- Home

- »

- Homecare & Decor

- »

-

Trash Bin Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Trash Bin Market (2026 - 2033)Report]()

Trash Bin Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Manual Bins, Smart IoT-enabled Bins, Compactor Bins), By Material (Plastic, Metal), By End Use (Residential, Commercial), By Distribution Channel, By Region, And Segment Forecasts

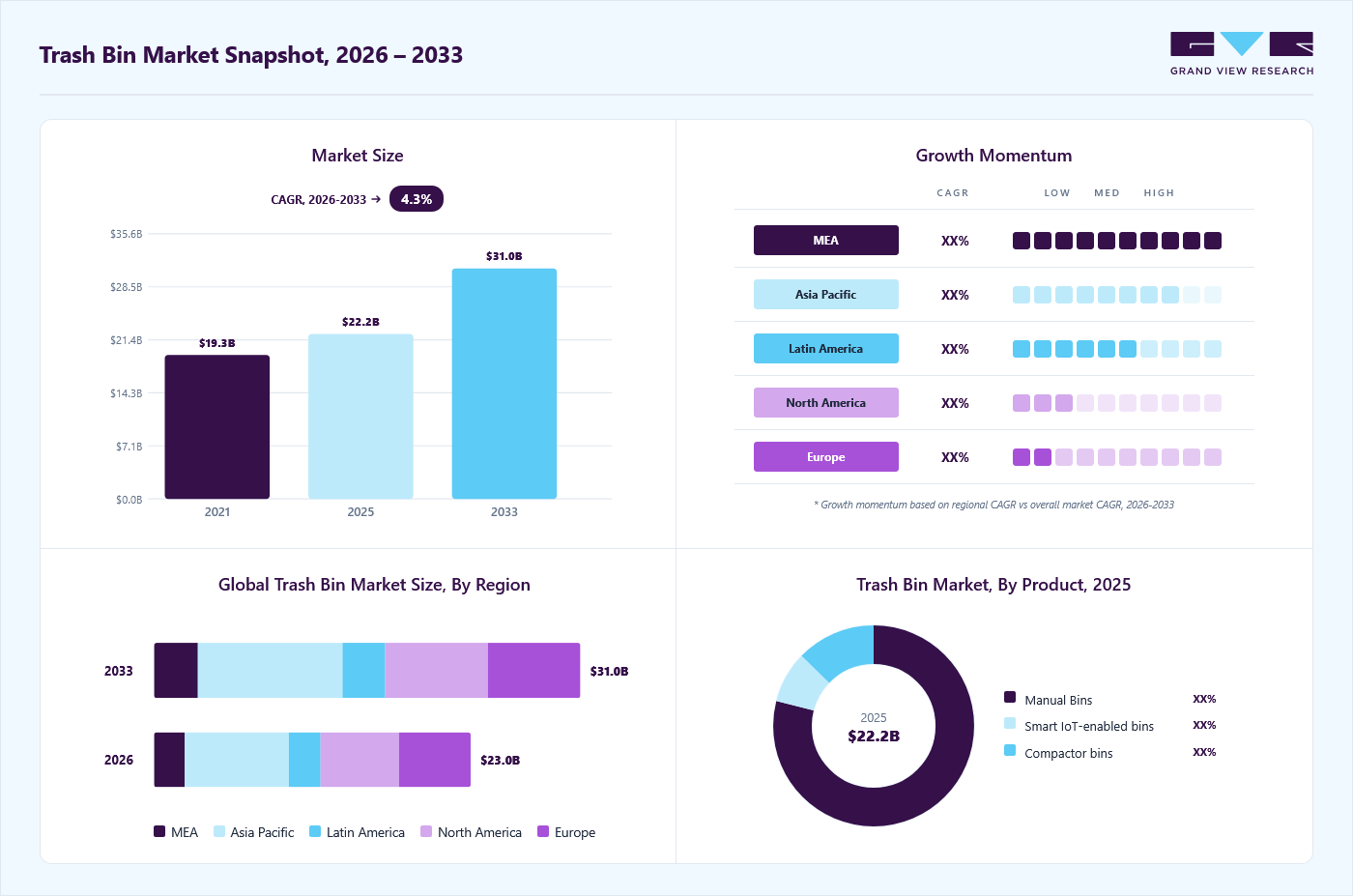

Market Size, 2025

$22.2BMarket Estimate, 2026

$23.0BMarket Forecast, 2033

$31.0BCAGR, 2026–2033

4.3%Trash Bin Market Summary

The global trash bin market size was valued at USD 22.2 billion in 2025 and is projected to grow from USD 23.0 billion in 2026 to USD 31.0 billion by 2033, at a CAGR of 4.3% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 32.7% in 2025. Rapid expansion of apartments, gated communities, office parks, retail malls, hospitals, and hospitality assets is multiplying waste-generation points per building, directly lifting demand for multiple trash bins across kitchens, bathrooms, corridors, common areas, and outdoor zones

