- Home

- »

- Specialty Polymers

- »

-

Thermoplastic Elastomer Market Size, Growth Report, 2026-2033GVR Report cover

![Thermoplastic Elastomer Market (2026 - 2033)Report]()

Thermoplastic Elastomer Market (2026 - 2033)

Size, Share & Trends Analysis Report By Application (Automotive, Electrical & Electronics, Industrial, Medical), By Material (Polystyrenes, Poly Olefins, Poly Ether Imides, Poly Esters, Poly Amides), By Region, And Segment Forecasts

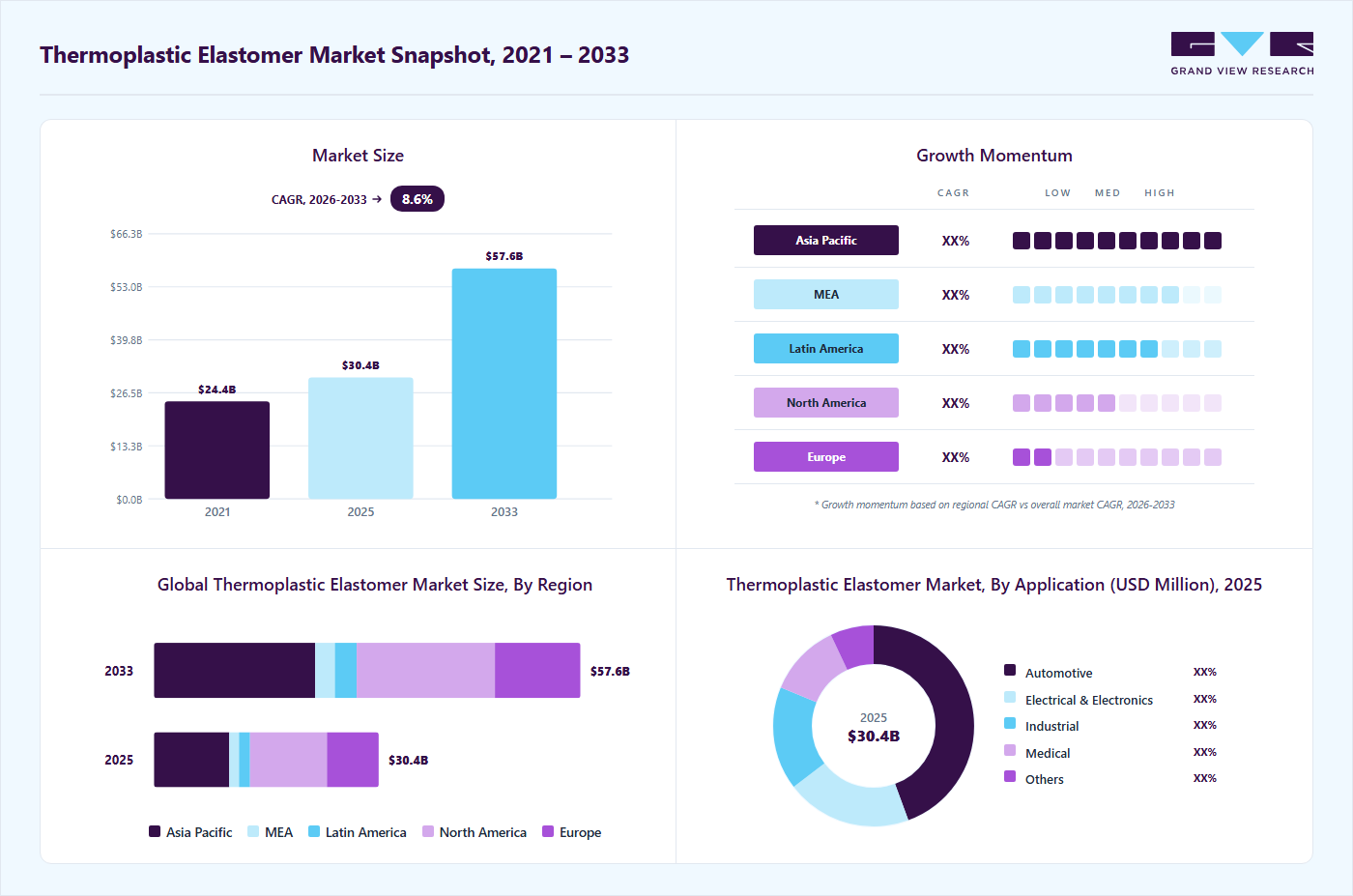

Market Size, 2025

$30.4BMarket Estimate, 2026

$32.4BMarket Forecast, 2033

$57.6BCAGR, 2026–2033

8.6%Thermoplastic Elastomer Market Summary

The global thermoplastic elastomer market size was valued at USD 30.4 billion in 2025 and is projected to grow from USD 32.4 billion in 2026 to USD 57.6 billion by 2033, at a CAGR of 8.6% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 34.21% in 2025. The rising demand for flexible and durable materials, such as thermoplastic elastomer (TPEs), across automotive, construction, and consumer goods industries is driving global market growth.

Key Market Trends & Insights

- By material: Polyamides segment is expected to grow at a considerable CAGR of 10.0% from 2026 to 2033 in terms of revenue.

- By application: Medical segment is expected to grow at the fastest CAGR of 10.1% from 2026 to 2033 in terms of revenue.

Regional Highlights

- Largest regional market: North America (34.21% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. thermoplastic elastomer industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 30.4 Billion

- Estimated market size in 2026: USD 32.4 Billion

- Projected market size by 2033: USD 57.6 Billion

- CAGR (2026-2033): 8.6%

Thermoplastic elastomers (TPEs) are a type of polymer material that merges the elastic properties of traditional rubber with the processing benefits of thermoplastics. They demonstrate reversible elasticity, flexibility, and softness at ambient temperatures, and can be melted and processed using standard thermoplastic methods like injection molding, extrusion, and blow molding. This unique combination of characteristics is achieved through a multiphase structure, usually consisting of rigid thermoplastic sections that provide mechanical strength and flexible elastomeric sections that provide elasticity.

