- Home

- »

- Next Generation Technologies

- »

-

Automotive Simulation Software Market Report, 2026-2033GVR Report cover

![Automotive Simulation Software Market (2026 - 2033)Report]()

Automotive Simulation Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Solution (Software, Service), By Deployment (On-premise, Cloud-based), By Application, By End Use (OEM, Automotive Component Manufacturers), By Region, And Segment Forecasts

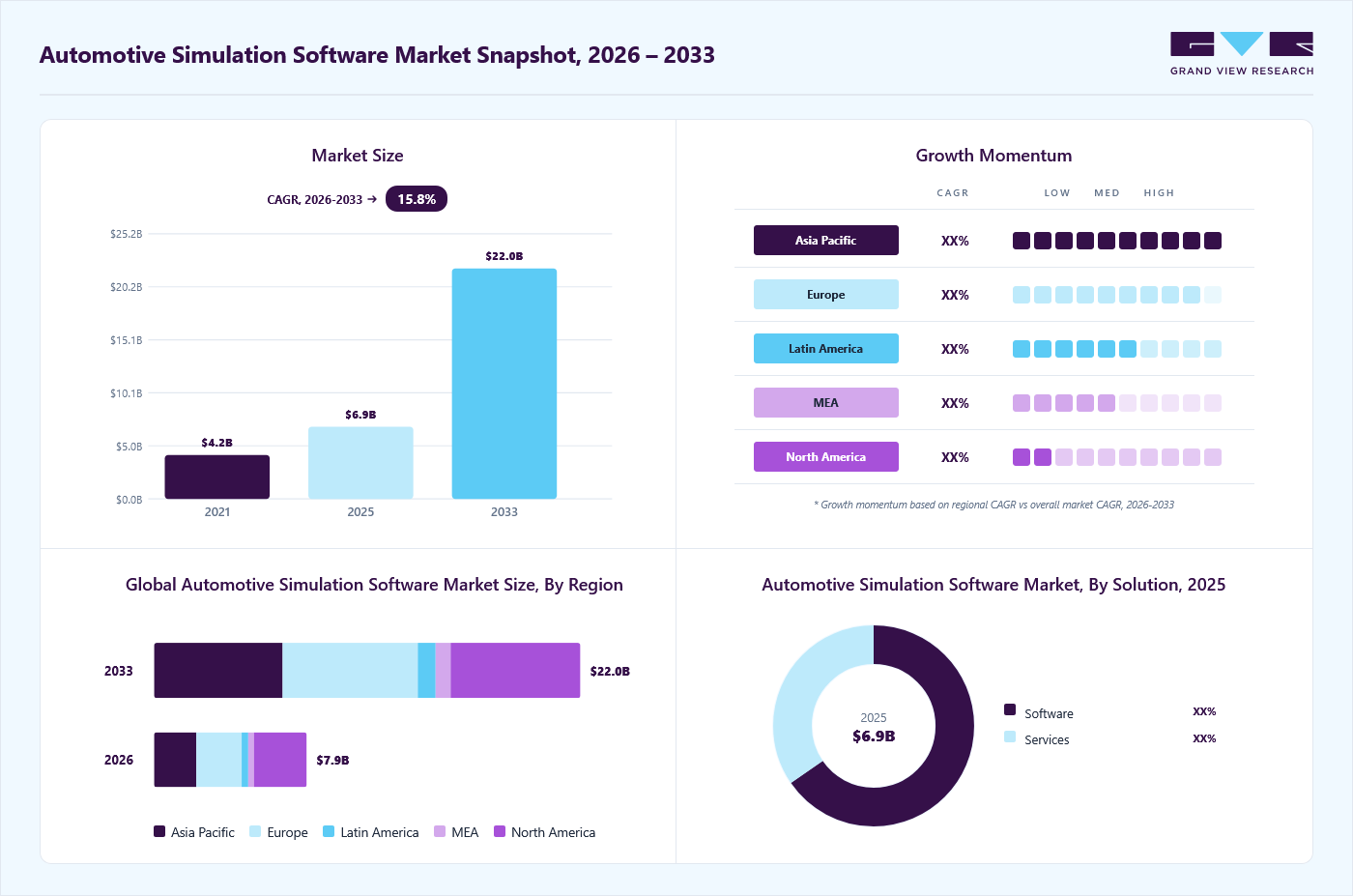

Market Size, 2025

$6.9BMarket Estimate, 2026

$7.9BMarket Forecast, 2033

$22.0BCAGR, 2026–2033

15.8%Automotive Simulation Software Market Summary

The global automotive simulation software market size was valued at USD 6.9 billion in 2025 and is projected to grow from USD 7.9 billion in 2026 to USD 22.0 billion by 2033, at a CAGR of 15.8% from 2026 to 2033. The market in North America dominated with a revenue share of 35.2% in 2025. In the automotive industry, simulation software stands as a significant tool, creating virtual real-time environments to assess the applicability and efficiency of various products and processes.

Key Market Trends & Insights

- By solution: Software segment accounted for the largest share of 65.3% in 2025.

- By application: Designing & development segment held the largest market share in 2025.

- By deployment: On-premise segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 6.9 Billion

- Estimated market size in 2026: USD 7.9 Billion

- Projected market size by 2033: USD 22.0 Billion

- CAGR (2026-2033): 15.8%

The automotive software market is growing due to the increasing adoption of electric vehicles (EVs), driving demand for advanced simulation software, coupled with continuous technological advancements and innovations that enhance product development processes, and the imperative role of simulation software in meeting stringent regulatory standards and conducting comprehensive testing in the automotive industry.The market is witnessing significant growth, driven by the increasing need to reduce production expenditures, optimize training costs, and accelerate vehicle development cycles. These software solutions enable automotive manufacturers to virtually design, test, and refine vehicle components and systems, allowing for early identification of performance issues and design inefficiencies. This capability is particularly critical in the context of reducing CO₂ emissions and improving fuel efficiency, as manufacturers increasingly focus on developing sustainable and environmentally compliant vehicles.

")

