- Home

- »

- Clinical Diagnostics

- »

-

Activated Clotting Time Testing Market Size Report, 2033GVR Report cover

![Activated Clotting Time Testing Market Size, Share & Trends Report]()

Activated Clotting Time Testing Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (ACT Analyzers, Consumables), By Test Type, By Application (Cardiovascular Surgery, Interventional Cardiology, Hemodialysis), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$1.2BMarket Estimate, 2026

$1.3BMarket Forecast, 2033

$2.1BCAGR, 2026–2033

7.6%Activated Clotting Time Testing Market Summary

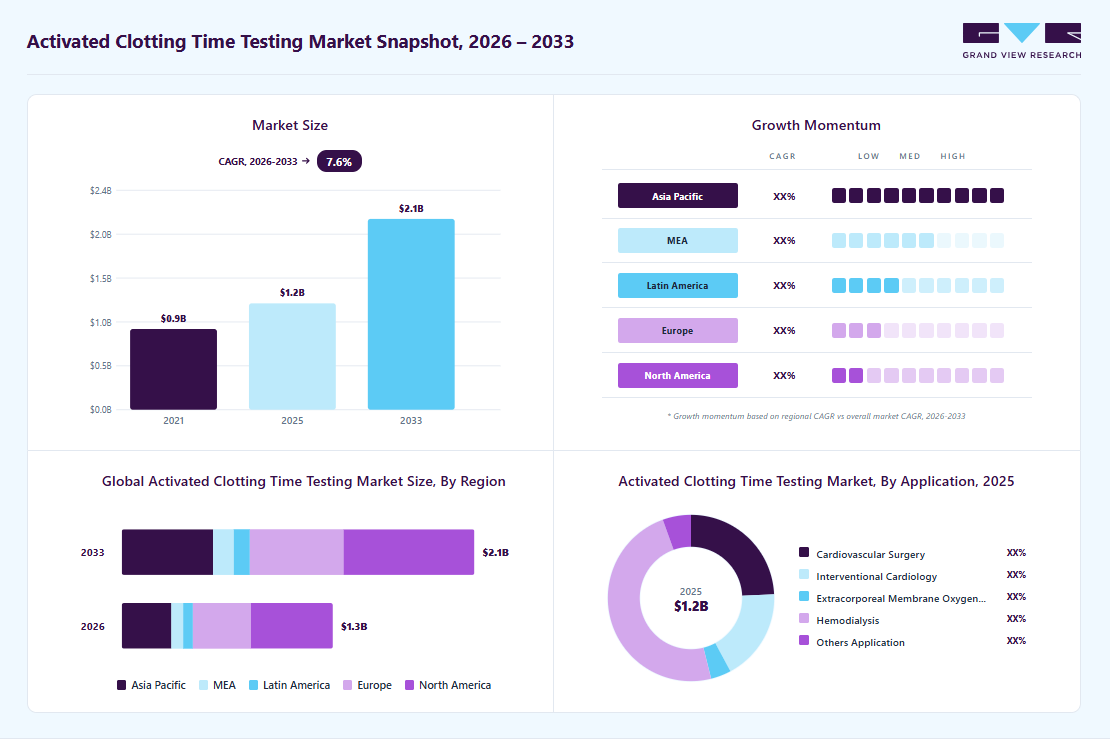

The global activated clotting time testing market size was valued at USD 1.2 billion in 2025 and is projected to grow from USD 1.3 billion in 2026 to USD 2.1 billion by 2033, at a CAGR of 7.6% from 2026 to 2033. North America dominated the global activated clotting time testing market with the largest revenue share of 39.1% in 2025. The growth of the market is driven by the increasing cardiovascular disease prevalence, growing adoption of point of care diagnostics, and a steady increase in the number of surgical procedures particularly minimally invasive surgeries.

Key Market Trends & Insights

- By product: Consumables segment dominated the global market and accounted for the largest revenue share of 87.99% 2025.

- By test type: High-range act tests, segment held the largest revenue share of 68.14% in 2025.

- By application: Hemodialysis segment held the largest revenue share of 48.38% in 2025.

