- Home

- »

- Advanced Interior Materials

- »

-

Abrasives Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Abrasives Market (2026 - 2033)Report]()

Abrasives Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Coated, Bonded), By Application (Automotive & Transportation, Heavy Machinery, Metal Fabrication, Electrical & Electronics Equipment), By Region, And Segment Forecasts

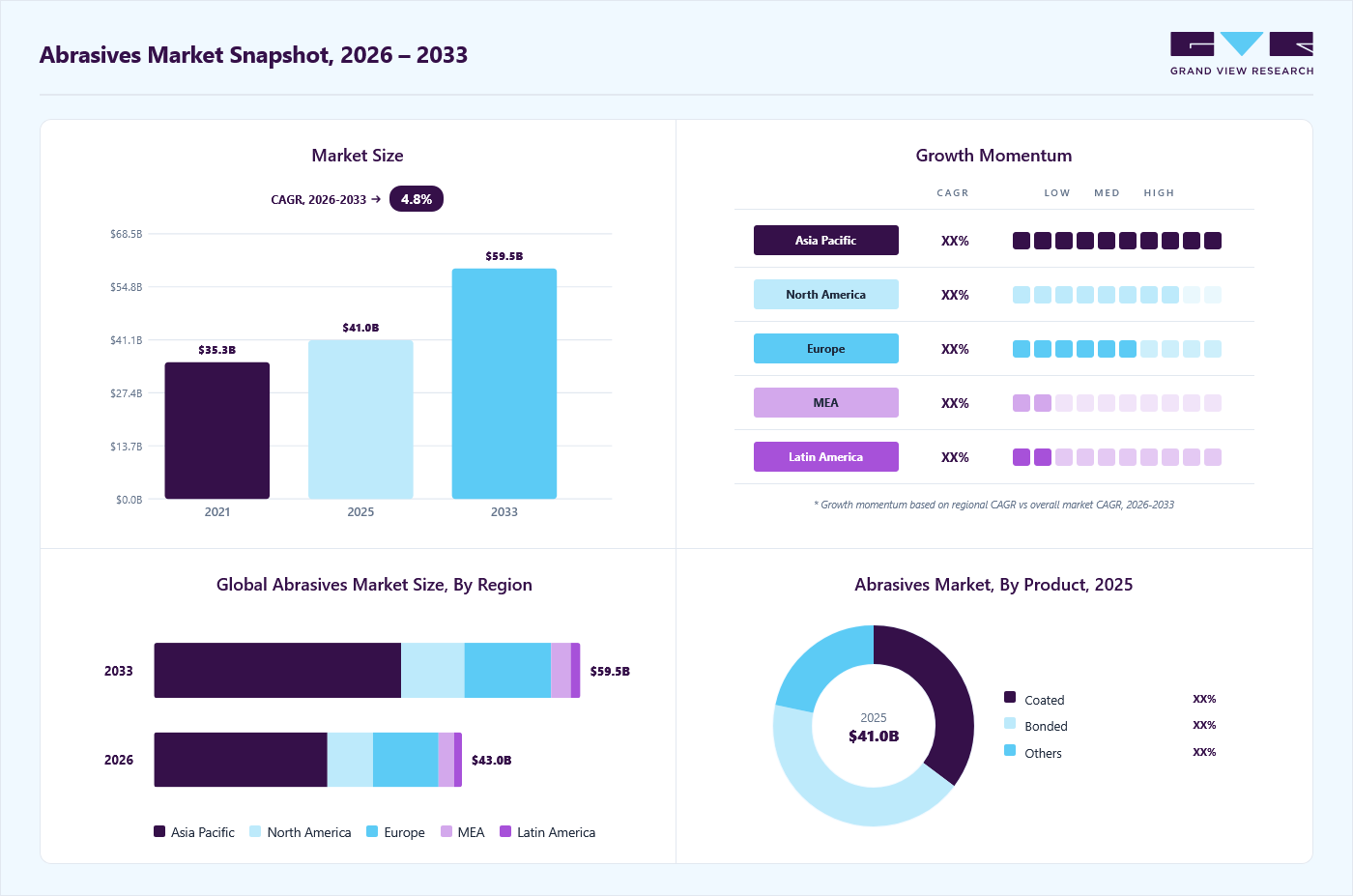

Market Size, 2025

$41.0BMarket Estimate, 2026

$43.0BMarket Forecast, 2033

$59.5BCAGR, 2026–2033

4.8%Abrasives Market Summary

The global abrasives market size was valued at USD 41.0 billion in 2025 and is projected to grow from USD 43.0 billion in 2026 to USD 59.5 billion by 2033, at a CAGR of 4.8% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 56.0% in 2025. Market growth is primarily driven by the steady expansion of the metal fabrication industry, which remains one of the largest consumers of abrasive products, including bonded wheels, coated abrasives, and super abrasives.

Key Market Trends & Insights

- By product: Bonded segment held the largest market share of 43.0% in 2025.

- By application: Automotive & transportation segment held the largest market share of 35.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (56.0% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 41.0 Billion

- Estimated market size in 2026: USD 43.0 Billion

- Projected market size by 2033: USD 59.5 Billion

- CAGR (2026-2033): 4.8%

The increasing adoption of pre-engineered buildings (PEBs) and prefabricated structural components has significantly increased demand for cutting, grinding, deburring, and surface-finishing solutions.Sustainability is becoming a defining theme in the global abrasives industry as manufacturers respond to tightening environmental regulations and increasing customer emphasis on responsible sourcing. Abrasive production, particularly synthetic variants such as aluminum oxide and silicon carbide, is energy-intensive, prompting producers to invest in energy-efficient furnaces, waste heat recovery systems, and renewable power integration. There is also growing adoption of recyclable and reusable abrasive media, including steel shot and garnet, especially in surface preparation and blasting applications. In addition, water-based bonding systems, low-VOC resins, and reduced-emission manufacturing processes are being implemented to minimize environmental impact.

