- Home

- »

- Next Generation Technologies

- »

-

AMOLED Display Market Size & Share Report, 2026-2033GVR Report cover

![AMOLED Display Market (2026 - 2033)Report]()

AMOLED Display Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Polymer, Glass), By Panel Type (Flexible, Transparent, Foldable), By Application (Smartphones & Tablets, Wearable Devices, Laptops), By End Use, By Region, And Segment Forecasts

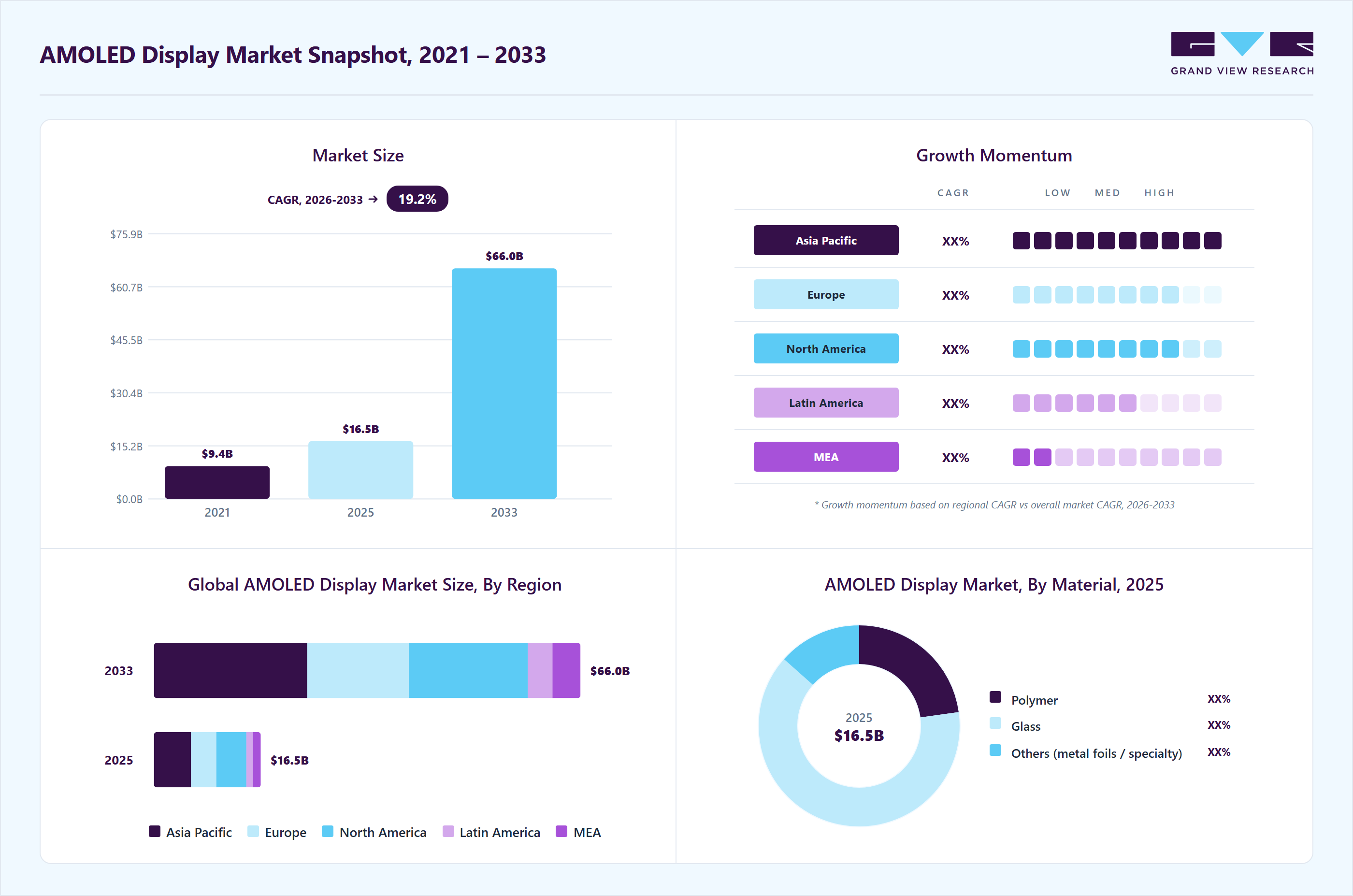

Market Size, 2025

$16.5BMarket Estimate, 2026

$19.3BMarket Forecast, 2033

$66.0BCAGR, 2026–2033

19.2%AMOLED Display Market Summary

The global AMOLED display market size was valued at USD 16.5 billion in 2025 and is projected to grow from USD 19.3 billion in 2026 to USD 66.0 billion by 2033, at a CAGR of 19.2% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 34.7% in 2025. The market is driven by the accelerating adoption of flexible and foldable AMOLED panels in premium smartphones, increasing integration of AMOLED displays across automotive infotainment and digital cockpit systems, rising demand for energy-efficient high-contrast displays in wearable devices, growing penetration of AMOLED technology in laptops and tablets to enhance premium user experience, and expanding deployment of AMOLED displays in medical and industrial visualization applications.

Key Market Trends & Insights

- By material: The glass segment led the market with the largest revenue share of 63.7% in 2025.

- By panel type: The rigid segment led the market with the largest revenue share of 46.5% in 2025.

- By end use: The automotive segment is expected to grow at the fastest CAGR of over 22.8% from 2026 to 2033.

Regional Highlights

- Largest regional market: Asia Pacific (34.7% revenue share, 2025)

- The AMOLED display industry in the China held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 16.5 Billion

- Estimated market size in 2026: USD 19.3 Billion

- Projected market size by 2033: USD 66.0 Billion

- CAGR (2026-2033): 19.2%

Increasing integration of AMOLED panels in automotive infotainment systems and digital cockpits is further supporting market expansion, particularly with the rise of electric and connected vehicles. Rising demand for energy-efficient, high-contrast displays in wearable devices continues to boost adoption, supported by growing consumer preference for smartwatches and fitness trackers. The growing penetration of AMOLED technology in laptops and tablets is enhancing visual performance in premium consumer electronics and professional devices. Expanding use of AMOLED displays in medical, industrial, and specialized visualization applications is also contributing to sustained market growth over the forecast period.")

