- Home

- »

- Medical Devices

- »

-

Cataract Surgery Devices Market Size Report, 2026-2033GVR Report cover

![Cataract Surgery Devices Market (2026 - 2033)Report]()

Cataract Surgery Devices Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Phacoemulsification Systems, Intraocular Lenses), By Surgical Technique (Phacoemulsification, FLACS), By Age, By Comorbidity, By End-use (Hospitals), By Region, And Segment Forecasts

Market Size, 2025

$7.5BMarket Estimate, 2026

$8.0BMarket Forecast, 2033

$11.7BCAGR, 2026–2033

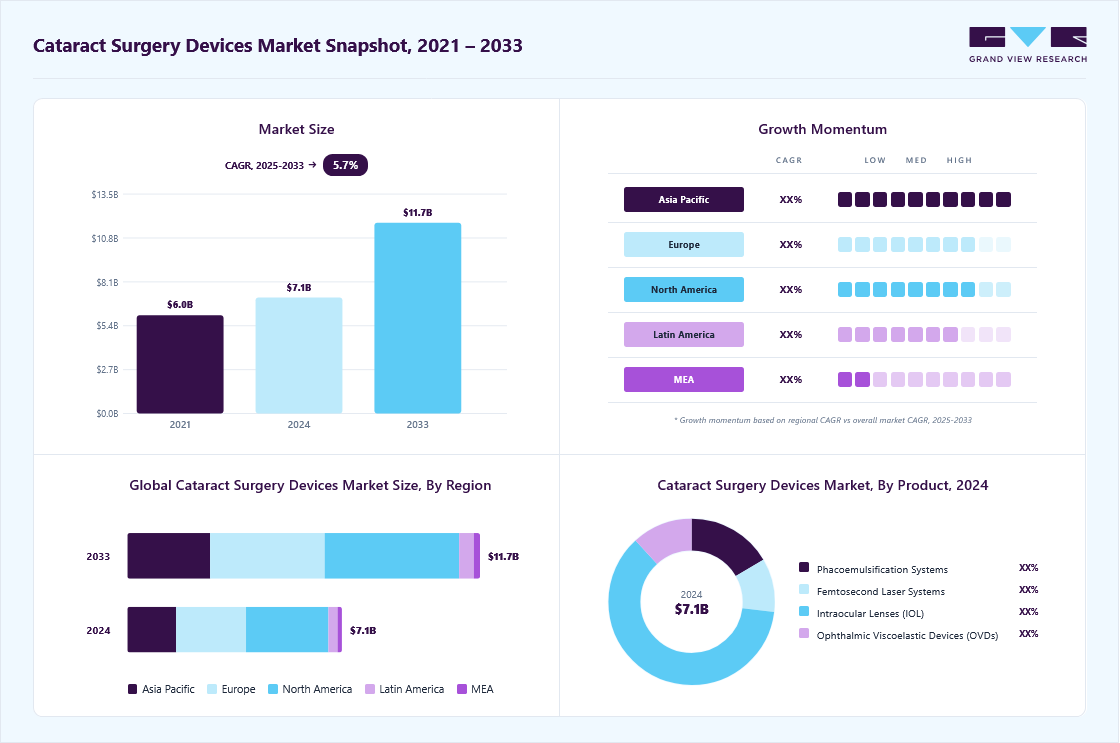

5.7%Cataract Surgery Devices Market Summary

The global cataract surgery devices market size was valued at USD 7.5 billion in 2025 and is projected to grow from USD 8.0 billion in 2026 to USD 11.7 billion by 2033, at a CAGR of 5.7% from 2026 to 2033. North America dominated the global market with the largest revenue share of 38.4% in 2025. This growth is attributed to improved access to healthcare services, technological innovation, and the rising healthcare expenditure.

Key Market Trends & Insights

- By product: Intraocular lenses (IOL) segment led the market with the largest revenue share of 56.4% in 2025.

- By surgical technique: Phacoemulsification segment led the market with the largest revenue share of 66.3% in 2025.

- By age group: 50 years & above segment led the market with the largest revenue share of 90.3% in 2025.

- By comorbidity: Without comorbidities segment led the market with the largest revenue share of 64.6%in 2025.

- By end use: Hospitals segment led the market with the largest revenue share of 68.0% in 2025.

Regional Highlights

- Largest regional market: North America (38.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 7.5 Billion

- Estimated market size in 2026: USD 8.0 Billion

- Projected market size by 2033: USD 11.7 Billion

- CAGR (2026-2033): 5.7%

One of the major factors driving the development of this market is the rising prevalence of cataract, specifically due to the aging population. Cataract is one of the most common causes of blindness globally, rising significantly with advancing age. According to an article from the National Library of Medicine, older adults, especially those above 60 years, are most affected by age-related cataracts, often influenced by diseases like diabetes and hypertension. Furthermore, the aging population has added more than 183 million cases of vision loss, making cataracts a growing public health challenge. This demographic trend will accelerate demand for cataract surgeries and advanced surgical devices.Over a very short period, technological improvements have changed surgical techniques and devices dramatically. The use of femtosecond laser-assisted cataract surgery (FLACS), advanced intraocular lenses (multifocal, toric, and EDOF), optical coherence tomography (OCT) imaging, improved phacoemulsification systems, and real-time intraoperative aberrometry has played a big part in accomplishing surgical accuracy, safety, and patient outcomes to a great extent. These new technologies help prevent unwanted side effects, allow for smaller incisions, and give the surgeon a more precise intraocular lens, leading to faster recovery and better vision correction. As a result, the choice of surgeons and patients is gradually turning towards these advanced procedures; thus, the worldwide use of modern cataract surgery devices is increasing.