")

From market and sustainability perspectives, TPEs are gaining popularity due to their recyclability, reduced energy consumption during processing, and their ability to enable lightweight construction compared to thermoset rubbers. Their ability to integrate with multi-material designs and support overmolding also enhances design flexibility and cost-effectiveness. Current advancements in materials are focusing on bio-based raw materials, improved heat and oil resistance, and increased durability, establishing TPEs as a vital material platform for future elastomeric applications.

Drivers, Opportunities & Restraints

The industry for thermoplastic elastomers (TPE) is primarily driven by the growing demand for lightweight, flexible, and recyclable materials across the automotive, consumer goods, and electrical & electronics sectors. In the automotive industry, manufacturers are increasingly replacing traditional rubber and PVC with TPEs to reduce weight, improve fuel efficiency, and comply with emissions standards. Furthermore, TPEs can be easily processed using conventional thermoplastic machinery, which, along with quicker cycle times and reduced scrap rates, promotes cost-effective manufacturing, making TPEs appealing for large-scale production.

A significant limitation of thermoplastic elastomers is their relatively higher cost compared to conventional elastomers and commodity plastics, especially in applications where price is a crucial factor. Some grades of TPE also exhibit limitations in high-temperature resistance, long-term creep resistance, and chemical or oil resistance compared with thermoset rubbers, which hampers their use in demanding industrial settings. Additionally, the variability in performance across different TPE types requires careful material selection, potentially complicating design processes and extending qualification timelines for end users.

