrate robotics, motorized assistance, and sensor-based systems to support recovery from stroke, orthopedic injuries, neurological disorders, and age-related mobility decline. Robotic-assisted gait trainers, exoskeletons, and automated therapy platforms enable repetitive, high-intensity, and task-specific rehabilitation that is difficult to achieve through manual therapy alone. These technologies improve functional outcomes, reduce therapist fatigue, and increase therapy consistency, driving adoption across hospitals, rehabilitation centers, and specialty clinics. For instance, in January 2025, IIT Kanpur introduced a Brain-Computer Interface (BCI)-based robotic hand exoskeleton for stroke recovery, integrating brain signals with therapeutic movements via closed-loop control.

In addition, Chronic Obstructive Pulmonary Disease (COPD) is a progressive respiratory condition that affects approximately 11% of adults aged over 25 years, with global COPD cases projected to grow by 23.3% to reach nearly 592 million by 2050. The rising prevalence of chronic respiratory diseases represents a high-impact driver for market growth. In addition, increasing awareness of respiratory comorbidities particularly obstructive sleep apnea (OSA) among COPD patients is contributing to higher diagnosis rates and expanding treatment demand, thereby supporting sustained market expansion.

Government and private-sector initiatives are accelerating the adoption of therapy devices by expanding access, funding, and institutional readiness for device-based therapeutic care. Public health programs targeting chronic disease management, disability rehabilitation, respiratory care, and mental health increasingly incorporate therapy devices as standard care tools. Government-backed investments in rehabilitation centers, pulmonary care units, and community health infrastructure create sustained demand for respiratory therapy devices, rehabilitation systems, neurotherapy devices, and pain management equipment. For instance, in the U.S., the CDC has included sleep apnea in its broader public health messaging about sleep hygiene and chronic disease management. Similarly, in the UK, the National Health Service (NHS) promotes sleep health awareness and encourages people to seek diagnostic testing for sleep apnea.

Some of the notable government initiatives support the growth and adoption of the CPAP devices market:

-

In September 2025, Brisbane-based Ceretas received a USD 2.4 million Australian Government grant via the MRFF CUREator+ program to advance its non-invasive therapeutic ultrasound device. Targeting memory/cognition improvement in Alzheimer’s patients, it uses neuromodulation to stimulate deep brain regions, clear amyloid/tau plaques by opening the blood-brain barrier and enhance drug delivery, without surgery.

Table 1: Global medical therapy device EMS ecosystem structure

Ecosystem Layer

Key Role in Value Chain

Typical Activities

Representative Regions / Hubs

Tier-1 Global EMS Providers

End-to-end manufacturing partners for OEMs

Design for Manufacturing (DfM), prototyping, PCBA, system integration, testing, regulatory-compliant production

U.S., Germany, China, Singapore

Tier-2 Regional EMS Firms

Regional manufacturing and integration

PCBA, electromechanical integration, box-build assembly, validation

Mexico, India, Malaysia, Vietnam, Eastern Europe

Tier-3 Component Suppliers

Critical component supply

Sensors, power electronics, ASICs, connectors, medical plastics, batteries

China, Japan, South Korea, Taiwan

OEM & MedTech Clusters

Complete analysis will be part of the final deliverable

Regulatory & Policy Frameworks

Export & Nearshore Manufacturing Hubs

Localization & Emerging Manufacturing Nodes

Market Concentration And Characteristics

The therapy devices industry exhibits a high degree of innovation, driven by advancements in the development of multifunctional devices that combine therapeutic modalities. For instance, in January 2026, Senseonics initiated the commercial launch of Eversense 365 CGM sensor integrated with Sequel Med Tech's twiist automated insulin delivery (AID) system on January 8, 2026. The first patients received the implantable one-year sensor paired with the Twiist pump, featuring iiSure insulin volume measurement and the Loop algorithm for precise delivery. Targets type 1 diabetes in adults.

The market is witnessing a moderate level of merger and acquisition (M&A) activity, as companies seek to enhance technological innovation and expand their global presence. For instance, in July 2025, neurocare group expanded its U.S. footprint through a collaborative arrangement with Mid-Ohio Behavioral Health, adding five outpatient clinics to its network delivering TMS therapy and related services.

The market is moderately regulated, by ensuring product safety, clinical effectiveness, and manufacturing quality. Strict approval pathways, post-market surveillance requirements, and compliance with international standards often extend development timelines and increase costs for manufacturers. However, these regulations also build clinical trust, accelerate adoption in hospitals and home care settings, and encourage companies to invest in evidence based innovation.