")

In recent years, there has been a considerable shift to outpatient and ambulatory surgical centers (ASCs). These centers provide lower procedural costs, quicker patient flow, and improved accessibility, making them highly attractive for cataract surgeries. For example, Unifeye Vision Partners took over Insight Vision Group in 2023, the latter consisting of two multi-specialty ASCs in California, representing the trend of the industry to expand outpatient care facilities. The demand for the development of suitable surgical devices for outpatient settings will increase as more cataract surgeries are performed in ASCs, resulting in further growth of the cataract surgery devices industry.

Cataracts are still the main cause of blindness globally, and they continue to be a major source of vision impairment of moderate-to-severe intensity. So far, 15.2 million cases of global blindness and 78.8 million cases of global moderate-to-severe vision impairment have been reported. The availability of access to cataract surgery is very different, and it is said that the rates of blindness and visual impairment in sub-Saharan Africa and Southeast Asia are eight times higher than those of high-income countries. The least access to healthcare is the most impacted group of people who are the most vulnerable (e.g., aged people, women, residents of rural areas, and members of ethnic minorities). Surgical innovations, intraocular lenses, and diagnostic tools are among the new technologies that have been improving the success and effectiveness of surgeries. Besides that, artificial intelligence has also been gaining ground as a tool for diagnostic accuracy, treatment planning, and surgical approaches. Therefore, patient care in each of these aspects can be improved with the help of AI.

Market Dynamics

Cataract surgery device solutions are gaining significant traction as they enable hospitals, ophthalmic specialty centers, and ambulatory surgical centers (ASCs) to address, treat, and optimize patient vision outcomes through advanced anterior segment surgical platforms. These solutions integrate technologies such as high-frequency phacoemulsification handpieces, ultra-precise femtosecond lasers (FLACS), advanced active fluidics management systems for anterior chamber stability, intraoperative aberration metrics, and digitally-connected surgical planning dashboards to provide real-time control over incision parameters, acoustic energy delivery, intraocular lens (IOL) power calculations, and refractive precision. Cataract surgery platforms help healthcare providers and ophthalmic practitioners address the rising global demand for efficient and high-quality vision restoration by supporting personalized premium lens implementation, targeted astigmatism correction, micro-incision cataract surgery (MICS), and proactive post-operative refractive management.

The global cataract surgery devices market is experiencing robust expansion driven by the ongoing, structural migration of ophthalmic procedures from traditional hospital inpatient settings to outpatient departments and freestanding Ambulatory Surgical Centers (ASCs). Cataract extractions are inherently high-volume, minimally invasive, and rapid-turnaround procedures, making them ideally suited for the streamlined operational model of an ASC. According to the Medicare Payment Advisory Commission (MedPAC) March 2026 report, extracapsular cataract removal with intraocular lens (IOL) insertion remains the single most common procedure performed in ambulatory surgical centers, commanding roughly 18% of the entire fee-for-service Medicare volume within these facilities. This sustained volume is further supported by regulatory tailwinds, such as the Centers for Medicare & Medicaid Services (CMS) granting a 2.9% ASC fee increase, which continues to widen the operational and economic advantages of outpatient settings over inpatient sites.

A major restraining factor for the growth of the cataract surgery devices market is lack of trained ophthalmologist and surgeons. Even though the number of older people with severe cataracts is skyrocketing in places like Sub-Saharan Africa, Latin America, and rural Asia, there are simply not enough doctors who know how to perform these operations. Because specialized procedures require complex technical training, many hospitals outside of major cities cannot use advanced, high-tech tools like phacoemulsification units or premium laser systems. This lack of human talent keeps surgical numbers low, leads to long waitlists, and severely limits how many medical devices can be sold or set up in these high-growth regions.

Market Concentration & Characteristics

The cataract surgery devices market is moderately concentrated, with several established competitors, such as Alcon Inc.; Johnson & Johnson; and Carl Zeiss Meditec AG, being some of the key players. These companies have large market shares partly due to their broad product portfolios and global access. The market is growing steadily due to the global aging population, the rising prevalence of cataract-associated visual difficulties, and continual technological advancements in surgical devices, which aim to improve surgeon precision, reduce recovery time, and improve patient outcomes.

