- Home

- »

- Clinical Diagnostics

- »

-

Tissue Diagnostics Market Size, Industry Report, 2033GVR Report cover

![Tissue Diagnostics Market Size, Share & Trends Report]()

Tissue Diagnostics Market (2026 - 2033) Size, Share & Trends Analysis Report By Technology (Immunohistochemistry, In Situ Hybridization), By Application (Breast Cancer), By Modality, By End Use (Hospital, Diagnostic Center), By Region, And Segment Forecasts

- Report Summary

- Table of Contents

- Segmentation

- Methodology

- Download FREE Sample

-

Download Sample Report

Download Sample Report

- Buy Now

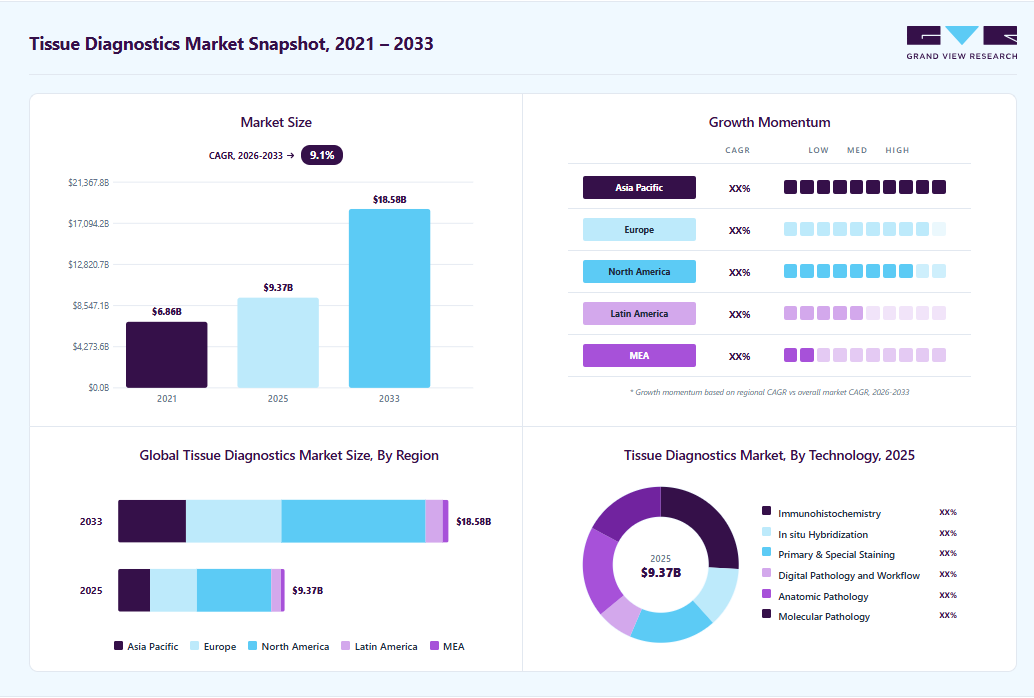

Market Size, 2025

$9.4BMarket Estimate, 2026

$10.1BMarket Forecast, 2033

$18.9BCAGR, 2026–2033

9.1%Tissue Diagnostics Market Summary

The global tissue diagnostics market size was valued at USD 9.4 billion in 2025 and is projected to grow from USD 10.1 billion in 2026 to USD 18.6 billion by 2033, at a CAGR of 9.1% from 2026 to 2033. The North America held the largest share of 44.6% of the global market in 2025. The rising global burden of cancer primarily drives market growth, the growing adoption of precision oncology, and continuous advancements in tissue-based diagnostic technologies.

Key Market Trends & Insights

- By technology: The immunohistochemistry segment accounted for the largest revenue share of 25.9% in 2025.

- By application: The breast cancer segment held the largest share of 50.7% in 2025.

- By end use: The hospitals segment dominated the market, accounting for the largest revenue share of 37.7% in 2025.

- By modality: The clinical market segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (44.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. is expected to grow significantly over the forecast period.

