- Home

- »

- Agrochemicals & Fertilizers

- »

-

Agroforestry Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Agroforestry Market (2026 - 2033)Report]()

Agroforestry Market (2026 - 2033)

Size, Share & Trends Analysis Report By System (Agrisilvicultural Systems, Silvopastoral Systems), By Product, By Region, And Segment Forecasts

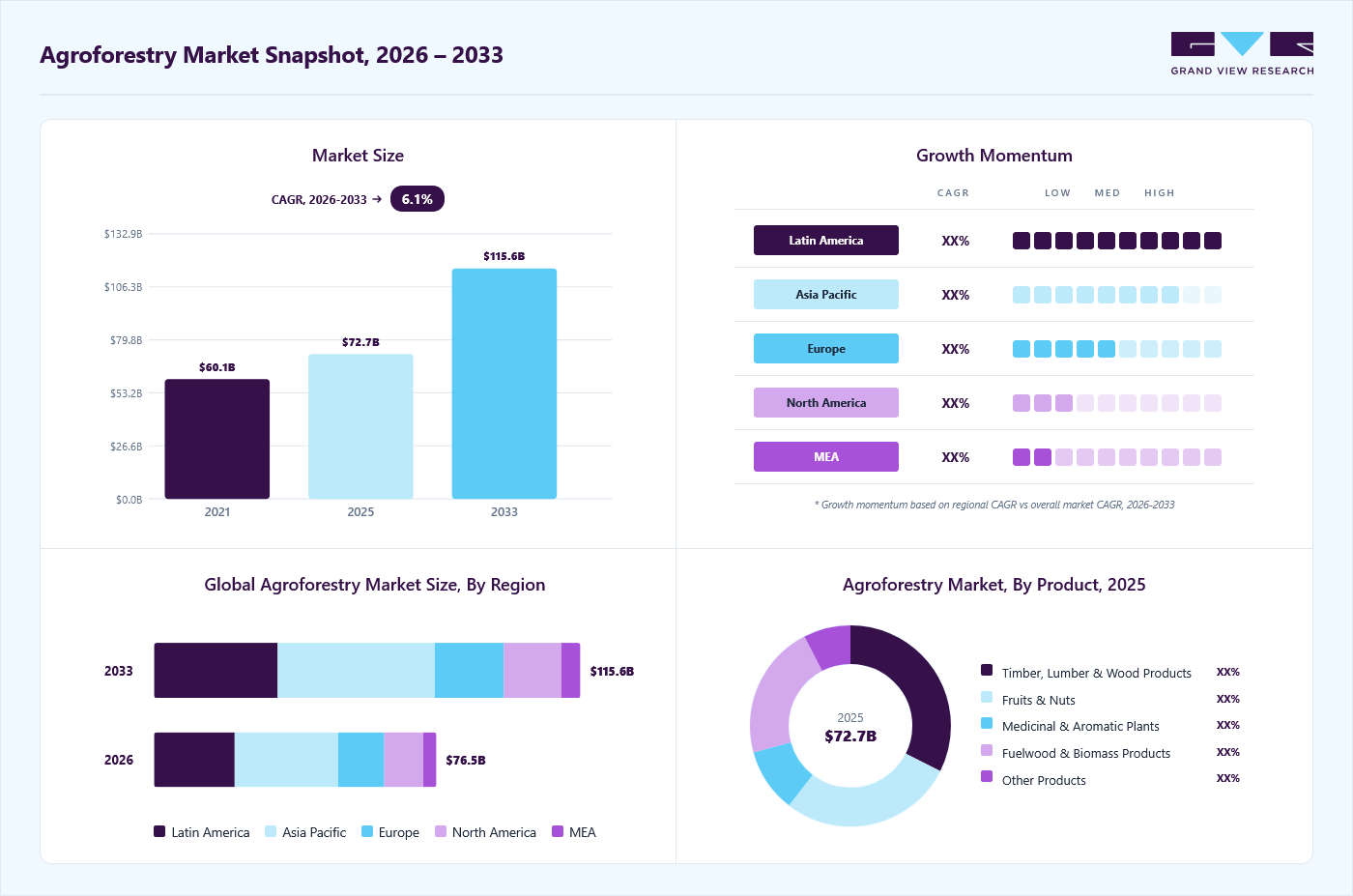

Market Size, 2025

$72.7BMarket Estimate, 2026

$76.5BMarket Forecast, 2033

$115.6BCAGR, 2026–2033

6.1%Agroforestry Market Summary

The global agroforestry market size was valued at USD 72.7 billion in 2025 and is projected to grow from USD 76.5 billion in 2026 to USD 115.6 billion by 2033, at a CAGR of 6.1% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 36.6% in 2025. The market is gaining momentum as producers and buyers prioritize production models that can improve long-term farm economics while strengthening land resilience.

