- Home

- »

- Next Generation Technologies

- »

-

AI Productivity Tools Market Size, Trends Report, 2026-2033GVR Report cover

![AI Productivity Tools Market (2026 - 2033)Report]()

AI Productivity Tools Market (2026 - 2033)

Size, Share & Trends Analysis Report By Offering (Virtual Assistants, RPA, Data Analytics, Document Management), By Deployment (Cloud, On-Premises), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$11.2BMarket Estimate, 2026

$14.1BMarket Forecast, 2033

$36.4BCAGR, 2026–2033

14.5%AI Productivity Tools Market Summary

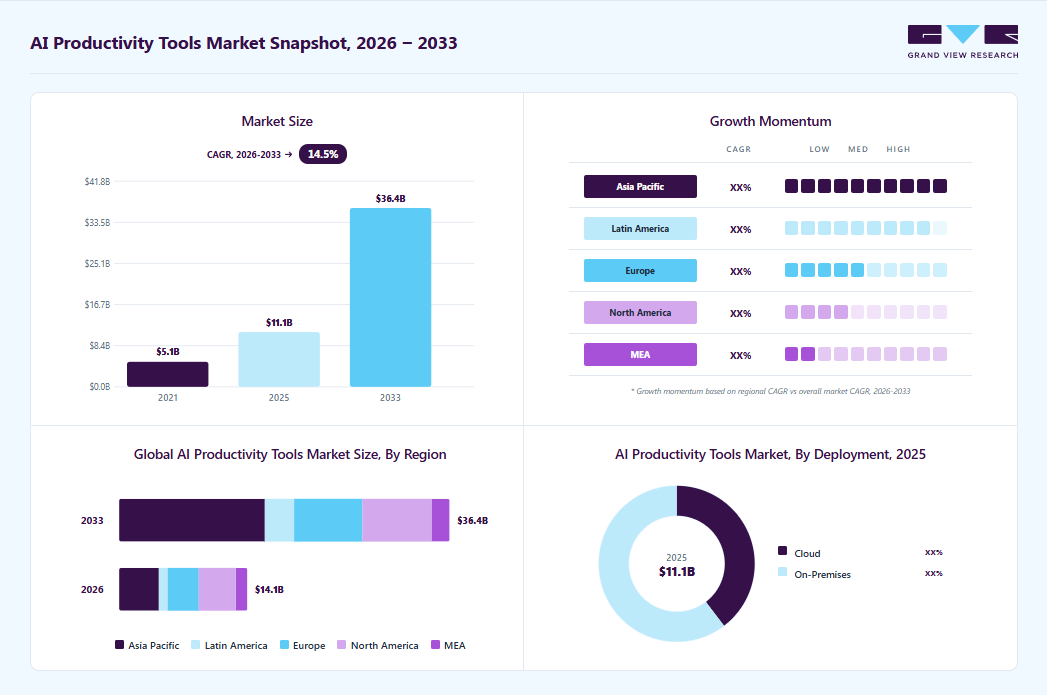

The global AI productivity tools market size was valued at USD 11.2 billion in 2025 and is projected to grow from USD 14.1 billion in 2026 to USD 36.4 billion by 2033, at a CAGR of 14.5% from 2026 to 2033. The market in North America dominated with a revenue share of 30.3% in 2025. Growth is rising due to the wider adoption of generative AI, smarter workflow orchestration, and the integration of AI assistants into business platforms as enterprises automate routine tasks and accelerate workflow efficiency across digital operations.

Key Market Trends & Insights

- By offering: Virtual assistants segment held the largest market share of 25.6% in 2025.

- By deployment: On-premises segment held the largest market share of 60.4% in 2025.

