- Home

- »

- Next Generation Technologies

- »

-

Zero Trust Security Market Size & Share Report, 2026-2033GVR Report cover

![Zero Trust Security Market (2026 - 2033)Report]()

Zero Trust Security Market (2026 - 2033)

Size, Share & Trends Analysis Report By Authentication (Single-factor, Multi-factor), By Type, By Deployment (Cloud, On-premises), By Enterprise Size, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$42.1BMarket Estimate, 2026

$48.5BMarket Forecast, 2033

$148.3BCAGR, 2026–2033

17.3%Zero Trust Security Market Summary

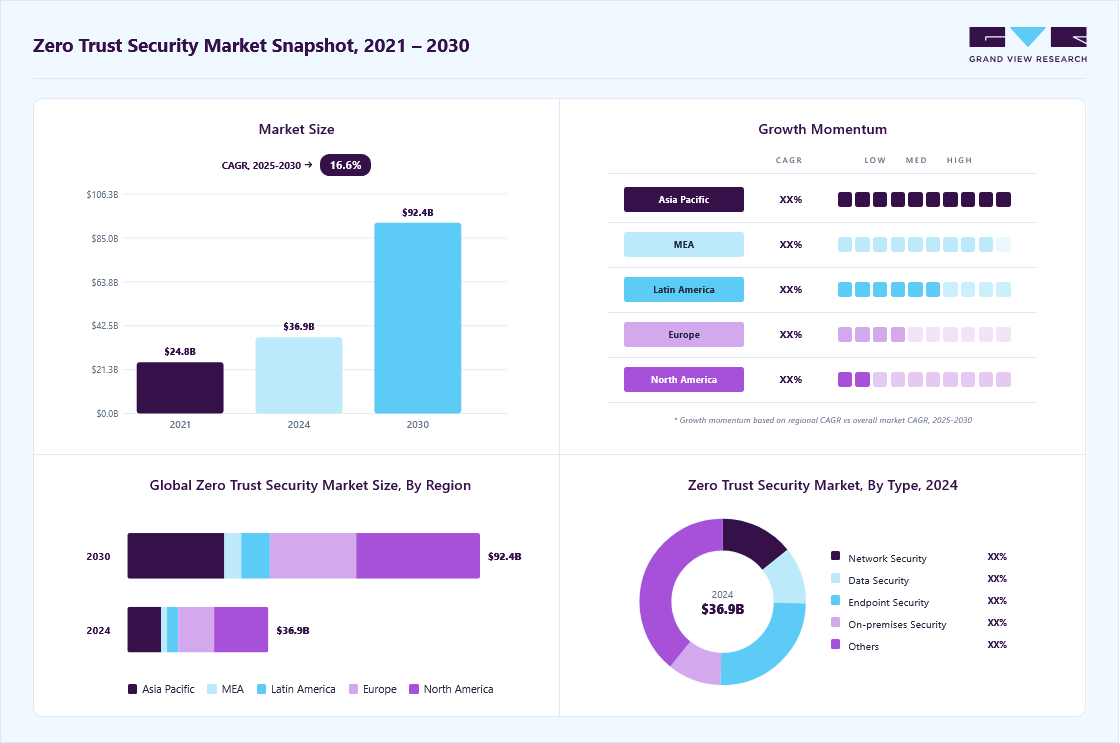

The global zero trust security market size was valued at USD 42.1 billion in 2025 and is projected to grow from USD 48.5 billion in 2026 to USD 148.3 billion by 2033, at a CAGR of 17.3% from 2026 to 2033. The North America market held the largest share of 39.9% of the global market in 2025. This growth is driven by the increasing adoption of cloud computing, remote work trends, and the surge in ransomware and insider threats.

Key Market Trends & Insights

- By type: The network security segment dominated the market, with a revenue share of 24.0% in 2025

- By deployment: The on-premises segment held the largest market share of 72.2% in 2025

- By authentication type: The Multi-factor Authentication Type segment held the largest revenue share in 2025

- By enterprise Size: The large enterprise segment held the largest revenue share in 2025

- By end use: The IT & telecom segment held the largest revenue share in 2025

Regional Highlights

- Largest regional market: North America (39.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 42.1 Billion

- Estimated market size in 2026: USD 48.5 Billion

- Projected market size by 2033: USD 148.3 Billion

- CAGR (2026-2033): 17.3%

Enterprises and government agencies are investing heavily in Zero Trust solutions, including multi-factor authentication (MFA), micro-segmentation, identity and access management (IAM), and endpoint security. Small and medium enterprises (SMEs) are also recognizing the benefits of Zero Trust architectures, driving demand for cost-effective and scalable solutions. As businesses continue to shift toward digital transformation, the zero trust security market is poised for exponential growth.")

