- Home

- »

- Next Generation Technologies

- »

-

Used Car Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Used Car Market (2026 - 2033)Report]()

Used Car Market (2026 - 2033)

Size, Share & Trends Analysis Report By Vehicle Type (Hybrid, Conventional), By Vendor Type (Organized, Unorganized), By Fuel Type (Diesel, Petrol), By Size (Compact Car, Mid-Sized, SUV), By Sales Channel (Offline), By Region, And Segment Forecasts

Market Size, 2025

$2,022.7BMarket Estimate, 2026

$2,155.0BMarket Forecast, 2033

$3,122.1BCAGR, 2026–2033

5.4%Used Car Market Summary

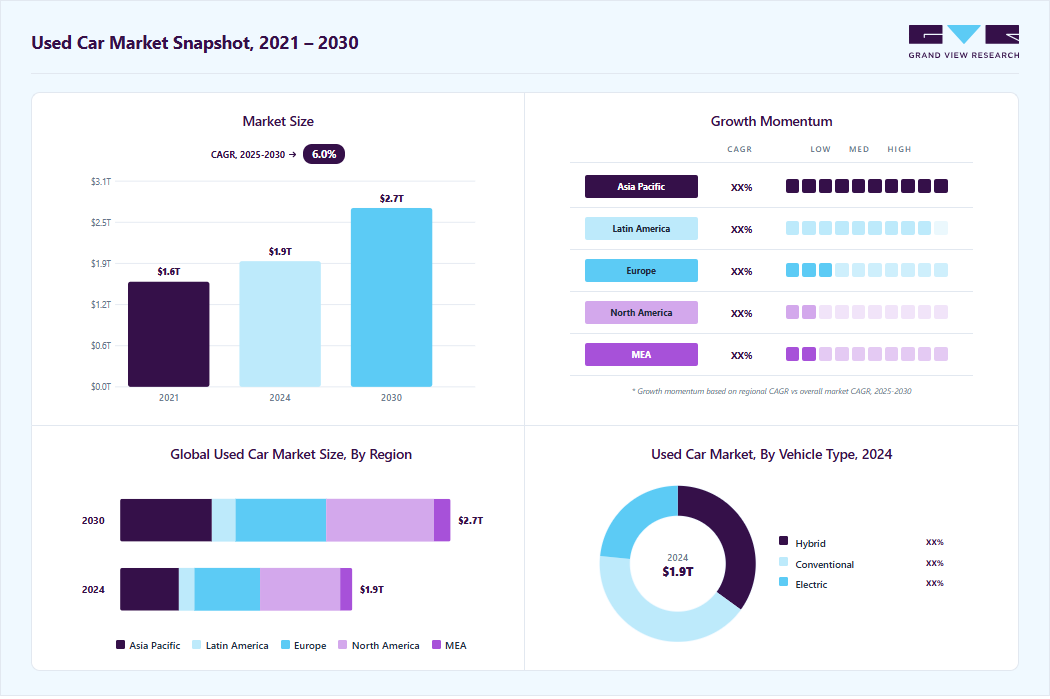

The global used car market size was valued at USD 2,022.7 billion in 2025 and is projected to grow from USD 2,155.0 billion in 2026 to USD 3,122.1 billion by 2033, at a CAGR of 5.4% from 2026 to 2033. North America dominated the global market with the largest revenue share of 34.2% in 2025. The market growth is driven by a sharp consumer shift toward organized digital platforms and certified pre-owned networks that offer transparency, safety warranties, and fair AI-driven pricing.

Key Market Trends & Insights

- By vehicle type: Conventional segment held the largest market share of 41% in 2025.

- By vendor type: Organized segment dominated the market, with a revenue share of 75.5% in 2025.

- By fuel type: Petrol segment held the largest revenue share in 2025.

- By size: Mid-sized segment held the largest revenue share in 2025.

- By sales channel: Offline segment accounted for the largest revenue share of 71.4% in 2025.