Regional Highlights

- Largest regional market: North America (39.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.2 Billion

- Estimated market size in 2026: USD 1.3 Billion

- Projected market size by 2033: USD 2.1 Billion

- CAGR (2026-2033): 7.6%

In addition, the expanding use of dialysis and extracorporeal membrane oxygenation (ECMO) procedures is contributing to sustained market demand. Activated Clotting Time (ACT) testing is extensively used across hospitals, cardiac catheterization laboratories, and critical care units to enable real-time monitoring of anticoagulation during complex procedures. Clinical data suggests that ACT tests are frequently performed in operating rooms during cardiac surgeries (32.4%) and cardiac catheterization procedures (32.3%), highlighting its strong and widespread clinical adoption.")

The rising global burden of cardiovascular diseases, including coronary artery disease, myocardial infarction, and thrombosis, is a key driver of growth in the ACT testing market. These conditions frequently require surgical and interventional procedures such as cardiac catheterization, angioplasty, and cardiopulmonary bypass, where effective anticoagulation management is critical. During these procedures, patients are administered high doses of anticoagulants, particularly heparin, to prevent thrombus formation within blood vessels and medical devices. However, maintaining the optimal balance of anticoagulation is essential, as excessive dosing can lead to severe bleeding complications. As a result, ACT testing is widely utilized to provide a rapid, real-time assessment of clotting time, enabling clinicians to monitor and adjust anticoagulation therapy effectively.

With the increasing prevalence of cardiovascular diseases globally, there has been a corresponding rise in the volume of cardiac surgeries and interventional procedures. This trend is directly driving demand for ACT testing devices and consumables across hospitals and cardiac catheterization laboratories. For instance, according to the World Health Organization (WHO), global cardiovascular disease cases increased from approximately 311 million in 1990 to around 626 million in 2023, resulting in nearly 19.8 million deaths annually. This increasing disease burden continues to strengthen the need for reliable anticoagulation monitoring solutions, thereby supporting sustained growth in the ACT testing market.

The growing adoption of point-of-care (POC) diagnostics is a key factor driving the market, as it enables rapid bedside testing and faster clinical decision-making. POC ACT testing allows real-time monitoring of anticoagulation during procedures such as surgeries, dialysis, and ECMO, enabling clinicians to promptly adjust anticoagulant dosing and reduce the risk of bleeding or clotting complications. Its ability to improve workflow efficiency, minimize sample transport, and support minimally invasive procedures has further accelerated its use. As healthcare systems increasingly shift toward decentralized diagnostics, demand for portable and automated ACT testing devices continues to rise, supported by the growing adoption of advanced systems such as the i-STAT platform in operating room settings.

Moreover, the increasing number of surgical procedures, particularly minimally invasive surgeries, is propelling the growth of the market. Minimally invasive techniques, such as laparoscopic and catheter-based interventions, are widely adopted due to their benefits, including reduced recovery time, lower risk of complications, and shorter hospital stays. However, these procedures often require precise anticoagulation management to prevent clot formation while minimizing bleeding risks. ACT testing is extensively used to provide rapid, real-time monitoring of clotting status during such interventions. With the global shift toward minimally invasive approaches and the rising volume of surgical procedures, the demand for ACT testing devices and consumables continues to increase across hospitals and surgical centers.

Market Concentration & Characteristics

The degree of innovation in the activated clotting time testing diagnostics market is moderate, driven by ongoing advancements in automated, portable, and point-of-care devices that enable rapid, accurate, and real-time anticoagulation monitoring. Key innovations include pre-calibrated cartridges, user-friendly digital interfaces, integration with hospital information systems, and emerging AI-assisted analytics, all of which enhance operational efficiency, minimize human error, and support faster clinical decision-making. These developments have improved the accessibility and usability of ACT testing across operating rooms, catheterization laboratories, and critical care settings, thereby supporting increased global adoption.

The Activated Clotting Time (ACT) testing market shows a moderate level of merger and acquisition activity, with key players focusing on strategic initiatives to strengthen their market position and expand their product portfolios. Companies are increasingly pursuing acquisitions and collaborations with point-of-care (POC) technology providers to enhance rapid testing capabilities and broaden their presence in coagulation diagnostics. For instance, in July 2024, Roche acquired select point-of-care testing assets from LumiraDx to strengthen its rapid diagnostics portfolio. Such transactions highlight ongoing consolidation trends within the broader POC diagnostics space, which also support the growth of coagulation assays, including ACT testing. Additionally, strategic partnerships between diagnostic companies and technology providers are enabling advancements in product development and expanding distribution networks, facilitating the delivery of more integrated solutions for anticoagulation monitoring.