The risk of cyberthreat is increasing considerably as cyber threat actors continue to explore vulnerabilities within an organization's IT infrastructure. Cyber threat actors gain access to critical information through vulnerabilities while maintaining anonymity. Cyber threat actors launch attacks such as persistent campaigns, advanced malware, spear-phishing, and watering holes to exploit organizational growth. For instance, according to research by Check Point Software Technologies Ltd., global cyberattacks increased by 28% in the third quarter of 2022 compared to 2021. Globally, the average number of weekly attacks per organization exceeded 1,100.

Over the years, targeted attacks on organizations across the globe have increased significantly. Attackers infiltrate a target organization's network infrastructure through endpoints, cloud-based applications, and other vulnerable networks. Such targeted attacks negatively impact a business's critical operations, leading to financial losses, loss of sensitive customer information, and loss of intellectual property. According to a sponsored study conducted by Trend Micro Incorporated with Quocirca, the most common objective of a targeted cyberattack is to impact organizational financial gains. Thus, a proactive detection layer is paramount to prevent the risk of losing regulated personal data, intellectual property, and economic loss. Through zero security principles, proactive detection and mitigation of cyber threats can be achieved by identifying the behavior of users infiltrating any network.

Market Dynamics

The global zero trust security market is experiencing robust growth as organizations increasingly adopt identity-centric security frameworks to address the rising sophistication of cyberattacks, expanding remote and hybrid work environments, and growing reliance on cloud-based applications and infrastructure. Zero Trust Security solutions continuously verify users, devices, applications, and network activities based on the principle of "never trust, always verify," helping organizations minimize unauthorized access and reduce attack surfaces. Key market trends include the integration of artificial intelligence (AI) and machine learning (ML) for adaptive risk assessment, increasing adoption of Zero Trust Network Access (ZTNA) as a replacement for traditional VPNs, and growing implementation of identity and access management (IAM), Multi-factor Authentication (MFA), and micro-segmentation technologies. Furthermore, stricter data privacy regulations, increasing ransomware incidents, and government-led cybersecurity initiatives are accelerating enterprise investments in Zero Trust architectures, positioning the market for sustained growth across both public and private sectors.

The growing emphasis on strengthening national cybersecurity resilience and protecting critical infrastructure is significantly driving the adoption of Zero Trust Security solutions worldwide. Governments and regulatory bodies are increasingly promoting Zero Trust architectures to address evolving cyber threats, ransomware attacks, insider risks, and vulnerabilities associated with cloud and hybrid work environments. As organizations move away from perimeter-based security models toward continuous verification of users, devices, and applications, demand for Zero Trust technologies such as identity and access management (IAM), Multi-factor Authentication (MFA), micro-segmentation, and Zero Trust Network Access (ZTNA) continues to rise. These initiatives are encouraging both public and private sector organizations to accelerate investments in Zero Trust implementations to enhance security posture and regulatory compliance.

For instance, in May 2026, the U.S. National Security Agency (NSA) launched a dedicated Zero Trust Implementation Guidelines Resource Webpage, providing organizations with comprehensive guidance and best practices for implementing Zero Trust architectures. The initiative aims to support federal agencies, defense organizations, and critical infrastructure operators in adopting standardized Zero Trust security frameworks, further accelerating market adoption and investment in Zero Trust technologies.

The adoption of Zero Trust Security solutions is often hindered by the complexity associated with integrating modern Zero Trust architectures into existing IT environments. Many organizations continue to rely on legacy applications, fragmented identity systems, and traditional network architectures that were not designed to support continuous authentication and least-privilege access principles. Implementing Zero Trust requires significant investments in identity management, network segmentation, endpoint visibility, policy orchestration, and employee training, which can increase deployment costs and extend implementation timelines. These challenges are particularly pronounced among small and medium-sized enterprises (SMEs) with limited cybersecurity budgets and technical resources, potentially slowing market adoption.