Considerable potential exists for thermoplastic elastomers as industries such as electric vehicles, medical devices, and sustainable materials continue to grow. In electric vehicles, TPEs are increasingly used in battery-pack components, cable insulation, and sealing applications due to their flexibility, vibration-damping properties, and compatibility with overmolding techniques. The introduction of bio-based, recyclable TPE variants, alongside improvements in heat and chemical resistance, is paving the way for innovations in healthcare, wearable technology, and high-end consumer goods. These developments position TPEs to gradually take market share away from both thermoset rubbers and traditional plastics in the medium to long term.

Market Concentration & Characteristics

The industry is highly fragmented, with key participants involved in R&D and technological innovations. Notable companies include BASF SE, Arkema, DuPont, Covestro AG, and China Petrochemical Corporation, among others. Several players are developing frameworks to improve their market share. For instance, in February 2025, Prism Worldwide collaborated with Sherwood Industries to bring to market sustainable thermoplastic elastomer sheets created from Prism's high-quality recycled TPE (Ancora) sourced from discarded tires. The partnership moved from testing in 2024 to official commercialization in early 2025, with Sherwood investing in specialized extrusion capabilities for these new materials.

Material Insights

The polystyrene segment led the market with a 32.01% revenue share in 2025, driven by its versatility across industries such as packaging, consumer goods, and automotive. This material offers a unique balance of flexibility, durability, and cost efficiency, making it a popular choice for manufacturing lightweight, high-performance products.

Poly-amide TPEs are projected to grow at the fastest CAGR of 10.0% over the forecast period. Nylon TPEs, a type of polyamide-based thermoplastic elastomer, are known for their combination of rigidity and flexibility, providing excellent thermal and mechanical performance. These TPEs are specifically engineered for demanding environments and are commonly utilized in automotive and industrial applications that require strength and heat resistance.

Application Insights

The automotive segment dominated the market, accounting for 40.15% of revenue in 2025. The automotive industry drives demand for TPEs due to their lightweight, durable, and flexible properties, which are utilized in manufacturing vehicle components such as seals, hoses, and interiors.

Medical applications of TPE are expected to grow at the fastest CAGR of 10.1% over the forecast period.The growing geriatric population in countries such as Japan, Germany, and the U.S. drives demand for medical devices. TPEs are gaining popularity in the medical field due to their biocompatibility, flexibility, and softness, making them ideal for applications such as medical tubing, catheters, and syringe components.

Regional Insights

North America's thermoplastic elastomer market dominated the global market in 2025, with a 34.21% revenue share, driven by robust demand from key industries such as automotive, construction, and consumer goods for TPEs. The region’s advanced manufacturing capabilities and emphasis on sustainable materials contribute to its dominance in the global market. Investment in innovation and product development also fuels growth.

U.S. Thermoplastic Elastomer Market Trends

The thermoplastic elastomer market in the U.S. dominated the North American market, accounting for 74.50% of revenue in 2025. Known for its advanced technological innovations across the automotive, healthcare, and electronics industries, the country’s strong technological infrastructure supports extensive R&D and promotes the use of TPEs in various innovations.

Europe Thermoplastic Elastomer Market Trends

The thermoplastic elastomer market in Europe held a substantial market share in 2025. The region is expected to maintain its dominance in the sector, driven by growing demand for lightweight electric and hybrid vehicles. The thermoplastic elastomer market in Germany led the European market, given its widespread applications and benefits in automotive components; this dominance is expected to further fuel market expansion.

Asia Pacific Thermoplastic Elastomer Market Trends

The thermoplastic elastomer market in Asia Pacific is expected to register the fastest CAGR of 10.2% in the forecast period. Market growth in the region is fueled by industrialization, urbanization, and demand for lightweight, durable, and recyclable materials in industries such as automotive, construction, and consumer goods. The shift to EVs and fuel-efficient vehicles further accelerates demand, particularly in automotive applications.

China dominated the Asia Pacific thermoplastic elastomer market in 2025, owing to its manufacturing dominance and strong demand from the automotive, construction, electronics, and consumer goods sectors. The country’s efforts to reduce emissions and its focus on sustainable development boost TPE adoption.

