- Home

- »

- Next Generation Technologies

- »

-

Aviation Software Market Size & Share Report, 2026-2033GVR Report cover

![Aviation Software Market (2026 - 2033)Report]()

Aviation Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Software Type, By Deployment Type (On-Premises, Cloud), By Application (Airline, Airport), By Region (North America, Europe, Asia Pacific, Middle East & Africa), And Segment Forecasts

Market Size, 2025

$11.8BMarket Estimate, 2026

$12.5BMarket Forecast, 2033

$22.5BCAGR, 2026–2033

8.8%Aviation Software Market Summary

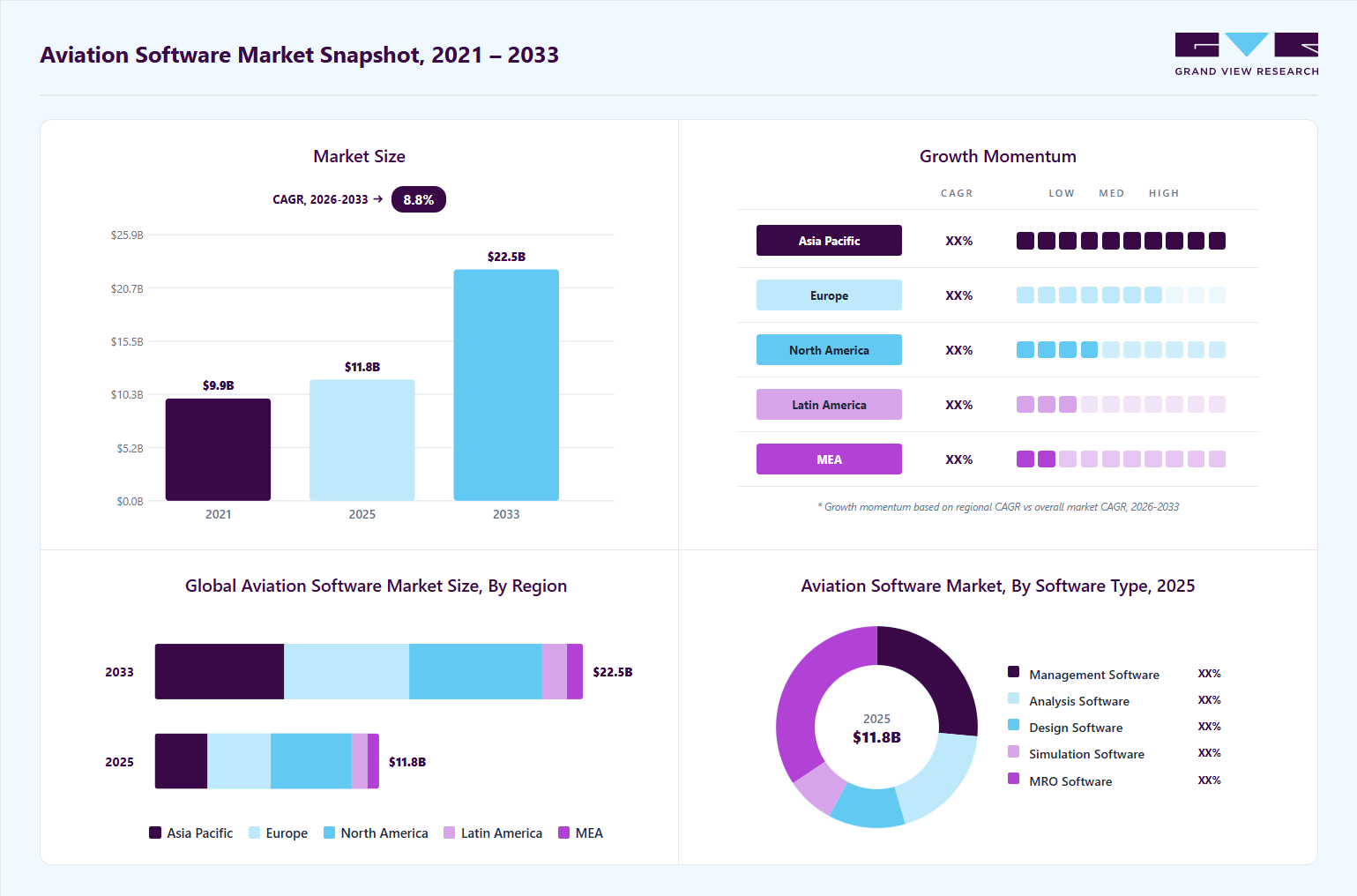

The global aviation software market size was valued at USD 11.8 billion in 2025 and is projected to grow from USD 12.5 billion in 2026 to USD 22.5 billion by 2033, at a CAGR of 8.8% from 2026 to 2033. The market in North America dominated with a revenue share of 36.0% in 2025. The increasing adoption of digital flight operations and airline management platforms drives the market growth.