The market is witnessing continuous diversification, driven By application launch and steady technological refinement. Companies are increasingly developing alternative devices that deliver similar therapeutic benefits while offering greater precision, enhanced patient comfort, and improved ease of use. These advancements are expanding treatment choices for providers and patients, while intensifying competition as newer, more efficient solutions replace conventional therapy approaches.

The devices market is witnessing moderate regional expansion, with leading manufacturers extending their presence across Asia-Pacific, the Middle East & North Africa (MENA), and Latin America to tap into growing demand driven by rising demand for rehabilitation, pain management, respiratory care, and home-based therapy solutions. Manufacturers are strengthening regional distribution channels, partnering with local healthcare providers, and expanding training programs to improve device availability and usage. This geographic expansion is improving access to modern therapies in emerging markets while supporting sustained global market growth.

Application Insights

By application, the respiratory therapy segment accounted for the largest revenue share of 33.93% in 2025. The demand for respiratory therapy devices is driven by the rising prevalence of chronic respiratory diseases, increasing diagnosis of sleep apnea, aging populations, and growing exposure to environmental risk factors such as air pollution and tobacco use. Healthcare systems are increasingly emphasizing non-invasive respiratory support to reduce hospital admissions, shorten lengths of stay, and enable long-term disease management in home and outpatient settings. These devices increasingly integrate automated pressure adjustment, adherence monitoring, and remote data transmission to support clinician oversight beyond hospital environments. This transition strengthens the role of respiratory therapy devices across the full continuum of care, spanning acute stabilization, chronic management, and functional rehabilitation.

The mental health and neurotherapy segment is expected to grow at the fastest CAGR over the forecast period. The mental health and neurotherapy segment comprises non-implantable devices designed to modulate brain activity and support the management of neurological and psychiatric conditions. The rising diagnosis rates, treatment resistance to pharmacotherapy, and demand for non-drug interventions continue to boost segment expansion. Furthermore, focused ultrasound-based neuromodulation is explored as an investigational approach for selected neurological indications. For instance, research published in August 2025 by teams at Shenzhen University and Longgang Central Hospital described a flexible, wearable ultrasound patch designed for noninvasive targeting of amyloid-β plaques in familial Alzheimer’s disease models. Preclinical results demonstrated reduced neuroinflammation and measurable cognitive improvement following short-term treatment. While such findings highlight future therapeutic potential, ultrasound-based neurotherapy remains largely within the research and early development phase.

End Use Insights

By end use, the hospitals & specialty clinics segment accounted for the largest revenue share of 37.10% in 2025. Hospitals and specialty clinics represent the primary adoption centers for advanced therapy devices as they deliver acute, post-operative, and complex therapeutic interventions. These settings utilize a broad range of devices, including respiratory therapy systems, infusion pumps, neurostimulation platforms, and rehabilitation equipment. High patient volumes and the need for continuous monitoring drive demand for reliable, high-performance therapeutic systems. Hospitals also serve as early adopters of technologically advanced and high-risk therapy devices. Moreover, in April 2025, the Brihanmumbai Municipal Corporation (BMC) Hospital integrated Sky Medical's geko neuromuscular electro-stimulator into physiotherapy protocols for neuro and orthopedic patients. Worn below the knee, it stimulates the peroneal nerve to boost circulation, reduce edema/spasticity, and enable early mobilization/home therapy, enhancing stroke/ortho recovery efficiency.

The home-care & consumer use segment is expected to grow at the fastest CAGR over the forecast period. Technological advancements are strengthening adoption in this segment through connectivity, automation, and simplified interfaces. Modern home-use therapy devices incorporate remote monitoring, mobile app integration, and automated therapy adjustments to support adherence and safety. These features allow clinicians to track patient progress while reducing the need for in-person visits. For instance, in June 2025, PharmaSens AG partnered with SiBionics to develop niia signature, an integrated wearable insulin patch pump combining real-time CGM with automated delivery. Leveraging PharmaSens' pump platform and SiBionics' biosensors, it simplifies type 1 diabetes management via a single discreet device.