Regional Highlights

- Largest regional market: North America (34.2% revenue share, 2025)

- Fastest growing regional market: Asia Pacific (highest CAGR, 2026–2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 2,022.7 Billion

- Estimated market size in 2026: USD 2,155.0 Billion

- Projected market size by 2033: USD 3,122.1 Billion

- CAGR (2026-2033): 5.4%

The market has been experiencing significant growth, driven by various factors, including economic shifts, changing consumer preferences, and advancements in technology. As new car prices rise, many buyers are turning to used cars as a more affordable alternative. This trend is particularly evident in the aftermath of the COVID-19 pandemic, which disrupted supply chains and led to inventory shortages in new car dealerships. As a result, the demand for used vehicles has surged, with consumers seeking reliable options that fit their budgets. Moreover, the rise of remote work and lifestyle changes has influenced purchasing decisions, prompting people to seek vehicles that cater to their new routines. The increasing availability of online platforms for buying and selling used cars has also made the process more convenient, allowing consumers to access a wider range of options.")

Technological advances are transforming the market. Online marketplaces and digital platforms have emerged as vital tools for both buyers and sellers, streamlining the purchasing process. Consumers can now browse vast inventories, read reviews, and compare prices with just a few clicks, making informed decisions without the need to visit multiple dealerships. Furthermore, technologies like vehicle history reports, virtual inspections, and augmented reality tools enhance transparency and build trust in the buying process. These innovations have contributed to increased consumer confidence, leading to more people considering used cars as viable options. Moreover, data analytics helps dealers optimize inventory management and pricing strategies, further enhancing market efficiency. As technology continues to evolve, the market is expected to benefit from ongoing innovations that improve the overall buying experience.

The growth of the market also reflects changing attitudes toward vehicle ownership and sustainability. Many consumers are now prioritizing the environmental impact of their purchasing decisions, leading to a preference for used vehicles as a more sustainable choice. Buying a used car often results in a smaller carbon footprint compared to purchasing a new vehicle, as it extends the lifecycle of existing cars and reduces waste. Furthermore, automakers are increasingly focusing on producing durable and long-lasting vehicles, which aligns with consumers' desires for sustainability. This shift is accompanied by a growing awareness of the benefits of reducing waste and conserving resources. As a result, the used car market is likely to continue expanding as more people embrace eco-friendly choices in their vehicle purchases.

Market Dynamics

The used car market is being driven by rising new vehicle prices, which are pushing cost-conscious consumers toward pre-owned alternatives that offer better value for money. Increasing availability of certified pre-owned vehicles, along with improved vehicle inspection and warranty programs, has strengthened buyer confidence and reduced perceived purchasing risks. Additionally, ongoing supply constraints in new vehicle production and longer vehicle ownership cycles continue to sustain strong demand for quality used cars across both developed and emerging markets.

The rising affordability of pre-owned vehicles compared to new cars is a major factor accelerating the growth of the used car market. Consumers, particularly first-time buyers and middle-income households, are increasingly choosing used vehicles due to their lower purchase prices, reduced insurance premiums, and slower depreciation rates. This cost advantage enables buyers to access higher vehicle segments and advanced features at comparatively lower budgets.

Additionally, the increasing availability of flexible financing options and low down-payment schemes has improved accessibility to used vehicles across urban and semi-urban regions. Certified inspection programs and warranty-backed offerings are also improving buyer confidence, reducing concerns regarding vehicle reliability and maintenance costs. As consumers become more value-conscious, the demand for affordable and dependable transportation continues to expand steadily. This trend is particularly strong among young professionals and families seeking economical mobility solutions.

The growing age of used vehicles often results in higher maintenance and repair requirements, creating a major restraint for the used car market. Older vehicles are more prone to component wear, engine issues, transmission failures, and frequent part replacements, increasing the overall cost of ownership for buyers. Consumers purchasing budget-friendly used cars may initially benefit from lower upfront costs, but unexpected repair expenses can reduce long-term affordability. In addition, the availability and rising prices of spare parts for discontinued or older models further add to ownership challenges.

Frequent servicing requirements and uncertainty regarding the previous owner’s maintenance practices often reduce buyer confidence in older used cars. Financial institutions and warranty providers may also hesitate to support high-mileage vehicles due to increased risk of breakdowns and reduced resale value. As a result, many consumers shift preference toward newer certified pre-owned vehicles or entry-level new cars offering better warranty coverage and lower maintenance burdens. This trend limits the growth potential of older vehicle categories within the used car market.

