- Home

- »

- Next Generation Technologies

- »

-

Anime Market Size, Share & Growth, Industry Report, 2033GVR Report cover

![Anime Market Size, Share & Trends Report]()

Anime Market (2026 - 2033) Size, Share & Trends Analysis Report By Type (T.V., Movie, Video, Internet Distribution, Merchandising, Music, Pachinko, Live Entertainment), By Genre (Action & Adventure, Sci-Fi & Fantasy), By Region, And Segment Forecasts

Market Size, 2025

$37.7BMarket Estimate, 2026

$41.7BMarket Forecast, 2033

$77.2BCAGR, 2026–2033

9.2%Anime Market Summary

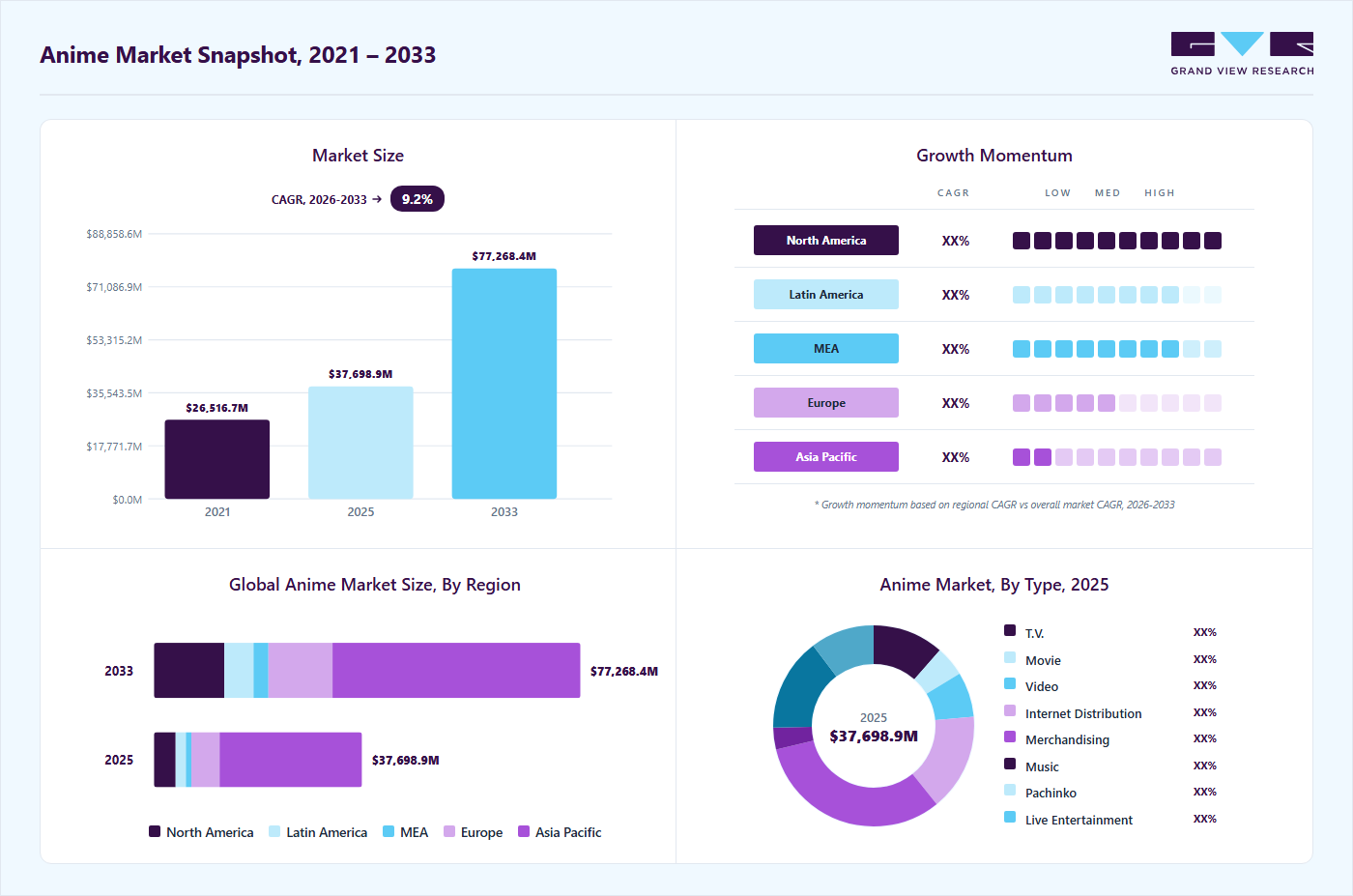

The global anime market size was valued at USD 37.7 billion in 2025 and is projected to grow from USD 41.7 billion in 2026 to USD 77.2 billion by 2033, at a CAGR of 9.2% from 2026 to 2033. Japan dominated the global anime market with the largest revenue share of 43.0% in 2025. This market expansion is driven by the increasing investment in original streaming-exclusive anime content by global OTT platforms, the rapid adoption of advanced animation technologies such as AI-assisted production and real-time rendering to improve production efficiency, and the growing international licensing of anime across emerging markets to support global audience expansion and cross-border content distribution.

Key Market Trends & Insights

- By type: Merchandising segment accounted for the largest revenue share of over 31% in 2025.

- By genre: Sci-fi & fantasy segment is expected to grow at the highest CAGR of 9.9% from 2026 to 2033.

- By application: Military & defense segment led the market with the largest revenue share of 92.3% in 2025.

Regional Highlights

- Largest regional market: Japan (43.0% revenue share, 2025)

- Fastest-growing regional market: North America (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 37.7 Billion

- Estimated market size in 2026: USD 41.7 Billion

- Projected market size by 2033: USD 77.2 Billion

- CAGR (2026-2033): 9.2%

The rapid evolution of AI-driven content generation and cloud-based animation pipelines is significantly transforming anime production workflows by enabling studios to accelerate frame rendering, optimize labor-intensive tasks, and maintain consistent visual quality across large-scale projects. These technologies leverage machine learning-based motion prediction, background generation, and voice synthesis tools to reduce production timelines and operational costs while supporting the creation of high-volume episodic content. The integration of scalable digital production ecosystems enables animation studios to manage distributed creative teams and handle simultaneous global releases, thereby strengthening the anime industry.

Additionally, the market is witnessing strong momentum toward the expansion of immersive and experiential entertainment formats, including anime-themed attractions, live events, and interactive exhibitions designed to deepen fan engagement and extend intellectual property (IP) lifecycles. Entertainment companies are increasingly developing location-based experiences, stage performances, and cinematic events that transform anime franchises into multi-sensory entertainment ecosystems. This shift toward experiential monetization strategies is enabling content owners to diversify revenue streams, enhance brand loyalty, and strengthen franchise longevity in the market.