Regional Insights

North America therapy devices industry dominated the global market with a share of 45.50% in 2025, driven by high incidence of osteoarthritis, chronic back pain, stroke, and sports injuries, thereby driving demand for therapy devices. An aging population increases the burden of degenerative joint and neuromuscular conditions requiring long-term rehabilitation. For instance, in December 2024, the Health Policy Institute reported that lower back pain affecting nearly 65 million Americans each year remains the most common MSK complaint. Obesity and sedentary lifestyles further contribute to musculoskeletal dysfunction. Early intervention protocols emphasize non-invasive therapeutic modalities. These epidemiological trends demand the procurement of therapy devices across clinical and home settings.

U.S. Therapy Devices Market Trends

The U.S. therapy devices industry accounted for the largest market share in North America in 2025. The U.S. reports a substantial incidence of arthritis, chronic back pain, cardiovascular disease, and neurological disorders. In addition, an aging population increases demand for rehabilitation, pain management, and mobility support solutions. Rising obesity rates contribute to orthopedic and joint-related conditions. Post-stroke and post-surgical rehabilitation requirements sustain the utilization of electrotherapy and robotic systems. Disease burden directly expands the addressable market for therapeutic devices.

Europe Therapy Devices Market Trends

The Europe therapy devices industry is expected to witness considerable growth over the forecast period. Europe has one of the world’s oldest populations, especially in Germany, Italy, France, and Spain. As life expectancy rises, chronic musculoskeletal disorders, stroke-related disabilities, neurodegenerative diseases, COPD, diabetes, and chronic wounds become more prevalent. Elderly patients with multiple conditions require ongoing therapeutic intervention instead of episodic care. In addition, according to the “Chronic Respiratory Diseases and Health Equity By 2050” report published by the WHO and the European Respiratory Society in June 2025, chronic respiratory diseases are the sixth leading cause of death in Europe, with around 80% of all CRD deaths caused by COPD.

The therapy devices industry in the UK is anticipated to grow over the forecast period. The increasing prevalence of chronic diseases is expected to drive demand for therapy devices. Moreover, high demand for respiratory devices is expected to drive the market, driven by the rising prevalence of chronic respiratory diseases in the country. According to an article published by the Sleep Apnea Trust in 2023, up to 10 million people in the UK suffer from the most prevalent type of OSA. Thus, the increasing prevalence of respiratory disorders in the country is expected to fuel market growth over the forecast period.

Germany therapy devices industry is expected to witness considerable growth over the forecast period. Germany’s medical technology sector benefits from strong engineering expertise and significant R&D investment. Domestic manufacturers produce advanced neurostimulation, respiratory therapy, and electromechanical rehabilitation systems. The integration of digital monitoring and therapy optimization improves clinical outcomes. For instance, in April 2025, Novocure's Optune Lua device received CE Mark approval for treating adults with metastatic NSCLC alongside immune checkpoint inhibitors or docetaxel post-platinum chemotherapy.

Asia Pacific Therapy Devices Market Trends

The therapy devices industry in Asia Pacific region is expected to grow during the forecast period. The region is experiencing rising rates of cardiovascular disease, diabetes, chronic respiratory disorders, and musculoskeletal conditions, driven by urbanization, sedentary lifestyles, and environmental factors. High smoking rates in several countries further increase the COPD burden. Furthermore, major players in the region are contributing to market growth by expanding their product portfolios & entering strategic partnerships. For instance, in November 2024, ResMed announced plans to expand its operations in Singapore, focusing on enhancing sleep and respiratory health solutions.

China therapy devices industry accounted for the largest market share in the Asia Pacific region in 2025. The high prevalence of chronic diseases in China, increasing applications in home care settings, ongoing demographic & economic trends, and rapid technological advancements are among the major factors driving market growth. Chronic respiratory diseases are a leading cause of death in China. For instance, in November 2023, the WHO stated that China has almost 100 million people living with chronic obstructive pulmonary disease (COPD) and accounts for almost 25% of all COPD cases globally. Increasing cigarette smoking and rising air pollution in this country are contributing to market growth.

Australia therapy devices industry is expected to grow at a significant CAGR over the forecast period. Australia’s well-developed healthcare infrastructure and strong regulatory framework support the adoption of therapy devices by ensuring the quality and safety of medical devices in the market, thereby fostering market growth. Moreover, conditions such as cardiovascular disease, diabetes, and hypertension are commonly linked with untreated sleep apnea, leading to a higher demand for effective management strategies such as CPAP therapy. For instance, according to data released by the Australian Government in June 2024, chronic obstructive pulmonary disease (COPD) accounted for 3.6% of the total disease burden, while respiratory conditions accounted for 50% of the overall health impact in 2023.