Rising fuel prices, expanding environmental awareness, and supportive government policies encouraging low-emission transportation are accelerating interest in pre-owned electric and hybrid vehicles. Many buyers who are unable to afford new electric vehicles are turning toward used alternatives that provide lower operating and maintenance costs compared to conventional internal combustion engine vehicles. Improvements in battery durability and the availability of vehicle health diagnostics are also increasing consumer confidence in purchasing second-hand electric vehicles. In addition, the expanding charging infrastructure across urban and semi-urban regions is supporting wider acceptance of used electric and hybrid models in everyday transportation.

The opportunity is further strengthened by the increasing number of leased electric vehicles entering the resale market, improving product availability and model variety for consumers. Digital used-car platforms enhancing transparency by providing battery performance reports, ownership history, and financing solutions for electric vehicles. Growing corporate fleet transitions toward electrification are additionally contributing to supply of used electric and hybrid vehicles in secondary markets. As sustainability goals continue to influence consumer purchasing behavior, the demand for affordable pre-owned electric mobility solutions is expected to strengthen across both developed and emerging economies.

Market Concentration & Characteristics

The threat of service substitutes in the used car market is moderate as consumers increasingly explore alternative mobility solutions such as ride-sharing, vehicle subscriptions, car leasing, and public transportation. Urban consumers, particularly younger demographics, are showing rising preference for flexible transportation services over vehicle ownership. However, used vehicles continue maintaining strong demand due to affordability advantages, ownership flexibility, and expanding financing accessibility. In developing economies, personal vehicle ownership remains highly preferred, limiting the overall substitution impact.

End-user concentration in the used car market is relatively high due to broad participation from individual consumers, small businesses, ride-hailing operators, and commercial fleet buyers. Demand is widely distributed across income groups because used vehicles provide cost-effective mobility alternatives compared to new vehicles. Urbanization, rising middle-class populations, and growing first-time vehicle ownership are significantly increasing consumer demand across emerging economies. Additionally, increasing online accessibility and financing availability are expanding the customer base globally.

Analyst Perspective

The used car market benefits from a combination of economic practicality, vehicle affordability gaps, and an expanding supply of higher-quality pre-owned inventory entering the secondary market. Rising new vehicle prices, longer vehicle replacement cycles, and improved access to financing have broadened the consumer base beyond traditional budget-conscious buyers, positioning used vehicles as a mainstream mobility solution. The defining competitive advantage, however, belongs to platforms and dealerships that can integrate vehicle sourcing, inspection, certification, financing, warranty coverage, and digital transaction capabilities into a seamless ownership ecosystem.

Vehicle Type Insights

Based on vehicle type, the conventional segment led the market with the largest revenue share of 41.0% in 2025 and is expected to grow at the fastest CAGR over the forecast period, due to the established infrastructure and consumer familiarity with internal combustion engine (ICE) vehicles. Gasoline and diesel-powered cars have been the primary mode of transportation for decades, benefiting from extensive refueling networks and a broad range of available models. This dominance is further bolstered by the affordability and convenience of traditional vehicles, which have made them the default choice for many consumers. Moreover, the internal combustion engine has seen continuous improvements in fuel efficiency and performance, maintaining its appeal in a competitive market.

The electric vehicle (EV) market is experiencing rapid growth, fueled by advancements in battery technology and increasing consumer awareness of sustainability. As governments implement stricter emissions regulations and offer incentives for EV purchases, more consumers are considering electric options. The range of available EV models is expanding, catering to various preferences and budgets, which helps to attract a broader audience. Furthermore, the development of charging infrastructure is enhancing the practicality of owning an electric vehicle, making it more accessible for everyday use. This combination of factors is positioning electric vehicles as a viable alternative, contributing to their increasing share in the overall automotive market.

Vendor Type Insights

The organized segment dominated the market in 2024 by utilizing established dealerships and certified pre-owned programs, creating a structured purchasing environment for consumers. These dealerships enhance consumer confidence through various benefits, such as warranties, comprehensive vehicle history reports, and accessible financing options. By adhering to higher standards of vehicle quality and customer service, organized players offer a more reliable buying experience that attracts cautious consumers. Moreover, their compliance with regulatory requirements and safety standards fosters trust among buyers, which is crucial in the used car market.