")

Processes such as laser cutting, waterjet machining, plasma treatment, and chemical-mechanical polishing (CMP) are gaining traction in specific high-precision and non-contact applications. These technologies can offer improved accuracy, reduced material loss, and lower secondary-finishing requirements in certain end-use sectors, such as aerospace and electronics. However, despite the emergence of these alternatives, conventional abrasives remain cost-effective, versatile, and indispensable for large-scale metal fabrication, construction, and industrial maintenance activities.

Drivers, Opportunities & Restraints

The global abrasives industry is driven by growing demand from the automotive, aerospace, metal fabrication, and heavy machinery industries, where abrasives are crucial for cutting, grinding, and surface finishing. In 2025, multiple automakers announced large-scale production expansions, boosting industrial machining activity. For example, General Motors expanded its EV and ICE vehicle manufacturing capacity in the U.S., increasing demand for precision grinding and finishing processes that rely on high-performance bonded and coated abrasives.

Rapid growth in semiconductor manufacturing and electronics production presents a major opportunity for abrasive producers, particularly in high-precision wafer slicing, lapping, and polishing applications. In 2025, industry forecasts indicated that global semiconductor manufacturing equipment spending would exceed USD 125 billion, reflecting accelerated investment in new fabs and advanced production lines in the U.S., Asia, and Europe. This expansion supports increased consumption of superabrasives and specialty coated products tailored for semiconductor fabrication processes.

The market faces challenges from raw material price volatility and tightening environmental regulations on abrasive manufacturing processes. In 2025, energy cost fluctuations driven by global oil and gas market instability increased production expenses for energy-intensive synthetic abrasive materials, pressuring producer margins. Simultaneously, several European regulators implemented stricter emissions and waste-discharge standards for industrial material producers, increasing compliance costs for abrasive manufacturers operating in the region and restraining capacity expansions.