The rising demand for premium smartphones, foldable devices, and high-resolution consumer electronics is driving strong growth in the AMOLED display industry. Increasing adoption of AMOLED panels across automotive displays, wearables, and next-generation TVs is further accelerating market expansion. Continuous technological advancements, including flexible, transparent, and energy-efficient display architectures, are enhancing product differentiation and supporting wider OEM integration. In addition, growing investments by major panel manufacturers to expand production capacity are strengthening supply chains and helping reduce unit costs. As a result, the market is positioned for sustained growth, supported by rapid innovation, expanding application areas, and strong consumer preference for superior visual performance.

The growing demand for premium smartphones, foldable devices, and high-resolution consumer electronics is driving strong expansion in the AMOLED display industry. Increasing integration of AMOLED panels in automotive displays, wearables, and next-generation televisions is further accelerating adoption across multiple end-use industries. Ongoing technological advancements, including flexible, transparent, and energy-efficient display architectures, are enhancing product differentiation and encouraging wider OEM deployment. In addition, rising investments by leading panel manufacturers to expand production capacity are strengthening supply chains and improving cost efficiencies. Consequently, the market is set for sustained growth, supported by continuous innovation, broader application scope, and increasing consumer preference for superior visual performance.

Material Insights

The glass segment led the market with the largest revenue share of 63.7% in 2025, driven by its widespread adoption in rigid AMOLED displays across smartphones, televisions, and other mainstream consumer electronics. Glass substrates continue to be preferred due to their superior dimensional stability, high optical clarity, and compatibility with high-volume manufacturing processes. Established production infrastructure and mature supply chains further support the large-scale deployment of glass-based AMOLED panels. In addition, glass substrates offer cost advantages over flexible alternatives for rigid display applications. As a result, strong demand from high-volume consumer electronics continues to reinforce the dominance of the glass segment.