The regulatory impact on the activated clotting time testing market is significantly influenced by variability and the lack of standardized testing protocols. The absence of universally accepted ACT thresholds and differences in results across point-of-care devices can lead to inconsistencies in clinical decision-making, highlighting the need for device-specific reference ranges. Regulatory requirements often mandate testing by trained personnel in controlled settings, which may limit true bedside use and introduce delays affecting outcomes. In addition, evolving guidelines from organizations such as ELSO and ISTH are emphasizing stricter anticoagulation control and, in some cases, shifting toward alternative monitoring methods such as anti-Xa assays. Despite high precision within individual devices, variability across technologies underscores the need for greater standardization to ensure consistent and reliable patient management.

Product expansion in the Activated Clotting Time (ACT) testing market is moderate to low, with companies focusing on enhancing existing platforms to improve performance and usability. Key players such as Werfen (Instrumentation Laboratory) have introduced advanced ACT systems with improved optics, better sample handling, and expanded test menus, including ACT+ and ACT-LR, to deliver faster and more reliable results. In addition, systems such as the GEM Hemochron 100 whole blood hemostasis system have received U.S. FDA 510(k) clearance, enabling rapid point-of-care testing and more efficient clinical workflows. The market has also seen the introduction of portable ACT devices that support real-time coagulation monitoring outside central laboratories, particularly in surgical and critical care settings. Furthermore, advancements in reagents and consumables are improving accuracy, reducing turnaround time, and supporting wider adoption across various clinical environments.

The Activated Clotting Time (ACT) testing market demonstrates strong regional variation, with North America leading due to high healthcare spending, well-established hospital infrastructure, and a significant burden of cardiovascular diseases. The U.S. remains a key contributor, driven by the adoption of advanced and automated diagnostic technologies. Europe represents a stable market, supported by developed laboratory infrastructure, stringent regulatory standards, and consistent demand for coagulation monitoring solutions. The Asia-Pacific region is expected to witness the fastest growth, fueled by improving healthcare access, rising disposable incomes, and increasing healthcare investments in countries such as China and India. Meanwhile, regions such as Latin America and the Middle East are emerging as growth opportunities, supported by ongoing healthcare infrastructure development and increasing adoption of modern diagnostic technologies.

Product Insights

Consumables segment dominated the market and accounted for the largest revenue share of 87.99% in 2025 and is anticipated to grow at the fastest growth rate during the forecast period. The dominance of the segment is attributed to the increasing adoption of point-of-care coagulation testing devices, the rising prevalence of cardiovascular and bleeding disorders, and the growing demand for rapid anticoagulation monitoring in surgical and critical care settings. Moreover, the recurring demand for reagents, cartridges, and test kits required for each coagulation test, as well as the increasing volume of surgical procedures and anticoagulation monitoring, is further propelling the market growth. In addition, hospitals and diagnostic laboratories rely heavily on consumables because they ensure test accuracy, compatibility with point-of-care devices, and efficient workflow in clinical settings.

ACT Analyzer segment is likely to grow with lucrative growth over the forecast period, due to the increasing number of cardiovascular and surgical procedures that require rapid coagulation monitoring. The rising prevalence of heart diseases and the growing use of anticoagulant therapies during procedures such as cardiac surgery, catheterization, and dialysis are driving demand for accurate point-of-care testing devices. In addition, technological advancements have improved the speed, portability, and reliability of ACT analyzers, making them more suitable for critical care settings. Expanding healthcare infrastructure and greater adoption of point-of-care diagnostics in hospitals and clinics further support the growth of the segment.

Test Type Insights

In 2025, the High-range ACT tests segment accounted for the largest revenue share of 68.14% and is anticipated to grow at the fastest growth rate over the forecast period. This growth is primarily driven by the increasing volume of complex cardiac surgeries and interventional procedures that require monitoring of high-dose heparin therapy. The widespread adoption of point-of-care devices capable of accurately measuring elevated clotting times, along with the growing focus on real-time anticoagulation management in critical care and extracorporeal procedures, further supports segment expansion. High-range ACT tests are particularly preferred in procedures such as cardiopulmonary bypass and ECMO, where precise monitoring of elevated anticoagulation levels is essential to ensure patient safety and optimize clinical outcomes.