Product Insights

Based on product, bonded abrasives dominated the global market in 2025, accounting for over 43.0% of total revenue. Bonded abrasives include grinding wheels, snagging wheels, mounted wheels, and other vitrified or resin-bonded products widely used for precision grinding, heavy stock removal, and rough grinding operations. Their high material removal rate, dimensional stability, and suitability for automated grinding systems make them indispensable in metal fabrication, automotive components, and industrial machinery applications. The segment continues to benefit from rising demand in structural steel processing and advanced manufacturing environments where performance consistency and durability are critical.

The coated abrasives segment is expected to register the fastest CAGR over the forecast period. This category includes rolls, sheets, discs, belts, and flap-wheel products used extensively in surface preparation and finishing applications. Growing demand from white goods, sanitaryware, furniture, automotive, fabrication, and construction industries has prompted capacity expansions among leading manufacturers. For instance, in 2025, Carborundum Universal Ltd. announced further capacity augmentation and technology upgrades in its coated abrasives division to strengthen its export footprint and meet rising demand from stainless steel fabrication and woodworking industries. The expansion aligns with rising demand in precision finishing applications, particularly in stainless steel processing and engineered wood products, which are witnessing sustained global growth.

Application Insights

Based on application, the automotive & transportation segment held the largest revenue share of over 35.0% in 2025. In automotive manufacturing, abrasives are critical for coarse sanding, lacquer sanding, precision grinding, and surface finishing of engine components, body panels, and drivetrain systems.

In 2025, global automotive production continued to expand and modernize, with major investments such as the expansion of automotive manufacturing capacity by key suppliers in North America, including a USD 110 million plant expansion by AUMOVIO in Texas aimed at boosting production of advanced driver-assistance components. This type of capacity build-out drives higher consumption of bonded and coated abrasives across machining, sanding, and finishing operations in vehicle assembly lines.

The heavy machinery application segment is witnessing accelerated growth as global industrial and infrastructure investments expand capital equipment production. Abrasives are extensively used in metal cutting, surface grinding, and the refurbishment of mining and construction machinery components.

The electrical & electronics segment is also strengthened, driven by record investments in semiconductor manufacturing infrastructure. In 2025, global semiconductor fabrication equipment is expected to reach approximately USD 125.5 billion, reflecting the sustained expansion of wafer fabrication capacity worldwide. In addition, major chipmakers announced plans to expand fab and procure equipment to meet growing demand for advanced semiconductors. Abrasives play a critical role in wafer slicing, lapping, grinding, and polishing of hard materials such as silicon and quartz, thereby directly linking semiconductor capital expenditure growth with increased demand for high-precision super abrasives.

Regional Insights

Asia Pacific abrasives industry dominated the global market with the largest market revenue share of over 56.0% in terms of both production and consumption in 2025, driven by rapid industrialization, urbanization, and infrastructure expansion. China, India, Japan, and South Korea are major manufacturing hubs for automotive, electronics, heavy machinery, and construction materials, driving substantial demand for bonded and coated abrasives. The region’s expanding semiconductor fabrication capacity and large-scale metal fabrication industry significantly contribute to superabrasive consumption. Competitive manufacturing costs and the presence of numerous local abrasive producers further strengthen Asia Pacific’s leadership in the global market.

China Abrasives Market Trends

China is one of the key consumers of abrasives, driven by its dominant position in manufacturing, metal fabrication, automotive production, electronics, construction, and precision engineering. The market comprises bonded abrasives (grinding wheels), coated abrasives (sandpaper and belts), and superabrasives (diamond and cubic boron nitride), with strong demand from steel processing, machinery manufacturing, shipbuilding, and the fast-growing EV and semiconductor sectors. China also has an integrated supply chain for key raw materials such as fused alumina and silicon carbide, making it a major exporter of abrasive grains and finished products.