The unorganized segment offers several benefits that attract price-sensitive consumers. This segment is characterized by individual sellers, small dealerships, and online classifieds, providing a wide variety of options at potentially lower prices. Consumers in this market can negotiate directly with sellers, often resulting in better deals and personalized service. Furthermore, the unorganized market typically features a diverse range of vehicles, including older models and unique finds that may not be available at organized dealerships. However, buyers in this segment should be cautious, as the lack of standardized quality assurance can lead to potential risks regarding vehicle reliability and transparency in vehicle history.

Fuel Type Insights

The petrol segment dominated the market in 2024 primarily due to its widespread availability and the long-standing preference among consumers for petrol-powered vehicles. Petrol cars are often perceived as more cost-effective in terms of initial purchase price and maintenance, making them a popular choice for budget-conscious buyers. Moreover, advancements in petrol engine technology have led to improved fuel efficiency and reduced emissions, which appeal to environmentally conscious consumers. The smoother driving experience and quieter operation of petrol vehicles further enhance their desirability.

The diesel segment is witnessing significant growth in the used car market, driven by increasing consumer interest in fuel efficiency and torque performance. Diesel engines are known for their superior fuel economy, making them an attractive option for buyers who drive long distances or have high mileage needs. As environmental regulations become stricter, manufacturers are focusing on producing cleaner diesel vehicles that meet modern emissions standards, helping to mitigate some of the negative perceptions associated with diesel fuel. Moreover, the growing availability of diesel models in the used car market offers buyers a wider selection of vehicles.

Size Insights

The SUV segment dominated the market in 2024. Known for their spacious interiors and higher seating positions, SUVs offer a sense of safety and comfort that many buyers prioritize. Moreover, the popularity of SUVs has led manufacturers to produce a wide variety of models, catering to different tastes and budgets. As fuel efficiency has improved in newer models, many consumers are increasingly drawn to SUVs, contributing to their market dominance. Furthermore, the lifestyle-oriented marketing strategies employed by manufacturers have successfully positioned SUVs as desirable vehicles for families and adventure-seekers alike.

The mid-sized vehicle segment is experiencing significant growth due to changing consumer preferences and increasing fuel efficiency standards. As buyers seek more affordable and economical options, mid-sized cars offer a balance of comfort, performance, and cost-effectiveness. These vehicles are often seen as ideal for urban driving, providing ample space while being easier to maneuver and park than larger SUVs. Moreover, advancements in technology and safety features have made mid-sized cars more appealing to buyers who value modern amenities. As consumers become more environmentally conscious, the growth of hybrid and electric mid-sized options further enhances their attractiveness, positioning this segment for continued expansion in the market.

Sales Channel Insights

Based on sales channel, the offline segment led the market with the largest revenue share of 71.4% in 2025. These traditional outlets offer a tangible experience, allowing customers to inspect vehicles, test drive them, and negotiate face-to-face with sellers. The personalized service and sense of security that comes with buying from a reputable dealer have contributed to the offline segment's stronghold in the market. Moreover, many buyers feel more comfortable purchasing cars through a process they can physically engage with, which has further supported offline dominance.

The online segment has been experiencing steady growth as more consumers turn to digital solutions for convenience. Online platforms provide users with a wider selection of vehicles, transparent pricing, and the ability to compare options without leaving their homes. This ease of access, coupled with advancements in technology such as virtual car tours and secure online payment systems, has boosted the appeal of buying used cars online. Consequently, while offline channels still lead, the online sector is quickly growing and changing how this market is structured.

Regional Insights

North America dominated the used car market with the largest revenue share of 34.2% in 2025. In North America, the market is expanding due to a shift in consumer preferences towards more affordable vehicle options. Economic factors, such as inflation and rising new car prices, have driven many buyers to consider used cars as a cost-effective alternative. The growing availability of certified pre-owned programs has further boosted confidence in the quality of used vehicles. Moreover, online platforms are making it easier for consumers to access a wider range of used cars, enhancing the market’s accessibility. These factors combined have led to steady growth in the region’s used car market.