Market Size & Forecast

- Market size in 2025: USD 9.4 Billion

- Estimated market size in 2026: USD 10.1 Billion

- Projected market size by 2033: USD 18.6 Billion

- CAGR (2026-2033): 9.1%

")

Market Dynamics

The worldwide rise in cancer prevalence is significantly driving demand for tissue diagnostics solutions, as accurate tissue analysis remains essential for cancer detection, tumor characterization, and treatment selection. Tissue diagnostic techniques, including immunohistochemistry, in situ hybridization, and digital pathology, enable pathologists to precisely identify tumor stage and biomarker expression. The increasing incidence of cancer has substantially increased the number of biopsy and histopathology procedures performed globally. According to the Global Burden of Disease (GBD) 2023 study, there were approximately 18.5 million new cancer cases and 10.4 million cancer-related deaths worldwide in 2023, contributing to nearly 271 million disability-adjusted life-years (DALYs). Cancer remained the second leading cause of death globally after cardiovascular diseases.

The projected increase in future cancer burden is further accelerating the adoption of tissue diagnostics solutions across hospitals, pathology laboratories, and cancer research centers. The GBD 2023 forecast estimates that global cancer cases will reach nearly 30.5 million and cancer deaths will increase to 18.6 million by 2050. The burden is expected to rise more rapidly in low- and middle-income countries due to population growth, aging demographics, and increasing exposure to behavioral and environmental risk factors. In addition, the growing adoption of precision oncology and targeted therapies is increasing reliance on tissue-based biomarker testing and companion diagnostics to support personalized treatment decisions. This trend is expected to sustain demand for advanced tissue diagnostics instruments, assays, and consumables throughout the forecast period.

The tissue diagnostics industry faces significant challenges due to the high costs of research and development and clinical validation. Developing advanced tissue diagnostic technologies, including digital pathology systems, molecular assays, immunohistochemistry reagents, and AI-based image analysis platforms, requires substantial investments in biomarker discovery, assay optimization, software integration, and regulatory compliance. Companies must also conduct extensive analytical and clinical validation studies to ensure diagnostic accuracy, reproducibility, and safety before commercial launch. These processes lengthen overall product development timelines and increase operational expenses, particularly for small- and mid-sized companies with limited financial resources.

Furthermore, clinical trials and regulatory approval procedures for tissue diagnostics products are complex and expensive, especially for companion diagnostics used in precision oncology applications. Manufacturers are required to generate large volumes of clinical evidence demonstrating the effectiveness of diagnostic tests across diverse patient populations and cancer indications. The need for specialized laboratory infrastructure, skilled professionals, tissue sample collection, and data management further increases development costs. Frequent technological advancements and the continuous need to upgrade diagnostic platforms also add financial pressure on market participants. These cost-related barriers can limit innovation, delay product commercialization, and restrict adoption in price-sensitive healthcare markets.

The increasing adoption of precision oncology and personalized medicine is creating substantial growth opportunities for the tissue diagnostics market. Healthcare providers are increasingly utilizing tissue-based biomarker testing to identify tumor characteristics, genetic mutations, and protein expression profiles that support targeted therapy selection and personalized treatment strategies. This trend is driving demand for advanced tissue diagnostic technologies, including immunohistochemistry, in situ hybridization, molecular diagnostics, and companion diagnostics. In addition, growing investments in oncology research and biomarker development are accelerating innovation across the market. For instance, in May 2026, Roche announced the acquisition of PathAI to strengthen its artificial intelligence-enabled digital pathology and companion diagnostics portfolio, reflecting the industry's increasing focus on precision oncology and advanced diagnostics.

The growing integration of digital pathology and artificial intelligence into pathology workflows is further creating significant market opportunities. AI-enabled image analysis platforms improve diagnostic efficiency, reduce interpretation variability, and support workflow optimization in pathology laboratories. The expansion of telepathology services is also enhancing access to diagnostic expertise in underserved and remote regions. Furthermore, increasing healthcare expenditure in emerging economies, expanding cancer screening programs, and rising awareness of the importance of early cancer diagnosis are expected to support the adoption of tissue diagnostics solutions.

Digital pathology is transforming traditional histopathology workflows by improving laboratory efficiency, enabling advanced image analysis, and enhancing collaboration among pathology professionals. The adoption of AI-enabled digital pathology platforms, automated staining systems, and image analysis tools is improving diagnostic precision, workflow standardization, and operational efficiency across pathology laboratories. These technologies also support remote consultations and expand access to specialized pathology services in underserved regions. In January 2024, Kobe University and CarbGeM Inc. introduced the PoCGS-Pro automated gram stainer, developed in collaboration with the National Center for Global Health and Medicine. The device was launched as a specified maintenance-controlled medical device and supports automated staining and workflow standardization. Such technological advancements are driving broader adoption of automated and AI-enabled diagnostic solutions across healthcare settings.