")

Moreover, the growing integration of advanced data analytics and audience intelligence platforms is driving demand for personalized content development and targeted distribution strategies within the anime industry. Production houses and distributors are increasingly leveraging viewer behavior analytics, recommendation algorithms, and sentiment analysis tools to refine storylines, optimize release schedules, and identify high-potential genres and characters. This data-driven decision-making approach is improving audience retention, maximizing return on content investments, and enabling studios to respond rapidly to shifting consumer preferences across regional markets.

Furthermore, the rising commercialization of anime intellectual property through cross-industry brand collaborations and digital collectibles ecosystems is reshaping monetization opportunities across the anime market. Media companies are increasingly partnering with fashion brands, technology firms, and digital platforms to launch co-branded products, limited-edition collectibles, and blockchain-enabled ownership models that enhance fan participation and brand exclusivity. This transition toward IP-centric business models and the commercialization of digital assets is positioning anime producers and licensors to capitalize on expanding global demand for premium, character-driven entertainment assets.

Market Dynamics

The expansion of streaming platforms is a key driver fueling the growth of the anime market due to several interconnected factors that enhance accessibility, audience reach, and content variety. Streaming platforms such as Netflix, Crunchyroll, Funimation, Hulu, and Amazon Prime Video have made anime content easily accessible to a broader audience than ever before. In the past, anime was often available only through niche outlets or physical media, limiting its reach. With the rise of streaming platforms, anime fans can now access hundreds of titles instantly on any device, allowing them to watch their favorite shows and discover new content conveniently.

Streaming services are continually expanding their anime libraries, offering a vast range of genres and styles to cater to diverse viewer preferences. Whether viewers are interested in action-packed series, emotional dramas, fantasy epics, or lighthearted comedies, the variety of anime available on streaming platforms attracts viewers across demographics, from younger viewers to older adults. This content diversity encourages new viewers to explore anime, while long-time fans are more likely to remain engaged. Moreover, platforms often curate and recommend titles based on user preferences, making it easier for viewers to discover anime that aligns with their interests.