- By end use: IT and telecom segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (30.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 11.2 Billion

- Estimated market size in 2026: USD 14.1 Billion

- Projected market size by 2033: USD 36.4 Billion

- CAGR (2026-2033): 14.5%

The increasing integration of enterprise workflows with cloud-based AI capabilities is accelerating growth in the AI productivity tools market. Organizations across industries are adopting AI-enabled platforms to automate repetitive and complex business processes, reducing operational delays and minimizing manual errors. The ability of AI productivity tools to deliver real-time insights, predictive analytics, and intelligent recommendations is improving decision-making across departments such as customer service, HR, finance, and IT operations. Additionally, the growing shift toward cloud infrastructure is further supporting the adoption of scalable AI productivity solutions that can be deployed across distributed work environments.")

Enterprises are increasingly prioritizing unified platforms that combine workflow management, enterprise data, AI models, and collaboration tools within a single ecosystem to improve efficiency and streamline operations. Prominent initiatives for strategic partnerships between enterprise software providers and cloud companies are also expanding the accessibility of AI-driven workflow automation solutions. For instance, in January 2025, ServiceNow and Google Cloud expanded their partnership to bring the Now Platform and workflows to Google Cloud Marketplace, integrating ServiceNow data with Google’s AI tools to enhance automation and enterprise productivity.

Advancements in NLP are driving the growth of the industry by enabling platforms to better understand and generate human language. Increasing adoption of NLP-powered tools by enterprises to automate tasks such as email management, document processing, meeting transcription, and customer communication, improving operational efficiency and reducing manual effort. AI-driven assistants can prioritize emails, generate contextual responses, and summarize large documents, helping organizations save time and accelerate decision-making. The rising use of virtual assistants and conversational interfaces is also improving user experience through more natural workplace interactions.

Market Dynamics

The growing integration of AI with enterprise workflow automation is significantly driving the adoption of AI productivity tools across industries. Organizations are increasingly deploying AI-powered platforms to automate repetitive and time-consuming tasks such as data entry, scheduling, document management, customer support, and internal communications. This automation helps businesses reduce operational costs, minimize human errors, and improve process efficiency across departments. Enterprises are also using AI-driven workflow systems to streamline collaboration and enhance productivity in hybrid and remote work environments.

In addition, the integration of AI with enterprise applications such as CRM, ERP, HR, and project management platforms enables seamless workflow orchestration and faster decision-making. AI productivity tools provide real-time insights, predictive recommendations, and intelligent task prioritization, helping organizations optimize resource allocation and improve operational performance. The increasing shift toward cloud-based infrastructure is further supporting the scalable deployment of AI-enabled workflow solutions across global enterprises. As companies continue prioritizing digital transformation and operational efficiency, demand for integrated AI productivity tools is expected to grow steadily across multiple business functions.

Many businesses face difficulties in effectively implementing and managing AI-powered platforms due to a shortage of professionals with expertise in AI, data analytics, automation, and workflow integration. Employees without adequate understanding of AI functionalities often struggle to utilize advanced features efficiently, reducing the overall return on investment for enterprises. In addition, resistance to adopting new AI-driven workflows and concerns regarding job displacement further slow organizational acceptance of these technologies.

SMEs enterprises are particularly affected, as they often lack the financial resources required for employee training and upskilling programs related to AI technologies. The rapid pace of AI innovation is also creating a widening skills gap, making it challenging for organizations to keep their workforce updated with evolving tools and applications. As a result, enterprises may continue relying on traditional productivity systems instead of transitioning to AI-enabled platforms. These skills and knowledge gap limits the effective utilization of AI productivity tools and restrain broader market growth across industries.

Organizations are increasingly investing in AI-powered collaboration platforms, virtual assistants, workflow automation tools, and intelligent scheduling systems to improve employee productivity across distributed workforces. These solutions help businesses streamline communication, automate repetitive administrative tasks, and enhance project coordination among teams operating from multiple locations. AI-driven productivity tools also provide real-time insights, task prioritization, and meeting summaries, enabling employees to manage workloads more efficiently and maintain operational continuity.

In addition, enterprises are focusing on improving employee experience and digital workplace efficiency through AI-enabled solutions that support seamless collaboration and faster decision-making. The growing dependence on cloud-based work environments is further accelerating the demand for scalable AI productivity platforms that can integrate with enterprise applications and communication tools. As remote and flexible working structures continue to expand across industries, the demand for intelligent productivity solutions is expected to create substantial market opportunities.