Historically, automotive manufacturers relied heavily on physical prototyping and complex mechanical engineering simulations, which involved substantial costs and extended development timelines. Despite multiple prototypes, the likelihood of design failures remained high, often leading to additional research and development (R&D) expenditures and increased pre- and post-production costs. The adoption of automotive simulation software has significantly reduced the dependence on extensive physical testing by enabling accurate virtual validation of multiple design iterations, thereby minimizing failure risks and overall development expenses. This shift is encouraging automotive companies to invest in advanced simulation tools across the product lifecycle.

Automotive manufacturers are also increasingly investing in artificial intelligence (AI)-enabled technologies to address the challenges of operating in a Volatile, Uncertain, Complex, and Ambiguous (VUCA) environment. In this context, virtual testing techniques are gaining traction, as they allow manufacturers to observe and evaluate the real-time behavior of AI-driven systems under diverse driving scenarios. These capabilities enhance product development efficiency while simultaneously reducing time-to-market and associated costs.

The market’s growth is further reinforced by the rapid proliferation of electric vehicles (EVs) and autonomous vehicles, which require extensive validation to ensure safety, reliability, and regulatory compliance. Simulation tools play a critical role in testing vehicle performance under real-world conditions without the constraints of physical testing. For instance, Tesla Motors adopted Dassault Systèmes’ Version 6 (V6) PLM platform as a unified environment for collaborative vehicle design, enabling the company to eliminate data silos, reduce development lead times, and lower costs during the development of the Model S. Such implementations underscore the growing reliance on simulation software as a strategic enabler in modern automotive manufacturing.

Solution Insights

The software segment dominated the market and accounted for the largest revenue share of over 65.3% in 2025. The automotive simulation software is essential for creating virtual environments and conducting complex simulations in the automotive industry. The advancements in software capabilities, such as improved algorithms and realistic modeling, have significantly enhanced the accuracy and efficiency of automotive simulations. The growing complexity of vehicle systems and the integration of emerging technologies like autonomous driving and electric vehicles necessitate sophisticated software solutions. In addition, software updates and customization options provided by vendors contribute to the segment's dominance, allowing manufacturers to adapt to evolving industry needs. Furthermore, the increasing demand for virtual testing and prototyping to reduce development costs and time further amplifies the significance of the software segment in the market.