For instance, according to the U.S. Cybersecurity and Infrastructure Security Agency (CISA), organizations implementing Zero Trust often face challenges related to legacy system compatibility, identity governance modernization, and integration across multiple security platforms. Such complexities can delay deployment schedules and increase operational costs, limiting the pace of Zero Trust adoption across certain sectors.

The rapid adoption of cloud computing, SaaS applications, hybrid work models, and distributed enterprise environments presents a significant growth opportunity for the Zero Trust Security market. As organizations increasingly shift applications and workloads beyond traditional corporate networks, conventional perimeter-based security approaches become less effective. This transition is driving demand for cloud-native Zero Trust solutions, particularly Zero Trust Network Access (ZTNA), which enables secure access to applications regardless of user location or device type. Additionally, the growing integration of artificial intelligence (AI), machine learning (ML), and behavioral analytics into Zero Trust platforms is creating opportunities for more adaptive and automated security frameworks.

For instance, according to the U.S. Federal Zero Trust Strategy, federal agencies are required to accelerate the adoption of cloud-based and identity-centric security architectures, promoting widespread deployment of Zero Trust capabilities across government networks. Similar initiatives by enterprises worldwide to secure remote workforces and cloud environments are expected to create substantial long-term growth opportunities for Zero Trust vendors and service providers.

Analyst Perspective

The zero trust security market is undergoing a structural shift from traditional perimeter-based cybersecurity models to identity-centric, continuously verified security architectures, driven by the convergence of cloud adoption, hybrid work environments, and escalating cyber threats. As enterprises increasingly distribute workloads across multi-cloud and edge environments, the concept of a trusted internal network is rapidly becoming obsolete, compelling organizations to adopt zero trust principles as a foundational security strategy rather than a supplementary layer. The growing endorsement of Zero Trust frameworks by government bodies and cybersecurity agencies is further accelerating enterprise adoption, positioning Zero Trust as a de facto standard for modern cybersecurity architectures.

The competitive differentiation in this market will increasingly depend on vendors’ ability to deliver fully integrated, cloud-native security platforms that unify identity management, endpoint security, network segmentation, and continuous risk assessment into a single orchestration layer. Players that can operate zero trust at scale while reducing complexity through automation, AI-driven policy enforcement, and seamless interoperability across legacy and cloud environments will be best positioned to capture enterprise demand. Over the long term, Zero Trust is expected to evolve from a security framework into a core enterprise operating model, embedded across digital infrastructure, application access, and workforce Authentication Type ecosystems.

Authentication Insights

Based on authentication type, the multi-factor authentication segment led the market with the largest revenue share of 72.1% in 2025. This growth is driven by the rising adoption of passwordless authentication, biometric-based access controls, and the increasing demand for cost-effective security solutions among SMEs. Organizations are prioritizing user-friendly authentication methods to enhance security while reducing friction in user experience. Additionally, regulatory compliance requirements and the integration of AI-driven authentication technologies are fueling market expansion. As businesses shift towards cloud-based and remote work environments, the need for seamless yet secure authentication solutions will further propel the demand for advanced SFA solutions in the coming years.

The multi-factor segment is predicted to grow significantly in the forecast years. This growth is fueled by the rising frequency of cyberattacks, phishing attempts, and credential-based breaches, which push organizations to adopt stronger authentication measures. The increasing adoption of cloud computing, remote work, and BYOD (Bring Your Own Device) policies has further accelerated the demand for MFA solutions, ensuring enhanced security beyond traditional passwords. Regulatory mandates like GDPR, CCPA, and the U.S. Executive Order on Cybersecurity are driving enterprises to implement MFA for compliance.

Type Insights

Based on type, the endpoint security segment led the market with the largest revenue share of 26.9% in 2025. The growth of the endpoint segment can be attributed to its benefits which include improved patch management, preventing insider threats, filtering content web, reducing AI threats, and streamlining cybersecurity, among others. Moreover, the companies in the market have been developing an enhanced solution to get better traction. Companies are involved in various strategic initiatives, including partnerships, acquisitions, and mergers. For instance, in January 2023, Xcitium cybersecurity provider announced a partnership with Carrier SI, a communication solution provider. The partnership is aimed at offering enhanced and affordable endpoint security. Moreover, Carrier SI customers will now have access to the endpoint cybersecurity technology capable of containing known and unknown cyberattacks.