Key Market Trends & Insights

- By system: Agrisilvicultural systems segment held the largest market share of 50.9% in 2025.

- By product: Timber, lumber & wood products segment held the largest market share of 32.4% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (36.6% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 72.7 Billion

- Estimated market size in 2026: USD 76.5 Billion

- Projected market size by 2033: USD 115.6 Billion

- CAGR (2026-2033): 6.1%

Agroforestry adoption is rising because it generates multi-cycle revenue from the same land base, while improving soil structure, water efficiency, and productivity stability under changing climate conditions.Market expansion is strongly linked to the ability of agroforestry systems to diversify output and reduce dependence on single commodity cycles. Farms integrating trees with crops and livestock can monetize timber, fruits, biomass, and specialty non-timber products alongside annual harvests. This structure improves cash flow consistency and lowers exposure to seasonal yield losses. As cost pressures rise across fertilizers, irrigation, and land management, agroforestry becomes a strategic pathway to improve profitability through biological efficiency rather than input intensification.

")

Buyers across food, beverage, forestry products, and natural ingredients are aligning procurement with traceable and low-impact sourcing models. Agroforestry supports these expectations by combining production with ecosystem restoration outcomes, enabling suppliers to meet sustainability benchmarks without reducing commercial output. This shift is increasing the attractiveness of certified production and long-term sourcing relationships, which strengthens revenue realization across agroforestry-linked value chains.

Investment activity further accelerates market development as financing flows toward regenerative systems that provide both agricultural returns and measurable environmental value. Carbon-linked payments, ecosystem service monetization, and blended finance mechanisms are improving the payback profile for tree establishment and long-term maintenance. This trend is visible in structured land restoration programs as well as private sector initiatives, including agroforestry in USA projects and localized adoption, such as agroforestry Maine initiatives, which demonstrate growing commercial interest in scalable tree-based farming systems.

Market Concentration & Characteristics

The market for agroforestry remains highly fragmented, shaped more by land ownership patterns and agricultural supply chains than by a centralized set of manufacturers. Commercial activity is distributed across smallholder farmers, cooperatives, plantation operators, and forestry-linked businesses, with value creation occurring through diversified outputs such as timber, tree crops, biomass, and non-timber forest products. As a result, the market is characterized by dispersed production and limited pricing standardization.

Market participation is also influenced by institutional support, certification networks, and project developers that enable access to financing and sustainability-linked procurement. Adoption depends heavily on technical expertise, local climate suitability, and long-term land planning, which creates variation in product quality and revenue potential. Innovation is increasingly driven by improved planting material, farm advisory services, and monitoring tools.

System Insights

The agrisilvicultural systems segment dominated the market in 2025, accounting for 50.9% of total revenue, primarily because of their operational simplicity and compatibility with conventional crop farming models. Farmers can incorporate timber or fruit-bearing trees into existing cropland with limited disruption to machinery use, labor allocation, or annual planting schedules. This flexibility lowers transition risk and reduces upfront restructuring costs. The system delivers dual revenue streams by combining annual crop income with medium- to long-term tree harvest returns, which enhances financial stability. Its scalability and lower complexity make it the most commercially established agroforestry configuration.

The agrosilvopastoral systems segment is projected to record the fastest growth, with a CAGR of 6.8% from 2026 to 2033, as it maximizes land productivity through the simultaneous integration of crops, livestock, and tree components. This model enhances overall farm efficiency by generating diversified outputs while optimizing nutrient cycling and natural resource utilization. Livestock benefit from improved shade and fodder availability, which can increase productivity and reduce stress-related losses. As producers seek higher per-hectare returns and stronger climate resilience, this integrated approach is gaining attention as a long-term strategy for sustainable profitability.