The increasing adoption of targeted therapies and personalized medicine is driving strong demand for companion diagnostics in oncology, creating significant growth opportunities for the tissue diagnostics market. Healthcare providers are increasingly utilizing tissue-based biomarker assays to identify eligible patient populations and support precision treatment selection. This trend is accelerating the adoption of companion diagnostic tests based on immunohistochemistry and molecular pathology technologies. For instance, in 2024, Agilent Technologies, Inc. received U.S. FDA approval for the PD-L1 IHC 22C3 pharmDx assay as a companion diagnostic for Jemperli (dostarlimab-gxly), developed in collaboration with GlaxoSmithKline for the treatment of endometrial cancer. The assay enables assessment of PD-L1 expression in tumor tissues, supporting personalized treatment decisions and improving clinical outcomes. Such regulatory approvals are strengthening the role of tissue diagnostics in precision oncology and the development of targeted cancer therapies.

Market Concentration & Characteristics

The industry demonstrates a high degree of innovation, driven by continuous advancements in digital pathology, artificial intelligence, biomarker discovery, and companion diagnostics. Companies are increasingly developing AI-enabled image analysis platforms, automated staining systems, and precision oncology assays to improve diagnostic accuracy and workflow efficiency. In addition, regulatory approvals for companion diagnostics are accelerating market innovation. For instance, in March 2026, Agilent Technologies received U.S. FDA approval for its PD-L1 IHC 22C3 pharmDx assay for esophageal and gastroesophageal junction carcinoma, further strengthening the role of tissue-based companion diagnostics in personalized cancer treatment and precision oncology applications. Such innovations are expected to support the broader adoption of advanced tissue diagnostics technologies and strengthen market growth throughout the forecast period.

The industry is experiencing strong merger and acquisition activity as companies expand capabilities in digital pathology, artificial intelligence, and companion diagnostics. Strategic acquisitions support advancements in precision oncology, biomarker discovery, and automated pathology workflows. For instance, in May 2026, Roche announced the acquisition of PathAI, a U.S.-based digital pathology and AI diagnostics company, to strengthen its AI-enabled tissue diagnostics portfolio. The acquisition is expected to enhance digital pathology workflows, improve biomarker analysis, accelerate the development of companion diagnostics, and support personalized cancer treatment and precision medicine applications.

Regulatory frameworks significantly influence the tissue diagnostics market by ensuring the safety, accuracy, and clinical effectiveness of diagnostic assays and pathology platforms. Stringent approval requirements for companion diagnostics, biomarker assays, and digital pathology solutions increase product development timelines and compliance costs. However, regulatory approvals from agencies such as the U.S. FDA also support market growth by accelerating the commercialization of innovative tissue-based diagnostics and precision oncology technologies.

Regional expansion in the industry is driven by increasing cancer prevalence, improving healthcare infrastructure, and rising adoption of precision oncology technologies across emerging economies. Market participants are expanding their presence in Asia-Pacific, Latin America, and the Middle East through partnerships, distribution agreements, and laboratory expansion initiatives. Growing investments in digital pathology, cancer screening programs, and pathology laboratory modernization are further supporting the adoption of advanced tissue diagnostics solutions across regional healthcare markets.

Technology Insights

The immunohistochemistry segment dominated the industry and accounting for the largest revenue share of 25.87% in 2025, driven by its extensive use in cancer diagnosis, biomarker analysis, and personalized treatment selection. Immunohistochemistry (IHC) utilizes specific antibodies to detect target proteins in tissue samples, enabling accurate tumor classification, prognosis assessment, and therapy selection. The technology is widely used for evaluating biomarkers such as PD-L1, HER2, ER, and PR across multiple cancer types. Growing adoption of precision oncology and companion diagnostics is further supporting segment growth. For instance, in April 2024, Roche received U.S. FDA approval for the VENTANA FOLR1 (FOLR1-2.1) RxDx Assay as a companion diagnostic to identify ovarian cancer patients eligible for treatment with ELAHERE (mirvetuximab soravtansine-gynx). The approval highlighted the growing importance of immunohistochemistry-based biomarker testing in precision oncology and targeted therapy selection.