Market Concentration & Characteristics

The AI productivity tools market demonstrates a high degree of innovation due to rapid advancements in generative AI, natural language processing (NLP), workflow automation, and intelligent collaboration technologies. Companies are continuously introducing AI-powered features such as automated content generation, smart scheduling, meeting summarization, predictive analytics, and conversational assistants to improve workplace efficiency. The growing integration of multimodal AI models and enterprise automation platforms is further accelerating product development and competitive differentiation. Continuous investments in AI research and cloud-based AI ecosystems are also driving innovation across enterprise productivity applications.

The AI productivity tools market has a relatively high level of end-user diversification, with adoption expanding across industries such as IT, BFSI, healthcare, retail, education, manufacturing, and professional services. Enterprises of all sizes are implementing AI productivity solutions to improve operational efficiency, employee collaboration, and workflow management. Large enterprises currently account for a significant share of adoption due to higher digital transformation spending and stronger cloud infrastructure capabilities. However, increasing accessibility of cloud-based and subscription-based AI tools is also supporting adoption among small and medium-sized businesses, expanding the overall customer base.

Offering Insights

The virtual assistants segment led the market and accounted for 25.6% of the global revenue in 2025. Organizations are increasingly adopting these solutions to manage large volumes of customer queries, reduce support workloads, and improve response efficiency across digital channels. Advancements in NLP and conversational AI are enabling virtual assistants to deliver more accurate, context-aware, and human-like interactions, improving user experience and reliability. As enterprises continue prioritizing automation, personalized engagement, and productivity optimization, demand for AI-powered virtual assistants is increasing across industries.

The data analytics segment is predicted to foresee significant growth in the forecast period. The segment is emerging due to its ability to deliver actionable business insights and improve operational decision-making. These tools help automate data collection, reporting, and workflow analysis, reducing manual effort while improving productivity and operational efficiency. Advanced predictive analytics capabilities also enable businesses to anticipate market trends, optimize resource allocation, and enhance customer engagement across functions as enterprises continue prioritizing data-driven decision-making and digital transformation.

Deployment Insights

The on-premises segment accounted for the largest market revenue share in 2025, owing to enterprises increasingly prioritizing direct control over sensitive operational and business data. This deployment model also offers greater infrastructure customization, enabling companies to optimize system performance, integrate legacy enterprise applications, and configure workflows to meet specific operational requirements. In addition, concerns regarding external data access, cybersecurity risks, and regulatory compliance continue to support the demand for on-premises AI productivity deployments across large enterprises.

The cloud segment is predicted to foresee significant growth in the forecast period, due to the increasing demand for scalable, flexible, and cost-efficient enterprise solutions. Organizations are rapidly adopting cloud-based AI productivity platforms to reduce infrastructure investments, minimize on-site maintenance requirements, and enable faster deployment across business operations. Cloud environments also enable seamless integration with enterprise applications, continuous AI model updates, and real-time data processing, improving overall operational efficiency.

End Use Insights

The IT and telecom segment accounted for the largest market revenue share in 2025, driven by the rapid adoption of digital transformation initiatives and increasing demand for intelligent workflow automation. AI-driven automation, predictive analytics, and virtual assistants are helping telecom and IT companies optimize workflows, reduce operational costs, and enhance service delivery. The growing need for real-time communication, faster decision-making, and efficient management of large-scale data is further accelerating the adoption of AI productivity platforms across the industry.

The BFSI segment is projected to grow significantly over the forecast period, anticipated by the increasing demand for workflow automation, operational efficiency, and data-driven decision-making. Financial institutions are adopting AI-powered productivity solutions to streamline processes such as customer service, compliance management, fraud detection, document processing, and financial analysis, reducing manual effort and improving accuracy. Advanced AI analytics and intelligent automation tools are helping banks and insurance providers assess risks, identify market trends, and optimize product offerings more effectively.