Product Insights

The timber, lumber & wood products segment led the market in 2025, accounting for 32.4% of total revenue. This segment held the largest share because wood remains one of the most commercially structured and monetizable outputs within agroforestry systems. Timber provides high absolute value per harvest cycle and integrates efficiently into established processing, distribution, and export networks. In many integrated farming models, trees function as long-term capital assets that appreciate over time while supporting soil improvement during growth. The presence of organized buyers and grading standards also improves price realization, making wood-based outputs more financially predictable compared to seasonal or niche products.

The medicinal & aromatic plants segment is expected to grow at the fastest rate, with a CAGR of 7.6% from 2026 to 2033. Growth in this segment reflects shifting consumer demand toward plant-derived ingredients in healthcare, personal care, and functional food applications. These crops typically command premium pricing and can be cultivated within understory or mixed-tree environments, enhancing land-use efficiency. Their shorter cultivation cycles compared to timber allow faster revenue generation, which improves return visibility for farmers. Expanding processing capacity and increasing formalization of botanical supply chains are further strengthening commercial scalability, positioning this segment as a high-growth opportunity within diversified agroforestry systems.

Regional Insights

Asia Pacific agroforestry industry held the largest share of the market in 2025, accounting for 36.6% of revenue. This leadership position reflects the region’s strong integration of tree-based systems within commercial agriculture and forestry-linked value chains. A large base of small and mid-sized farms practices diversified production that combines timber, fruits, nuts, and biomass outputs. The presence of organized domestic demand alongside export-oriented supply chains improves revenue realization. Continuous farm intensification, coupled with increasing emphasis on soil restoration and long-term land productivity, supports sustained commercial scale in agroforestry operations across the region.

China agroforestry industry benefits from large-scale ecological restoration initiatives and strong domestic demand for timber, fruits, and medicinal plants. Integrated tree-crop systems are widely used to improve land productivity in both commercial plantations and smallholder settings. Government-backed reforestation and land rehabilitation programs reinforce tree integration within agricultural landscapes. Established processing capacity for wood products and botanical ingredients improves value capture, positioning agroforestry as both a production and land restoration strategy within the country’s agricultural framework.

North America Agroforestry Market Trends

The North America agroforestry industry is shaped by increasing adoption of regenerative land management practices and diversified farm income strategies. Producers are integrating trees into cropland and pasture to improve soil carbon, reduce erosion, and stabilize long-term yields. Structured supply chains for timber, specialty crops, and biomass support commercialization, while sustainability-linked procurement standards encourage traceable production. Carbon programs and conservation incentives are improving the financial case for tree establishment, making agroforestry more attractive to commercial operators seeking both productivity gains and environmental performance.

U.S. Agroforestry Market Trends

U.S. agroforestry industry is influenced by growing interest in soil health, climate resilience, and income diversification across large-scale farming operations. Alley cropping, silvopasture, and windbreak systems are gaining traction as producers look to improve land efficiency without reducing output. Institutional support, technical extension services, and sustainability-aligned food companies are encouraging adoption. Access to developed wood markets and emerging ecosystem service payments enhances monetization potential, strengthening agroforestry’s positioning as a commercially viable long-term land management strategy.

Europe Agroforestry Market Trends

Europe’s agroforestry industry is driven by policy-backed land stewardship goals and strong environmental compliance standards within agricultural systems. Farmers are integrating trees to improve biodiversity performance, reduce soil degradation, and meet sustainability benchmarks required by food and fiber buyers. Mature certification frameworks and premium product positioning enhance revenue realization for agroforestry outputs. While land availability limits rapid expansion, structured support mechanisms and sustainability-focused procurement continue to encourage steady adoption across mixed farming landscapes.

Latin America Agroforestry Market Trends

Latin America agroforestry industry is projected to grow at the fastest rate, with a CAGR of 6.3% from 2026 to 2033. The region’s growth outlook is driven by expanding commercialization of tree-crop systems and integrated livestock models that enhance land-use efficiency. Agroforestry practices are increasingly linked with high-value export commodities and sustainability-aligned procurement standards. As producers focus on improving productivity while preserving ecological assets, integrated farming systems are gaining stronger financial justification. Improved traceability, certification frameworks, and private investment participation are expected to accelerate structured expansion in agroforestry-based production.