The service segment is expected to register the highest CAGR of 17.6% over the forecast period. The growth of the segment can be attributed to its integral role in providing customized solutions and support services to address the unique needs of automotive manufacturers. With the increasing complexity of simulation software applications, companies are seeking specialized services for implementation, training, and ongoing maintenance, contributing to the rapid growth of the service segment. In addition, as the automotive industry undergoes constant technological advancements, service providers play a significant role in ensuring seamless integration, upgradation, and troubleshooting, further fueling the demand for service-oriented solutions.

Deployment Insights

The on-premise segment asserted its dominance in the market, claiming the largest market share of over 62.9% in 2025, primarily attributed to its early adoption within the automotive industry. On-premise deployment, a conventional method involving the installation of software directly at the user's location, has succeeded due to its ability to uphold data confidentiality and security. This approach aligns well with companies prioritizing the protection of their sensitive data, offering a robust defense against potential cyber threats. The steadfast growth of the on-premise segment is linked to its provision of a secure and confidential environment, making it the preferred choice for many automotive entities in the landscape of simulation software deployment.

The cloud-based segment is expected to register the highest CAGR of 17.7% over the forecast period. The growth of this segment can be attributed to the increasing adoption of cloud-based solutions, which have gained traction as automotive companies seek enhanced flexibility, scalability, and accessibility in their simulation processes. Cloud deployment enables seamless collaboration and real-time access to simulation data from diverse locations, promoting agility and efficiency in product development. In addition, the cost-effectiveness of cloud-based solutions, as they eliminate the need for extensive on-premise infrastructure, has fueled their popularity, contributing significantly to the segment's growth.

Application Insights

The designing & development segment dominated the target market, accounting for a revenue share of more than 41.7% in 2025. Designing and developing new vehicles involves intricate processes, and simulation software proves valuable in optimizing various aspects of vehicle design before the manufacturing phase. Furthermore, as automotive manufacturers strive for innovation and efficiency, simulation tools are extensively utilized in the initial stages of product development to refine designs and identify potential challenges. Moreover, the segment’s growth is also driven by the need for comprehensive virtual prototyping, enabling manufacturers to enhance vehicle performance, safety, and overall functionality. In addition, the designing & development segment is instrumental in reducing time-to-market by allowing iterative testing and refinement before physical prototypes are produced.

The testing & validation segment is expected to grow at the fastest CAGR of 16.8% over the forecast period. As the automotive industry continues to grow with continuous technological advancements, rigorous testing and validation processes become essential to ensuring the reliability and safety of vehicles. Automotive simulation software plays a significant role in virtual testing scenarios, enabling manufacturers to assess the performance and functionality of vehicles across various conditions and scenarios. Furthermore, the increasing complexity of vehicle systems, especially with the integration of advanced technologies such as autonomous driving and electric propulsion, has elevated the demand for simulation tools in the testing and validation phases. In addition, the need to meet stringent regulatory standards and comply with safety requirements further propels the adoption of simulation software in the testing and validation processes.

End Use Insights

The OEMs segment dominated the market and accounted for the largest revenue share of more than 52.1% in 2025. The high revenue share of the segment is attributable to the increased adoption of simulation software and solutions by OEMs, recognizing the key role of simulation software in optimizing vehicle design and performance. As automotive manufacturers continuously strive for innovation and efficiency, simulation tools have become indispensable in the development of cutting-edge vehicle models. OEMs utilize simulation software extensively for virtual testing, enabling them to identify and rectify potential issues before physical prototyping, thereby reducing development time and costs. Moreover, the increasing complexity of vehicle systems and the integration of emerging technologies like electric vehicles and autonomous driving further drive the demand for simulation software among OEMs. In addition, OEMs' commitment to meeting stringent regulatory standards and enhancing vehicle safety further emphasizes their reliance on simulation tools.