Key Market Trends & Insights

- By product: Manual segment held the largest market share of 78.9% in 2025.

- By material: Plastics segment held the largest market share of 62.1% in 2025.

- By end-use: Residential trash bins segment held the largest market share of 40.1% in 2025.

- By distribution channel: Direct sales segment held the largest market share of 33.8% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (32.7% revenue share, 2025)

- Fastest-growing regional market: Middle East & Africa (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 22.2 Billion

- Estimated market size in 2026: USD 23.0 Billion

- Projected market size by 2033: USD 31.0 Billion

- CAGR (2026-2033): 4.3%

As urban development becomes more vertical and space efficiency tightens, consumers and facility managers are prioritizing compact, high-capacity bin designs that fit into constrained layouts without compromising volume. This trend is driving steady new installations alongside consistent replacement demand, while also encouraging integrated kitchen waste solutions aligned with the garbage disposal unit market.Regulatory pressure is a strong structural driver across residential, commercial, and public infrastructure. Municipal mandates around source segregation, recycling compliance, and hygienic waste handling are pushing housing societies, offices, schools, and public venues to move away from single-bin setups toward organized, multi-stream systems. Demand for multi-compartment, color-coded, and clearly labeled trash bins for wet, dry, recyclable, and hazardous waste is accelerating, increasing the average number of bins per site and standardizing product specifications.

")

Heightened focus on hygiene and health safety has further elevated trash bins from a low-involvement purchase to an essential household and institutional product. Post-pandemic sensitivity to cleanliness has made odor control, touchless operation, and ease of cleaning core buying criteria. Kitchens, bathrooms, healthcare facilities, and foodservice environments are increasingly adopting pedal-operated bins, sensor-based smart bins, antimicrobial plastics, and sealed-lid designs that reduce direct contact and contamination risks, reinforcing upgrade and replacement cycles.

Growth in the commercial and institutional sector continues to strengthen market momentum. Offices, airports, railway stations, shopping centers, educational campuses, and hospitality venues require large volumes of durable bins designed for high-frequency use and heavy waste loads. Facility managers prefer standardized, long-life products made from stainless steel, heavy-duty plastics, or coated metals that can withstand rough handling and repeated cleaning. This supports bulk procurement, contract-based supply, and predictable replacement demand.

Furthermore, the expansion of e-commerce and organized retail is improving product accessibility and visibility across price tiers. Online platforms enable easy comparison of sizes, materials, features, and prices, encouraging faster replacement and feature-driven upgrades. At the same time, organized retail and B2B suppliers are offering standardized waste solutions for residential projects and commercial developments, supporting structured demand growth and complementing kitchen-level waste management adoption within the garbage disposal unit market.

Brand Market Share Analysis

Manufacturers in the trash bins industry are competing in a highly fragmented environment where functionality, regulatory compliance, and scalability carry as much weight as visual design. Differentiation is increasingly driven by practical engineering, higher load-bearing capacity, weather-resistant construction for outdoor deployment, fire-retardant materials, and mobility features such as wheels for commercial and municipal use. For institutional buyers, decision-making is centered on standardization, ease of maintenance, compatibility with existing waste collection systems, and long service life. This is pushing suppliers toward robust, specification-led product portfolios rather than purely decorative offerings, aligning trash bins more closely with structured waste infrastructure requirements seen across the garbage disposal unit market.

Competitive strategies are also evolving around portfolio depth and channel focus. Larger players are expanding tiered product lines across economy, mid-range, and premium segments to serve households, offices, hospitality venues, and public infrastructure projects simultaneously. Meanwhile, smaller and emerging brands are leveraging contract manufacturing, private labeling, and faster design iteration cycles to address niche or project-based demand quickly. Established manufacturers are countering this with investments in logistics reliability, customization capability, and after-sales service, using long-term B2B contracts and institutional relationships to defend volume and margin stability.