The degree of innovation in the cataract surgery devices industry is high, reflecting a steady transition from conventional techniques toward precision-driven, patient-centric solutions. Intraocular lenses (IOLs) have advanced beyond basic monofocal designs to include multifocal, toric, and extended depth-of-focus variants, addressing both refractive errors and astigmatism to improve postoperative quality of life. Phacoemulsification platforms now integrate real-time imaging, fluidics control, and AI-enabled guidance, enhancing surgical safety and consistency. Femtosecond laser systems, although more expensive, represent another leap by automating critical steps such as corneal incisions and capsulotomy with micron-level accuracy. Even supporting tools like ophthalmic viscoelastic devices (OVDs) are evolving to offer better protection of ocular tissues and facilitate lens implantation. Collectively, these innovations demonstrate a strong push not only toward improved visual outcomes but also toward efficiency, minimally invasive techniques, and broader customization to individual patient needs.

Key players in the cataract surgery industry are partnering with ambulatory surgical centers, hospitals, and technology companies to improve patient care. For instance, in April 2024, Carl Zeiss Meditec AG acquired Dutch Ophthalmic Research Center (D.O.R.C.), enhancing its surgical instruments and workflow solutions while strengthening ties with healthcare providers. Similarly, in January 2023, Bausch + Lomb acquired AcuFocus, adding the IC-8 Apthera intraocular lens to its surgical portfolio and expanding options for partnered clinics. These collaborations improve efficiency, patient outcomes, and access to advanced cataract surgical technologies.

Regulatory oversight significantly influences the cataract surgery devices market, especially for intraocular lenses (IOLs). Agencies like the U.S. FDA and the European CE Mark body ensure products meet strict safety, efficacy, and reliability standards. These regulations also aim to foster innovation by adjusting requirements for new IOL technologies. Although regulatory processes can sometimes cause delays, they are vital for safeguarding patients and maintaining clinical quality. Compliance with these standards helps manufacturers build trust, enhance their market standing, and promote safer, more effective cataract procedures.

In the market for cataract surgery devices, genuine substitutes are scarce because intraocular lenses (IOLs) and supporting surgical technologies are the standard treatment for restoring vision after cataract removal. Nonetheless, there are some alternative options at the edges. Non-surgical solutions, such as stronger eyeglasses, contact lenses, or magnifying devices, can temporarily help manage vision problems but cannot replace cataract removal once the opacity worsens. Meanwhile, research into anti-cataract eye drops and drugs that slow lens opacification is ongoing, but no clinically approved non-surgical alternatives exist yet. Within surgical methods, techniques like manual small-incision cataract surgery (MSICS) can be lower-cost options compared to phacoemulsification systems, especially in resource-limited areas. However, because of the high success and widespread use of IOL implantation, these substitutes are limited, reinforcing surgery as the only definitive treatment for cataracts.

Regional expansion is a major growth driver for the cataract surgery devices market. While North America and Europe dominate with high adoption of advanced technologies, emerging regions such as Asia Pacific, Latin America, and the Middle East & Africa present strong opportunities due to large patient pools, rising healthcare spending, and government programs to improve eye care access. Success in these markets depends on balancing affordability with innovation and aligning with local regulatory and clinical needs, enabling companies to capture growth beyond saturated developed markets.

Analyst Perspective

The cataract surgery devices market is positioned at the intersection of several long-term healthcare and ophthalmic industry trends, including the growing global demand for premium refractive outcomes, an increasing clinical focus on micro-incision and minimally invasive techniques, and continuous advancements in digitally-connected anterior segment surgical platforms. Rising global incidences of age-related cataracts, coupled with a rapidly aging global population, are creating significant opportunities for ophthalmic equipment manufacturers and healthcare facility developers, as surgeons seek highly predictable, efficient solutions to restore visual acuity and correct pre-existing astigmatism or presbyopia in a single procedure. In addition, the expanding adoption of advanced outpatient platforms across multi-specialty hospitals, dedicated eye clinics, and high-volume ambulatory surgical centers (ASCs) coupled with core technological innovations such as high-frequency active-fluidics phacoemulsification systems, ultra-precise femtosecond cataract lasers (FLACS), intraoperative biometry guidance, and next-generation advanced-material intraocular lenses (IOLs) is significantly improving surgical safety, optimizing operating room throughput, and maximizing long-term patient visual outcomes.

Product Insights

Based on product, the intraocular lenses (IOL) segment led the market with the largest revenue share of 56.4% in 2025. The growth is fueled by the rising incidence of cataracts, an increasing demand for premium lenses, and technological advancements that have led to better visual outcomes and patient satisfaction. Intraocular lenses (IOLs) are frequently implanted in different patient cohorts since they address cataract removal and refractive needs. Therefore, they have the highest adoption rate of all intraocular products used in cataract surgery. For instance, in April 2025, Rayner announced the expansion of its IOL manufacturing capacity to meet the growing global demand for IOLs. This expansion highlights the rapid adoption of IOLs as the preferred product category, indicating their significant role in improving cataract surgical outcomes and contributing to the growth of this expanding market.