The competition among streaming platforms has led to a surge in exclusive deals and original anime productions, both of which are instrumental in driving market growth. Services such as Netflix and Hulu have invested heavily in producing original anime content or securing exclusive streaming rights to popular series, making their platforms the go-to destination for specific titles. This strategy creates a sense of exclusivity and encourages viewers to subscribe to platforms to access these shows. Original content such as Netflix’s "Castlevania" and exclusives such as "Attack on Titan" on Hulu help attract new subscribers while deepening engagement with the anime genre, boosting the overall growth of the anime market.

Cultural differences and localization challenges act as a restraint for the global anime market, particularly when expanding into new international regions. Many anime series contain themes, humor, social references, and storytelling styles that are deeply rooted in Japanese culture. In some markets, these elements may be difficult for audiences to fully understand or relate to, limiting mainstream acceptance among broader consumer groups.

Localization through subtitles, dubbing, and cultural adaptation requires substantial investment and careful execution to maintain the original narrative quality. Poor translation or low-quality dubbing can negatively affect viewer experience and reduce audience engagement. Additionally, differences in censorship regulations and broadcasting standards across countries may require edits or modifications to content, potentially affecting the authenticity of the original production.

Moreover, certain anime genres or themes may face criticism or restrictions in conservative markets due to violence, mature content, or cultural sensitivities. These regulatory and cultural barriers can slow market penetration and pose challenges for distributors seeking to expand anime consumption globally.

The increasing commercialization of anime intellectual properties presents a major opportunity for market growth. Successful anime titles are no longer limited to television or streaming revenues; they generate substantial income through merchandise, mobile games, collectibles, apparel, and licensing partnerships. Popular franchises often evolve into large multimedia ecosystems that extend audience engagement beyond screen-based entertainment.

Anime-inspired mobile and console games attract large fan bases and create recurring revenue streams through in-game purchases and digital events. Collaborations between anime studios and gaming companies are becoming increasingly common, helping brands expand their reach and maintain long-term consumer interest.

Additionally, rising global demand for anime-themed events, conventions, cafes, and experiential entertainment is creating new monetization channels. Emerging markets in Southeast Asia, India, the Middle East, and Latin America also offer significant growth potential, driven by rising internet penetration, smartphone adoption, and the growing acceptance of Japanese pop culture among younger consumers.

Market Concentration & Characteristics

The anime merchandising market is fragmented, with strong IP-level concentration and a widely dispersed production, licensing, and retail ecosystem across global markets. The market shows medium to high innovation driven by experimentation in collectibles, figures, apparel collaborations, blind-box formats, and digital merchandise tied to streaming and gaming. Additionally, M&A activity is moderate, mainly focused on distribution consolidation and IP acquisition by entertainment groups, strengthening anime portfolios.

Furthermore, regulatory impact is low to medium, owing to IP protection, licensing, and cross-border trade rules, with varying enforcement across regions. Substitution risk is high as consumer spending competes with gaming, streaming, and digital entertainment, limiting exclusivity in merchandise demand. End-user concentration is low to medium, with globally distributed demand but stronger spending in key anime markets like Japan, North America, and parts of Asia. Overall, the market is characterized by high innovation intensity, moderate M&A activity, medium regulatory influence, high substitute pressure, and low-to-moderate end-user concentration, with the industry currently in a globally expanding, franchise-driven growth phase supported by strong pop-culture adoption and digital ecosystem integration.

Type Insights

The merchandising segment accounted for the largest market share of over 31% in 2025, driven by the strong monetization potential of character-based intellectual property and the continuous expansion of branded product portfolios. The growing organization of large-scale fan conventions, pop-up retail experiences, and direct-to-consumer sales channels further reinforces the segment’s leading position, as companies increasingly deploy diversified product strategies to generate recurring revenue streams and strengthen brand visibility across global consumer markets.

The internet distribution segment is expected to witness the fastest CAGR of over 13% from 2026 to 2033. This rapid growth can be attributed to the rapid adoption of digital-first content delivery models and the growing deployment of cloud-based streaming infrastructure designed to support on-demand viewing experiences. Media companies are increasingly leveraging advanced content delivery networks and mobile-optimized platforms to reach geographically dispersed audiences. The rising focus on simultaneous global releases and subscription-based monetization frameworks is expected to support expansion in the internet distribution segment of the anime industry.