Middle East & Africa Agroforestry Market Trends

The Middle East & Africa agroforestry industry is expanding as land restoration and climate adaptation priorities reshape agricultural practices. Tree integration is widely used to improve soil fertility, reduce desertification risks, and support smallholder income diversification. While monetization levels vary, growing participation from development finance institutions and private sustainability programs is improving market structure. Increasing attention to drought resilience and long-term land productivity is encouraging broader adoption of integrated tree-based farming systems across the region.

Key Agroforestery Company Insights

The two key dominant manufacturers in the market are Weyerhaeuser Company and Stora Enso.

-

Weyerhaeuser Company operates as a major forest products producer with strong capabilities in timber harvesting and wood processing. The company focuses on sustainably managed forestlands and generates commercial output across lumber and engineered wood categories. Its scale and established forestry operations support long-term wood production and value-added processing aligned with construction and industrial demand.

-

Stora Enso is a leading wood-based products manufacturer with a strong focus on renewable materials derived from forest resources. The company produces a broad portfolio of wood products and pulp-based solutions, supporting demand across packaging, construction, and bio-based applications. Its emphasis on renewable forestry resources strengthens its role in commercial wood product production markets.

Key Agroforestry Companies:

The following key companies have been profiled for this study on the agroforestry market.

- Weyerhaeuser Company

- ArborGen LLC

- EcoPlanet Bamboo

- Green Resources AS

- Stora Enso

- Suzano S.A.

- West Fraser Timber Co. Ltd.

- Gratitude Farms

- Natba Greene

- Mul Biotech Farms

Recent Developments

-

In December 2025, the USDA announced a $700 million Regenerative Pilot Program to reduce farmer production costs and promote regenerative practices improving soil health, water quality, and long-term productivity. HHS will fund research linking regenerative agriculture to public health under the MAHA strategy.

-

In December 2025, Kenya launched its National Agroforestry Strategy (2025-2035), a ten-year framework to scale tree-based farming, restore degraded landscapes, enhance climate resilience, and improve smallholder livelihoods through coordinated public, private, and research sector support.

Global Agroforestry Market Report Scope

Report Attribute

Details

Market size in 2025

USD 72.7 billion

Estimated market size in 2026

USD 76.5 billion

Projected market size by 2033

USD 115.6 billion

Growth rate

CAGR of 6.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2018 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

System, product, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Brazil; Argentina; Germany; UK; Italy; Spain; France; China; Japan; South Korea; Saudi Arabia; South Africa

Key companies profiled

Weyerhaeuser Company; ArborGen LLC; EcoPlanet Bamboo; Green Resources AS; Stora Enso; Suzano S.A.; West Fraser Timber Co. Ltd.; Gratitude Farms; Natba Greene; Mul Biotech Farms

Customization scope

Free report customization (equivalent to up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Agroforestry Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global agroforestry market report based on system, product, and region

-

System Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2033)

-

Agrisilvicultural Systems

-

Silvopastoral Systems

-

Agrosilvopastoral Systems

-

Other Systems

-

-

Product Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2033)

-

Timber, Lumber & Wood Products

-

Fruits & Nuts

-

Medicinal & Aromatic Plants

-

Fuelwood & Biomass Products

-

Other Products

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

Spain

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

Timber, lumber & wood products held the largest revenue share 32.4% in 2025.

Asia Pacific dominated with a 36.6% revenue share in 2025.

The global agroforestry market size was estimated at USD 72.7 billion in 2025 and is expected to reach USD 76.5 billion in 2026.

The global agroforestry market is expected to grow at a compound annual growth rate of 6.1% from 2026 to 2033, reaching USD 115.6 billion by 2033.

Agrisilvicultural systems segment dominated the market in 2025, accounting for 50.9% of total revenue.

Some of the key players operating in the agroforestry market include Weyerhaeuser Company, ArborGen LLC, EcoPlanet Bamboo, Green Resources AS, Stora Enso, Suzano S.A., West Fraser Timber Co. Ltd., Gratitude Farms, Natba Greene, Mul Biotech Farms.

The market is gaining momentum as producers and buyers prioritize production models that can improve long-term farm economics while strengthening land resilience. Agroforestry adoption is rising because it generates multi-cycle revenue from the same land base, while improving soil structure, water efficiency, and productivity stability under changing climate conditions.

About the Author(s)

Agrochemicals & Fertilizers Research Team

Bulk Chemicals · Agrochemicals & FertilizersThis report was authored by the agrochemicals & fertilizers research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the agrochemicals & fertilizers segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.