U.S. Used Car Market Trends

The used car market in the U.S. held the largest share in the North America region in 2025. The used car market in the U.S. is seeing significant growth, driven by high demand for both affordable and reliable transportation. Economic uncertainty has led many consumers to seek cheaper alternatives to new vehicles, boosting sales in the used car sector. A strong focus on certified pre-owned programs by dealerships has built trust among buyers, further fueling the market. Online platforms are also contributing by making the buying process more convenient and transparent for U.S. consumers.

Europe Used Car Market Trends

The used car market in Europe is growing due to an increasing preference for fuel-efficient vehicles amid rising fuel costs and environmental concerns. The transition to electric vehicles (EVs) has also impacted the market, with many consumers opting for used EVs as a more affordable option. Regulatory incentives in certain countries further support the growth of the used car market by encouraging sustainable transportation. Online platforms have played a significant role in expanding access to a wider variety of vehicles across borders.

Asia Pacific Used Car Market Trends

The used car market in Asia Pacific is driven by a growing middle class seeking affordable transportation options. In countries with dense urban populations, used cars offer a cost-effective alternative to new vehicles, especially as vehicle ownership increases. Economic growth and rising disposable incomes are also contributing to higher demand for used cars. Moreover, online marketplaces are helping streamline the buying and selling process, attracting more consumers to the market. This, combined with the increased availability of financing options, is fueling the growth of the used car market across the region.

Key Used Car Company Insights

Some of the key companies in the used car market include Alibaba.com, CarMax Enterprise Services, LLC, Asbury Automotive Group, and others. Organizations are focusing on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions and partnerships with other major companies.

-

Alibaba.com has expanded into the used car market by utilizing its vast e-commerce platform to connect buyers and sellers. The company offers a wide range of vehicles, making use of its established logistics and payment systems for seamless transactions. Alibaba has integrated AI-driven solutions to enhance the buyer experience, including virtual tours and pricing comparisons.

-

Asbury Automotive Group is a major player in the U.S. used car market, operating an extensive network of dealerships offering a wide range of pre-owned vehicles. The company has made significant investments in digital platforms to enhance its online sales capabilities, including features like home delivery and virtual consultations. Strategic acquisitions and dealership expansions have strengthened its presence in the used car sector.

Key Used Car Companies

The following key companies have been profiled for this study on the used car market.

-

Alibaba.com.

-

CarMax Enterprise Services, LLC

-

Asbury Automotive Group

-

TrueCar, Inc.

-

Scout24 SE

-

Lithia Motor Inc.

-

Group 1 Automotive, Inc.

-

eBay.com

-

Hendrick Automotive Group

-

AutoNation.com

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: CarMax Enterprise Services, LLC; Asbury Automotive Group; Hendrick Automotive Group; Lithia Motor Inc.

- Expanding dealership networks and certified programs strengthen long-term customer retention.

- Integrating digital retailing with financing improves operational efficiency and convenience.

- Strong brand recognition and inventory scale increase customer trust significantly.

- Advanced pricing analytics and warranty services enhance competitive market positioning.

- High dealership operational costs reduce profitability during economic market slowdowns.

- Slower digital transformation limits adaptability against rapidly growing online competitors.

Emerging Players: Alibaba.com; TrueCar, Inc.; Scout24 SE; eBay.com

- Digital-first platforms and AI pricing attract technology-driven used vehicle consumers.

- Asset-light partnerships support scalable expansion with lower operational infrastructure costs.

- Strong digital capabilities simplify vehicle discovery and purchasing experiences efficiently.

- Flexible business models rapidly adapt to changing consumer market preferences.

- Limited inspection services reduce customer trust in vehicle quality assurance.

- Third-party inventory dependence affects profitability and fulfillment consistency significantly.

Recent Developments

-

In August 2024, MOTORS collaborated with Parkers, a U.K. platform for used car buyers, to expand the reach of its multisite advertising service. This collaboration aims to give dealers more visibility and offer consumers a broader selection of used cars on one of the U.K.'s most trusted automotive platforms.