The digital pathology and workflow segment is anticipated to grow at the fastest CAGR of 12.70% over the forecast period, driven by increasing adoption of AI-enabled pathology platforms, laboratory automation, and remote diagnostic solutions. Digital pathology enhances tissue diagnostics by enabling high-resolution scanning, image analysis, data management, and streamlined pathology workflows. The integration of digital pathology with in situ hybridization (ISH) technologies improves visualization of nucleic acid targets and supports accurate interpretation of tissue-based biomarker results. In addition, digital workflow solutions simplify data storage, retrieval, and sharing, improving collaboration among pathologists and research institutions. Growing demand for workflow efficiency, precision oncology, and telepathology services is further accelerating segment growth across hospitals and diagnostic laboratories.

Application Insights

The breast cancer segment held the largest share of 50.72% in 2025, and is anticipated to grow at the fastest CAGR during the forecast period. The increasing incidence of breast cancer, the rising aging population, and the growing adoption of precision oncology are supporting segment growth. According to the report published by the World Health Organization in April 2026, breast cancer caused approximately 670,000 deaths globally in 2022 and remained the most common cancer among women in 157 countries out of 185. Breast cancer is commonly classified into Hormone Receptor (HR)-positive, HER2-positive, and Triple Negative Breast Cancer (TNBC), requiring advanced tissue-based biomarker testing for accurate diagnosis and treatment selection. Technologies such as genomic testing, immunohistochemistry, and in situ hybridization are widely utilized to evaluate tumor characteristics and guide targeted therapies. In addition, continuous advancements in companion diagnostics, biomarker discovery, and AI-enabled pathology solutions are further improving diagnostic precision and supporting personalized treatment strategies in breast cancer management.

The non-small cell lung cancer (NSCLC) segment is expected to grow significantly over the forecast period, driven by the rising global burden of lung cancer and the increasing demand for precision oncology diagnostics. NSCLC is the most common form of lung cancer and includes adenocarcinoma, squamous cell carcinoma, and large cell carcinoma subtypes. According to the American Cancer Society, lung cancer accounts for approximately 13% of all new cancer cases. The growing prevalence of NSCLC is increasing demand for tissue-based biomarker testing, companion diagnostics, and molecular pathology solutions to support targeted therapy selection and personalized treatment approaches. Since NSCLC diagnosis primarily relies on biopsy-based tissue analysis, technologies such as immunohistochemistry, in situ hybridization, and molecular diagnostics are critical for disease detection and tumor profiling. In addition, increasing research and development activities focused on novel biomarker assays, targeted therapies, and AI-enabled pathology tools are expected to create substantial growth opportunities within the segment.

End Use Insights

The hospitals segment dominated the market, accounting for the largest revenue share of 37.74% in 2025, driven by the increasing adoption of advanced cancer diagnostic technologies across hospital-based pathology laboratories. Hospitals are increasingly utilizing tissue diagnostics solutions, including immunohistochemistry, molecular pathology, digital pathology, and in situ hybridization, to support accurate disease diagnosis, biomarker analysis, and personalized treatment planning. The growing shift from conventional diagnostic procedures to automated tissue-based testing is improving turnaround times, workflow efficiency, and diagnostic accuracy. Rising cancer prevalence, increasing biopsy volumes, and growing demand for precision oncology are further supporting segment growth. In addition, the expanding adoption of AI-enabled pathology systems and laboratory automation technologies is strengthening hospitals' role as primary end users of tissue diagnostics solutions.

The CRO segment is expected to grow at the fastest CAGR over the forecast period, driven by its essential role in supporting pharmaceutical and biotechnology companies throughout the drug development lifecycle. CROs offer specialized services, including preclinical and clinical testing, where tissue diagnostics play a key role. They provide expert analysis using advanced technologies that may not be available in-house, ensuring high-quality and accurate data for drug development. During preclinical studies, CROs use tissue diagnostics to assess the pharmacokinetics, pharmacodynamics, and toxicity of new compounds. In contrast, in clinical trials, these diagnostics are vital for monitoring treatment effects and validating drug efficacy. In addition, CROs help pharmaceutical companies meet regulatory requirements by providing detailed tissue analyses necessary for regulatory submissions. By outsourcing tissue diagnostics to CROs, companies can enhance efficiency and cost-effectiveness, avoiding the need for significant investments in specialized equipment & technology. Overall, CROs are integral to advancing drug development, providing expert tissue diagnostics, ensuring compliance, & streamlining research processes.