The automotive component manufacturer segment is expected to grow at the fastest CAGR of 16.5% over the forecast period. This growth is attributed to the adoption of simulation software by automotive component manufacturers and the significance of simulation tools in refining the design and functionality of individual automotive parts. As vehicle systems become more intricate, automotive component manufacturers leverage simulation software to ensure the optimal performance and compatibility of their products within the broader automotive ecosystem. Furthermore, the need for precision and efficiency in component manufacturing processes prompts these manufacturers to adopt simulation technologies for virtual testing and validation. In addition, advancements in simulation software cater specifically to the intricate requirements of component design, attracting automotive part manufacturers seeking specialized solutions. Furthermore, the emphasis on cost-effective and streamlined production processes, along with the demand for high-quality components, has fueled the adoption of simulation tools among automotive component manufacturers.

Regional Insights

North America automotive simulation software market asserted its dominance in 2025, capturing the largest revenue share at 35.2%. The growth is driven by major automakers such as General Motors and Ford, which extensively use simulation tools for cost-effective vehicle development and compliance with stringent safety and emission standards. Advanced infrastructure and robust digital ecosystems further support efficient virtual testing and simulation processes. Companies in North America are increasingly focusing on AI-driven vehicle software and simulation platforms to enhance safety, accelerate development, and enable continuous over-the-air updates. For instance, in January 2026, NVIDIA’s DRIVE AV software made its production debut in the Mercedes-Benz CLA, delivering Level 2 driver-assistance capabilities, AI-powered vehicle control, and over-the-air software updates, demonstrating how AI-enabled simulation and software platforms are improving vehicle safety and performance. Collaborations between automakers and software providers, along with high R&D investment, continue to reinforce North America’s leadership in advanced automotive simulation and AI-driven vehicle development.

U.S. Automotive Simulation Software Market Trends

The automotive simulation software market in the U.S. held a substantial market share in 2025, driven by the growing emphasis on electric and autonomous vehicles, which is increasing demand for advanced simulation tools to comprehensively test and validate complex vehicle systems. Stringent safety regulations and evolving software validation requirements are further accelerating the adoption of simulation software across the industry. U.S.-based companies are increasingly focusing on cloud-native simulation, AI-driven validation, and virtual testing environments to support the development of software-defined vehicles while achieving efficiency gains and cost savings through reduced physical prototyping. For instance, in March 2025, Applied Intuition partnered with the TRATON GROUP to deploy AI-powered vehicle software and virtual testing platforms, enabling early software validation and accelerated development of software-defined commercial vehicles through cloud-based simulation workflows. Such trends underscore how simulation software is becoming a core enabler for U.S. manufacturers seeking to maintain technological leadership and shorten time-to-market in an increasingly software-centric automotive landscape.

Asia Pacific Automotive Simulation Software Market Trends

The automotive simulation software market in the Asia Pacific recorded the fastest CAGR of 17.2% over the forecast period. The region is a major hub for the automotive industry, with countries like China, Japan, and South Korea hosting leading automobile manufacturers such as Toyota, Honda, and Hyundai. These companies leverage simulation software extensively to enhance product development efficiency. For instance, in March 2023, Toyota Motor Corporation announced the development of Version 7 of its THUMS (Total Human Model for Safety) crash test simulation software, specifically tailored to account for changes in people's posture during automated driving. The latest version enhances the modeling of the human body, including men, women, and children, providing more accurate representations of key body parts and predicting the effects of reclined positions or emergency maneuvers on bones, organs, and muscles. Furthermore, the increasing demand for electric vehicles (EVs) in the Asia Pacific has led to a surge in the adoption of simulation tools for designing and optimizing electric drivetrains and battery systems.

China automotive simulation software marketheld a substantial market share in 2025. The market is expanding rapidly due to the surging demand for electric vehicles and the accelerated development of autonomous driving technologies, supported by strong government policies promoting vehicle electrification and smart mobility. Chinese automakers are increasingly leveraging simulation platforms to reduce development timelines and comply with stringent safety and emission standards. The widespread presence of domestic EV manufacturers and technology-driven startups is further fueling demand for advanced simulation tools across vehicle design, battery optimization, and ADAS validation. For instance, companies such as NIO utilize simulation solutions like Siemens’ Simcenter to conduct comprehensive virtual testing and verification of electric and autonomous vehicle architectures. Also, China’s leadership in connected vehicle infrastructure and large-scale pilot programs for autonomous driving is reinforcing the adoption of simulation software to validate complex driving scenarios and AI-enabled systems.