The polymer segment is predicted to experience at the fastest CAGR over the forecast period, owing to its increasing adoption in flexible and foldable AMOLED displays across premium smartphones and next-generation consumer electronics. Polymer substrates enable lightweight, thin, and bendable display designs, supporting innovative form factors such as curved, rollable, and foldable devices. Rising OEM focus on product differentiation and advanced industrial design is further accelerating demand for polymer-based AMOLED panels. In addition, ongoing improvements in polymer material durability and barrier performance are enhancing display reliability and lifespan. As flexible display adoption expands across smartphones, wearables, and emerging applications, polymer substrates are expected to be a key growth driver for the market.

Panel Type Insights

The rigid segment accounted for the largest market revenue share in 2025, primarily driven by its extensive adoption in high-volume consumer electronics, including smartphones, televisions, and monitors. Rigid AMOLED displays leverage well-established glass-substrate manufacturing technologies, ensuring high production efficiency and consistent display quality. Their comparatively lower production costs make them attractive for large-scale deployment in mainstream and mid-range devices. Strong compatibility with existing supply chains further supports widespread OEM adoption. Consequently, sustained demand from mature consumer electronics applications continues to drive the dominance of the rigid segment.

The foldable segment is predicted to experience at the fastest CAGR over the forecast period, owing to its ability to deliver innovative form factors that combine larger screen real estate with compact device designs. Increasing consumer demand for premium, multifunctional smartphones is encouraging OEMs to expand foldable product portfolios. Foldable AMOLED displays enable enhanced user experiences through multitasking, immersive content consumption, and improved portability. Ongoing advancements in hinge mechanisms, ultra-thin glass, and the durability of flexible substrates are further improving product reliability. As device prices gradually decline and adoption broadens beyond early adopters, foldable displays are expected to emerge as a key growth driver within the market.

Application Insights

The smartphones & tablets segment led the market with the largest revenue share of 53.3% in 2025, driven by the increasing demand for high-resolution, energy-efficient displays in mainstream and premium mobile devices. Rapid replacement cycles and frequent model upgrades are encouraging OEMs to integrate AMOLED panels across a wider range of price points. AMOLED technology offers superior contrast, vibrant color reproduction, and improved battery efficiency, aligning with evolving consumer preferences. The growing adoption of features such as always-on displays and in-display fingerprint sensors is further driving AMOLED penetration in smartphones and tablets. As mobile devices remain the primary platform for digital content consumption, sustained demand from this segment continues to drive market growth.

The wearable devices segment is projected to grow at the fastest CAGR over the forecast period, owing to rising consumer demand for smartwatches and fitness trackers with high-visibility, power-efficient displays. AMOLED technology supports always-on display functionality while minimizing battery consumption, making it well-suited for compact wearable devices. Increasing health and fitness awareness is further driving the adoption of wearable electronics across both consumer and healthcare applications. OEMs are also integrating curved, flexible AMOLED panels to enable ergonomic, lightweight wearable designs. As wearable device penetration continues to expand globally, this segment is expected to remain a key growth driver for the AMOLED display industry.

End Use Insights

The consumer electronics segment led the market with the largest revenue share of 63.9% in 2025, primarily driven by the widespread adoption of AMOLED displays across smartphones, televisions, wearables, laptops, and tablets. Strong consumer demand for superior visual quality, high contrast ratios, and vibrant color reproduction is accelerating the integration of AMOLED displays in everyday devices. Continuous product innovation and frequent upgrade cycles are encouraging manufacturers to adopt AMOLED panels across both premium and mid-range offerings. In addition, increasing consumption of digital content and gaming is reinforcing demand for high-performance displays. As consumer electronics remain the largest application base, sustained device shipments continue to drive segment dominance.

The automotive segment is projected to grow at the fastest CAGR over the forecast period, driven by the rapid adoption of advanced digital displays across vehicle infotainment systems, instrument clusters, and digital cockpits. Automakers are increasingly integrating AMOLED panels to deliver enhanced visual clarity, contrast, and design flexibility. The transition toward electric and connected vehicles is further accelerating demand for larger, curved, and multi-display configurations. AMOLED technology also supports improved readability and power efficiency, which are critical for in-vehicle applications. As vehicles evolve into software-defined platforms, rising display content per vehicle is expected to strongly drive AMOLED adoption in the automotive segment.