Regional Insights

The North America AI productivity tools industry dominated the market with 30.3% revenue share in 2025. The market is primarily driven by the early adoption of advanced digital technologies and a strong enterprise focus on workplace automation. Organizations across the region are heavily investing in AI-powered productivity solutions to improve operational efficiency, streamline workflows, and enhance customer engagement. The presence of major technology companies, AI innovators, and cloud service providers is accelerating product development and market expansion across industries.

U.S. AI Productivity Tools Market Trends

The AI productivity tools industry in the U.S. is primarily driven by the strong presence of advanced digital infrastructure and leading AI technology providers. The growing demand for cloud-based enterprise applications, remote work solutions, and intelligent workflow automation is further supporting market expansion in the country. In addition, rising investments in generative AI integration and enterprise digital transformation initiatives are driving the adoption of AI productivity tools across businesses in the U.S.

Europe AI Productivity Tools Market Trends

The AI productivity tools industry in Europe is primarily driven as organizations focus on automation to improve operational efficiency and employee productivity. Businesses across industries are integrating AI-powered solutions to automate repetitive and time-consuming tasks, allowing employees to focus on strategic and higher-value activities. As companies continue prioritizing innovation, workforce optimization, and smart business operations, the adoption of AI productivity tools is expected to expand steadily across Europe.

Asia Pacific AI Productivity Tools Market Trends

The AI productivity tools industry in the Asia Pacific is expected to experience the fastest CAGR during the forecasted period, due to the rapid pace of digital transformation and increasing investments in advanced technologies across emerging and developed economies. The strong expansion of SMEs and large enterprises is driving demand for AI-powered productivity solutions to improve workflow efficiency, automate business processes, and enhance employee collaboration across industries. The increasing focus on automation, scalable cloud-based solutions, and enterprise digitalization is expected to continue accelerating the adoption of AI productivity tools across the Asia Pacific.

Key AI Productivity Tools Company Insights

Some key companies in the AI productivity tools industry are Cisco Systems, Inc., Grammarly Inc., Dropbox Inc., and Automation Anywhere, Inc.

-

Cisco Systems, Inc. has focused on integrating AI capabilities into its collaboration and networking solutions to enhance productivity. The company leverages AI-driven analytics to optimize enterprise network performance and support decision-making. Its platforms include virtual assistants and automation tools to streamline workflows for IT and business teams. Cisco’s investments in AI-powered security and communication tools strengthen its market presence.

-

Dropbox Inc. has enhanced its cloud storage and collaboration platform with AI-powered productivity features. The company uses AI to automate file organization, improve search functionality, and support content recommendations. Integration with virtual assistants and workflow automation tools helps users manage tasks more efficiently. Dropbox’s continuous development of AI-driven collaborative features strengthens user engagement and platform adoption.

Key AI Productivity Tools Companies:

The following key companies have been profiled for this study on the AI productivity tools market.

-

Automation Anywhere, Inc.

-

Blue Prism Limited

-

Cisco Systems, Inc.

-

Dropbox Inc.

-

Grammarly Inc.

-

Google LLC

-

IBM Corporation

-

Microsoft

-

UiPath

-

Workato

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Microsoft; Cisco Systems; Google LLC; Dropbox Inc.

- Expanding integrated AI ecosystems across enterprise productivity and collaboration platforms.

- Using partnerships, acquisitions, and AI enhancements to increase adoption.

- Strong global presence and enterprise customer base strengthen market positioning.

- Heavy AI investments support innovation, automation, scalability, and product differentiation.

- Legacy systems and large structures slow innovation and operational flexibility.

- High implementation costs limit adoption among small and mid-sized businesses.

Emerging Players: Grammarly Inc.; Workato

- Focusing on niche AI productivity and workflow automation solutions.

- Using agile development and subscription models for rapid expansion.

- Faster innovation cycles and specialized AI capabilities improve market competitiveness.

- User-friendly platforms deliver personalized and efficient productivity optimization solutions.

- Limited global presence and financial resources restrict large-scale expansion.

- Rising competition from integrated AI platforms affects long-term differentiation.