Key Market Trends & Insights

- By software type: MRO software segment held the largest market share of 34.0% in 2025.

- By deployment type: Cloud segment held the largest market share of 66.0% in 2025.

- By application: Airlines segment held the largest market share of 77.0% in 2025.

Regional Highlights

- Largest regional market: North America (36.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 11.8 Billion

- Estimated market size in 2026: USD 12.5 Billion

- Projected market size by 2033: USD 22.5 Billion

- CAGR (2026-2033): 8.8%

Rising demand for real-time data analytics and operational efficiency optimization is enabling airlines and airports to streamline complex workflows, improve on-time performance, and enhance safety compliance. The increasing adoption of next-generation aviation software technologies, such as cloud-native flight operations platforms, AI-powered predictive maintenance systems, advanced air traffic management solutions, digital twin simulation tools, and real-time data integration frameworks, is expected to enhance operational efficiency, improve safety performance, and enable high-impact decision-making. The growing emphasis on automated flight scheduling, smart airport digitalization, and integrated airline operations management, along with rising demand for regulatory compliance, operational visibility, and cost-effective fleet optimization strategies, is accelerating airline, airport, and maintenance service provider investments in advanced aviation software solutions, thereby contributing to the sustained market expansion.")

The increasing implementation of advanced cybersecurity and aviation safety management solutions, including threat detection platforms, secure data exchange systems, identity and access management tools, and regulatory compliance monitoring software, is anticipated to strengthen data protection, enhance operational resilience, and safeguard critical aviation infrastructure from cyber risks. The growing emphasis on aviation data security, regulatory compliance with international aviation authorities, and protection of passenger and operational information, combined with rising digitalization of airline and airport systems, is driving investments in secure aviation software platforms, thereby contributing to the sustained expansion of the aviation software market.

Additionally, the growing adoption of revenue management, dynamic pricing, and passenger analytics software across airlines and travel operators is expected to improve profitability, optimize seat inventory utilization, and enhance customer engagement. The increasing demand for personalized travel experiences, digital ticketing systems, and integrated customer relationship management platforms, along with growing competition among airlines to maximize ancillary revenue streams and operational efficiency, is accelerating the deployment of advanced commercial aviation software solutions across global airline networks.

Moreover, the rapid modernization of air traffic management infrastructure and the deployment of next-generation air navigation technologies, such as satellite-based navigation systems, automated traffic flow management software, and collaborative decision-making platforms, is anticipated to enhance airspace capacity, improve flight coordination, and reduce congestion in high-traffic aviation corridors. The growing focus on airspace optimization, real-time flight tracking, and cross-border aviation coordination, combined with increasing investments by aviation authorities in digital air traffic control systems, is driving large-scale adoption of advanced aviation software solutions.

Market Dynamics

The ongoing digital transformation of the global aviation industry is driving significant demand for aviation software solutions across airlines, airports, and air traffic management authorities. Airlines are rapidly adopting integrated software platforms to improve operational efficiency, optimize fuel management, automate scheduling, and enhance passenger service experiences. Aviation software solutions are increasingly deployed to streamline flight operations, reduce delays, improve crew coordination, and enhance decision-making capabilities through AI-powered analytics and automation technologies.

The rapid modernization of airport infrastructure and increasing investments in smart airport initiatives are supporting market growth. Airports are deploying advanced aviation software for baggage handling, biometric verification, and air traffic coordination to improve security. Regulatory requirements related to aviation safety, cybersecurity, and operational transparency are encouraging airlines and airport operators to upgrade legacy IT systems with modern digital platforms. The growing integration of IoT-enabled aircraft monitoring systems, digital twins, and predictive maintenance software is helping aviation companies reduce operational costs and minimize aircraft downtime, further strengthening the market expansion.