North America Abrasives Market Trends

North America abrasives industry represents a mature yet innovative-driven market for abrasives, supported by strong automotive manufacturing, aerospace production, metal fabrication, and defense sectors. The presence of advanced manufacturing infrastructure in the U.S., Canada, and Mexico sustains demand for high-performance bonded and superabrasives used in precision machining and surface finishing applications. Increasing investments in electric vehicle production, semiconductor fabrication facilities, and infrastructure modernization projects continue to reinforce abrasive consumption. In addition, the region emphasizes automation and Industry 4.0 integration in grinding and finishing operations, supporting demand for technologically advanced abrasive solutions with improved durability and efficiency.

The U.S. abrasives industry represents a technologically advanced, high-value market globally, driven by strong demand from automotive manufacturing, aerospace & defense, metal fabrication, construction, and semiconductor production. The country’s well-established industrial base supports extensive use of bonded, coated, and superabrasives for precision grinding, surface finishing, and high-performance machining applications. Ongoing investments in electric vehicle manufacturing, infrastructure modernization, and domestic semiconductor fabrication facilities are further reinforcing demand for advanced abrasive solutions.

Europe Abrasives Market Trends

Europe abrasives industry maintains a stable share in the global market, driven by its well-established automotive, aerospace, machinery, and industrial equipment industries. Countries such as Germany, Italy, and France are key contributors due to their strong engineering and manufacturing bases. The region also exhibits a growing focus on sustainability, encouraging the adoption of energy-efficient production processes and recyclable abrasive materials. Demand for precision abrasives remains strong in automotive component manufacturing and metalworking, while investments in renewable energy infrastructure and rail transport modernization further support steady market growth.

Latin America Abrasives Market Trends

Latin America abrasives industry presents moderate but steadily growing demand for abrasives, primarily driven by mining, construction, automotive assembly, and metal fabrication. Countries such as Brazil and Mexico are key contributors, benefiting from infrastructure development and industrial expansion initiatives. Growth in mining operations particularly supports demand for grinding and cutting abrasives used in equipment maintenance and mineral processing. While the region faces economic volatility at times, gradual industrial diversification and foreign investments are expected to sustain stable abrasive consumption over the forecast period.

Middle East & Africa Abrasives Market Trends

The Middle East & Africa abrasives industry is experiencing gradual market growth, driven by infrastructure development, oil & gas projects, mining activities, and increasing industrialization. Construction expansion in Gulf Cooperation Council (GCC) countries supports demand for cutting, grinding, and surface preparation abrasives. In Africa, mining and resource extraction activities contribute to demand for heavy-duty abrasive products used in equipment fabrication and maintenance. Although the market size remains comparatively small compared to other regions, ongoing diversification efforts and industrial investments are expected to create new growth opportunities in the coming years.

Key Abrasives Company Insights

Some of the key players operating in the market include 3M, Saint-Gobain, Carborundum Universal Ltd., and others

-

3M is a U.S.-based multinational corporation founded in 1902, operating across diversified industrial and consumer segments, including a comprehensive abrasives portfolio. The company manufactures bonded, coated, and superabrasive products used in metal fabrication, automotive manufacturing, aerospace, electronics, and construction applications. 3M emphasizes research-driven innovation, precision engineering, and sustainability by developing high-performance abrasive solutions with improved durability and reduced environmental impact. With a strong global distribution network and advanced manufacturing capabilities, the company serves industrial customers across North America, Europe, and the Asia Pacific.

-

Saint-Gobain is a France-based multinational corporation founded in 1665, recognized as one of the global leaders in abrasive manufacturing through its performance materials division. The company offers a broad range of bonded, coated, and superabrasive solutions under well-established brands, serving automotive, aerospace, metal fabrication, construction, and industrial maintenance sectors. Saint-Gobain focuses on sustainable manufacturing, energy-efficient production processes, and product innovation to enhance cutting precision and operational efficiency. With manufacturing facilities and sales operations worldwide, the company maintains a strong presence across developed and emerging markets.