The automotive simulation software market in Japan held a substantial market share in 2025. Market growth in Japan is driven by a strong emphasis on innovation, vehicle safety, and engineering precision, supported by the presence of globally established automotive OEMs and Tier I suppliers. Japanese manufacturers increasingly rely on simulation software to enhance product reliability, optimize vehicle dynamics, and meet evolving global safety regulations. The country’s focus on next-generation mobility, including hybrid vehicles, hydrogen-powered vehicles, and advanced driver assistance systems, is further accelerating the adoption of simulation platforms.

India automotive simulation software market held a substantial market share in 2025. Market growth is driven by domestic automakers and component suppliers adopting simulation tools to accelerate product development, improve design accuracy, and reduce physical prototyping costs amid rising production volumes and export-oriented manufacturing. Government initiatives such as FAME and stricter emission norms are further driving the use of simulation software in EV and powertrain development. Companies in India are increasingly focusing on digital twin-based simulations and software-defined vehicle validation to manage complex electronics and software systems. For instance, in October 2025, Tata Technologies partnered with Synopsys to deploy digital twin simulations for testing and validating ADAS, powertrain, infotainment, and other electronic systems, enabling OEMs to detect issues early and accelerate the development of software-driven vehicles.

Europe Automotive Simulation Software Market Trends

The automotive simulation software market in Europe was identified as a lucrative region in 2025. The accelerating transition toward vehicle electrification drives market growth across Europe, the integration of autonomous driving technologies, and the enforcement of stringent safety and emission regulations. Automotive manufacturers across the region are increasingly adopting simulation software to streamline product development, reduce engineering costs, and ensure regulatory compliance throughout the vehicle lifecycle. Europe’s strong focus on sustainability, supported by ambitious carbon neutrality targets and regulatory frameworks such as Euro emission standards, is further strengthening demand for virtual testing and validation tools. Companies across the region are focusing on advanced digital twin and sensor simulation capabilities to improve ADAS and autonomous vehicle validation. For instance, in January 2024, Valeo partnered with Applied Intuition to deliver a digital twin-based ADAS simulation platform, enabling OEMs to conduct advanced sensor perception testing in virtual environments, improve validation accuracy, accelerate software development, and support faster deployment of production-ready autonomous driving features.

The UK automotive simulation software market held a substantial market share in 2025. A strong focus on technological innovation, vehicle safety, and the development of next-generation mobility solutions supports market growth in the UK. Automotive manufacturers and engineering service providers are increasingly relying on simulation tools to enhance vehicle performance, reduce development cycles, and support compliance with evolving safety standards. Companies in the UK are focusing on advanced vehicle dynamics simulation and virtual testing to improve design accuracy and reduce prototyping costs. For instance, in September 2025, Siemens and rFpro launched a tyre-road simulation solution that integrates Simcenter Tire MF-Tyre/MF-Swift models with rFpro’s high-resolution TerrainServer, enabling precise vehicle and tyre dynamics simulations, reducing development time and costs, and supporting both automotive and motorsport virtual testing workflows.

The automotive simulation software market in Germanyheld a substantial market share in 2025. Market expansion in Germany is driven by the country’s leadership in automotive manufacturing and the growing focus on advanced driver assistance systems, autonomous driving, and AI-native simulation technologies. German OEMs and Tier I suppliers are increasingly focusing on virtual engineering, digital twin integration, and AI-driven validation to support software-defined and electric vehicle platforms. Companies are focusing on AI-native simulation and digital twin capabilities to accelerate autonomous driving development and reduce engineering complexity. For instance, in January 2026, Siemens expanded its partnership with NVIDIA at CES to advance AI-native simulation technologies, introducing Digital Twin Composer and Industrial AI Operating System initiatives to enable AI-driven design, testing, and manufacturing workflows. The increasing adoption of advanced simulation tools for traffic modeling, ADAS validation, and mobility simulations continues to strengthen Germany’s position as a key market for automotive simulation software, supported by strong R&D investments and Industry 4.0 initiatives.