The aviation software market faces challenges due to the complexity of integrating modern software platforms into existing aviation infrastructure and legacy systems. Many airlines and airport operators continue to rely on outdated operational technologies that are difficult to integrate with advanced cloud-based aviation software solutions. The transition from traditional systems to fully digitalized operational ecosystems often requires substantial investments in infrastructure upgrades, employee training, and system customization. These high implementation costs and operational disruptions can slow software adoption, particularly among small and medium-sized airlines operating under tight budget constraints.

Cybersecurity risks and strict regulatory compliance requirements pose major restraints on the aviation software industry. Aviation systems manage highly sensitive operational, passenger, and navigation data, making them vulnerable to cyberattacks, ransomware incidents, and data breaches. The variations in aviation regulations across different countries create operational challenges for multinational aviation software providers. Concerns related to software reliability, interoperability, and data protection continue to limit the rapid implementation of advanced digital aviation platforms.

The increasing adoption of artificial intelligence, machine learning, and advanced predictive analytics technologies is creating substantial growth opportunities in the aviation software market. Airlines operators are increasingly investing in AI-powered aviation software solutions to improve operational forecasting, automate maintenance planning, and enhance passenger engagement. Predictive analytics platforms enable aviation companies to identify maintenance issues before failures occur, reducing aircraft downtime, minimizing operational disruptions, and improving fleet reliability. The growing use of real-time operational intelligence and automated decision-support systems is expected to generate significant demand for next-generation aviation software platforms.

The expansion of smart airport projects, connected aircraft technologies, and autonomous aviation systems is further opening new opportunities for software vendors and technology providers. Emerging trends such as biometric passenger processing, digital airport ecosystems, unmanned aerial vehicle integration, and cloud-native air traffic management platforms are driving the need for highly scalable, interoperable aviation software solutions. Developing economies are investing heavily in airport modernization programs and expanding aviation infrastructure, creating favorable conditions for software deployment across the commercial and defense aviation sectors. The growing emphasis on sustainability, fuel-efficiency optimization, and carbon-emission reduction initiatives is expected to further accelerate demand for intelligent aviation software solutions.

Market Concentration & Characteristics

The aviation software market is moderately concentrated, with a mix of large global aviation technology providers, enterprise software companies, and specialized aviation IT vendors. The market is experiencing accelerating growth due to rising digital transformation initiatives, increasing passenger traffic, and growing demand for real-time operational efficiency. Strategic collaborations, mergers, and acquisitions are increasingly common as companies aim to expand software portfolios, strengthen cloud capabilities, and enhance AI-driven aviation analytics platforms. Continuous investments in cloud-native aviation systems are becoming a central competitive strategy within the market.

The aviation software industry is characterized by a high degree of innovation, supported by increasing adoption of AI, IoT-enabled aircraft monitoring, and advanced data analytics platforms. The industry experiences moderate levels of mergers and acquisitions as aviation companies pursue technological modernization. Regulatory compliance requirements related to aviation safety, cybersecurity, and data management significantly influence software development. Competition from substitute service models remains moderate, as operators increasingly rely on integrated aviation software ecosystems to optimize scheduling, fleet management, and passenger experience. Growing investments in smart airport infrastructure and autonomous aviation technologies are expected to accelerate the market growth.

Software Type Insights

The MRO software segment accounted for the largest market share of over 34.0% in 2025, driven by the increasing demand for predictive maintenance and fleet lifecycle management across commercial and cargo aviation fleets, rising regulatory requirements for aircraft safety and maintenance documentation, and growing investments in digital transformation of maintenance operations. The growing emphasis on reducing aircraft downtime, optimizing spare parts inventory, and enabling condition-based maintenance is further reinforcing the expansion of the MRO software segment within the aviation software industry.

The simulation software repeaters segment is expected to grow at the fastest CAGR of over 12% from 2026 to 2033. This growth is attributed to the increasing adoption of advanced pilot training and virtual flight simulation technologies. The growing demand for immersive training solutions, real-time flight performance modeling, and air traffic management simulations, along with advancements in augmented reality (AR), virtual reality (VR), and AI-driven simulation engines, is accelerating the growth of the simulation software segment.