Consumer Insights for Trash Bin

Buyers are evaluating products based on functional efficiency, spatial compatibility, and ease of integration within existing interiors. Storage capacity, internal layout, lid mechanisms, and ease of access are key decision factors, particularly in kitchens, bathrooms, and utility areas where space constraints are common. There is a growing preference for trash bins that can be easily positioned, moved, or replaced without altering surrounding fixtures, reflecting a shift toward flexible solutions that support changing household and workplace needs. Material performance is also under scrutiny, with consumers favoring bins that resist moisture, odors, and daily wear in high-use environments.

Purchasing behavior is being driven more by renovation and interior refresh cycles than by new construction alone. Homeowners and commercial operators are upgrading trash bins to modernize spaces without undertaking major structural changes, increasing demand for products that fit seamlessly into existing layouts while delivering visible aesthetic improvement. This has elevated the importance of finishes, surface textures, and color coordination, with buyers often relying on in-store displays, online configurators, and visual references to assess how trash bins will complement flooring, cabinetry, and lighting. As a result, trash bins are increasingly treated as deliberate interior elements rather than background utilities.

Product Insights

Manual bins accounted for a share of 78.94% of the global revenue in 2025, supported by their widespread adoption across residential and commercial settings due to affordability, ease of use, and minimal maintenance requirements. Demand has been particularly strong in urbanizing markets where apartment living and compact kitchen layouts are driving the need for practical, space-efficient waste solutions. Consumers are increasingly opting for manual bins equipped with user-friendly features such as soft-close lids, pull-out mechanisms, and organized internal compartments to enhance day-to-day convenience.

Smart IoT-enabled bins are projected to grow at a CAGR of 8.2% from 2026 to 2033, driven by increasing adoption of connected and automated home solutions. Rising urbanization and smaller living spaces are encouraging consumers and facility managers to invest in trash bins that offer features such as fill-level monitoring, touchless operation, odor control, and usage alerts to maintain cleaner and more efficient environments. These solutions are gaining traction across residential, commercial, and public settings where hygiene, convenience, and operational efficiency are critical.

Demand for smart bins is further supported by growth in residential construction and large-scale commercial developments, including apartments, offices, airports, and shopping centers, where standardized layouts and centralized waste management systems benefit from connected infrastructure. Municipalities and facility operators are increasingly adopting IoT-enabled bins to optimize collection schedules, reduce overflow, and lower maintenance costs.

Material Insights

Trash bins made out of plastic accounted for a share of around 62.14% of the global revenue in 2025. Plastic bins offer a favorable balance between durability and price, making them the preferred choice for mass deployment in apartments, offices, schools, hospitals, and municipalities where frequent replacement and standardized specifications are required. Their lightweight construction simplifies handling, transportation, and installation, while compatibility with automated waste collection systems and wheeled configurations supports use in high-traffic environments.

Metal trash bins are projected to grow at a CAGR of 5.4% from 2026 to 2033, driven by expanding demand across commercial, institutional, and residential applications. Rapid urban development and rising investment in offices, healthcare facilities, retail outlets, foodservice kitchens, and industrial environments are increasing the need for durable waste solutions that can withstand heavy use. Metal trash bins are widely preferred in these settings due to their structural strength, hygiene advantages, and long service life, particularly in locations with strict cleanliness and safety standards.

End User Insights

Residential trash bins accounted for a share of around 40.07% of the global revenue in 2025. Households generate consistent, high-frequency waste across kitchens, bathrooms, and utility areas, which increases wear, odor buildup, and hygiene concerns over time, prompting regular upgrades of trash bins even without major renovations. As living standards rise, homeowners are placing greater emphasis on cleanliness, ease of waste segregation, and clutter reduction, leading to higher adoption of covered, pedal-operated, and multi-compartment bins designed specifically for residential use.

Trash bins used in the municipal/public sector are projected to grow at a CAGR of 5.6% from 2026 to 2033, driven by expanding investments in urban cleanliness, waste management infrastructure, and public health initiatives. Governments and local authorities are increasing the installation of trash bins in high-visibility areas such as streets, public parks, transit corridors, educational campuses, and government buildings to manage rising waste volumes and reduce littering. Population growth in urban centers and higher daily footfall in public spaces are reinforcing the need for durable, high-capacity bins that can operate reliably under continuous outdoor use.