France automotive simulation software market held a substantial market share in 2025. The market is expanding due to a growing emphasis on sustainable mobility, innovation-driven vehicle design, and the electrification of passenger and commercial vehicles. French automotive manufacturers are increasingly adopting simulation software to optimize powertrain efficiency, reduce emissions, and accelerate the development of electric and hybrid models. Government support for low-emission vehicles and investments in smart mobility infrastructure are further driving demand for virtual testing and validation tools. For instance, companies such as Renault actively utilize simulation software to optimize vehicle architectures, improve fuel efficiency, and shorten development timelines.

MEA Automotive Simulation Software Market Trends

The automotive simulation software market in the MEAis expected to grow significantly, propelled by the region's increasing focus on technological advancements within the automotive sector. As MEA countries strive for economic diversification and development, automotive companies are adopting simulation tools to accelerate innovation, optimize vehicle designs, and enhance safety features. The rising demand for electric vehicles and autonomous driving technologies further contributes to market expansion in the MEA region.

Saudi Arabia automotive simulation software marketheld a substantial market share in 2025. Market growth in the country is driven by increasing investments in advanced driver assistance systems and autonomous vehicle technologies, supported by national digital transformation initiatives and smart mobility programs under Vision 2030. Automotive stakeholders are increasingly adopting simulation software to reduce development costs, enhance safety validation, and accelerate innovation in next-generation vehicle platforms. The expansion of smart city projects, intelligent transportation systems, and connected mobility infrastructure is further reinforcing the adoption of virtual testing and simulation tools. Local automotive and mobility-focused entities are leveraging platforms such as ANSYS VRXPERIENCE to accelerate the development, validation, and optimization of advanced vehicle features in immersive virtual environments.

Key Automotive Simulation Software Company Insights

Some of the key companies operating in the market include ANSYS, Inc., Dassault Systèmes, among others.

-

ANSYS, Inc. is a company specializing in engineering simulation software development and marketing. Using Workbench as its platform for building simulation technologies, the company offers a comprehensive suite of software solutions. These include applications in 3D design, structural analysis, embedded software, electromagnetic field simulation, computational fluid dynamics, semiconductors, systems modeling, and validation. ANSYS serves a diverse range of industries and verticals, including industrial equipment and rotating machinery, automotive, consumer goods, materials & chemical processing, construction, aerospace & defense, and healthcare.

-

Dassault Systèmes specializes in providing advanced solutions for the market, offering 3D digital mock-up, 3D design, and product lifecycle management software. The company caters its innovative software products to various industries, including automotive, ensuring comprehensive simulation capabilities for design and product development. Leveraging its expertise, Dassault Systèmes supports automotive companies in achieving efficiency and excellence throughout the product lifecycle.

Applied Intuition, Inc. and PTC are some of the emerging market companies in the target market.

-

Applied Intuition is a California-based technology company that specializes in creating software for autonomous vehicles. The company's software allows entities in the autonomous automotive industry to develop, test, and deploy their vehicles at scale. The company's software offers a suite of products that focus on simulation and analytics and deliver sophisticated infrastructure built for scale, enabling automotive industries to test and rapidly accelerate their autonomous vehicle development comprehensively.

-

PTC is a prominent provider of cutting-edge technology solutions for the automotive industry, specializing in automotive simulation software. Their offerings enable manufacturers to simulate and validate various facets of vehicle design, emphasizing safety, durability, and efficiency. PTC's comprehensive portfolio also includes product lifecycle management, computer-aided design, and application lifecycle management solutions, contributing to enhanced efficiency and innovation across the automotive product development lifecycle.

Key Automotive Simulation Software Companies:

he following are the leading companies in the automotive simulation software market. These companies collectively hold the largest market share and dictate industry trends.

- Altair Engineering, Inc.

- Autodesk Inc.

- ANSYS, Inc.

- PTC

- Dassault Systèmes

- The MathWorks, Inc.

- Rockwell Automation

- Simulations Plus

- ESI Group

- GSE Solutions

- Applied Intuition, Inc.

Recent Developments

-

In January 2026, SiMa.ai and Synopsys introduced an integrated blueprint to accelerate automotive AI SoC development, enabling early architecture exploration and virtual software validation for ADAS and IVI applications, reducing development risk, lowering costs, and supporting software-defined vehicle innovation.