Regional Insights

The AMOLED display market in North America is expected to hold a significant share of 28.1% in 2025, primarily driven by the increasing demand for high-performance and energy-efficient display technologies across premium smartphones and wearable devices. The rapid expansion of advanced automotive infotainment systems and digital cockpit displays is further accelerating AMOLED adoption across the region. In addition, strong investments in research and development by leading technology companies are driving continuous innovations in flexible and foldable display solutions. The growing consumer preference for superior visual quality, including enhanced brightness, color accuracy, and thinner display panels, is further propelling regional market growth.

U.S. AMOLED Display Market Trends

The AMOLED display market in the U.S. maintains a strong position, driven by the high penetration of premium smartphones, advanced consumer electronics, and strong demand for next-generation display technologies. The presence of leading technology innovators and display solution developers is driving continuous product advancements and accelerating the commercialization of flexible and foldable AMOLED panels. In addition, the rising adoption of AMOLED displays in automotive digital dashboards, infotainment systems, and augmented and virtual reality devices is further supporting market expansion. Strong consumer purchasing power and rapid adoption of technologically advanced electronic devices continue to drive sustained growth in the U.S. AMOLED display industry.

Asia Pacific AMOLED Display Market Trends

Asia Pacific dominated the global AMOLED display market with the largest revenue share of 34.7% in 2025 and is expected to grow at the fastest CAGR during the forecast period, primarily driven by the strong presence of major display panel manufacturers and large-scale consumer electronics production capabilities across the region. The rapid growth in smartphone adoption, increasing demand for smart wearable devices, and expanding penetration of OLED televisions are driving significant market expansion. In addition, supportive government initiatives promoting domestic semiconductor and display manufacturing are accelerating production capacity and technological innovation. The rising disposable income and growing consumer preference for premium and high-resolution electronic devices are further driving AMOLED display demand across the region.

The AMOLED display market in China is expected to record at the fastest CAGR over the forecast period, driven by aggressive capacity expansions and strong government support for domestic display manufacturing. Leading Chinese panel makers are investing heavily in next-generation flexible and foldable AMOLED production lines to strengthen their global competitiveness. Rising demand from domestic smartphone brands, wearables, and automotive display applications is further accelerating adoption across multiple end-use sectors. As a result, China is rapidly emerging as a major production hub, challenging the dominance of established South Korean manufacturers and reshaping global supply dynamics.

Europe AMOLED Display Market Trends

The AMOLED display market in Europe is expanding steadily, supported by the rising demand for high-quality and energy-efficient display technologies across consumer electronics and automotive applications. Increasing integration of advanced digital instrument clusters and infotainment systems in luxury and electric vehicles is driving AMOLED adoption across the region. In addition, strong regulatory focus on energy efficiency and sustainable electronic components is encouraging manufacturers to adopt AMOLED display solutions. Growing consumer demand for premium smartphones, smart wearables, and high-resolution entertainment devices is further driving regional market growth.

Key AMOLED Display Company Insights

Some key companies in the AMOLED display industry are Samsung Display, LG Display, BOE Technology Group, China Star Optoelectronics Technology, Tianma Microelectronics, and Visionox Information Technology

-

Samsung Display is the global leader in the AMOLED display industry, driven by its dominant position in smartphone and foldable OLED panels. The company benefits from strong partnerships with major smartphone OEMs and continuous investments in next-generation flexible and QD-OLED technologies. Its advanced manufacturing capabilities and large-scale production capacity enable it to maintain cost competitiveness and technological leadership. Samsung Display specializes in high-performance AMOLED panels for premium smartphones, foldable devices, and next-generation televisions.

-

LG Display is a key player in the AMOLED industry, particularly recognized for its leadership in large-size OLED panels for televisions and automotive displays. The company has focused on expanding its OLED portfolio across TVs, automotive, and IT applications to strengthen its market position. Continuous investments in advanced OLED production lines and innovative panel technologies support its long-term growth strategy. LG Display specializes in large-area OLED panels, especially for premium TVs, automotive infotainment systems, and high-end consumer electronics.