Distribution Channel Insights

Direct sales of trash bins accounted for a share of around 33.84% of the global revenue in 2025. Purchasing directly from manufacturers or authorized suppliers allows buyers to select specific sizes, materials, and functional features that match existing layouts and usage needs, without relying on bundled or contractor-driven procurement. This is especially relevant in kitchens, bathrooms, offices, and utility areas where precise fit, capacity, and placement matter, making direct purchasing a practical choice during minor upgrades and routine replacements.

Sales of trash bins through e-commerce are projected to grow at a CAGR of 5.5% from 2026 to 2033, driven by increasing preference for online procurement across both residential and commercial buyers. Digital platforms enable consumers, contractors, and facility managers to compare specifications, sizes, materials, and prices efficiently, supporting informed purchasing decisions without the need for physical store visits. The availability of detailed product visuals, installation guides, and customer reviews is further accelerating online adoption, particularly for standardized and modular trash bin designs.

E-commerce demand is also being supported by renovation-led purchasing and small- to mid-scale construction projects, where buyers seek faster delivery and flexible ordering rather than bulk offline procurement. Developers and property owners increasingly rely on online channels for sourcing trash bins that offer consistent quality, factory-finished surfaces, and predictable installation requirements.

Regional Insights

North America trash bin market accounted for a share of 24.90% of the global revenue in 2025. The region has a large stock of aging residential and commercial buildings, where trash bins are routinely replaced during kitchen, bathroom, and utility-area refurbishments. High renovation frequency in the U.S. and Canada, combined with widespread adoption of modular kitchens and standardized cabinetry dimensions, has made built-in and pull-out trash bins a default specification in both retrofit and new-fit projects. In addition, strict hygiene norms in offices, healthcare facilities, foodservice outlets, and public buildings drive regular replacement of trash bins to meet cleanliness and compliance standards, sustaining consistent demand across residential and non-residential applications.

U.S. Trash Bin Market Trends

The trash bin market in the U.S. is projected to grow at a significant CAGR from 2026 to 2033. U.S. households, offices, healthcare facilities, and foodservice operators require durable, hygienic trash bins capable of handling frequent daily use, which supports steady replacement and volume demand. In addition, federal and local waste management regulations, along with growing emphasis on waste segregation and recycling, are increasing demand for standardized, multi-bin, and clearly labeled trash bin solutions.

Europe Trash Bin Market Trends

The trash bin market in Europe accounted for a share of 22.72% of the global revenue in 2025, driven by strict waste segregation regulations, high recycling compliance, and strong municipal waste management frameworks across the EU. Mandatory source separation of waste in residential, commercial, and public spaces is increasing demand for multi-compartment, color-coded, and standardized trash bins across households, offices, transport hubs, and public infrastructure. In addition, European buyers prioritize long service life, material efficiency, and compliance with environmental standards, supporting demand for metal and high-grade plastic bins designed for repeated use and low maintenance.

Asia Pacific Trash Bin Market Trends

The trash bin market in Asia Pacific accounted for a share of 32.75% of the global revenue in 2025. Rapid population concentration in cities is increasing daily solid waste volumes in residential, commercial, and public spaces, driving sustained demand for basic, durable trash bins across households, offices, transport hubs, and institutional facilities. In addition, stricter enforcement of waste segregation policies in countries such as China, Japan, South Korea, and parts of Southeast Asia is accelerating the adoption of multi-bin and color-coded trash bin systems.

Central & South America Trash Bin Market Trends

The trash bin market in Central & South America is projected to grow at a CAGR of 4.4% from 2026 to 2033, driven by rising urban density and the need for practical waste handling solutions in compact residential layouts. Increasing solid waste generation in major cities is pushing households, residential complexes, and local authorities to adopt standardized and space-efficient trash bins suited for apartments and multi-family housing. In addition, the gradual formalization of waste collection systems and improved access to organized retail are expanding the availability of durable, affordable trash bins across the region. Local manufacturing and region-specific product sizing are further supporting adoption by aligning cost structures and functionality with regional usage patterns.