The on-premises security segment is predicted to foresee significant growth in the coming years. This growth is driven by the increasing need for data sovereignty, regulatory compliance, and enhanced control over security infrastructure, especially among large enterprises and government organizations. Industries handling sensitive data, such as finance, healthcare, and defense, prefer on-premises solutions to mitigate risks associated with cloud vulnerabilities. Additionally, the rising threat of cyberattacks, insider threats, and ransomware has fueled demand for dedicated, in-house security architectures.

Deployment Insights

Based on deployment, the on-premises segment led the market with the largest revenue share of 72.2% in 2025. The growth of the cloud-based segment can be attributed to the comfort and convenience the cloud-based deployment offers, which includes the lesser need for in-house resources, less need for upfront costs, continuous monitoring, flexible options, automatic backups, and effective patch management, among others. The flexibility and scalability of cloud-based deployment have been among the major factors that contributed to the growth of the cloud-based deployment of the market over 2025-2030.

The on-premises segment is expected to witness significant growth in the coming yearsdue to a high preference for this type of deployment. Organizations prefer to keep confidential data in-house rather than turning it over to a cloud provider. Moreover, on-premises solutions allow hands-on ownership and control of security monitoring, which offers a flexible and adaptive security program. This is expected to increase the demand for on-premises deployment over the forecast period. However, enterprises are migrating from on-premises to cloud-based solutions due to cost-effectiveness benefits.

Enterprise Size Insights

Based on enterprise size, the large enterprise segment led the market with the largest revenue share of 76.0% in 2025, owing to complex networking, programs, and endpoints of large-scale companies that need robust solutions to safeguard data by continuously validating and recording authentication in real-time. Companies rely on only adhering to compliance and entrusting authorized users with a higher risk of an internal breach. The compliant network does not guarantee a secure environment, as the threat to breach is not merely external but also could be by internal trusted sources. The zero-trust security model regards enterprise-authorized users with zero trust and provides the least privileged access to the users.

The SMEs segment is anticipated to exhibit the fastest CAGR over the forecast period. The COVID-19 pandemic affected both large- and small-scale vendors as cases of data breaches increased while employees resorted to the remote working environment. Small- and medium-sized banking, financial institutions, IT, manufacturing, telecom, and retail companies are targeted as they need robust security solutions. Zero trust security ensures that the user with correct credentials is an internal and trusted user, not hackers relying on phishing and other methods to gain illegitimate access to login credentials. Thereby, the adoption of a zero-trust security model is increasing among SMEs for implementing multi-level authorization verification.

End Use Insights

Based on end use, the IT & telecom segment led the market with the largest revenue share of 46.4% in 2025, due to the sector's intricate IT infrastructure demands. Increased preference for cloud-based infrastructure and digital applications to procure information and facilitate business drives the need for unified, secure access and network solutions. In addition, the telecom industry incumbents primarily provide data transfer services and spend on several security-related technologies. With the increasing awareness about the benefits and applications of zero-trust security, the adoption of this model is expected to grow significantly.

The healthcare segment is anticipated to exhibit the fastest CAGR over the forecast period. Continued innovation and implementation of technologies, such as telehealth services and analytics, to facilitate effective communication between end-users and entities are driving the need for secure network infrastructure services. Moreover, the increasing instances of cyber-attacks across healthcare IT infrastructures created the need for an advanced security framework for protecting critical information. These factors are expected to accelerate the demand for zero-trust security in the healthcare sector.

Regional Insights

North America dominated the global zero-trust security market with the largest revenue share of 39.9% in 2025. The rising demand for solutions pertaining to the zero-trust security model due to the increasing security spending by the government and public authorities is expected to drive the regional market. Furthermore, the increased adoption of the Internet of Things (IoT), AI, and digital technology by SMEs and large enterprises and the increasing stringency in standards and policies for maintaining data privacy and security are contributing to regional market growth.