Recent Developments

-

In May 2026, Automation Anywhere introduced new enhancements to its Agentic Process Automation (APA) platform to support AI-driven enterprise processes across business operations. The company also launched AAI Code, a low-code development tool designed to accelerate enterprise application and workflow creation using natural language inputs and existing process documents.

-

In November 2025, Cisco Systems launched Cisco IQ, a unified AI-powered digital interface designed to connect the entire customer journey across enterprise support and professional services. The platform integrates real-time insights, troubleshooting, automation, personalized learning, and AI-driven recommendations within a single interface to simplify IT operations and improve operational efficiency.

-

In October 2025, IBM introduced new software products and intelligent infrastructure capabilities to help enterprises operationalize AI across development, operations, and business workflows. The company expanded its AI and hybrid cloud portfolio with advanced agentic orchestration, infrastructure automation, and AI-powered productivity solutions designed for enterprise environments.

-

In May 2025, Grammarly launched AI agents designed to support workplace productivity through automated communication, content development, and task execution capabilities. The launch expands Grammarly’s transition from an AI writing assistant provider to a broader AI productivity platform focused on enterprise workflow efficiency.

AI Productivity Tools Market Report Scope

Report Attribute

Details

Market size in 2025

USD 11.2 billion

Estimated market size in 2026

USD 14.1 billion

Projected market size by 2033

USD 36.4 billion

Growth rate

CAGR of 14.5% from 2026 to 2033

Base year for estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Offering, deployment, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Automation Anywhere, Inc.; Blue Prism Limited; Cisco Systems, Inc.; Dropbox Inc.; Grammarly Inc.; Google LLC; IBM Corporation; Microsoft; UiPath; Workato

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AI Productivity Tools Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global AI productivity tools market report based on offering, end use, deployment, and region.

-

Offering Outlook (Revenue, USD Billion, 2021 - 2033)

-

Virtual Assistants

-

Document Management

-

RPA

-

Data Analytics

-

Others

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-Premises

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare

-

Retail and e-commerce

-

IT and telecom

-

Media and Entertainment

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Objective

Custom Research Modules Delivered

Strategic Value / Business Impact

Market Entry & Expansion Assessment

- Regional demand sizing and forecasting

- Customer segmentation and buying behavior analysis

- Competitive landscape benchmarking

- Regulatory and distribution channel assessment

- Identified high-growth market opportunities Supported go-to-market strategy development

- Highlighted investment priorities and risks

- Enabled data-driven expansion planning

Product Positioning & Competitive Intelligence

- Product benchmarking and feature comparison

- Pricing and value proposition analysis

- Brand perception and customer preference study

- Competitor strategy evaluation

- Improved product differentiation strategy

- Supported pricing optimization

- Identified unmet customer needs

- Enhanced competitive positioning

Technology & Innovation Assessment

- Emerging technology trend analysis

- Innovation pipeline

- Technology adoption readiness assessment

- Ecosystem and partnership mapping

- Identified future growth areas

- Supported innovation roadmap planning

- Evaluated commercialization potential

- Strengthened strategic partnership decisions

Frequently Asked Questions About This Report

The global AI productivity tools market size was valued at USD 11.2 billion in 2025 and is estimated at USD 14.1 billion for 2026.

The global AI productivity tools market is expected to grow at a CAGR of 14.5% from 2026 to 2033, reaching USD 36.4 billion by 2033.

North America dominated with a 30.3% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Some key players operating in the AI productivity tools market include Automation Anywhere, Inc.; Blue Prism Limited; Cisco Systems, Inc.; Dropbox Inc.; Grammarly Inc.; Google LLC; IBM Corporation; Microsoft; UiPath; Workato

Key factors that are driving the market growth include increasing adoption of generative AI, smarter workflow orchestration, and integration of AI assistants into business platforms.

The virtual assistants segment led with a 25.6% revenue share in 2025.

The on-premises segment led with a 60.4% revenue share in 2025.

The IT and telecom segment held the largest revenue share in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.