-

In October 2023, TrueCar, Inc. collaborated with Car and Driver to enhance the online car shopping experience for Car and Driver's 15 million users by integrating TrueCar's platform into their model review pages. This collaboration aims to provide a seamless process for consumers while expanding visibility for TrueCar dealers and utilizing Car and Driver's comprehensive automotive content and insights.

-

In January 2023, CarMax Enterprise Services, LLC collaborated with UVeye Inc., an automatic vehicle inspection provider, to implement automated vehicle assessment technology, enhancing AI-driven condition reports for wholesale vehicle buyers at auctions. This collaboration aims to improve transparency and efficiency in the wholesale auction process by providing detailed imagery and automated inspections of vehicles.

Used Car Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2,022.7 billion

Estimated market size in 2026

USD 2,155.0 billion

Projected market size by 2033

USD 3,122.1 billion

Growth rate

CAGR of 5.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Vehicle Type, Vendor Type, Fuel Type, Size, Sales Channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; South Africa; UAE

Key companies profiled

Alibaba.com, CarMax Enterprise Services, LLC, Asbury Automotive Group, TrueCar, Inc., Scout24 SE, Lithia Motor Inc., Group 1 Automotive, Inc., eBay.com, Hendrick Automotive Group, AutoNation.com

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Used Car Market Report Segmentation

This report forecasts volume & revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global used car market report based on vehicle type, vendor type, fuel type, size, sales channel, and region:

-

Vehicle Type Outlook (Shipment, Million Units; Revenue, USD Trillion, 2021 - 2033)

-

Hybrid

-

Conventional

-

Electric

-

-

Vendor Type Outlook (Shipment, Million Units; Revenue, USD Trillion, 2021 - 2033)

-

Organized

-

Unorganized

-

-

Fuel Type Outlook (Shipment, Million Units; Revenue, USD Trillion, 2021 - 2033)

-

Diesel

-

Petrol

-

Others

-

-

Size Outlook (Shipment, Million Units; Revenue, USD Trillion, 2021 - 2033)

-

Compact Car

-

Mid-Sized

-

SUV

-

-

Sales Channel Outlook (Shipment, Million Units; Revenue, USD Trillion, 2021 - 2033)

-

Offline

-

Online

-

-

Regional Outlook (Shipment, Million Units; Revenue, USD Trillion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Vehicle Type

Revenue capture definition

Hybrid

Revenue in this segment is generated by the resale of vehicles that combine internal combustion engines with electric propulsion systems. This segment captures demand from buyers seeking improved fuel efficiency and lower operating costs.

Conventional

The conventional used car segment derives revenue from the sale of pre-owned gasoline and diesel-powered vehicles. Its revenue contribution remains significant due to the lower acquisition costs relative to alternative powertrain technologies.

Electric

Revenue in the electric used car segment is generated from battery electric vehicles (BEVs) and other fully electric pre-owned models. Market expansion is supported by increasing EV adoption, improving battery performance, and growing charging infrastructure coverage.

Segment - Vendor Type

Revenue capture definition

Organized

Organized vendors operate through standardized sales, inspection, financing, and after-sales processes. Revenue is captured from used vehicle transactions conducted through formally registered businesses, including associated services.

Unorganized

The unorganized segment functions with limited operational standardization. Revenue capture includes the value of pre-owned vehicle sales facilitated through these informal channels, excluding revenues generated by organized dealership networks and certified retail platforms.

Segment - Fuel Type

Revenue capture definition

Diesel

Revenue in the diesel segment is from the resale and trade of pre-owned diesel-powered passenger and commercial vehicles. Demand is primarily concentrated among high-mileage users and buyers seeking lower fuel costs per kilometer, particularly in long-distance travel applications.

Petrol

The petrol segment captures revenue from used gasoline-powered vehicles across hatchbacks, sedans, SUVs, and crossovers. Its contribution is supported by broad vehicle availability, lower maintenance complexity, and strong adoption in urban and suburban markets.

Others

The others segment includes used vehicles powered by alternative fuels such as CNG, LPG, hybrid, and electric powertrains. Revenue is derived from growing consumer interest in fuel efficiency, emissions reduction, and access to government-supported mobility ecosystems.