Latin America Therapy Devices Market Trends

The therapy devices industryin Latin America is expected to witness significant growth over the forecast period, attributed to improving healthcare infrastructure, rising awareness of non-invasive treatment options, and increasing demand for home-based and rehabilitation therapies. Hospitals and clinics are gradually adopting advanced therapy technologies to manage chronic conditions, post-surgical recovery, and mobility-related disorders more effectively. At the same time, cost-efficient devices and portable therapy solutions are gaining popularity as access to private healthcare expands across major urban areas.

Brazil therapy devices industry is anticipated to grow over the forecast period. The growing prevalence of chronic diseases such as hypertension, cardiovascular diseases (CVDs), chronic respiratory disorders, and cancer is driving the market growth. In addition, the aging population plays a significant role, as older adults are more susceptible to COPD, driving the need for respiratory devices.

MEA Therapy Devices Market Trends

The therapy devices industryin the MEA is expected to grow significantly owing to growing healthcare investments, rising awareness of rehabilitation and pain management solutions, and increasing adoption of home-based therapy equipment. Hospitals across Gulf countries are integrating advanced therapy technologies as part of broader healthcare modernization initiatives, while emerging African markets are showing improving access to basic therapeutic devices through public and private sector programs. In addition, the demand for portable and easy-to-use therapy systems is increasing as providers focus on long-term patient care and recovery outside traditional clinical settings.

South Africa therapy devices industry is anticipated to witness considerable growth over the forecast period, driven by rising private healthcare facilities, growing demand for rehabilitation and pain management solutions, and increased adoption of home-based therapy equipment. Hospitals and specialty clinics are gradually integrating modern therapy technologies to support post-surgical recovery, chronic condition management, and mobility improvement. At the same time, cost-effective and portable devices are gaining traction as access to outpatient and home care services improves.

Key Therapy Devices Company Insights

Leading players in the therapy devices industry such as PAJUNK, OMRON Healthcare, Inc. and Zynex Medical have strategically employed innovative approaches, including mergers and acquisitions, market penetration initiatives, partnerships, and distribution agreements. These strategies aim to enhance their revenue streams by leveraging collaborative efforts, expanding market reach, and fostering synergies within the dynamic landscape of therapy devices. Emerging market entrants such as Compex and Pain Care Labs are directing their efforts toward broadening their market presence, creating inventive technologies, and establishing strategic partnerships as part of their strategy to contend with established industry leaders.

Key Therapy Devices Companies:

The following key companies have been profiled for this study on the therapy devices market.

- PAJUNK

- OMRON Healthcare, Inc.

- Zynex Medical

- Litemed

- DJO Global

- Boston Scientific Corporation

- SPR

- Medtronic

- Nalu Medical, Inc.

- Abbott

- Atricure, Inc.

- ThermaCare

- Avanos Medical, Inc

- ICU Medical, Inc.

- Dynatronics Corporation

- RS Medical

- Bioventus

- BioElectronics Corporation

- ProMedTek Inc.

- InfuSystem

- Gladiator Therapeutics

- PAIN MANAGEMENT TECHNOLOGIES, INC.

- PainPod

- BioWave Corporation

- DIS&L

- TrueRelief, LLC

- MAI Medical

- Compex

- Pain Care Labs

- PowerCure Europe

- Shenzhen WELLD Medical Electronics Co., Ltd.

- Longest Medical

- Shenzhen Roundwhale Technology Co., Ltd

- Shenzhen Xinmaikang Technology Co., Ltd.

- Huizhou Huan Dong Industrial Co., Ltd.

- Yunblaze Technology China

- Hong Qiangxing (Shenzhen) Electronics Limited

- Shenzhen Jrw Technology Co., Ltd.

- Quanding Medical

- Shenzhen Xinkang Health Technology Co., Ltd.

Recent Developments

-

In February 2026, AIROS Medical launched the FDA-cleared ARTAIRA arterial compression device, a non-invasive pneumatic system designed to improve lower-limb blood circulation and manage peripheral arterial disease symptoms in home-based treatment settings.

-

In February 2026, StimLabs received FDA 510(k) clearance for DermaForm collagen scaffold particulate device, expanding its wound care portfolio, strengthening collaboration with Geistlich, and supporting treatment of complex chronic and acute wounds.