The low-range ACT tests segment is expected to witness strong growth over the forecast period, driven by the increasing need for precise coagulation monitoring in procedures involving lower levels of anticoagulation. These tests are widely used in cardiac catheterization, percutaneous interventions, and routine anticoagulation management, where lower doses of heparin require accurate, real-time assessment. Low-range ACT testing enables clinicians to quickly evaluate clotting time and adjust therapy as needed, reducing the risk of both bleeding and thrombotic complications. The rising number of minimally invasive cardiovascular procedures, along with the growing prevalence of cardiovascular diseases, is further supporting segment growth. In addition, advancements in point-of-care diagnostic technologies and a greater focus on patient safety and procedural efficiency are expected to drive continued adoption.

Application Insights

In 2025, the hemodialysis segment led the market, accounting for 48.38% of the revenue share, and is anticipated to grow with the fastest growth over the forecast period. This growth is driven by the increasing prevalence of chronic kidney disease and the rising number of patients undergoing hemodialysis, all of whom require continuous anticoagulation monitoring. ACT testing plays a critical role in dialysis settings by enabling real-time monitoring of clotting time, allowing clinicians to adjust heparin dosing to prevent clot formation in the extracorporeal circuit while minimizing the risk of bleeding. The growing adoption of point-of-care ACT devices in dialysis centers further supports this trend, as these systems offer rapid results, reduce reliance on central laboratories, and improve overall treatment efficiency and patient safety.

The cardiovascular surgery segment is expected to witness significant growth over the forecast period, driven by the rising prevalence of cardiovascular diseases and the increasing number of procedures such as coronary artery bypass grafting, valve replacement, and other complex cardiac surgeries. These procedures require continuous and accurate monitoring of coagulation to maintain optimal anticoagulation levels and ensure patient safety. Activated Clotting Time (ACT) testing plays a critical role in managing heparin therapy and reducing the risk of complications, including excessive bleeding and clot formation. In addition, advancements in surgical techniques, the growing adoption of minimally invasive cardiac procedures, and improvements in healthcare infrastructure are further supporting demand for effective coagulation monitoring solutions, contributing to the segment’s growth.

End-use Insights

In 2025, the hospitals segment accounted for the largest share of the Activated Clotting Time (ACT) testing market, contributing 75.05% of total revenue, and is expected to grow at the fastest rate during the forecast period. This dominance is driven by the high volume of complex surgical procedures, cardiac interventions, and critical care cases performed in hospital settings, all of which require real-time anticoagulation monitoring. Hospitals are increasingly adopting point-of-care ACT devices to support rapid clinical decision-making, minimize procedural delays, and enhance patient safety. Furthermore, the presence of skilled healthcare professionals, well-established laboratory infrastructure, and the integration of ACT testing into routine clinical workflows continue to strengthen the position of hospitals as the leading end-use segment.

The ambulatory surgical centers (ASCs) segment is expected to witness strong growth over the forecast period, driven by the increasing number of minimally invasive and outpatient procedures, along with rising patient preference for same-day surgeries. The growing adoption of point-of-care ACT testing devices in ASCs is further supporting this trend, as these facilities increasingly perform procedures that require effective anticoagulation management. ACT testing enables rapid, real-time monitoring of clotting status, allowing clinicians to adjust heparin dosing during procedures, improve patient safety, and minimize delays. The portability, ease of use, and quick turnaround time of these devices make them well-suited for outpatient settings. Additionally, the ongoing shift toward decentralizing surgical care from hospitals to outpatient centers, aimed at reducing costs and improving efficiency, is expected to further drive demand for ACT testing solutions in ambulatory surgical centers.

Regional Insights

North America dominated the global Activated Clotting Time (ACT) testing market, accounting for 39.08% of the total revenue share in 2025. Growth in the region is driven by well-established healthcare infrastructure and high healthcare spending, which support the rapid adoption of advanced diagnostic technologies. The increasing prevalence of cardiovascular and blood-related disorders, along with a high volume of complex procedures such as cardiac surgeries, ECMO, and vascular interventions, is further driving demand for accurate, real-time ACT monitoring. In addition, the strong adoption of point-of-care testing devices, integration of advanced digital solutions with hospital systems, and the presence of major market players such as Abbott, Haemonetics, and HemoSonics continue to strengthen North America’s leading position in the market.