The zero trust security market in the U.S. held the largest share in the North America region in 2025, driven by increasing cyber threats, stringent regulatory requirements, and rapid digital transformation across industries. The surge in ransomware attacks, data breaches, and insider threats has compelled enterprises and government agencies to adopt zero-trust architectures for enhanced security. Additionally, the rise of cloud computing, remote work, and IoT has increased the demand for identity-centric security solutions, multi-factor authentication (MFA), and micro-segmentation.

Europe Zero Trust Security Market Trends

The zero trust security market in the Europe is expected to witness significant growth over the forecast period, driven by rising cyber threats, strict regulatory frameworks, and increased cloud adoption. The enforcement of GDPR, NIS2 Directive, and other data protection laws is pushing enterprises to implement zero-trust architectures to ensure compliance and mitigate security risks. Additionally, the rise in state-sponsored cyberattacks and ransomware incidents has led businesses and government agencies to prioritize Zero Trust frameworks.

Asia Pacific Zero Trust Security Market Trends

The zero trust security market in the Asia Pacific region is anticipated to register the fastest CAGR over the forecast period, driven by increasing cyber threats, rapid digital transformation, and stringent regulatory policies across major economies like China, India, Japan, and Australia. Governments are strengthening cybersecurity frameworks, with initiatives like India’s Personal Data Protection Act (PDPA) and China’s Cybersecurity Law, compelling organizations to adopt zero-trust architectures.

Key Zero Trust Security Company Insights

Some key players in the zero trust security market include Broadcom, Inc., Fortinet, Inc., Palo Alto Networks, Inc., IBM Corporation, and Microsoft.

-

Broadcom Inc. is a key player in the zero trust security market, leveraging its expertise in enterprise security, network protection, and identity management. Through its Symantec division, Broadcom offers advanced zero trust solutions that include multi-factor authentication (MFA), endpoint security, network micro-segmentation, and threat intelligence. The company’s AI-driven security analytics help organizations detect and prevent sophisticated cyber threats in real-time. With increasing demand for cloud-based zero trust architectures, Broadcom has expanded its portfolio to support secure access service edge (SASE) frameworks and zero trust network access (ZTNA) solutions.

-

Fortinet, Inc. is a foremost player in the zero trust security market, offering a comprehensive portfolio of Zero Trust Network Access (ZTNA), endpoint security, and identity-based access solutions. Its FortiNAC and FortiAuthenticator solutions enable enterprises to implement network segmentation, multi-factor authentication (MFA), and continuous verification to reduce attack surfaces. Fortinet’s AI-driven threat intelligence and Secure Access Service Edge (SASE) solutions further enhance Zero Trust capabilities, ensuring secure access to applications and data across hybrid environments.

Key Zero Trust Security Companies

The following key companies have been profiled for this study on the zero trust security market.

-

Broadcom, Inc.

-

Fortinet, Inc.

-

Palo Alto Networks, Inc.

-

IBM Corporation

-

Microsoft

-

Cisco Systems, Inc.

-

Cloudflare, Inc.

-

Check Point Software Technology Ltd.

-

CrowdStrike, Inc.

-

Forcepoint

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Mature Players (Broadcom; Fortinet, Inc.; Palo Alto Networks, Inc.; IBM Corporation; Microsoft; Cisco Systems Inc.; Check Point Software Technologies Ltd.)

- Expand integrated cybersecurity ecosystems combining Zero Trust, network security, endpoint protection, and cloud security under unified platforms.

- Strengthen enterprise adoption through large-scale cloud partnerships, managed security services, and deep integration with existing IT infrastructure.

- Strong global enterprise customer base with established trust and long-term contracts across industries.

- Broad, end-to-end cybersecurity portfolios enabling bundled Zero Trust adoption within existing security stacks.

- High complexity in product portfolios leading to slower innovation cycles and longer deployment customization timelines.

- Legacy infrastructure dependencies that can limit agility in rapidly evolving cloud-native Zero Trust architectures.

Emerging Players (CrowdStrike Inc.; Cloudflare, Inc.; Forcepoint)

- Focus on cloud-native, API-driven Zero Trust solutions emphasizing identity-centric security, SASE (Secure Access Service Edge), and ZTNA-first architectures.

- Expand rapidly through subscription-based SaaS models, lightweight deployment, and strong developer/DevSecOps ecosystem integration.