The adoption of femtosecond laser systems is witnessing significant growth at a CAGR of 7.0%, fueled by the growing interest in precision, safety, and minimally invasive practices. These systems employ ultrafast laser pulses to carry out several necessary maneuvers in cataract surgery, like corneal incisions, capsulotomy, and lens fragmentation, with better precision than traditional manual methods. The shift from conventional phacoemulsification to femtosecond-assisted surgery has resulted in better results, lower surgical complications, and rapid patient recovery. For instance, a study conducted in October 2023 showed enhanced adoption of femtosecond laser ablation in ophthalmic surgery. It reported improved precision and outcomes in surgery, accounting for the increased global uptake of femtosecond laser systems.

Surgical Technique Insights

Based on surgical technique, the phacoemulsification segment led the market with the largest revenue share of 66.3% in 2025, driven by its established position as the standard technique for cataract extraction. This method has several advantages, such as small incisions, quick recovery, and fewer complications. The rise in the incidence of cataract, especially among older people, has increased the need for an efficient and effective surgical remedy. According to an article by ProBiologists, in 2025, phacoemulsification's effectiveness and quick visual recovery have solidified its status as the preferred method for cataract surgery.

The femtosecond laser-assisted cataract surgery (FLACS) segment is witnessing significant growth at a CAGR of 5.83% during the forecast period. This growth is driven by its accuracy, safety, and advantages in providing better visual outcomes than conventional surgical techniques. Compared to manual techniques, FLACS automates some of the more time-consuming, delicate, and potentially difficult steps, such as corneal incisions, capsulotomy, and lens fragmentation. With FLACS, these intricacies are completed efficaciously, while reducing surgical complication rates and improving the reproducibility of the steps. This approach shortens patient recovery times and is satisfactory to patients, with cases in both developed and emerging markets increasing, and inquiring further into the segment in cataract surgery.

Age Group Insights

Based on age group, the 50 years & above segment led the market with the largest revenue share of 90.3% in 2025. Adults in this age group are the primary recipients of cataract surgery, as the prevalence of age-related cataracts rises significantly after 50. Cataract surgery restores vision, improves quality of life, and prevents blindness in older adults. According to a population-based survey across 55 countries, adults aged 50 and older accounted for most cataract surgical procedures. Early access to surgery in this age group helps maintain independence and reduces the risk of falls and other age-related complications.

The 19-50 Years age group is expected to grow significantly, at a CAGR of 5.67% during the forecast period. This rise is driven by younger individuals with early-onset cataracts due to lifestyle factors, such as excessive screen time, unhealthy diet, smoking, and UV light exposure. In addition, the rise in diabetes and hypertension among systemic health problems in younger adults is contributing to early cataracts. Increased awareness of eye health and the availability of affordable eye care are also allowing this age group to access care more timely.

Comorbidity Insights

Based on comorbidity, the without comorbidities segment led the market with the largest revenue share of 64.6%in 2025. The segment is expected to grow at a CAGR of 5.66% over the forecast period. These individuals are generally healthier adults whose cataracts result from normal aging or the impact of lifestyle choices. Growing awareness about eye health, regular eye examinations, and thoughtful access to cost-effective surgical treatment are all drivers of demand for cataract surgery in this population. By considering early intervention in patients with no comorbidities, patients can retain clear vision, improve their quality of life, and minimize the consequences of untreated cataracts in terms of potential surgery and reduced regular activities.

The with comorbidities segment is expected to grow significantly at a CAGR of 5.70% during the forecast period. Individuals with certain health conditions, like diabetes, hypertension, or cardiovascular diseases, are at the greatest risk of developing cataracts, and they often require surgery earlier than healthy adults. Routine medical monitoring, increased awareness of eye health, and proactive management of associated health conditions drive this population's demand for cataract surgery. Addressing cataracts in patients with comorbidities is crucial to prevent vision impairment and maintain overall quality of life.

End-use Insights

Based on end use, the hospitals segment led the market with the largest revenue share of 68.0% in 2025. Hospitals provide comprehensive care and have the infrastructure to handle even a complex procedure. They offer pre-surgery evaluations, advanced surgical equipment, and post-surgery follow-up all in one place. Patients prefer hospitals for safety, convenience, and the ability to manage complications quickly. Additionally, hospitals are expanding their ophthalmology departments and adopting new technologies, which attracts more patients and drives growth in this segment.

The ambulatory surgical centers (ASCs) segment is expected to grow significantly at a CAGR of 6.05% during the forecast period. ASCs are vastly preferred because of their cost-effectiveness, efficiency, and patient convenience. Cataract procedures in ASCs are generally less expensive than hospital outpatient departments, providing savings for patients and healthcare systems. Adopting advanced surgical technologies and streamlined processes in ASCs further drives their growth, making them a key setting for cataract surgeries.

Regional Insights

North America dominated the cataract surgery devices market with the largest revenue share of 38.4% in 2025. The North American cataract surgery devices marketdemonstrates significant growth due to the high incidence of cataract cases, the quickly aging population, and increases in demand for premium surgical devices such as vanced intraocular lenses (IOLs). Technological innovations in surgical devices and the greater adoption of outpatient surgery centers contribute to the growth of this market. For instance, the increasing demand for premium IOLs in the U.S. and Canada indicates a growing trend toward individualized treatment and improved visual outcomes, emphasizing how the evolving patient needs and advanced surgical solutions influence the regional market growth.