Deployment Type Insights

The cloud segment accounted for the largest share of the aviation software industry in 2025, driven by the increasing demand for scalable and centralized aviation data management platforms, rising adoption of Software-as-a-Service (SaaS) solutions, and the growing need for real-time operational visibility. Cloud-based aviation software deployments remain highly preferred across airline operations centers due to their flexibility, cost efficiency, and remote accessibility. The growing adoption of digital transformation initiatives, expansion of data-driven decision-making frameworks, and increasing reliance on integrated analytics continue to support the cloud segment.

The on-premises segment is expected to witness a significant CAGR from 2026 to 2033. This growth is attributed to the rising demand for enhanced data security and system control in safety-critical aviation environments, increasing regulatory requirements for local data storage and compliance management, and growing investments by defense aviation authorities. The growing need for high-performance computing in air traffic control systems, mission-critical flight operations, and secure maintenance data processing is accelerating the growth of the on-premises segment in the aviation software industry.

Application Insights

The airlines segment accounted for the largest share of the aviation software market in 2025, driven by the increasing adoption of integrated flight operations management platforms, rising demand for real-time fleet performance monitoring, and growing investments in digital revenue optimization systems. Aviation software deployments remain highly preferred across airline operations control centers, crew scheduling departments, and customer engagement platforms. The increasing transition toward data-driven airline operations and the need for automated compliance reporting to meet evolving aviation regulations continue to support the dominance of the airline segment in the aviation software industry.

The airport repeaters segment is expected to grow at the fastest CAGR from 2026 to 2033. This growth is attributed to the rapid expansion of smart airport initiatives, increasing investments in advanced passenger processing, and the rising demand for seamless airport operations. Airport authorities are increasingly deploying integrated airport management software to enhance passenger flow, baggage handling efficiency, and airside operations in large international hubs. The growing adoption of biometric identification technologies and AI-enabled passenger experience solutions is accelerating the expansion of the segment in the market.

Regional Insights

The North America aviation software market accounted for the largest share of over 36.0% in 2025, fueled by the region’s strong adoption of advanced airline operations management platforms, significant investments in digital air traffic control modernization programs, and the rapid expansion of predictive maintenance. The growing integration of artificial intelligence-driven analytics, cloud-based aviation platforms, and advanced cybersecurity frameworks is improving operational efficiency and ensuring compliance with safety standards, thereby strengthening the market for aviation software.

U.S. Aviation Software Market Trends

The U.S. aviation software industry accounted for the largest share of over 72.0% in 2025, driven by increasing investments in next-generation air traffic management systems, rising demand for advanced passenger service, and revenue management platforms. The country benefits from a highly developed aviation ecosystem and the continuous modernization of airport infrastructure, which encourages large-scale deployment of aviation software solutions. The increasing implementation of automated crew scheduling systems and integrated airport operations control systems is accelerating operational efficiency, thereby supporting the continued market growth.

Europe Aviation Software Market Trends

The Europe aviation software industry is expected to grow at a CAGR of over 9.0% from 2026 to 2033. In Europe, the market is driven by strong regulatory emphasis on aviation, safety compliance, and environmental sustainability. The region’s focus on carbon reduction targets, efficient airspace management, and cross-border aviation coordination is strengthening long-term software adoption. The growing adoption of collaborative decision-making platforms, the expansion of digital air navigation services, and the increasing deployment of automated airport resource management systems are driving steady market growth across Europe.

The UK aviation software market is expected to grow at a significant rate in the coming years. This expansion is supported by nationwide airport modernization initiatives, strong investments in digital passenger processing and border control systems, and increasing demand for advanced airport security and surveillance software. The growing focus on biometric identification technologies, expansion of smart airport programs, and rising adoption of cloud-based airport management platforms are strengthening the market in the country.

The aviation software market in Germany is rapidly expanding, driven by strong demand for automated maintenance planning and engineering software across major aerospace manufacturing. The growing emphasis on operational efficiency in cargo aviation and logistics operations is accelerating the adoption of digital maintenance management platforms. Germany’s leadership in aerospace engineering innovation is reinforcing its position as a key market growth driver.

Asia Pacific Aviation Software Market Trends

The Asia Pacific aviation software industry is expected to grow at the fastest CAGR of over 12.0% from 2026 to 2033, fueled by the rapid expansion of commercial airline fleets, increasing air passenger traffic, and digital transformation initiatives. The region’s growing middle-class population, rising demand for air travel services, and increasing adoption of automated passenger handling and baggage management systems are enabling faster deployment of advanced aviation software solutions. The growing development of new international airports and strong government support for aviation infrastructure are positioning Asia Pacific as a high-growth region.