- High agility and faster innovation cycles compared to traditional security vendors.

- Strong positioning in cloud-first environments with simplified, scalable deployment models.

- Limited legacy enterprise penetration compared to established cybersecurity vendors.

- Narrower product breadth requiring reliance on partnerships for full-stack enterprise cybersecurity coverage.

Recent Developments

-

In December 2024, Cognizant and Zscaler announced an expanded partnership aimed at helping enterprises across industries streamline and enhance their security posture with an AI-powered Zero Trust cloud security platform. This collaboration addresses evolving cyber threats by delivering coordinated services and solutions that reduce security complexity, strengthen defenses, and provide cost-effective, scalable protection. By combining their expertise, Zscaler and Cognizant enable organizations to modernize cybersecurity strategies while ensuring rapid and comprehensive security transformation.

-

In October 2024, Alkira Inc., a prominent player in Network Infrastructure as a Service, unveiled Alkira Zero Trust Network Access (ZTNA), a cutting-edge cloud-based solution designed to revolutionize secure enterprise access from anywhere. Scheduled for general availability in Q4 2024, Alkira ZTNA integrates zero trust principles with Alkira’s expertise in network infrastructure, providing a seamless, end-to-end security platform. This innovative service ensures robust protection and streamlined connectivity without compromising network performance and efficiency, making it a game-changer for modern enterprises.

-

In January 2024, Zscaler, Inc., a leader in cloud security, introduced Zscaler Zero Trust SASE, the industry’s first single-vendor SASE solution powered by Zscaler Zero Trust AI. Designed to simplify Zero Trust implementation across users, devices, and workloads, this solution helps organizations reduce costs and complexity. Additionally, Zscaler announced the general availability of its Zero Trust SD-WAN solution and a portfolio of plug-and-play appliances, enabling businesses to modernize secure connectivity for branch offices, factories, and data centers. By eliminating the need for VPNs and traditional firewalls, Zscaler’s solutions provide a more efficient, scalable, and secure approach to enterprise networking.

Zero Trust Security Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 42.1 billion

Estimated market size in 2026

USD 48.5 billion

Projected market size by 2033

USD 148.3 billion

Growth rate

CAGR of 17.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share analysis, competitive landscape, growth factors, and trends

Segments covered

Type, deployment, authentication type, enterprise size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Broadcom; Inc.; Fortinet, Inc.; Palo Alto Networks, Inc.; IBM Corporation; Microsoft; Cisco Systems Inc.; Cloudflare, Inc.; Check Point Software Technology Ltd.; CrowdStrike Inc.; Forcepoint

Customization scope

Free report customization (equivalent to up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Zero Trust Security Market Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global zero trust security market report based on type, deployment, authentication type, enterprise size, end use, and region.

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Network Security

-

Data Security

-

Endpoint Security

-

Cloud Security

-

Identity and Access Management (IAM) Security

-

Security Information and Event Management (SIEM)

-

Application Security

-

Others

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-Premises

-

-

Authentication Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Single-Factor Authentication Type

-

Multi-factor Authentication Type

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

SMEs

-

Large Enterprises

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT & Telecom

-

BFSI

-

Healthcare

-

Retail

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

U.K.

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

MEA

-

UAE

-

South Africa

-

KSA

-

-

Research Methodology

Segment Definition

Segment - Type

Revenue capture definition

Network Security

Revenue is generated through subscriptions and licensing fees for Zero Trust Network Access (ZTNA), micro-segmentation, software-defined perimeter (SDP), network access control (NAC), and secure remote access solutions. Additional revenue is captured through implementation, consulting, and managed security services that help organizations enforce least-privilege access across networks.

Data Security

Revenue is earned through licensing and subscription models for data loss prevention (DLP), encryption, data classification, data access governance, and information protection solutions. Growing regulatory compliance requirements and the need to protect sensitive enterprise data continue to drive spending within this segment.

Endpoint Security

Revenue is captured through endpoint detection and response (EDR), extended detection and response (XDR), device trust verification, endpoint protection platforms, and continuous endpoint monitoring solutions. The increasing number of remote and mobile devices accessing corporate resources has strengthened demand for endpoint-centric Zero Trust security controls.

