- Home

- »

- Next Generation Technologies

- »

-

Wireless Charging Market Size, Share Report, 2023-2030GVR Report cover

![Wireless Charging Market (2023 - 2030)Report]()

Wireless Charging Market (2023 - 2030)

Size, Share & Trends Analysis Report By Component (Transmitters, Receivers), By Technology (Inductive, Resonant, RF), By Application, By End-use, By Region, And Segment Forecasts

Market Size, 2022

$5.7BMarket Estimate, 2026

$13.9BMarket Forecast, 2030

$31.6BCAGR, 2023–2030

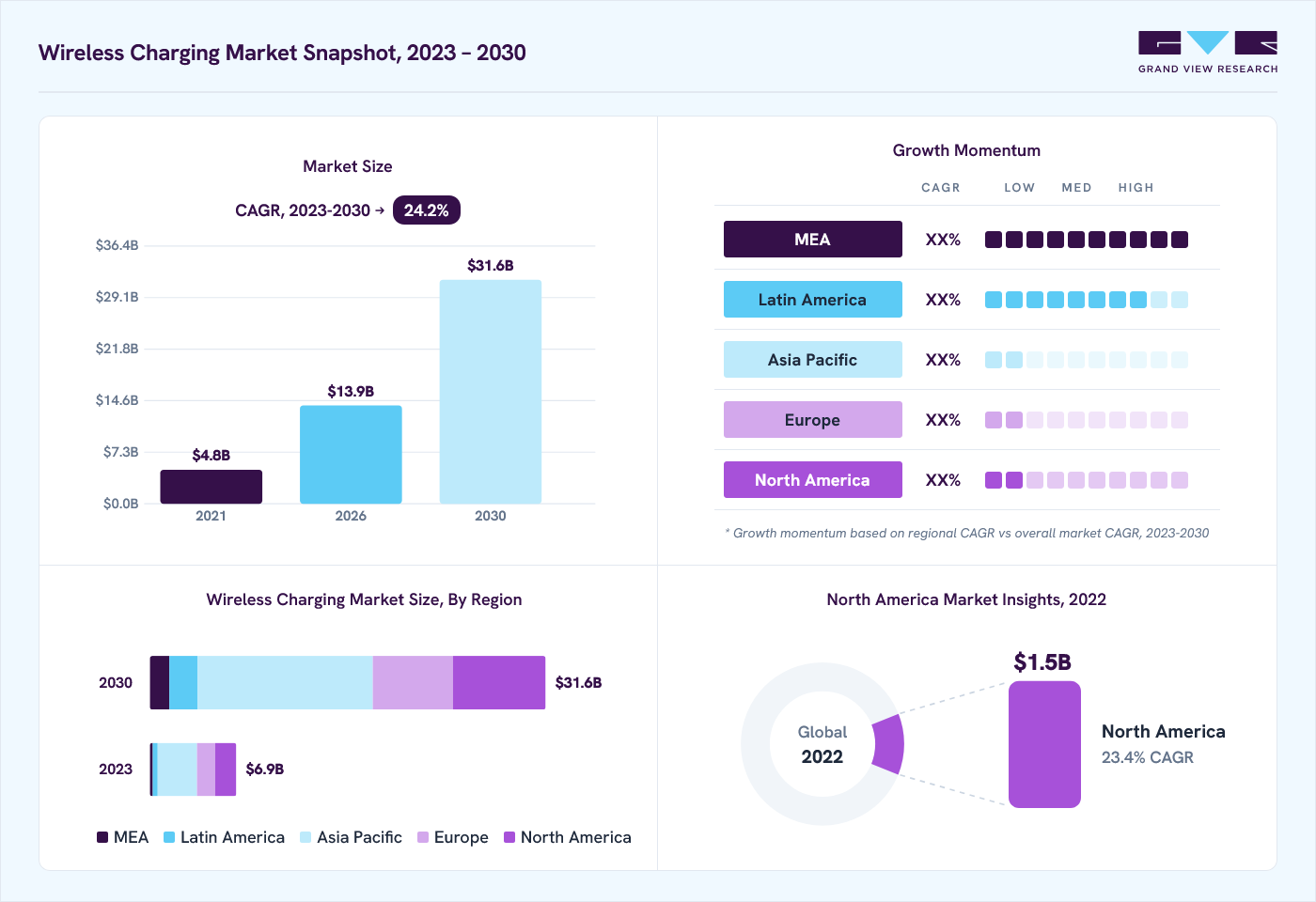

24.2%Wireless Charging Market Size & Trends

The global wireless charging market size was valued at USD 5.7 billion in 2022 and is projected to grow from USD 13.9 billion in 2026 to USD 31.6 billion by 2030, at a CAGR of 24.2% from 2023 to 2030. Asia Pacific dominated the market, accounting for a revenue share of 45.0% in 2022. The growing demand for high-speed wireless and simultaneous multi-device charging stations is expected to drive the market growth. Furthermore, the technology reduces wear and tear on device ports and connectors, leading to an extended lifespan of devices and reduces the maintenance and replacement costs, which is anticipated to fuel the demand for wireless charging market over the forecast period.