U.S. Activated Clotting Time Testing Market Trends

The U.S. accounted for the largest share of the North American Activated Clotting Time (ACT) testing market in 2025, driven by its advanced healthcare infrastructure, high healthcare expenditure, and widespread adoption of point-of-care and automated coagulation testing technologies. The region continues to benefit from well-established hospital systems, a high prevalence of cardiovascular and blood-related disorders, and strong uptake of rapid testing solutions that enable real-time anticoagulation monitoring. Additionally, the presence of leading market players, supportive reimbursement frameworks, and the growing integration of digital diagnostic solutions further strengthen the U.S. market within North America.

Europe Activated Clotting Time Testing Market Trends

The Europe Activated Clotting Time (ACT) testing market is experiencing steady growth, driven by the increasing prevalence of cardiovascular diseases, a rapidly aging population, and the growing adoption of point-of-care (POC) testing for effective anticoagulation monitoring during surgical procedures. The high burden of conditions such as coronary heart disease, stroke, and deep vein thrombosis is contributing to increased demand for ACT testing, while the shift toward rapid bedside diagnostics in hospitals and emergency care settings is further supporting market expansion across the region.

The Germany activated clotting time testing market is expanding due to its advanced healthcare infrastructure, rising investments in hospital technologies, and increasing emphasis on accurate coagulation monitoring in surgical and critical care settings. The demand for precise, automated, and reliable ACT testing solutions that integrate seamlessly into hospital workflows is driving adoption, particularly in cardiac catheterization laboratories, intensive care units, and surgical centers. Strong diagnostic capabilities and a focus on preventive healthcare further support steady market growth in the country.

Activated clotting time testing market in the UK is expected to witness significant growth over the forecast period, driven by the rising number of cardiac surgeries, an increasing geriatric population, and a growing focus on bedside diagnostic solutions. The widespread adoption of point-of-care ACT testing devices across hospitals, ambulatory surgical centers, and critical care units is accelerating, as healthcare providers prioritize rapid, accurate, and reliable coagulation monitoring to enhance patient safety and improve clinical efficiency.

Asia Pacific Activated Clotting Time Testing Market Trends

The Asia Pacific ACT testing market is projected to witness the fastest growth, registering a CAGR of 9.17% over the forecast period. This growth is driven by the rising prevalence of cardiovascular diseases, rapid urbanization, increasing healthcare expenditure, and improving access to advanced diagnostic technologies. Key markets such as China, Japan, and India are experiencing increased adoption of point-of-care (POC) ACT testing devices across hospitals, critical care units, cardiac catheterization laboratories, and dialysis centers, supported by the growing need for real-time coagulation monitoring and improved patient outcomes. In Japan, market growth is further supported by advanced healthcare infrastructure, a growing aging population, and increasing demand for minimally invasive procedures. The integration of ACT testing into surgical and critical care workflows, along with a strong focus on patient safety and timely anticoagulation monitoring, is driving adoption across hospitals and clinical laboratories.

Latin America Activated Clotting Time Testing Market Trends

The Latin America ACT testing market is experiencing steady growth, driven by the increasing number of cardiovascular procedures and the growing adoption of point-of-care (POC) testing devices. Healthcare facilities are increasingly upgrading to automated and user-friendly POC analyzers to reduce turnaround times and enhance patient safety, particularly in surgical and intensive care settings. Improved access to advanced diagnostic technologies, rising healthcare expenditure, and increasing awareness of anticoagulation monitoring are further supporting market expansion. Countries such as Brazil and Argentina are leading adoption, supported by ongoing improvements in healthcare infrastructure and a greater focus on clinical efficiency.

Middle East & Africa Activated Clotting Time Testing Market Trends

The Middle East & Africa ACT testing market is expanding, supported by ongoing healthcare infrastructure development, increasing adoption of point-of-care (POC) devices, and a rising number of cardiovascular surgeries. Key countries such as Saudi Arabia, the UAE, Egypt, and South Africa are driving regional growth due to the presence of advanced healthcare facilities and growing investments in medical diagnostics. Increasing awareness of blood disorders, a rising aging population, and the need for effective anticoagulation monitoring are further contributing to market growth. Additionally, the adoption of rapid, automated, and easy-to-use POC coagulation testing systems, along with technological advancements and strategic partnerships, is enhancing accessibility and supporting overall market expansion.

Key Activated Clotting Time Testing Company Insights

The Activated Clotting Time (ACT) testing market is highly competitive, with leading players focusing on strengthening their market position through continuous product innovation and strategic initiatives. Companies are investing in advanced automated analyzers, portable point-of-care (POC) devices, assay standardization, and integrated workflow solutions to enable accurate and rapid anticoagulation monitoring. Market participants are also expanding their portfolios and forming strategic partnerships and collaborations with hospitals and healthcare networks to enhance testing efficiency and clinical adoption.