Modality Insights

The clinical segment dominated the market in 2025 and is expected to register the fastest CAGR of 9.53% over the forecast period. Segment growth is primarily driven by the increasing prevalence of cancer, rising demand for precision medicine, and growing adoption of advanced diagnostic technologies across clinical laboratories and hospitals. Healthcare providers are increasingly utilizing tissue diagnostics solutions, including immunohistochemistry, molecular pathology, digital pathology, and in situ hybridization, to support accurate disease diagnosis, biomarker evaluation, and personalized treatment selection. The growing complexity of oncology cases is further increasing demand for companion diagnostics and tissue-based biomarker testing. In addition, integrating artificial intelligence and machine learning into pathology workflows is improving diagnostic accuracy, workflow efficiency, and laboratory automation. Increasing adoption of AI-enabled digital pathology platforms and automated tissue analysis systems is expected to support segment expansion throughout the forecast period further.

The pharma/CRO/research segment is experiencing significant growth, driven by rising investments in precision oncology, biomarker discovery, and targeted drug development. Pharmaceutical companies and contract research organizations are increasingly adopting advanced tissue diagnostics technologies to support translational research, clinical trials, and the development of companion diagnostics. The growing demand for biomarker-based therapies is accelerating the adoption of digital pathology, multiplex immunohistochemistry, molecular tissue analysis, and AI-enabled image interpretation platforms. These technologies enable detailed evaluation of cellular interactions and improve research efficiency in oncology studies. In addition, the shift toward personalized medicine is increasing the need to identify tissue-based biomarkers and predict therapeutic response. For instance, in June 2024, Tempus AI collaborated with Pathos AI to strengthen AI-driven molecular and pathology data analysis for oncology drug development and precision medicine research.

Regional Insights

North America Tissue Diagnostics Market Trends

North America tissue diagnostics market dominated the global industry, accounting for the largest revenue share of over 44% in 2025, driven by the increasing prevalence of cancer and growing demand for advanced diagnostic technologies across hospitals, pathology laboratories, and cancer research institutes. The rising adoption of precision oncology and companion diagnostics is driving the use of tissue-based biomarker testing, immunohistochemistry, molecular pathology, and digital pathology solutions across the region. In addition, strong healthcare infrastructure, high healthcare expenditure, and favorable reimbursement frameworks are supporting the adoption of advanced tissue diagnostics platforms. The presence of major market participants, continuous technological advancements, and increasing investments in oncology research are further contributing to regional market growth. Growing integration of artificial intelligence-enabled pathology workflows and laboratory automation technologies is also improving diagnostic accuracy, workflow efficiency, and clinical decision-making across healthcare settings in North America.

U.S. Tissue Diagnostics Market Trends

The tissue diagnostics market in the U.S. is expected to grow significantly over the forecast period, driven by the rising prevalence of cancer and the increasing demand for precision oncology and early disease detection solutions. According to the American Cancer Society, approximately 2.04 million new cancer cases and 618,120 cancer-related deaths were projected in the U.S. in 2025. Breast cancer remains highly prevalent, with nearly one in eight women expected to develop invasive breast cancer during their lifetime. The increasing cancer burden is accelerating the adoption of tissue diagnostics technologies, including immunohistochemistry, molecular pathology, digital pathology, and companion diagnostics. In addition, advancements in AI-enabled image analysis, automated tissue analysis systems, and digital pathology platforms are improving diagnostic efficiency and supporting personalized treatment planning across hospitals and pathology laboratories nationwide.

Europe Tissue Diagnostics Market Trends

The tissue diagnostics market in Europe is expected to witness significant growth during the forecast period, driven by increasing cancer prevalence, rising demand for precision oncology, and continuous advancements in diagnostic technologies. Healthcare providers across the region are increasingly adopting immunohistochemistry, molecular pathology, digital pathology, and companion diagnostics solutions to improve early disease detection and personalized treatment planning. Technological advancements in artificial intelligence-enabled image analysis and digital pathology platforms are further improving diagnostic accuracy, workflow efficiency, and pathology data management across healthcare facilities. In addition, increasing oncology research funding, expanding cancer screening programs, favorable healthcare policies, and growing awareness regarding early cancer diagnosis are expected to support the adoption of advanced tissue diagnostics solutions across hospitals, pathology laboratories, and cancer research institutes throughout Europe.