Key AMOLED Display Companies:

The following key companies have been profiled for this study on the AMOLED display market.

- Samsung Display

- LG Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- China Star Optoelectronics Technology (CSOT)

- Tianma Microelectronics

- AU Optronics (AUO)

- Visionox Information Technology

- Japan Display Inc. (JDI)

- Universal Display Corporation (UDC)

- EverDisplay Optronics (EDO)

- Innolux Corporation

- Sharp Corporation

Recent Developments

-

In August 2025, Lava International launched the Blaze AMOLED 2 smartphone featuring a 6.67-inch Full HD+ AMOLED display with a 120Hz refresh rate, targeting the mid-range smartphone segment. The device is powered by the MediaTek Dimensity 7060 processor, delivering enhanced performance and efficient multitasking capabilities. The smartphone offers premium display features such as improved colour accuracy, deeper contrast levels, and smoother visual experience. The launch reflects the increasing adoption of AMOLED display technology in competitively priced smartphones, supporting broader market penetration.

-

In May 2025, Tianma introduced new AMOLED display technologies at Display Week 2025, focusing on enhancing display performance and multifunctional integration. The company showcased a 6.51-inch Hybrid Optoelectronic Integration display incorporating fingerprint recognition, ambient light sensing, and OLED emitter monitoring capabilities. Tianma also presented a switchable privacy AMOLED display designed to improve data security through adjustable viewing modes. Additionally, the company introduced a fluorescent AMOLED technology aimed at improving energy efficiency, color quality, and display durability.

AMOLED Display Market Report Scope

Report Attribute

Details

Market size in 2025

USD 16.5 billion

Estimated market size in 2026

USD 19.3 billion

Projected market size by 2033

USD 66.0 billion

Growth rate

CAGR of 19.2% from 2026 to 2033

Base year for estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, panel type, application, end use, region.

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Samsung Display; LG Display Co. Ltd.; BOE Technology Group Co. Ltd.; China Star Optoelectronics Technology (CSOT); Tianma Microelectronics; AU Optronics (AUO); Visionox Information Technology; Japan Display Inc. (JDI); Universal Display Corporation (UDC); EverDisplay Optronics (EDO); Innolux Corporation; Sharp Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AMOLED Display Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global AMOLED display market report based on material, panel type, application, end use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Polymer

-

Glass

-

Others

-

-

Panel Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Rigid

-

Flexible

-

Transparent

-

Foldable

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Smartphones & Tablets

-

Televisions

-

Wearable Devices

-

Laptops

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer Electronics

-

Automotive

-

Healthcare

-

Aerospace

-

Advertising

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The glass segment led with a 63.7% revenue share in 2025, while polymer segment is the fastest-growing material.

The rigid segment led with a 46.5% revenue share in 2025, while foldable is the fastest-growing type.

The consumer electronics segment led with a 63.9% revenue share in 2025, while automotive is the fastest-growing segment.

Smartphones & tablets segment held the largest share (over 53.0%) in 2025, while wearable devices is the fastest-growing application.

The global AMOLED display market size was valued at USD 16.5 billion in 2025 and is estimated at USD 19.3 billion for 2026.

The global AMOLED display market is expected to grow at a CAGR of 19.2% from 2026 to 2033, reaching USD 66.0 billion by 2033.

Asia Pacific dominated the AMOLED display market with a share of over 34% in 2025, primarily driven by the strong presence of major display panel manufacturers and large-scale consumer electronics production capabilities across the region. The rapid growth in smartphone adoption, increasing demand for smart wearable devices, and expanding penetration of OLED televisions are driving significant market expansion.

Key players include Samsung Display; LG Display Co. Ltd.; BOE Technology Group Co. Ltd.; China Star Optoelectronics Technology (CSOT); Tianma Microelectronics; AU Optronics (AUO); Visionox Information Technology; Japan Display Inc. (JDI); Universal Display Corporation (UDC); EverDisplay Optronics (EDO); Innolux Corporation; Sharp Corporation.

Key factors that are driving the market growth include flexible form factors, rising demand for premium smartphones, energy efficiency advantages, expansion into automotive and wearables, and the growth of foldable and rollable displays.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.