The Japan aviation software market is gaining momentum, driven by strong demand for advanced flight safety and disaster management systems and rising adoption of robotics and artificial intelligence in airport logistics services. Japan’s focus on operational precision and resilience in transportation infrastructure supports continuous innovation in aviation software deployment. The increasing implementation of automated ground handling coordination platforms and integrated airport command and control systems is strengthening long-term market expansion in the country.

The aviation software market in China is witnessing robust expansion, fueled by large-scale airport construction projects, strong government-backed aviation modernization programs, and rapid growth in domestic air travel demand. The growing development of smart airport ecosystems, expansion of air cargo logistics networks, and strong investments in artificial intelligence-based aviation analytics platforms are driving widespread adoption of aviation software, thereby supporting strong market growth.

Key Aviation Software Company Insights

Some of the key players operating in the market are Airbus SE and Thales Group.

-

Airbus SE is a global aerospace leader driving innovation in digital aviation platforms, aircraft lifecycle management, and integrated flight operations solutions across commercial and defense aviation markets. The company’s emphasis on advanced data analytics, connected aircraft ecosystems, and predictive maintenance software accelerates the deployment of aviation software in mission-critical applications ranging from fleet performance optimization to air traffic management modernization, reinforcing Airbus’s position as a strategic technology partner in the aviation software industry.

-

Thales Group is a multinational technology provider delivering advanced avionics, air traffic management systems, and cybersecurity-enabled digital aviation solutions across global aviation networks. The company’s focus on AI-powered decision-support platforms, secure communication systems, and integrated airport operations technologies strengthens real-time situational awareness and operational resilience, enabling the adoption of aviation software in safety-critical environments and reinforcing Thales’s leadership in the aviation software market.

Ramco Systems Limited and Veryon are some of the emerging participants in the aviation software market.

-

Ramco Systems Limited is an enterprise software company advancing cloud-native aviation maintenance and engineering management platforms for airlines, maintenance organizations, and defense operators worldwide. The company’s emphasis on mobile-enabled maintenance workflows, artificial intelligence-driven predictive analytics, and integrated enterprise resource planning capabilities supports efficient aircraft lifecycle management and cost optimization, positioning Ramco as a fast-growing innovator in the aviation software industry.

-

Veryon is a specialized aviation technology firm delivering digital maintenance intelligence, aircraft reliability analytics, and regulatory compliance management solutions across commercial and business aviation sectors. The company’s focus on data-driven maintenance insights, real-time operational visibility, and cloud-based software platforms enhances maintenance planning accuracy and fleet availability, strengthening Veryon’s emergence as a dynamic growth player in the aviation software industry.

Key Aviation Software Companies:

The following key companies have been profiled for this study on the aviation software market.

- Airbus SE

- Bigscal Technologies Pvt. Ltd.

- CHAMP Cargosystems

- General Electric Company

- Honeywell International Inc.

- IFS

- Indra Avitech GmbH

- Leonardo S.p.A.

- Ramco Systems Limited

- RTX Corporation

- SITA

- Veryon

- Thales Group

- The Boeing Company

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Airbus SE; General Electric Company; Honeywell International Inc.; Leonardo S.p.A.; RTX Corporation; Thales Group; The Boeing Company

- Mature players focus on developing integrated aviation software ecosystems combining flight operations, predictive maintenance, avionics, and airline resource planning platforms.

- These companies heavily invest in AI-driven analytics, cloud-enabled aviation platforms, cybersecurity solutions, and digital twin technologies to improve operational efficiency.

- Their competitive edge lies in extensive aerospace expertise, strong global airline partnerships, advanced avionics capabilities, and established aviation software deployment across commercial and defense sectors.

- They benefit from strong R&D investments, broad aviation infrastructure portfolios, regulatory compliance expertise, and the ability to deliver highly reliable mission solutions.

- Mature players face challenges including complex integration of legacy aviation systems, slower software modernization cycles, and high operational costs.

- Their large organizational structures sometimes reduce agility in responding quickly to emerging aviation software trends and rapidly evolving digital aviation technologies.