The UK tissue diagnostics market is expected to grow steadily over the forecast period, driven by technological advancements, rising cancer prevalence, and increased investment in oncology research infrastructure. The rising adoption of digital pathology, molecular diagnostics, and AI-enabled tissue analysis solutions is improving diagnostic accuracy and enabling early disease detection across healthcare facilities. In addition, increasing government support and research funding are accelerating innovation in tissue diagnostics technologies. Growing emphasis on precision oncology and clinical research activities is further supporting the adoption of advanced tissue diagnostics.

The tissue diagnostics market in Germany is expected to grow over the forecast period, driven by the rising burden of cancer and the growing demand for advanced diagnostic technologies. According to the German Cancer Research Center (DKFZ), nearly 510,000 new cancer cases are diagnosed annually in Germany, highlighting the growing need for accurate and early disease diagnosis. The increasing prevalence of cancer is supporting the adoption of immunohistochemistry, molecular pathology, digital pathology, and companion diagnostics solutions across hospitals and pathology laboratories. In addition, the growing emphasis on precision oncology, expanding cancer screening programs, and continuous advancements in tissue-based biomarker analysis are further driving market growth in Germany.

Asia Pacific Tissue Diagnostics Market Trends

The tissue diagnostics market in Asia Pacific is experiencing significant growth, driven by the rising prevalence of cancer and increasing demand for advanced diagnostic technologies across countries such as China, India, Japan, and South Korea. The growing emphasis on early disease detection, precision oncology, and personalized treatment planning is accelerating the adoption of immunohistochemistry, molecular pathology, digital pathology, and companion diagnostics solutions across healthcare facilities in the region. According to the World Health Organization (WHO), the South-East Asia region reported approximately 2.4 million new cancer cases and 1.5 million cancer-related deaths in 2022, with cancer incidence and mortality projected to rise substantially by 2050. The increasing cancer burden is driving demand for advanced tissue-based diagnostic technologies that support accurate tumor identification, staging, and biomarker analysis across the Asia Pacific region.

China tissue diagnostics market is experiencing significant growth, driven by the rising burden of cancer and increasing demand for advanced diagnostic technologies. According to recent estimates from China’s National Cancer Center, approximately 5.15 million new cancer cases and 2.58 million cancer-related deaths were reported in China in 2024, highlighting the growing need for accurate and early disease diagnosis. The increasing prevalence of lung, colorectal, breast, liver, and thyroid cancers is accelerating the adoption of tissue diagnostics technologies, including immunohistochemistry, molecular pathology, digital pathology, and companion diagnostics across hospitals and pathology laboratories. In addition, expanding healthcare infrastructure, increasing oncology research investments, and growing focus on precision oncology and biomarker-based testing are further supporting market growth in China.

Latin America Tissue Diagnostics Market Trends

The tissue diagnostics market in Latin America is expected to witness steady growth during the forecast period, driven by increasing healthcare investments, rising cancer prevalence, and growing demand for accurate diagnostic technologies. Healthcare providers across the region are increasingly adopting immunohistochemistry, molecular pathology, digital pathology, and companion diagnostics solutions to support early disease detection and personalized treatment planning. In addition, market participants are expanding their regional presence through strategic partnerships, collaborations, and distribution agreements with local healthcare institutions and diagnostic laboratories. These initiatives are supporting the localization of advanced tissue diagnostics technologies and improving accessibility to modern diagnostic solutions across the region. Growing awareness of cancer screening, improving healthcare infrastructure, and increasing focus on precision oncology are further driving market growth across Latin America.

Middle East and Africa Tissue Diagnostics Market Trends

The tissue diagnostics market in the Middle East & Africa is experiencing notable growth, driven by rising cancer prevalence, improved healthcare infrastructure, and increased investments in diagnostic innovation across the region. Growing adoption of immunohistochemistry, molecular pathology, digital pathology, and companion diagnostics solutions is supporting early disease detection and precision oncology applications. Start-ups and emerging healthcare technology companies are also playing an important role in market development by introducing innovative diagnostic platforms and AI-enabled pathology solutions. For instance, in May 2023, Moroccan healthtech company DataPathology secured USD 1 million in funding from the Azur Innovation Fund to support the development of digital pathology and AI-driven cancer diagnostic solutions aimed at improving access to cancer diagnosis across underserved regions in Africa. In addition, increasing government initiatives, expanding healthcare investments, and rising focus on oncology research are further supporting the adoption of advanced tissue diagnostics technologies throughout the Middle East & Africa region.