Segment - Size

Revenue capture definition

Compact

It captures revenue through high transaction volumes driven by affordability, fuel efficiency, and lower maintenance costs. Demand is among first-time buyers, urban commuters, and budget-conscious households seeking practical mobility solutions.

Mid-Sized

Revenue in this segment is generated from consumers seeking a balance between purchase cost, cabin space, comfort, and vehicle features. Its market contribution is by family buyers and professionals upgrading from entry-level vehicles.

SUV

The SUV segment accounts for a significant share due to higher ASP and sustained consumer preference for larger vehicles. Growth in this category is supported by demand for enhanced seating capacity, cargo space, driving visibility, and multi-purpose usability.

Segment - Sales Channel

Revenue capture definition

Offline

This captures revenue through franchised dealerships, independent used-car dealers, and local automotive retailers. Revenue is generated from vehicle sales, dealer margins, financing commissions, warranties, and value-added services offered at physical locations.

Online

Captures revenue from digital platforms through websites and mobile applications. Revenue is derived from vehicle transactions, platform commissions, listing fees, subscription services, advertising, and associated financing or protection products sold through digital channels.

Estimation Model

Layer Name

Key Questions

Description

Ownership Layer

Who Owns Vehicles for Resale?

Identify vehicles reaching resale age and estimate the addressable stock of vehicles - establishes the addressable base of vehicles available for used-car transactions.

Transaction Layer

How Many Vehicles Are Traded?

Apply vehicle turnover and resale rates to estimate the number of used vehicles exchanged annually through dealer, online, and private-party channels. This converts the vehicle base into active market transactions.

Channel Layer

Where Are Used Cars Sold?

Measure the distribution of transactions across organized dealerships, certified programs, online, and independent sellers. This reflects the penetration and utilization of various sales channels within the market.

Monetisation Layer

How Much Revenue Is Generated?

Apply the average transaction value per vehicle and aggregate revenues from vehicle sales, dealer margins, financing, warranties, and ancillary services to estimate total market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Entry & Expansion Assessment

Regional demand sizing and forecasting

Customer segmentation and buying behavior analysis

Competitive landscape benchmarking

Regulatory and distribution channel assessment

Identified high-growth market opportunities.

Supported go-to-market strategy development

Highlighted investment priorities and risks

Enabled data-driven expansion planning

Customer & End-User Insights Study

Consumer awareness and adoption analysis

Purchase decision journey mapping

Satisfaction and loyalty assessment

Usage pattern and pain-point evaluation

Revealed key adoption drivers and barriers

Supported customer-centric product development

Improved targeting and engagement strategy

Identified opportunities for retention and upselling

Channel Partner & Distribution Study

Dealer/distributor network analysis

Channel performance benchmarking

Margin and profitability assessment

Route-to-market evaluation

Optimized channel strategy

Identified distribution gaps

Improved partner engagement approach

Enhanced market penetration planning

Frequently Asked Questions About This Report

The global used car market size was estimated at USD 2,022.7 billion in 2025 and is expected to reach USD 2,155.0 billion in 2026.

The global used car market is expected to grow at a compound annual growth rate of 5.4% from 2026 to 2033 to reach USD 3,122.1 billion by 2033.

Asia Pacific is the fastest-growing region over the forecast period.

The Conventional segment led with a 41.0% revenue share in 2025, while Electric is the fastest growing segment.

Offline held the largest revenue share in 2025, while online is the fastest growing segment.

The Petrol segment led with a 41.8% revenue share in 2025, while Diesel is the prominent growing segment.

North America dominated the used car market with a share of 34.2% in 2025. In North America, the used car market is expanding due to a shift in consumer preferences towards more affordable vehicle options.

Some key players operating in the used car market include Alibaba.com, CarMax Enterprise Services, LLC, Asbury Automotive Group, TrueCar, Inc., Scout24 SE, Lithia Motor Inc., Group 1 Automotive, Inc., eBay.com, Hendrick Automotive Group, AutoNation.com

Key factors driving the growth of the used car market include various factors including economic shifts, changing consumer preferences, and advancements in technology. As new car prices rise, many buyers are turning to the used car market as a more affordable alternative.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.