-

In January 2026, BioStem Technologies acquisition of BioTissue Holdings’ surgical and wound care business, integrating Neox and Clarix product lines with a national sales force to expand acute/chronic wound care presence.

Therapy Devices Market Report Scope

Report Attribute

Details

Market size in 2025

USD 27.2 billion

Estimated market size in 2026

USD 29.5 billion

Projected market size by 2033

USD 47.1 billion

Growth rate

CAGR of 6.9% from 2026 to 2033

Actual Data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Australia; Thailand; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

PAJUNK; OMRON Healthcare, Inc.; Zynex Medical Litemed; DJO Global; Boston Scientific Corporation; SPR; Medtronic; Nalu Medical, Inc.; Abbott; Atricure, Inc.; ThermaCare; Avanos Medical, Inc; ICU Medical, Inc.; Dynatronics Corporation; RS Medical; Bioventus; BioElectronics Corporation; ProMedTek Inc.; InfuSystem; Gladiator Therapeutics; PAIN MANAGEMENT TECHNOLOGIES, INC.; PainPod; BioWave Corporation; DIS&L; TrueRelief, LLC; MAI Medical; Compex; Pain Care Labs; PowerCure Europe;Shenzhen WELLD Medical Electronics Co., Ltd.; Longest Medical; Shenzhen Roundwhale Technology Co., Ltd; Shenzhen Xinmaikang Technology Co., Ltd.; Huizhou Huan Dong Industrial Co., Ltd.; Yunblaze Technology China; Hong Qiangxing (Shenzhen) Electronics Limited; Shenzhen Jrw Technology Co., Ltd.; Quanding Medical; Shenzhen Xinkang Health Technology Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Therapy Devices Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global therapy devices market report based on application, end use, and region:

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Pain Management

-

Electrical Stimulation (TENS/NMES)

-

Cryo / Thermotherapy

-

Laser therapy

-

Ultrasound Therapy

-

-

Rehabilitation & Physical Therapy

-

Robotic Rehabilitation Systems

-

Virtual Reality Therapy Systems

-

Exoskeleton Devices

-

Electromechanical Therapy Platforms

-

-

Mental Health & Neurotherapy

-

Neurostimulation (tDCS, TMS)

-

EEG-based Neurofeedback Devices

-

-

Respiratory Therapy

-

CPAP / BiPAP

-

Non-Invasive Ventilators/Resuscitators

-

Pulmonary Rehab Devices

-

Nebulizers / Aerosol Systems

-

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals & Specialty Clinics

-

Rehabilitation Centers

-

Home-care & Consumer Use

-

Long-term Care Facilities

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The respiratory therapy segment led with a 33.9% revenue share in 2025, while mental health and neurotherapy is the fastest-growing segment.

Hospitals & specialty clinics held the largest revenue share 37.1% in 2025, while home-care & consumer use is the fastest-growing area.

North America therapy devices market dominated the with a share of 45.5% in 2025.

The growth is attributed to the growing burden of pain & musculoskeletal disorders and rising adoption of advanced neurotherapy and mental health solutions. In addition, rise in chronic respiratory diseases and growing geriatric population further contribute to market growth. Moreover, growing shift towards home-based and self-administered therapy and supportive initiatives by government and private organizations drive market growth further.

The global therapy devices market size was estimated at USD 27.2 billion in 2025 and is expected to reach USD 29.5 billion in 2026.

The global therapy devices market is expected to grow at a compound annual growth rate of 6.0% from 2026 to 2033 to reach USD 47.1 billion by 2033.

Some key players operating in the therapy devices market include ProMedTek Inc.; InfuSystem; Gladiator Therapeutics; PAIN MANAGEMENT TECHNOLOGIES, INC.; PainPod; BioWave Corporation; DIS&L; TrueRelief, LLC; MAI Medical; Compex; Pain Care Labs; PowerCure Europe;Shenzhen WELLD Medical Electronics Co., Ltd.; Longest Medical; Shenzhen Roundwhale Technology Co., Ltd; Shenzhen Xinmaikang Technology Co., Ltd.; Huizhou Huan Dong Industrial Co., Ltd.; Yunblaze Technology China; Hong Qiangxing (Shenzhen) Electronics Limited; Shenzhen Jrw Technology Co., Ltd.; Quanding Medical; Shenzhen Xinkang Health Technology Co., Ltd.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.