Key Tissue Diagnostics Company Insights

Key players operating in the tissue diagnostics market are undertaking various initiatives to strengthen their market presence and increase the reach of their technology and services. Strategies such as expansion activities and partnerships are playing a key role in propelling the market growth.

Key Tissue Diagnostics Companies:

The following key companies have been profiled for this study on the tissue diagnostics market.

- F. Hoffmann-La Roche Ltd.

- Abbott Laboratories

- Thermo Fisher Scientific Inc.

- Siemens

- Danaher

- bioMérieux SA

- QIAGEN

- BD

- Merck KGaA

- GE Healthcare

- BioGenex

- Cell Signaling Technology, Inc.

- Bio SB

- DiaGenic ASA

- Agilent Technologies

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: F. Hoffmann-La Roche Ltd. - Focus on integrated diagnostic ecosystems combining instruments, reagents, consumables, and software platforms.

- Expansion through acquisitions, partnerships, and regulatory approvals to strengthen oncology and companion diagnostics portfolios.

- Investments in automation, digital pathology, and AI-enabled workflow solutions to improve laboratory efficiency.

- Strong global presence and extensive installed base across hospitals and pathology laboratories.

- Broad and clinically validated product portfolios supporting multiple tissue diagnostics applications.

- High R&D capabilities and regulatory expertise enabling continuous product innovation and commercialization.

- High instrument and testing costs are limiting adoption in price-sensitive markets.

- Longer product development and approval timelines due to regulatory complexity.

- Dependence on proprietary platforms reduces flexibility for laboratory customization.

Emerging Players: BioGenex - Focus on niche biomarker assays and specialized pathology solutions.

- Expansion through collaborations, regional partnerships, and targeted market penetration.

- Development of cost-effective and customizable tissue diagnostics products for mid-sized laboratories.

- Higher flexibility and adaptability to evolving biomarker and oncology testing needs.

- Ability to provide specialized and customized diagnostic solutions.

- Lower-cost product offerings supporting adoption among smaller laboratories and research centers.

- Limited global reach and lower brand recognition compared to established companies.

- Smaller financial capacity for large-scale R&D and commercialization activities.

- Dependence on external partnerships for distribution and market expansion.

Recent Developments

-

In May 2026, Roche entered into a definitive merger agreement to acquire PathAI, a U.S.-based digital pathology and AI-powered diagnostics company, to strengthen its digital pathology and companion diagnostics capabilities. The acquisition is expected to enhance Roche’s AI-enabled pathology workflows, biomarker discovery, and precision oncology portfolio by integrating PathAI’s advanced image management and AI analysis platform. The collaboration is also expected to support the development of novel diagnostic tools, improve laboratory efficiency, and accelerate the adoption of personalized medicine and AI-driven tissue diagnostics solutions globally.

-

In February 2024, Merck KGaA inaugurated a new $21.88 million distribution center in Cajamar, São Paulo, Brazil, aimed at improving service for its life science clients. This investment enhances Merck’s operational efficiency and responsiveness, supporting the delivery of advanced tissue diagnostics solutions to the region.

-

In January 2024, QIAGEN expanded its operations in the Middle East by opening new regional headquarters in Dubai, United Arab Emirates. This strategic move aligns with the company's goal of strengthening its presence in emerging markets and improving access to its molecular diagnostics and sample preparation technologies. The new headquarters will support key projects across healthcare, research, and industrial sectors, advancing QIAGEN's mission to grow its footprint in the region and foster local partnerships

Tissue Diagnostics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 9.4 billion

Estimated Market size in 2026

USD 10.1 billion

Projected Market size by 2033

USD 18.6 billion

Growth rate

CAGR of 9.1% from 2026 to 2033

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, modality, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

F. Hoffmann-La Roche Ltd.; Abbott Laboratories; Thermo Fisher Scientific, Inc.; Siemens; Danaher; bioMérieux SA; QIAGEN; BD; Merck KGaA; GE Healthcare; BioGenex; Cell Signaling Technology, Inc.; Bio SB; DiaGenic ASA; Agilent Technologies