Genre Insights

The action & adventure segment accounted for the largest market share in 2025, driven by the strong global demand for high-intensity storytelling formats featuring dynamic combat sequences, hero-driven narratives, and cinematic animation. Production studios are prioritizing investments in large-scale franchise development and high-budget animation projects designed to sustain long-term audience engagement. The growing expansion of theatrical anime releases, premium video-on-demand launches, and global fan events further reinforces the segment’s leading position across the anime market.

The sci-fi & fantasy segment is expected to register the fastest CAGR from 2026 to 2033, fueled by the rising adoption of futuristic world-building concepts, advanced visual effects, and technology-driven narratives. Content creators and animation studios are increasingly developing complex universe-based storylines featuring artificial intelligence, space exploration, and supernatural ecosystems designed to support multi-season production pipelines. The growing focus on high-concept storytelling, virtual production techniques, and transmedia content across games, films, and digital platforms is expected to drive growth in the sci-fi & fantasy segment of the anime industry.

Regional Insights

North America anime market is expected to grow at the highest CAGR of over 15% from 2026 to 2033, driven by the strong presence of global media conglomerates, advanced digital entertainment infrastructure, and the increasing investment in premium animation production. The region is witnessing robust demand for high-quality animated content across theatrical releases, television networks, and digital platforms, supported by rising consumer spending on subscription-based entertainment and franchise-based content ecosystems. The expansion of animation studios, content localization capabilities, and cross-media storytelling initiatives is further strengthening market growth in the region.

U.S. Anime Market Trends

The U.S. anime market is expected to grow at a CAGR of over 15% from 2026 to 2033, fueled by increasing investments in original anime production, licensing partnerships, and content distribution networks. The rising focus on developing exclusive animated series, theatrical anime films, and franchise-based storytelling formats is encouraging the expansion of anime content portfolios. The growing presence of dedicated anime distributors and digital content companies is contributing to market growth in the country.

Europe Anime Market Trends

Europe anime market is expected to grow at a CAGR of over 10% from 2026 to 2033. This growth is driven by the increasing demand for localized and culturally adapted anime content across television broadcasting networks and digital entertainment services. The region is experiencing a surge in demand for multilingual dubbing, subtitling, and regional content licensing solutions that support wider audience accessibility across diverse markets. The integration of advanced digital production technologies and collaborative content development frameworks is supporting improved content delivery efficiency and audience engagement across the anime industry.

The UK anime market is expected to grow significantly in the coming years, driven by the rising expansion of animation education programs, creative media funding initiatives, and government-supported digital content production ecosystems. Increasing collaboration between animation studios, universities, and creative technology providers is fostering innovation in storytelling techniques, visual design, and animation workflows. The growing focus on strengthening the country’s creative industries and digital media exports is boosting demand for anime content development.

The Germany anime market is fueled by the increasing focus on digital media consumption, high-speed broadband penetration, and the expansion of licensed entertainment retail networks within the country. Germany is witnessing a rising demand for officially licensed anime content, physical media collections, and premium collector editions that cater to dedicated fan communities. Strong emphasis on media localization, organized fan conventions, and structured distribution channels is encouraging the development of reliable, scalable, and technologically advanced anime distribution solutions across the country.

Asia Pacific Anime Market Trends

Asia Pacific anime accounted for a significant share of over 25% in 2025, driven by the rapid expansion of digital content production capabilities and the increasing investment in animation studios. The region is experiencing rising demand for original animated content, supported by expanding internet connectivity, smartphone penetration, and youth-driven entertainment consumption patterns. The growing penetration of regional streaming services, digital payment platforms, and content creation ecosystems is enhancing demand for high-volume and cost-efficient anime production and distribution solutions across the market.

The China anime market is experiencing rapid expansion fueled by the increasing localization of animation production, the rapid development of domestic digital entertainment platforms, and strong government support for cultural and creative industries. The country is witnessing strong growth in youth-oriented animated content, online video platforms, and mobile-based entertainment ecosystems that incorporate interactive storytelling formats. The expansion of large-scale animation studios and intellectual property commercialization initiatives is accelerating demand for high-volume and technologically advanced anime production capabilities across the country.

Japan Anime Market Trends

The Japan anime marketdominated the market with a share of over 43% in 2025, owing to the increasing investment in high-quality animation production, intellectual property development, and global content export strategies within the country. Japan is focusing on strengthening its animation workforce, studio infrastructure, and digital production pipelines to maintain leadership in global anime creation. The growing emphasis on international co-production agreements, franchise expansion, and cinematic anime releases is encouraging investments in advanced animation technologies and large-scale storytelling capabilities across the national entertainment industry.