The rising adoption of electric vehicles (EVs) is generating high demand for seamless and uncomplicated charging solutions is driving the expansion of the market. The wireless technology removes the need for physical cables and connectors, providing EV owners with a considerably smoother and user-focused charging process. This convenience factor plays a major role in driving the widespread acceptance of technology, which is augmenting the robust growth of the wireless charging market.

Furthermore, key organizations are continuously working on improving the standards associated with the technology to offer enhanced user experience. For instance, in 2023, Wireless Power Consortium, Inc. (WPC) is expected to launch a new wireless charging standard with the goal of unifying the industry under a single global standard. This strategic initiative aims to enhance efficiency and convenience for wearables and mobile devices, which is expected to boost the market expansion over the forecast period.

The COVID-19 pandemic led to the subsequent lockdown restrictions and temporarily forced manufacturing units and factories to remain shut, affecting the demand and supply chain worldwide and hampering numerous industries, including semiconductor industry. However, the growing importance of contactless solutions and hygiene awareness after the pandemic is potentially driving interest in technology as a convenient and touch-free alternative. As remote work and digital connectivity increases, the reliance on devices demanding reliable power sources is expected to boost the market. Moreover, the ongoing innovation and development in the market are anticipated to propel the market growth over the forecast period.

Moreover, key market players are continuously innovating and adapting technologies to improve their product’s efficiency and performance, which is expected to drive market growth. For instance, in September 2022, Morphine, a subsidiary of ZAGG, launched its snap+ wireless charging ecosystem. These latest additions bring enhanced power solutions that provide a wireless power output of up to 15W, catering to both at-home and on-the-go multi-device charging needs. In addition, these solutions are MagSafe compatible and are also suitable for Qi-enabled smartphones. Such product introductions by market players are expected to propel the market growth over the forecast period.

Component Insights

The transmitter component segment accounted for the largest market share in 2022. This is attributed to the significant advancements in transmitter technology that have facilitated substantial improvements in power delivery, charging speed, and transmission range. These enhancements have significantly bolstered the efficiency and practicality of the technology, which is expected to drive the segment’s growth over the forecast period.

The receiver component segment is expected to register a significant CAGR of over 23% over the forecast period. This growth is attributed to an increasing number of devices, including smartphones, smartwatches, and wireless earbuds, which are integrated with wireless charging receiver components. This integration simplifies the charging process and encourages consumers to opt for wireless charging options, which is expected to drive the segment growth further.

Technology Insights

The inductive technology segment accounted for the largest market share in 2022. This is attributed to the adoption of technology along with standardization across the industry, especially with the Qi wireless charging standard. This standardization simplifies device compatibility and encourages manufacturers to integrate inductive technology into their product offerings. Moreover, the inductive technology provides the ease of effortlessly positioning devices onto charging pads, eliminating the need for complicated cable connections, which is driving the segment growth over the forecast period.

The radio frequency technology segment is expected to grow at the fastest CAGR over the forecast period. This growth is attributed to the capability of RF-based wireless charging to facilitate extended-range power transfer, surpassing the limitations of traditional inductive methods. This flexibility in device placement makes RF charging more convenient and user-friendly. In addition, the RF technology can potentially charge multiple devices simultaneously within its coverage area, which is expected to augment the segment demand over the forecast period.

Application Insights

The consumer electronics segment accounted for the largest revenue share in 2022 and is expected to continue the same trend over the forecast period. The growth of the segment is attributed to the widespread integration of the technology into smartphones, smartwatches, wireless earbuds, and various consumer electronics that has substantially augmented the potential user base. Furthermore, the growing popularity of wearables like smartwatches and wireless earbuds are expected to fuel the segment growth during the forecast period.

The defense segment is expected to grow at the fastest CAGR over the forecast period. The integration of wireless charging into the defense sector, particularly in drones and unmanned vehicles, is expected to drive the segment growth. Moreover, this innovation enables UAVs to achieve automated battery recharging upon their return to allocated charging stations. Such wireless charging functionality substantially increases operational longevity and extends mission durations, which is anticipated to fuel the segment growth over the forecast period.