The growing focus on cardiovascular care, increasing volume of surgical procedures, and the need for real-time anticoagulation monitoring are further driving demand across hospitals and critical care settings. Key systems offered by leading players, such as Werfen’s Hemochron, Medtronic’s HMS Plus/ACT Plus, and Abbott’s i-STAT, are widely used for heparin monitoring during cardiac surgeries and interventional procedures. In addition, newer solutions such as the Werfen GEM Hemochron (GH100) are gaining traction by offering faster results, lower sample volume requirements, and improved cost efficiency, intensifying competition within the market.

Key Activated Clotting Time Testing Companies:

The following key companies have been profiled for this study on the activated clotting time (ACT) testing market.

- Werfen

- Medtronic

- Helena Laboratories Corporation

- Abbott

- Sienco, Inc.

- F. Hoffmann-La Roche Ltd

- Sysmex Corporation

- Danaher Corporation

- Thermo Fisher Scientific Inc.

- Siemens Healthineers AG

- SEKISUI

Recent Developments

-

In March 2025, Siemens Healthineers announced U.S. FDA clearance of its INNOVANCE Antithrombin assay as a companion diagnostic for Qfitlia (fitusiran), a hemophilia therapy developed by Sanofi. The assay is used to measure antithrombin activity levels, enabling clinicians to monitor patients and adjust dosing during treatment, thereby supporting personalized anticoagulation management.

-

In January 2022, Werfen announced that its GEM Hemochron 100 Whole Blood Hemostasis Testing System received U.S. FDA 510(k) clearance. The system enables rapid Activated Clotting Time (ACT) testing at the point of care, delivering results within minutes to support effective heparin management during procedures such as cardiac surgery and catheterization.

Activated Clotting Time Testing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.2 billion

Estimated market size in 2026

USD 1.3 billion

Projected market size by 2033

USD 2.1 billion

Growth rate

CAGR of 7.6% from 2026 to 2033

Actual Data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, test type, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; Australia; Thailand; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Werfen; Medtronic; Helena Laboratories Corporation; Abbott;Sienco, Inc.; F. Hoffmann-La Roche Ltd; Sysmex Corporation; Danaher Corporation; Thermo Fisher Scientific Inc.; Siemens Healthineers AG; SEKISUI Diagnostics.

Customization scope

Free report customization (equivalent up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Activated Clotting Time Testing Market Report Segmentation

This report forecasts revenue growth at country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global activated clotting time testing market report on the basis of product, test type, application, end-use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

ACT Analyzers

-

Consumables (Cartridges, Tubes, Reagents)

-

-

Test Type Outlook (Revenue, USD Million, 2021 - 2033)

-

High-Range ACT Tests

-

Low-Range ACT Tests

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Cardiovascular Surgery

-

Interventional Cardiology

-

Extracorporeal Membrane Oxygenation (ECMO)

-

Hemodialysis

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospital

-

Ambulatory Surgical Centers

-

Clinical Laboratories

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Norway

-

Denmark

-

Sweden

-

Rest of Europe

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

Rest of Asia Pacific

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

Rest of Middle East & Africa

-

-

Frequently Asked Questions About This Report

The global activated clotting time testing market size was estimated at USD 1.2 billion in 2025 and is expected to reach USD 1.3 billion in 2026.

The global activated clotting time testing market is expected to grow at a compound annual growth rate of 7.6% from 2026 to 2033 to reach USD 2.1 billion by 2033.

North America dominated the activated clotting time testing market with a share of 39.1% in 2025.

Some key players operating in the activated clotting time testing market include Werfen, Medtronic, Helena Laboratories Corporation, Abbott Sienco, Inc., F. Hoffmann-La Roche Ltd ,Sysmex Corporation Danaher Corporation ,Thermo Fisher Scientific Inc., Siemens Healthineers AG ,SEKISUI Diagnostics.

Key factors that are driving the market growth include the increasing cardiovascular disease prevalence, growing adoption of point of care diagnostics, and a steady increase in the number of surgical procedures particularly minimally invasive surgeries.

The consumables segment led with a 87.9% revenue share in 2025.

High-range ACT tests held the largest revenue share 68.1% in 2025.

Hemodialysis held the largest share (over 48.4%) in 2025.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.