Cloud Security

Revenue is generated through cloud-native security platforms, cloud access security brokers (CASB), cloud workload protection, identity security, and secure access service edge (SASE) solutions. Rising cloud adoption and multi-cloud deployments are accelerating demand for Zero Trust security solutions designed specifically for distributed cloud environments.

Identity and Access Management (IAM) Security

As one of the largest Zero Trust segments, revenue is primarily captured through licensing and subscription fees for identity governance, privileged access management (PAM), multi-factor authentication (MFA), single sign-on (SSO), adaptive authentication, and identity verification platforms. Continuous user authentication and least-privilege access principles drive strong demand.

Security Information and Event Management (SIEM)

Revenue is generated through software subscriptions, cloud-based platforms, and managed services that collect, correlate, and analyze security events across enterprise environments. Advanced SIEM solutions integrated with AI-driven threat detection and Zero Trust policy enforcement represent a growing revenue stream.

Application Security

Revenue is earned through application security testing, runtime protection, API security, web application firewalls (WAFs), secure software development tools, and continuous application monitoring solutions. Increasing adoption of cloud-native and DevSecOps practices is supporting revenue growth in this segment.

Others

This segment includes threat intelligence, security analytics, user and entity behavior analytics (UEBA), risk assessment, orchestration and automation platforms, and other Zero Trust-related technologies not covered under the primary classifications. Revenue is generated through software subscriptions, professional services, and managed security offerings.

Segment - Deployment

Revenue capture definition

On-Premises

Revenue is generated through perpetual software licenses, maintenance contracts, hardware appliances, implementation services, and security infrastructure upgrades deployed within an organization's own data centers. Demand is particularly strong among highly regulated industries requiring complete control over security environments and sensitive data.

Cloud

Revenue is captured through subscription-based SaaS models, cloud-native Zero Trust platforms, managed security services, and usage-based pricing structures. Increasing cloud migration, hybrid work adoption, and the adoption of distributed IT environments are driving recurring revenue opportunities within cloud deployments.

Segment - Authentication Type

Revenue capture definition

Single-Factor Authentication Type

Revenue is generated through basic identity verification solutions that rely on passwords, PINs, or security tokens. Although adoption is declining due to security limitations, the segment continues to generate revenue from legacy systems, cost-sensitive organizations, and transitional Zero Trust deployments.

Multi-factor Authentication Type

As the dominant Authentication Type segment, revenue is primarily captured through subscription and licensing fees for solutions utilizing passwords combined with biometrics, one-time passcodes (OTP), hardware tokens, mobile authenticators, and adaptive Authentication Type technologies. Regulatory requirements and increasing cyber threats continue to drive widespread adoption.

Segment - Enterprise Size

Revenue capture definition

Large Enterprise

Revenue is captured through large-scale deployments of Zero Trust architectures, enterprise-wide identity governance, network segmentation, privileged access management, security analytics, and managed security services. Multi-year contracts, complex integrations, and compliance-driven security investments contribute significantly to revenue generation within this segment.

SMEs

Revenue is generated through cloud-based Zero Trust subscriptions, managed security services, bundled cybersecurity offerings, and scalable identity management solutions. SMEs increasingly adopt cost-effective security platforms to strengthen cyber resilience while minimizing capital expenditure requirements.

Segment - End Use

Revenue capture definition

IT & Telecom

Revenue is generated through the deployment of Zero Trust frameworks across distributed networks, cloud environments, data centers, and remote workforces. Continuous technology modernization and high cybersecurity spending make this one of the largest end-use segments.

BFSI

Revenue is earned through investments in identity verification, fraud prevention, privileged access management, data protection, and regulatory compliance solutions. Financial institutions require robust Zero Trust architectures to protect sensitive customer and transaction data from increasingly sophisticated cyber threats.

Healthcare

Revenue is captured through the deployment of Zero Trust solutions that secure electronic health records (EHRs), medical devices, telehealth platforms, and clinical systems. Regulatory requirements regarding patient privacy and healthcare data protection are major drivers of spending in this segment.

Retail

Revenue is generated through solutions securing customer data, payment systems, e-commerce platforms, supply chains, and distributed retail locations. Increasing digital commerce activity and rising cyberattacks targeting retailers continue to support market growth.