Key Anime Company Insights

Some of the key players operating in the market Crunchyroll (Sony Pictures Entertainment), Bioworld Merchandising, Inc.

-

Crunchyroll (Sony Pictures Entertainment Inc.) is a joint venture that operates independently, formed by U.S.-based Sony Pictures Entertainment, Inc. and Japan’s Aniplex, which is a subsidiary of Sony Music Entertainment (Japan) Inc. The company provides a streaming platform specializing in anime, manga, and Asian media, primarily targeting the U.S. market. The platform offers a vast library of titles, including simulcasts of popular series, allowing fans to watch episodes shortly after their release in Japan.

-

Bioworld Merchandising, Inc. is a company specializing in licensed apparel and accessories, offering a wide range of products tied to popular culture, including anime. The company plays a crucial role by producing and distributing merchandise that enhances fan engagement and reflects the increasing mainstream acceptance of anime, thereby supporting the thriving fan culture and driving demand for anime-related products.

Atomic Flare, and Eleven Arts are some of the emerging participants in the anime market.

-

Atomic Flare is a company dedicated to providing hard-to-find video games, anime, and pop culture merchandise at affordable prices. The company features a diverse range of officially licensed products from popular franchises such as Final Fantasy, Pokemon, and My Hero Academia, among others. The company emphasizes local shipping and personalized customer service, ensuring a memorable shopping experience.

-

Eleven Arts is a dedicated film distribution company specializing in bringing anime and live-action films to North American audiences. Originally focused on theatrical releases, Eleven Arts has expanded its operations to encompass all aspects of film distribution, including translation, localization, home video, and merchandise. By collaborating closely with studios and producers in Japan, Eleven Arts aims to enhance the overall experience for anime fans in North America, striving to deliver compelling stories and high-quality content.

Key Anime Companies:

The following key companies have been profiled for this study on the anime market.

- Pierrot Co., Ltd.

- Production I.G, Inc.

- Studio Ghibli, Inc.

- Bioworld Merchandising, Inc.

- Sunrise, Inc. (Bandai Namco Filmworks)

- Toei Animation Co., Ltd.

- Bones Inc.

- Kyoto Animation Co., Ltd.

- MADHOUSE, Inc.

- Crunchyroll (Sony Pictures Entertainment Inc.)

- Progressive Animation Works Co., Ltd. (PA Works)

- Good Smile Company, Inc.

- Discotek Media

- Sentai Holdings, LLC (AMC Networks)

- VIZ Media, LLC

- Ufotable Co., Ltd.

- Eleven Arts

- Atomic Flare

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Crunchyroll, Bandai Namco Filmworks Inc., Studio Ghibli, Inc.

- Focus on increasing their market by licensing popular anime and officially providing merchandising for it.

- Expand franchise monetization through premium collectibles, collaborations, and limited-edition launches.

- Strong brand recognition and established relationships with major anime IP holders

- Large-scale manufacturing, merchandising expertise, and wider retail penetration.

- High dependence on expensive licensing agreements and franchise renewals

- Greater exposure to inventory risks and slower adaptation to rapidly changing fan trends.

Emerging Players: Stronger Co., Ltd., Atomic Flare, Good Smile Company, Inc.

- Leverage niche fandoms, digital-first sales channels, and social media-driven marketing

- Focus on customizable, small-batch, and trend-based merchandise offerings

- Higher flexibility in responding to evolving consumer preferences and viral trends

- Ability to innovate quickly in product formats and fan engagement models.

- Limited access to major licensed IPs and smaller distribution capabilities

- Lower brand visibility and financial resources compared to established competitors.

Recent Developments

-

In October 2025, Crunchyroll collaborated with Delta Air Lines to integrate its anime catalog into in-flight entertainment systems worldwide. The partnership expanded digital distribution channels and enhanced accessibility of anime content across international travel networks, reinforcing the company’s strategy to broaden audience reach beyond traditional streaming platforms.

-

In October 2025, Toei Animation Co., Ltd. restructured the production schedule of its flagship anime series to adopt a seasonal release model, enabling higher animation quality and improved resource allocation across long-running franchises. The operational shift highlighted strategic production modernization designed to support sustainable content delivery and maintain global audience engagement in the anime industry.

-

In April 2025, Pierrot Co., Ltd. entered a capital and business alliance with Asahi Production to strengthen its anime production pipeline and ensure the stable delivery of high-quality animated series. The collaboration combined Pierrot’s long-running franchise management expertise with advanced digital animation and post-production capabilities, enhancing production scalability and supporting the company’s long-term content expansion strategy in the global anime market.