U.S. Cataract Surgery Devices Market Trends

The cataract surgery devices market in the U.S. held the largest share in the North America region in 2025. The U.S. cataract surgery devices industry is seeing robust growth driven by the rising prevalence of cataracts and awareness of treatment options. The University Of Florida Department Of Ophthalmology reports that by age 80, over 50% of all Americans will have cataracts and approximately 4 million cataract surgeries are performed annually in the U.S. Because of improved surgical techniques and devices, the outcome of surgery is remarkable, with over 90% of patients achieving 20/20 vision with glasses and surgical infection rates of less than 0.1%. All these facts suggest a large and growing population, a reasonable success with surgery, and increased demand for sophisticated devices for cataract surgery.

Europe Cataract Surgery Devices Market Trends

The Europe cataract surgery devices industry is experiencing substantial growth over the forecast period, due to new technologies and changes in surgical techniques. For example, Immediate Sequential Bilateral Cataract Surgery (ISBCS) involves cataract procedures on both eyes during a single operation. Research shows patients can often return to their daily activities soon after ISBCS, leading to shorter recovery times and reduced costs. At the same time, data-driven tools are helping surgeons perform more accurate procedures. For instance, the ESCRS IOL calculator lets surgeons input patient data once and compare results across multiple modern formulas, making decision-making faster and more efficient.

The UK's cataract surgery devices market is expanding due to hospitals and clinics preferring more advanced intraocular lenses (IOLs) to improve surgical outcomes. For instance, a study conducted by the Royal College of Ophthalmologists in 2023 explains how some hospitals will take on the costs of the more expensive hydrophobic IOLs to enable better long-term results, whilst others will use cheaper hydrophilic IOLs, highlighting the demand for better-quality cataract surgery devices in the UK.

The cataract surgery devices market inGermany is witnessing significant growth, driven by an aging population, rising cataract prevalence, and technological advancements. The country’s leadership is exemplified by ZEISS, showcasing milestones at ESCRS 2025 such as over 10 million surgeries with VisionBlue, the AI-powered CIRRUS PathFinder, and integrated cataract-glaucoma workflows. Platforms like DORC EVA NEXUS highlight Germany’s focus on improving surgical outcomes and strengthening its global Cataract Surgery device presence.

The cataract surgery devices market in France is witnessing significant growth, led by its aging population, increasing cataract prevalence, and continued adoption of newer technologies in surgical techniques. For instance, in December 2022, Elios Vision, Inc. announced that its ELIOS procedure had been registered to treat glaucoma with cataract surgery through an implant-free laser-assisted methodology. The clinical utilization of ELIOS demonstrates the ongoing importance of France in enhancing clinical outcomes and streamlining the integration of novel challenges in remaining innovative in advancing surgical workflows within cataract surgery, thereby enhancing its influence in the regional cataract surgery device sector.

Asia Pacific Cataract Surgery Devices Market Trends

The Asia Pacific cataract surgery devices industry is growing rapidly due to an aging population, rising prevalence of cataracts, and technological advancements in surgery. Asia-Pacific represents a substantial proportion of cataract incidence in countries such as India and China, which have extensive patient demographics and government initiatives to reduce avoidable blindness. Moreover, the growing middle class is adding to the demand for advanced cataract treatment, which includes premium intraocular lenses (IOLs) and contemporary surgical devices. Eye health is a major public health concern, impacting people’s quality of life and daily activities. At the 36th APACRS Annual Meeting and the 24th CSCRS in Chengdu, leading cataract and refractive surgery experts across the Asia-Pacific region shared knowledge and insights. Alcon, a global leader in eye care, showcased its latest ophthalmic surgical products, equipment, and refractive cataract solutions. The company also unveiled upgraded innovations based on its Clareon intraocular lens platform, aiming to make advanced eye care more accessible and support the growing needs of the Chinese market.

The growth of the cataract surgery devices market in Japan is driven by several factors. A rapidly aging population has led to a growing prevalence of cataracts, increasing the need for timely surgical interventions. Advances in surgical technology, including femtosecond laser-assisted cataract surgery, premium intraocular lenses (IOLs), and data-driven surgical planning tools, enable safer, more precise procedures and further encourage adoption. Additionally, rising patient awareness of vision quality and the desire for improved postoperative outcomes push public and private healthcare providers to invest in cutting-edge cataract surgery solutions. For instance, Alcon’s UNITY VCS and CS systems, featuring UNITY 4D Phaco, HYPERVIT 30K, and Intelligent Fluidics, aim to improve efficiency and outcomes in cataract and vitreoretinal surgery, with shipments to Japan expected in May 2025, highlighting the country’s adoption of advanced surgical technologies.

The India cataract surgery devices market is growing steadily due to advancements in technology, increased access to healthcare, and a growing patient population. The rising rate of cataracts, increased awareness, and affordability of surgical treatments are driving demand for higher-quality surgical devices. In August 2025, the Army Hospital Research and Referral (AHRR) in Delhi became the first government facility in India and the second facility in South Asia to conduct robotic custom laser cataract surgery, demonstrating the increased use of innovative technologies in the public health sector.