The healthcare segment is expected to grow at a considerable CAGR over the forecast period. The integration of wireless charging into medical devices such as wearable health monitors, smart medical implants, and portable diagnostic equipment is driving the segment growth. Moreover, the technology enables seamless and uninterrupted power supply to devices that require constant monitoring, ensuring that critical patient data is consistently transmitted to medical professionals, which is anticipated to fuel the segment growth over the forecast period.

Regional Insights

The Asia Pacific regional market captured the highest market share of over 45% in 2022. The increasing adoption of electric vehicles (EVs) across Asia Pacific, especially in countries like China and Japan, is driving the demand for wireless charging infrastructure to support these vehicles. Moreover, the region boasts a large consumer electronics market, with countries like China, Japan, and South Korea being major players in device manufacturing, which is expected to drive the market growth across the region.

North America accounted for the second highest market share over the forecast period. This growth is attributed to the region's ongoing technological advancements along with the surge in demand for the technology, particularly within the consumer electronics and automotive sectors, propels market growth in the region. The rising reliance on electronic devices such as laptops, tablets, smartphones, and similar gadgets is expected to fuel the expansion of the throughout the forecast period.

The Middle East & Africa region is expected to grow at the highest CAGR of over 30% over the forecast period. This growth is attributed to the increasing adoption of smartphones and tablets in the region. Moreover, there is a growing awareness of the benefits of wireless charging in the region as the technology is considered to be more convenient and safer alternative to wired charging, which is expected to boost the demand for the wireless charging market over the forecast period.

Key Companies & Market Share Insights

The market is classified as highly competitive, with the presence of several market players. The key players operating in the industry are focusing on strategic alliances, product development, expansion, and mergers & acquisitions to remain competitive in the industry. For instance, in August 2023, Tesla, a U.S. based electric car company, acquired Wiferion GmbH, a specialist in wireless charging solutions. This acquisition is in line with Tesla's continuous endeavors to elevate its wireless charging solutions for electric vehicles (EVs). Such mergers & acquisitions by the ley players are anticipated to augment the market growth over the forecast period.

Key Wireless Charging Companies:

- Belkin International, Inc.

- ConvenientPower HK Ltd.

- Energous Corporation

- Ossia Inc.

- Plugless Power LLC

- Powercast Corporation

- Powermat Technologies

- Renesas Electronics Corporation

- Samsung Electronics

- Texas Instruments, Inc.

- WiTricity Corporation

Wireless Charging Market Report Scope

Report Attribute

Details

Market size in 2022

USD 5.7 billion

Estimated market size in 2026

USD 13.9 billion

Projected market size by 2030

USD 31.6 billion

Growth rate

CAGR of 24.2% from 2023 to 2030

Base year for estimation

2022

Historical data

2018 - 2021

Forecast period

2023 - 2030

Quantitative units

Revenue in USD million/billion and CAGR from 2023 to 2030

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, technology, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Germany; U.K.; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Mexico; Saudi Arabia; UAE

Key companies profiled

Samsung Electronics; Energous Corporation; Powermat Technologies; Ossia Inc.; WiTricity Corporation; Plugless Power LLC; Powercast Corporation; ConvenientPower HK Ltd.; Texas Instruments, Inc.; Semtech Corporation; Renesas Electronics Corporation; Belkin International, Inc.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Wireless Charging Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For the purpose of this study, Grand View Research has segmented the global wireless charging market report on the basis of component, technology, application, and region:

-

Component Outlook (Revenue, USD Million, 2018 - 2030)

-

Transmitters

-

Receivers

-

-

Technology Outlook (Revenue, USD Million, 2018 - 2030)

-

Inductive

-

Resonant

-

Radio Frequency

-

Others

-

-

Application Outlook (Revenue, USD Million, 2018 - 2030)

-

Automotive

-

Consumer Electronics

-

Industrial

-

Healthcare

-

Defense

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

Germany

-

U.K.

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa (MEA)

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The global wireless charging market size was valued at USD 5.7 billion in 2022 and is estimated at USD 13.9 billion for 2026.

The global wireless charging market is expected to grow at a CAGR of 24.2% from 2023 to 2030, reaching USD 31.6 billion by 2030.

Asia Pacific dominated with a revenue share of 45.0% in 2022.

Some key players operating in the wireless charging market include Belkin International, Inc., ConvenientPower HK Ltd., Energous Corporation, Ossia Inc., Plugless Power LLC, Powercast Corporation, Powermat Technologies, Renesas Electronics Corporation, Samsung Electronics, Semtech Corporation, Texas Instruments, Inc., WiTricity Corporation.

Key factors that are driving the wireless charging market growth include breakthroughs in wireless charging of medical implants, rising adoption of electric vehicles (EVs), growing demand for smartphones, and user-friendliness.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.