Emerging Players: Bigscal Technologies Pvt. Ltd.; Indra Avitech GmbH; Ramco Systems Limited; Veryon

- Emerging players focus on delivering specialized aviation software solutions targeting maintenance management, operational analytics, and airport digital transformation.

- These companies emphasize agile software development and rapid customization capabilities.

- Their competitive edge lies in faster innovation cycles, flexible deployment models, niche aviation expertise, and the ability to provide cost-effective software services.

- They benefit from cloud-native architectures, strong customer responsiveness, and focused solutions designed for aviation.

- Emerging players face challenges, including limited global presence, smaller customer bases, and lower financial resources.

- They encounter difficulties in achieving large-scale aviation certifications and competing against mature players with integrated aerospace technology.

Recent Developments

-

In March 2026, Ramco Systems Limited secured a contract to deploy its next-generation aviation maintenance software platform at a new defense MRO facility operated by Tata Advanced Systems Limited to support maintenance operations for C-130J Super Hercules aircraft. This development underscores the rising demand for modern digital maintenance management platforms and predictive analytics capabilities, thereby accelerating the adoption of aviation software solutions in the military and commercial aviation sectors.

-

In February 2026, Honeywell International Inc. introduced advanced cloud-connected avionics and predictive maintenance software enhancements designed to support software-defined aircraft operations and improve flight efficiency across commercial aviation fleets. The initiative focuses on integrating real-time aircraft health monitoring, digital flight data analytics, and connected cockpit technologies to enable proactive maintenance and operational optimization, thereby supporting the sustained expansion of the aviation software market.

-

In January 2026, Airbus SE partnered with robotics firm UBTech to integrate advanced humanoid robotics into aviation manufacturing and operational workflows, enabling automation and digital coordination. The collaboration demonstrates the growing convergence of robotics, automation, and aviation software platforms to improve operational efficiency. This development highlights the accelerating adoption of intelligent automation systems that rely heavily on integrated aviation software solutions.

Aviation Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 11.8 billion

Estimated market size in 2026

USD 12.5 billion

Projected market size by 2033

USD 22.5 billion

Growth rate

CAGR of 8.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report Product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Software type, deployment type, application, and region

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Airbus SE; Bigscal Technologies Pvt. Ltd.; CHAMP Cargosystems; General Electric Company; Honeywell International Inc.; IFS; Indra Avitech GmbH; Leonardo S.p.A.; Ramco Systems Limited; RTX Corporation; SITA; Veryon; Thales Group; The Boeing Company

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Aviation Software Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest technology trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the aviation software market report based on software type, deployment type, application, and region:

-

Software Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Management Software

-

Analysis Software

-

Design Software

-

Simulation Software

-

MRO Software

-

-

Deployment Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premises

-

Cloud

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Airport

-

Airlines

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Technology & Innovation Assessment

Emerging technology trend analysis

Innovation pipeline and patent review

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Product Positioning & Competitive Intelligence

Product benchmarking and feature comparison

Pricing and value proposition analysis

Brand perception and customer preference study

Competitor strategy evaluation

Improved product differentiation strategy

Supported pricing optimization

Identified unmet customer needs

Enhanced competitive positioning

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The MRO software segment held the highest market share of 34.0% in 2025. while simulation software repeaters is the fastest-growing segment.

The cloud segment accounted for the largest share of 66.0% in 2025, while on-premises is growing significantly.

The airlines segment led with a 77.0% revenue share in 2025, while airport repeaters is the fastest-growing segment.

The global aviation software market size was estimated at USD 11.8 billion in 2025 and is expected to reach USD 12.5 billion in 2026.

The global aviation software market is expected to grow at a compound annual growth rate of 8.8% from 2026 to 2033 to reach USD 22.5 billion by 2033.

North America dominated with a 36.0% revenue share in 2025.

Some key players operating in the aviation software market include Airbus SE, Bigscal Technologies Pvt. Ltd., CHAMP Cargosystems, General Electric Company, Honeywell International Inc., IFS, Indra Avitech GmbH, Leonardo S.p.A., Ramco Systems Limited, RTX Corporation, SITA, Veryon, Thales Group, The Boeing Company

Key factors include increasing adoption of digital flight operations and airline management platforms. Rising demand for real-time data analytics and operational efficiency optimization is enabling airlines and airports to streamline complex workflows, improve on-time performance, and enhance safety compliance.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.