Latin America Cataract Surgery Devices Market Trends

Latin America is an emerging space in the cataract surgery devices industry, as demand grows due to an aging population, an increase in cataract prevalence, and technological advances in surgery. There is an increasing adoption of advanced ophthalmic surgical procedures in the region, a key driver of demand for cataract surgery devices, particularly ophthalmic viscoelastic devices (OVDs) and intraocular lenses. Emerging markets in countries such as Brazil and Argentina drive the demand for cataract surgical devices, reflecting the continued modernization. The technology-based care trend is changing care for patients diagnosed with cataracts. These trends illustrate Latin America's growing position in the global cataract surgery device market, combining rising patient demand and the adoption of advanced surgical solutions.

Brazil’s cataract surgery devices market is expanding rapidly, propelled by technological innovation, increasing cataract cases, greater healthcare awareness, and better access to advanced procedures. Using premium IOLs and laser-assisted surgical systems improves precision and patient outcomes, while government programs, private sector growth, and startups continue to drive demand. Rayner’s introduction of the RayOne Galaxy and RayOne Galaxy Toric AI-designed spiral IOLs highlights this trend, offering continuous vision with less glare and halo effects, and showcasing Brazil’s adoption of cutting-edge ophthalmic technologies.

Middle East and Africa Cataract Surgery Devices Market Trends

The cataract surgery devices industry in the Middle East and Africa is steadily expanding, fueled by an aging population and the rising occurrence of cataracts. Cataract-related surgical devices constitute a significant part of the broader ophthalmology market, indicating growing demand for advanced solutions. Increased healthcare investments and modern eye care facilities improve access to surgeries, while innovations such as phacoemulsification systems and premium intraocular lenses improve patient outcomes. These factors collectively strengthen the role of cataract surgery devices throughout the region.

The Saudi Arabia cataract surgery devices market is growing steadily, driven by technological advancements, an aging population, and increased awareness of eye health. The rising number of cataract cases has created a strong demand for improved surgical devices that enhance precision, safety, and patient outcomes. Minimally invasive techniques like phacoemulsification and the development of advanced intraocular lenses (IOLs) are resulting in better visual results and shorter recovery times. These trends show the country's wider adoption of modern ophthalmic technologies and greater investment in eye care infrastructure.

The cataract surgery devices market in the UAE is expanding due to technological advances, a higher prevalence of cataracts, and an increasing demand for precision in surgical procedures. Incorporating modern devices such as femtosecond laser-assisted cataract surgery (FLACS), microincision phacoemulsification systems, and premium intraocular lenses (IOLs) is enhancing surgical outcomes and patient recovery. Industry leaders like Dr. Rami Hamed Center (DRHC) in Dubai are leading this trend by introducing advanced technologies that include multifocal, toric, and extended depth-of-focus IOLs, supporting the country’s goal to modernize eye care and boost the market growth.

Key Cataract Surgery Devices Company Insights

The cataract surgery devices market is highly competitive, with key players such as Alcon Inc.; Johnson & Johnson Vision; and Bausch+Lomb holding significant positions. The major companies undertake various organic and inorganic strategies such as product introduction, collaborations, and regional expansion to serve the unmet needs of their customers.

Key Cataract Surgery Devices Companies

The following key companies have been profiled for this study on the cataract surgery devices market.

-

Alcon Inc.

-

Johnson & Johnson Vision

-

Bausch + Lomb

-

Carl Zeiss Meditec AG

-

HOYA Surgical

-

NIDEK Co., Ltd.

-

Rayner

-

STAAR Surgical

-

LENSAR, Inc.

-

Ophtec BV

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Alcon Inc., Johnson & Johnson Vision, Bausch + Lomb)

- Focus on expanding advanced premium intraocular lens (IOL) and femtosecond laser-assisted cataract surgery (FLACS) portfolios for precise refractive outcomes, presbyopia correction, and astigmatism management.

- Emphasize strategic collaborations with multi-specialty hospitals, high-volume Ambulatory Surgical Centers (ASCs), and global ophthalmic teaching institutes to deploy fully integrated digital operating room ecosystems, biometry platforms, and cloud-connected guidance dashboards.

- Dominant brand recognition, vast capital equipment installs bases, highly entrenched global distribution networks, and a comprehensive presence across mature outpatient healthcare markets.

- Advanced R&D capabilities and proprietary biomaterial/optical designs that support superior long-term visual acuity and clinical safety.

- Escalating product development expenses, demanding regulatory clearance cycles (FDA/CE Mark), and massive commercialization/training costs associated with premium surgical systems.

- Intense internal competition within the premium IOL segment alongside a structural reliance on public and private reimbursement stability, which creates localized pricing pressure.

Emerging Players (NIDEC Co., Ltd, Rayner, STAAR Surgical)

- Focus on high-volume, niche, and cost-competitive monofocal intraocular lenses targeting rapidly growing emerging markets and mid-tier public ophthalmic clinics.