Anime Market Report Scope

Report Attribute

Details

Market size in 2025

USD 37.7 billion

Estimated market size in 2026

USD 41.7 billion

Projected market size by 2033

USD 77.2 billion

Growth rate

CAGR of 9.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report Product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, genre, region

Region scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa; Japan

Country scope

U.S.; Canada; UK; Germany; France; Italy; Spain; Poland; Hungary; Austria; Russia; Netherlands; Finland; Sweden; Czech Republic; ANZ; China; Philippines; South Korea; Indonesia; Vietnam; Thailand; Malaysia; India; Brazil; Mexico; Saudi Arabia; Turkey

Key companies profiled

Pierrot Co., Ltd.; Production I.G, Inc.; Studio Ghibli, Inc.; Bioworld Merchandising, Inc.; Sunrise, Inc. (Bandai Namco Filmworks); Toei Animation Co., Ltd.; Bones Inc.; Kyoto Animation Co., Ltd.; MADHOUSE, Inc.; Crunchyroll (Sony Pictures Entertainment Inc.); Progressive Animation Works Co., Ltd. (PA Works); Good Smile Company, Inc.; Discotek Media; Sentai Holdings, LLC (AMC Networks); VIZ Media, LLC; Ufotable Co., Ltd.; Eleven Arts; Atomic Flare

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Anime Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest technology trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global anime market report based on type, genre, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

T.V.

-

Movie

-

Video

-

Internet Distribution

-

Merchandising

-

Music

-

Pachinko

-

Live Entertainment

-

-

Genre Outlook (Revenue, USD Million, 2021 - 2033)

-

Action & Adventure

-

Sci-Fi & Fantasy

-

Romance & Drama

-

Sports

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Poland

-

Hungary

-

Austria

-

Russia

-

Netherlands

-

Finland

-

Sweden

-

Czech Republic

-

-

Asia Pacific

-

ANZ

-

China

-

Philippines

-

South Korea

-

Indonesia

-

Vietnam

-

Thailand

-

Malaysia

-

India

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

Saudi Arabia

-

Turkey

-

-

Japan

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Entry & Expansion Assessment

Regional demand sizing & forecasting across key anime markets

Customer segmentation & buying behavior analysis of fan groups

Competitive landscape benchmarking across licensed merch players

Regulatory & distribution channel assessment (IP, retail, online, conventions)

High-growth opportunity identification in premium collectibles and collaborations

Go-to-market strategy support across regions and channels

Investment priorities & risk identification in IP and supply chain

Data-driven expansion planning into emerging anime markets

Product Positioning & Competitive Intelligence

Product benchmarking and feature comparison

Pricing and value proposition analysis

Brand perception and customer preference study

Competitor strategy evaluationImproved product differentiation strategy

Supported pricing optimization

Identified unmet customer needs

Enhanced competitive positioning

Frequently Asked Questions About This Report

The global anime market size was valued at USD 37.7 billion in 2025 and is expected to reach USD 41.7 billion in 2026.

The global anime market is expected to grow at a compound annual growth rate (CAGR) of 9.2% from 2026 to 2033 to reach USD 77.2 billion by 2033.

The rising popularity and sales of Japanese anime content in other parts of the world apart from Japan are expected to drive the growth of the anime market over the forecast period.

Some key players operating in the anime market include Pierrot Co., Ltd.; Production I.G, Inc.; Studio Ghibli, Inc.; Sunrise, Inc. (Bandai Namco Filmworks); Toei Animation Co., Ltd.; Bones Inc.; Kyoto Animation Co., Ltd.; MADHOUSE, Inc.; Crunchyroll (Sony Pictures Entertainment Inc.); Progressive Animation Works Co., Ltd. (PA Works); Good Smile Company, Inc.; Discotek Media; Sentai Holdings, LLC (AMC Networks); VIZ Media, LLC; Ufotable Co., Ltd.; Atomic Flare

The Japan anime dominated the market with a share of over 43% in 2025, owing to the increasing investment in high-quality animation production, intellectual property development, and global content export strategies within the country.

The action & adventure segment largest revenue share in 2025, while sci-fi & fantasy is the fastest-growing segment.

Merchandising held the largest revenue share 31% in 2025, while internet distribution is the fastest-growing area.

North America is the fastest-growing region over the forecast period.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.