-

Carborundum Universal Ltd. (CUMI) is an India-based abrasives and ceramics manufacturer founded in 1954 and part of the Murugappa Group. The company produces a wide portfolio of bonded abrasives, coated abrasives, superabrasives, and electro-mineral products catering to automotive, engineering, steel, construction, and woodworking industries. CUMI emphasizes capacity expansion, technological upgrades, and the development of export markets to strengthen its competitive position. With manufacturing facilities across India and international subsidiaries, the company serves both domestic and global markets, positioning itself as a key player in the Asia Pacific abrasives landscape.

Key Abrasive Companies:

The following key companies have been profiled for this study on the abrasives market.

- 3M

- Asahi Diamond Industrial Co., Ltd.

- Bosch Limited

- Carborundum Universal Ltd. (CUMI)

- Fujimi Incorporated

- Henkel AG & Co. KGaA

- SAK Abrasives Limited

- Saint-Gobain

- sia Abrasives Industries AG

- Tyrolit Group

Recent Developments

-

Saint-Gobain completed the acquisition of FOSROC on February 7, 2025, purchasing the global construction chemicals player with approximately USD 487 million in 2024 revenues and around 3,000 employees. This strategic acquisition expands Saint-Gobain’s presence in high-growth emerging markets-particularly India, the Middle East, and Asia-Pacific and increases its combined construction chemicals sales to an estimated USD 7.0-7.1 billion across 76 countries, reinforcing its competitive footprint in complementary industrial segments.

-

3M reported strong Q4 2025 results, with quarterly sales of USD 6.02 billion, exceeding analysts’ revenue forecasts by approximately 3.7%, reflecting robust performance in its industrial and safety segments that include abrasives and related products. This performance underscores renewed operational momentum and resilience in core industrial markets during 2025.

-

3M also reaffirmed its R&D investment strategy in 2025, committing to spend approximately USD 3.5 billion on research and development through 2027 to accelerate innovation across its material science and industrial product portfolio, including advanced abrasive technologies designed to improve performance and sustainability.

Abrasives Market Report Scope

Report Attribute

Details

Market definition

Market size refers to the annual sales value of abrasive products in a given year.

Market size in 2025

USD 41.0 billion

Estimated market size in 2026

USD 43.0 billion

Projected market size by 2033

USD 59.5 billion

Growth rate

CAGR of 4.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Russia; China; India; Japan; Australia; Brazil

Key companies profiled

3M; Asahi Diamond Industrial Co., Ltd.; Bosch Limited; Carborundum Universal Ltd.; Fujimi Incorporated; Henkel AG & Co. KGaA; SAK Abrasives Limited; Saint-Gobain; sia Abrasives Industries AG; Tyrolit Group

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Abrasives Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global abrasives market report based on product, application, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Coated

-

Bonded

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Automotive & Transportation

-

Heavy Machinery

-

Metal Fabrication

-

Electrical & Electronics Equipment

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Frequently Asked Questions About This Report

Some of the key vendors of the global abrasives market are 3M, Asahi Diamond Industrial Co., Ltd., Bosch Limited, Carborundum Universal Ltd., Fujimi Incorporated, Henkel AG & Co. KGaA, SAK Abrasives Limited, Saint-Gobain, sia Abrasives Industries AG, and Tyrolit Group, among others.

The global abrasives market is primarily driven by rising demand for metal fabrication, supported by expansion in the manufacturing sector. Increasing industrial production across the automotive, construction, and heavy machinery industries is expected to augment market growth over the forecast period.

The global abrasives market size was estimated at USD 41.0 billion in 2025 and is expected to reach USD 43.0 billion in 2026.

The global abrasives market is expected to grow at a compound annual growth rate of 4.8% from 2026 to 2033 to reach USD 59.5 billion by 2033.

The automotive & transportation segment dominated the market, accounting for over 35.0% of revenue in 2025.

Bonded abrasives held the largest revenue share 43.0% in 2025, while coated abrasives is the fastest-growing area.

Asia Pacific dominated with a 56.0% revenue share in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.