Customization scope

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Tissue Diagnostics Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global tissue diagnostics market report based on technology, modality, application, end use, and region:

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Immunohistochemistry

-

Instruments

-

Slide Staining Systems

-

Tissue Microarrays

-

Tissue Processing Systems

-

Slide Scanners

-

Cell Processors

-

Microtomes

-

Embedding Systems

-

Cover Slippers

-

Other Products

-

-

Consumables

-

H&E stainer coverslipper

-

IHC stainer coverslipper

-

Antibodies

-

Other IHC reagents

-

-

-

In Situ Hybridization

-

Instruments

-

Stainers

-

Others

-

Total

-

-

Consumables

-

Software

-

-

Primary & Special Staining

-

Digital Pathology And Workflow

-

Image Analysis Informatics

-

Information Management System Storage & Communication

-

-

Anatomic Pathology

-

Instruments

-

Microtomes & Cryostat Microtomes

-

Tissue Processors

-

Automatic Strainers

-

Other Products

-

-

Consumables

-

Reagents & Antibodies

-

Probes & Kits

-

Others

-

-

-

Molecular Pathology

-

Instruments

-

Reagents

-

Fluorescence Reagents

-

Others

-

-

Others

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Breast Cancer

-

Non-small Cell Lung Cancer

-

Prostate Cancer

-

Gastric Cancer

-

Other Cancers

-

-

Modality Outlook (Revenue, USD Million, 2021 - 2033)

-

Clinical market

-

Pharma / CRO / Research market

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Diagnostic Center

-

Pharmaceutical Organizations

-

Contract Research Organizations (CROs)

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

Spain

-

France

-

Italy

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-matrix analysis across cancer type, product category, and technology

Developed a multi-layered cross-matrix integrating cancer indication (breast, lung, colorectal, prostate, hematologic cancers), product type (instruments, consumables, antibodies, probes), and technology platform (IHC, ISH, digital pathology, NGS-based tissue diagnostics).

Enabled identification of high-growth technology and cancer segments with stronger adoption potential across pathology workflows.

Comparative assessment of IHC, ISH, and molecular tissue diagnostics

Conducted side-by-side benchmarking of immunohistochemistry, in situ hybridization, and molecular pathology workflows across sensitivity, specificity, turnaround time, scalability, and clinical utility.

Helped clients evaluate technology transition trends and prioritize high-value diagnostic platforms.

Competitive benchmarking of tissue diagnostic companies

Benchmarked global and regional players based on product portfolio, companion diagnostic capabilities, automation integration, digital pathology presence, pricing, and regulatory approvals.

Supported strategic positioning, partnership evaluation, and competitive differentiation planning.

Workflow transition analysis from manual to automated pathology

Evaluated the migration trend from conventional/manual histopathology workflows toward fully automated staining and digital pathology solutions.

Highlighted workflow efficiency opportunities and automation-driven market expansion areas.

Cross-segment analysis by end user and testing setting

Developed mapping across hospitals, reference laboratories, cancer research institutes, and academic centers by testing modality and workflow adoption.

Provided visibility into high-value customer segments and technology penetration trends.

Frequently Asked Questions About This Report

Key factors that are driving the market growth include rising global burden of cancer primarily drives market growth, the growing adoption of precision oncology, and continuous advancements in tissue-based diagnostic technologies.

The global tissue diagnostics market was valued at USD 9.4 billion in 2025 and is expected to reach USD 10.1 billion in 2026.

The breast cancer segment held the largest revenue share in 2025.

The hospitals segment dominated the market, accounting for the largest revenue share of 37.7% in 2025.

The clinical market segment held the largest market share in 2025.

Some of the key participants in the global tissue diagnostics market include F. Hoffmann-La Roche Ltd.; Abbott Laboratories; Thermo Fisher Scientific, Inc.; Siemens; Danaher; bioMérieux SA; QIAGEN; BD; Merck KGaA; GE Healthcare; BioGenex; Cell Signaling Technology, Inc.; Bio SB; DiaGenic ASA; Agilent Technologies, among others.

North America dominated the tissue diagnostics market with the largest revenue share of 44.6% in 2025.

Asia Pacific is the fastest growing regional market and is projected to lead the regional market.

In 2025, the immunohistochemistry segment accounted for the largest revenue share of 25.9%.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Share this report with your colleague or friend.

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.