Middle East & Africa Trash Bin Market Trends

The trash bin market in the Middle East & Africa is projected to grow at a CAGR of 5.2% from 2026 to 2033. Growth in planned residential communities, large-scale housing projects, and mixed-use developments is increasing baseline demand for trash bins across apartments, villas, and shared facilities. In parallel, government-led urban development programs and sanitation initiatives are driving the installation of standardized trash bins in public spaces, commercial buildings, and residential compounds. Strong demand from the Gulf region for durable, high-capacity bins suited to hot climates, along with increasing adoption of organized waste management practices in parts of Africa, is sustaining steady market growth across the region.

Key Trash Bin Companies Insights

Key players operating in the trash bin market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key Trash Bin Companies:

The following key companies have been profiled for this study on the trash bin market.

- Simplehuman

- Brabantia

- Rubbermaid Commercial Products

- Joseph Joseph

- IKEA

- Hailo-Werk Rudolf Loh GmbH & Co. KG

- Rev-A-Shelf LLC

- Hettich Holding GmbH & Co. oHG

- Blanco GmbH + Co KG

- iTouchless Housewares

Recent Developments:

-

In December 2025, Mill and Amazon partnered to roll out an industry-first food waste solution at select Whole Foods Market stores. Under the initiative, Mill’s smart food waste technology was installed in participating locations to process food scraps on-site, converting organic waste into a dehydrated output that could be composted or repurposed. The program enabled Whole Foods to track and manage food waste more efficiently while reducing landfill disposal, supporting the retailer’s broader sustainability and waste-reduction goals within its store operations.

-

In April 2025, Mill, a sustainability tech company based in California, has reached over USD 20 million in revenue and is expanding its product line with a smart food waste recycling bin aimed at workplaces. Designed to help businesses reduce organic waste, the system uses sensors and technology to convert food scraps into dehydrated material that can be composted or reused, while also providing data and reporting features for corporate sustainability tracking.

Trash Bin Market Report Scope

Report Attribute

Details

Market size in 2025

USD 22.2 billion

Estimated market size in 2026

USD 23.0 billion

Projected market size by 2033

USD 31.0 billion

Growth rate

CAGR of 4.3% from 2026 to 2033

Actuals

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, material, end use, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; U.K.; France; Italy; Spain: China; Japan; India; South Korea; Australia & New Zealand; Brazil; South Africa

Key companies profiled

Simplehuman; Brabantia; Rubbermaid Commercial Products; Joseph Joseph; IKEA; Hailo-Werk Rudolf Loh GmbH & Co. KG; Rev-A-Shelf LLC; Hettich Holding GmbH & Co. oHG; Blanco GmbH + Co KG; iTouchless Housewares

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Trash Bin Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis of the latest trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global trash bins market report on the basis of product, material, end user, distribution channel, and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Manual Bins

-

Smart IoT-enabled bins

-

Compactor bins

-

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic

-

Metal

-

Wood

-

Other

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Residential

-

Commercial

-

Industrial

-

Municipal/Public Sector

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Direct Sales

-

Supermarkets/Hypermarkets

-

Wholesaler/Distributors

-

Home Improvement Stores

-

E-commerce

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia & New Zealand

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

-

Frequently Asked Questions About This Report

The global trash bin market size was estimated at USD 22.2 billion in 2025 and is expected to reach USD 23.0 billion in 2026.

The global trash bin market is expected to grow at a compound annual growth rate of 4.3% from 2026 to 2033 to reach USD 31.0 billion by 2033.

The manual segment led with a 78.9% revenue share in 2025.

Some key players in the global trash bin market include Simplehuman; Brabantia; Rubbermaid Commercial Products; Joseph Joseph; IKEA; Hailo-Werk Rudolf Loh GmbH & Co. KG; Rev-A-Shelf LLC; Hettich Holding GmbH & Co. oHG; Blanco GmbH + Co KG; iTouchless Housewares

Key factors driving the trash bin market include rising urbanization and waste generation, increasing emphasis on cleanliness and hygiene across residential and commercial spaces, and growing adoption of organized waste segregation systems supported by municipal regulations and sustainability initiatives

The plastics segment led with a 62.1% revenue share in 2025.

The residential trash bins segment led with a 40.1% revenue share in 2025.

Direct sales segment held the largest share (over 33.0%) in 2025.

Asia Pacific dominated with a 32.7% revenue share in 2025.

About the Author(s)

Homecare & Decor Research Team

Consumer Goods · Homecare & DecorThis report was authored by the homecare & decor research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the homecare & decor segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.