Key Thermoplastic Elastomer Companies Insights

Key players operating in the thermoplastic elastomer market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key Thermoplastic Elastomer Companies:

The following key companies have been profiled for this study on the thermoplastic elastomer market.

- BASF SE

- Arkema

- DuPont

- Covestro AG

- China Petrochemical Corporation

- Dynasol Elastomerss

- EMS-CHEMIE HOLDING AG

- Evonik Industries

- Kraton Polymers LLC

- LG Chem

- LCY Chemical Corporation

- Lubrizol Corporation

- LyondellBasell Industries

- Tosoh Corporation

- Avient Corporation

- Teknor APEX Company

- The Dow Chemical Company

- TSRC Corporation

Recent Developments

-

In August 2025, SABIC introduced a new flame-retardant thermoplastic compound, LNP THERMOCOMP WFC061I, aimed at improving safety and performance in electric vehicle control units (EVCUs). This material offers flame-retardant properties that are both non-brominated and non-chlorinated, along with strong structural characteristics, making it ideal for protective housings and enclosures for essential EV electronics.

-

In February 2025, Prism Worldwide collaborated with Sherwood Industries to bring to market sustainable thermoplastic elastomer sheets created from Prism's high-quality recycled TPE (Ancora) sourced from discarded tires. The partnership moved from testing in 2024 to official commercialization in early 2025, with Sherwood investing in specialized extrusion capabilities for these new materials.

Thermoplastic Elastomer Market Report Scope

Report Attribute

Details

Market size in 2025

USD 30.4 billion

Estimated Market size in 2026

USD 32.4 billion

Projected Market size by 2033

USD 57.6 billion

Growth rate

CAGR of 8.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in kilotons; revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Volume and revenue forecast, company ranking, competitive landscape, growth factors, trends

Segments covered

Application, material, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; China; India; Japan; Brazil; Saudi Arabia

Key companies profiled

BASF SE; Arkema; DuPont; Covestro AG; China Petrochemical Corporation; Dynasol Elastomers; EMS-CHEMIE HOLDING AG; Evonik Industries; Kraton Polymers LLC; LG Chem; LCY Chemical Corporation; Lubrizol Corporation; LyondellBasell Industries; Tosoh Corporation; Avient Corporation; Teknor APEX Company; The Dow Chemical Company; TSRC Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Thermoplastic Elastomer Market Report Segmentation

This report forecasts volume and revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global thermoplastic elastomer market report based on material, application, and region:

-

Material Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Polystyrenes

-

Poly Olefins

-

Poly Ether Imides

-

Poly Urethanes

-

Poly Esters

-

Poly Amides

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Electrical & Electronics

-

Industrial

-

Medical

-

Consumer Goods

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

-

Frequently Asked Questions About This Report

Some key players operating in the thermoplastic elastomer market include Advanced Elastomer Systems L.P., Arkema S.A., BASF SE, Bayer MaterialScience LLC, China Petroleum & Chemical Corporation, Dynasol Elastomers LLC, EMS group, Evonik Industries

Key factors that are driving the thermoplastic elastomer market growth include increasing demand in automotive component manufacturing and increasing consumer preference for high-performance and lightweight passenger cars.

Automotive held the largest revenue share 40.2% in 2025, while medical is the fastest-growing area.

North America dominated with a 34.2% revenue share in 2025.

The global thermoplastic elastomer market size was estimated at USD 30.4 billion in 2025 and is expected to reach USD 32.4 billion in 2025.

The global thermoplastic elastomer market is expected to grow at a compound annual growth rate of 8.6% from 2026 to 2033, reaching USD 57.6 billion by 2033.

Polystyrene segment led with a 32.0% revenue share in 2025, while Poly-amide TPEs is the fastest-growing segment.

About the Author(s)

Specialty Polymers Research Team

Specialty & Chemicals · Specialty PolymersThis report was authored by the specialty polymers research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the specialty polymers segment of the specialty & chemicals industry. All findings are based on proprietary specialty & chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.