- Prioritize innovation and supply-chain efficiency in high-turnaround manual techniques, such as Manual Small-Incision Cataract Surgery (MSICS) or entry-level phacoemulsification consumables, featuring localized distribution and lower-tier cost structures.

- Accelerated mid-tier product innovation cycles and highly flexible, localized commercialization strategies that allow quick adaptation to changing cost constraints and surgeon preferences in developing countries.

- Disruptive pricing models that maximize market penetration and device adoption in price-sensitive geographies and smaller independent outpatient clinics.

- Constrained financial resources, significantly lower international brand awareness, and restricted distribution networks relative to the multi-billion-dollar dominant market leaders.

- Persistent roadblocks related to complex multi-country regulatory approvals, a deficiency of long-term global clinical trial data, and lower surgeon familiarity with new proprietary delivery systems, which slows overall platform adoption.

Recent Developments

-

In September 2025, the TECNIS PureSEE intraocular lens (IOL) was introduced for cataract surgery, offering clear vision across all distances without glasses. A multicenter study showed high patient satisfaction, reduced spectacle dependence, and fewer visual side effects, marking a major advancement in cataract surgery devices.

-

In June 2025, the ASCRS (American Society of Cataract and Refractive Surgery) meeting highlighted major advances in cataract care, including innovations in intraocular lens (IOL) technologies, new pre- and postoperative medical drops, and updates on legislative and regulatory challenges. These developments aim to improve surgical outcomes, patient safety, and access to cataract surgery.

-

In April 2025, Alcon launched the UNITY Vitreoretinal Cataract System (VCS) and the UNITY Cataract System (CS), advanced surgical platforms designed to improve the efficiency and accuracy of cataract surgeries. These systems include 4D Phaco Technology, Intelligent Fluidics, and Thermal Sentry for safer and quicker procedures. The devices have received FDA 510(k) clearance and will be introduced in the U.S., Europe, Japan, and Australia, aiming to enhance surgical outcomes and patient safety.

-

In September 2024, Johnson & Johnson launched the TECNIS Odyssey next-generation intraocular lens (IOL) for cataract surgery, promising continuous, precise vision at all distances under any lighting.

Cataract Surgery Devices Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.5 billion

Estimated market size in 2026

USD 8.0 billion

Projected market size by 2033

USD 11.7 billion

Growth rate

CAGR of 5.7% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, surgical technique, age group, comorbidity, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait;

Key companies profiled

Alcon Inc.; Johnson & Johnson Vision; Bausch + Lomb; Carl Zeiss Meditec; HOYA Surgical Optics; NIDEC Co., Ltd; Rayner; STAAR Surgical; LENSAR, Inc.; Ophtec BV.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cataract Surgery Devices Market Report Segmentation

This report forecasts revenue growth at country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the cataract surgery devices market report on the basis of product, surgical technique, age group, comorbidity, end -se, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Phacoemulsification Systems

-

Femtosecond Laser Systems

-

Intraocular Lenses (IOL)

-

Monofocal Intraocular Lens

-

Multifocal Intraocular Lens

-

Toric Intraocular Lens

-

Accommodative Intraocular Lens

-

-

Ophthalmic Viscoelastic Devices (OVDs)

-

Others

-

-

Surgical Technique Outlook (Revenue, USD Million, 2021 - 2033)

-

Phacoemulsification

-

Manual small-incision cataract surgery (MSICS)

-

Femtosecond laser-assisted cataract surgery (FLACS)

-

Others

-

-

Age Group Outlook (Revenue, USD Million, 2021 - 2033)

-

18 Years & Below

-

19-50 Years

-

50 Years & Above

-

-

Comorbidity Outlook (Revenue, USD Million, 2021 - 2033)

-

With Comorbidities

-

Without Comorbidities

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Ophthalmic Clinics

-

ASCs

-

Others

-

-

Regional Outlook (Revenue, USD million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

Segment Definition

Segment - Product

Revenue capture definition

Phacoemulsification Systems

Revenue is generated through the sale or leasing of phacoemulsification capital hardware platforms used to emulsify and extract the eye's natural lens. Manufacturers derive income from initial equipment capital sales, multi-year post-warranty service and maintenance contracts, physical platform upgrades (such as foot pedals or active fluidics modules), and handpiece replacements.

Femtosecond Laser Systems

Revenue is captured through the commercialization of high-end femtosecond laser hardware platforms used for corneal incisions, capsulotomies, and laser lens fragmentation. Market participants generate revenue from premium initial hardware installations, recurring per-procedure software activation fees (click fees), specialized patient interface consumables, and intensive engineering service contracts.

Intraocular Lenses (IOL)

Revenue flows from the high-volume sale of synthetic lenses implanted into the eye to replace the clouded natural lens during cataract surgery. Equipment and optical manufacturers earn revenue from bulk procurement contracts, recurring single-use lens shipments, and premium tier pricing across advanced technological variants.