Others

This segment includes government, manufacturing, education, energy & utilities, transportation, and other industries. Revenue is derived from identity security, access control, data protection, and compliance-focused Zero Trust deployments as organizations seek to strengthen cybersecurity resilience and reduce operational risk.

Estimation Model

Layer

Question

Analysis

Identity & Access Base Layer

Who requires Zero Trust protection?

Identify the total population of enterprise users, devices, workloads, applications, and digital identities operating across on-premises, cloud, and hybrid environments to define the potential addressable base for Zero Trust Security solutions. This includes employees, contractors, third-party users, endpoints, servers, and cloud resources requiring secure access controls.

Security Readiness & Infrastructure Layer

Which organizations can deploy Zero Trust architectures?

Apply factors such as cloud adoption maturity, identity management capabilities, cybersecurity spending, network modernization, regulatory requirements, and security infrastructure readiness to determine the serviceable market capable of implementing Zero Trust frameworks. Organizations with established IAM, MFA, endpoint security, and cloud security foundations form the primary deployment base.

Zero Trust Adoption Layer

Who actively implements Zero Trust Security solutions?

Apply enterprise cybersecurity priorities, ransomware exposure, remote/hybrid workforce penetration, compliance requirements, and digital transformation initiatives to convert the serviceable market into active adopters of Zero Trust technologies. This includes organizations deploying Zero Trust Network Access (ZTNA), Identity and Access Management (IAM), Privileged Access Management (PAM), micro-segmentation, and continuous Authentication Type solutions.

Monetization Layer

How much revenue is generated?

Assess revenue generation potential by analyzing spending on Zero Trust software licenses, SaaS subscriptions, professional services, implementation and integration services, managed security services, identity governance solutions, endpoint security tools, and ongoing monitoring and compliance management across active Zero Trust adopters.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Regulatory & Government-Led Security Framework Assessment

Analyzed the impact of government initiatives, regulatory mandates, and cybersecurity guidelines promoting Zero Trust implementation across public sector, defense, and critical infrastructure organizations.

Provides insights into compliance-driven adoption, policy-led cybersecurity investments, and expansion opportunities across regulated industries and government networks.

Technology Integration & Enterprise Readiness Assessment

Evaluated integration requirements for Zero Trust solutions with legacy IT systems, identity governance platforms, endpoint security tools, and cloud-native environments, along with implementation challenges and deployment maturity levels.

Supports strategic planning by identifying implementation barriers, modernization needs, and opportunities for long-term enterprise security transformation.

Cloud & Remote Workforce Security Opportunity Assessment

Assessed the growing demand for Zero Trust solutions in cloud computing environments, SaaS ecosystems, hybrid work models, and distributed enterprise networks, including ZTNA adoption trends and AI-driven security enhancements.

Enables the identification of scalable growth opportunities driven by cloud-first strategies, remote-access security requirements, and increasing enterprise digital transformation initiatives.

Frequently Asked Questions About This Report

Key factors that are driving the zero-trust security market growth include the increasing adoption of cloud computing, remote work trends, and the surge in ransomware and insider threats. Enterprises and government agencies are investing heavily in Zero Trust solutions, including multi-factor authentication (MFA), micro-segmentation, identity and access management (IAM), and endpoint security.

Some key players operating in the zero-trust security market include Broadcom, Inc., Fortinet, Inc., Palo Alto Networks, Inc., IBM Corporation, Microsoft, Cisco Systems, Inc., Cloudflare, Inc., Check Point Software Technology Ltd., CrowdStrike, Inc., Forcepoint

The on-premises segment led with a 72.2% revenue share in 2025, while cloud segment is the fastest-growing segment.

The IT & telecom segment led with a 46.4% revenue share in 2025, while healthcare segment is the fastest-growing segment.

The multi-factor authentication segment led with a 72.1% revenue share in 2025 and is also the fastest-growing segment.

Asia Pacific is the fastest-growing region over the forecast period.

The global zero-trust security market size was estimated at USD 42.1 billion in 2025 and is expected to reach USD 48.5 billion in 2026.

North America emerged as a dominant regional zero-trust security market capturing 39.9% of the overall zero-trust security revenue share in 2025.

The global zero-trust security market is expected to grow at a compound annual growth rate of 17.3% from 2026 to 2033 to reach USD 148.3 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.