-

In March 2025, dSPACE launched its XSG Power Electronics Systems simulation software to support hardware-in-the-loop testing of high-frequency power electronics, enabling safe and accurate validation of SiC- and GaN-based power converters used in electric vehicle and e-mobility applications.

-

In February 2025, ESI Group launched BM-Stamp. This intuitive automotive stamping simulation tool enables fast, predictive feasibility and forming simulations on advanced materials, helping manufacturers reduce physical try-outs, lower production costs, and accelerate development timelines without requiring specialized FEM expertise.

-

In January 2025, Stellantis partnered with dSPACE to accelerate cloud-based vehicle software development by integrating dSPACE’s VEOS simulation platform into its Virtual Engineering Workbench, enabling early software testing, scalable validation, and reduced time-to-market for next-generation connected and autonomous vehicles.

-

In February 2024, Dassault Systèmes announced a strategic partnership with BMW Group to develop BMW's future engineering platform, utilizing Dassault Systèmes' 3DEXPERIENCE platform as its core. This collaboration involves over 17,000 BMW employees globally working on a virtual twin of a vehicle, allowing real-time configuration for different model variants. The partnership represents the next phase in their longstanding collaboration, leveraging digital innovation to streamline engineering processes and enhance the development of personalized and sustainable automotive experiences for BMW customers.

-

In January 2024, ANSYS, Inc. announced that its AVxcelerate Sensors will be integrated into NVIDIA DRIVE Sim, a scenario-based autonomous vehicle (AV) simulator powered by NVIDIA Omniverse. This collaboration aimed to enhance the development and validation of AV perception systems, incorporating Ansys's physics solvers for camera, lidar, radar, and thermal camera sensors. The integration enables users to access high-fidelity sensor simulation outputs for training and validating perception ADAS/AV systems in a controlled virtual environment, addressing the challenges of testing and validating sensor suites and software in real-world driving scenarios.

Automotive Simulation Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 6.9 billion

Estimated market size in 2026

USD 7.9 billion

Projected market size by 2033

USD 22.0 billion

Growth rate

CAGR of 15.8% from 2026 to 2033

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Solution, deployment, application, end use, material, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Altair Engineering, Inc.; Autodesk Inc.; ANSYS, Inc.; PTC; Dassault Systèmes; The MathWorks, Inc.; Rockwell Automation; Simulations Plus; ESI Group; GSE Solutions; Applied Intuition, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Automotive Simulation Software Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global automotive simulation software market report based on solution, deployment, application, end-user, material, and region.

-

Solution Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Computer-Aided Engineering Simulation Software

-

Electromagnetic Simulation Software

-

Training/Human-in-the-Loop (HITL) Simulation Software

-

ADAS Simulation Software

-

Others

-

-

Services

-

Simulation Development Services

-

Training and Support & Maintenance

-

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

On-Premise

-

Cloud-based-based

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Designing & Development

-

Testing & Validation

-

Supply Chain Simulation

-

Others

-

-

End User Outlook (Revenue, USD Million, 2021 - 2030)

-

OEM

-

Automotive component manufacturers

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Key players include Altair Engineering, Inc., Autodesk Inc., ANSYS, Inc., PTC, Dassault Systèmes, The MathWorks, Inc., Rockwell Automation, Simulations Plus, ESI Group, GSE Solutions, and Applied Intuition, Inc.

The automotive software market is growing due to the increasing adoption of electric vehicles (EVs), driving demand for advanced simulation software, coupled with continuous technological advancements and innovations that enhance product development processes, and the imperative role of simulation software in meeting stringent regulatory standards and conducting comprehensive testing in the automotive industry.

The global automotive simulation software market size was valued at USD 6.9 billion in 2025 and is estimated to reach USD 8.0 billion for 2026.

The global automotive simulation software market is expected to grow at a CAGR of 15.8% from 2026 to 2033, reaching USD 22.0 billion.

North America dominated with a 35.2% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The software segment led with a 65.3% revenue share in 2025, while the service segment is the fastest-growing segment.

The on-premise segment led with a 62.9% revenue share in 2025. while the cloud-based segment is the fastest-growing segment.

The designing & development segment led with a 41.7% revenue share in 2025, while the testing & validation segment is the fastest-growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.