Ophthalmic Viscoelastic Devices (OVDs)

Revenue is generated through the continuous sale of clear, gel-like consumable liquids injected during surgery to protect the corneal endothelium and maintain space in the anterior chamber. Income is earned through recurring single-use syringe pack sales, multi-pack institutional volume bundles, and variations between cohesive and dispersive OVD formulations.

Others

Revenue is captured from miscellaneous cataract surgical consumables and accessories, including surgical knives, disposable cassettes, irrigation/aspiration (I/A) tubing sets, drapes, sutures, and single-use micro-forceps. Market participants capture steady, high-margin, high-volume recurring cash flows driven directly by the total number of surgeries performed.

Segment - Surgical Technique

Revenue capture definition

Phacoemulsification

Revenue flows from devices, equipment, and consumables specifically designed for traditional ultrasound-driven cataract extraction. Income is driven by the deployment of phacoemulsification machines, reusable ultrasound handpieces, and specialized single-use phaco tips, sleeves, and fluidics test chambers utilized per procedure.

Manual small-incision cataract surgery (MSICS)

Revenue is derived from low-cost, high-volume surgical toolkits utilized in manual, non-machine-dependent cataract extractions, primarily favored in emerging economies. Income is captured via specialized manual surgical instrument sets, metal or diamond tunnel knives, manual IOL delivery systems, and lower-cost monofocal lens portfolios.

Femtosecond laser assisted cataract surgery (FLACS)

Revenue is generated through the high-value clinical pathway that integrates advanced lasers into the surgical workflow. Market participants earn substantial recurring revenue through a hybrid mix of high-end laser capital sales, mandatory per-procedure single-use patient interfaces, and advanced software license authorizations required to run the automated imaging and cutting sequences.

Others

Revenue is captured from alternative or historical surgical approaches, such as intracapsular (ICCE) or conventional extracapsular cataract extraction (ECCE). Revenue is limited to basic surgical instruments, rigid non-foldable PMMA lenses, and legacy replacement parts for older surgical platforms.

Segment - Age Group

Revenue capture definition

18 Years & Below

Revenue flows from specialized ophthalmic equipment and micro-sized consumables optimized for pediatric cataract surgeries (congenital or traumatic). Income is captured through smaller-diameter phaco tips, lower-volume fluidics software profiles, pediatric-sized speculums, and customized micro-IOL models tailored for developing ocular anatomy.

19-50 Years

Revenue is derived from cataract surgery devices utilized on working-age adults experiencing early-onset, secondary, or traumatic cataracts. Revenue in this segment is heavily skewed toward premium presbyopia-correcting and toric IOLs, advanced pre-operative digital tracking software, and high-precision laser-assisted platforms (FLACS) to meet high lifestyle demands for spectacles-free vision.

50 Years & Above

Revenue is generated through the massive, high-volume procurement of cataract devices for the primary age-related cataract demographic. This segment drives the bulk of steady, recurring market revenue across all product lines, including mainstream phacoemulsification systems, standard monofocal lenses, high-volume OVD packs, and long-term institutional maintenance contracts.

Segment - Comorbidity

Revenue capture definition

With Comorbidities

Revenue flows from advanced cataract technologies used on patients with concurrent ocular conditions like glaucoma, macular degeneration, or diabetic retinopathy. Income is captured through premium specialized devices, such as combination phaco-vitrectomy platforms, intraoperative iris expanders, specialized capsular tension rings (CTRs), and advanced-material lenses designed to minimize posterior capsular opacification (PCO).

Without Comorbidities

Revenue is captured from standard, highly predictable cataract procedures performed on patients with healthy ocular backgrounds outside of cataracts. Revenue is driven by standardized high-throughput workflows, using predictable baseline phaco systems, standard monofocal or premium IOLs, and standard single-use consumable procedure packs.

Segment - End Use

Revenue capture definition

Hospitals

Revenue is generated through the institutional procurement, leasing, or public tendering of cataract surgery infrastructure to major medical networks. This segment drives significant capital inflows from high-end multi-platform acquisitions (e.g., femtosecond laser suites combined with premium microscopes), enterprise software networks, and high-margin multi-year preventive service agreements.

Ophthalmic Clinics

Revenue is derived from specialized, physician-owned eye care practices and outpatient ophthalmology networks. Revenue is driven by the purchase of advanced pre-operative biometry and diagnostic systems, tailored phacoemulsification hardware financing plans, and high-margin premium IOL portfolios (Toric and Multifocal) marketed directly to private-pay patients.

Ambulatory Surgical Centers (ASCs)

Revenue is captured through the rapid procurement of high-efficiency cataract devices by standalone outpatient surgical hubs. Revenue in this segment is driven heavily by high-throughput, reliable phaco systems optimized for fast room turnover, scalable volume discounts on single-use consumable packs, and streamlined fluidic cassette kits designed to maximize daily operational return on investment (ROI).

Others

Revenue flows from secondary end-users, including mobile eye surgical camps, military health facilities, humanitarian healthcare organizations, and academic ophthalmic training institutes. Manufacturers capture revenue via low-footprint, ruggedized portable phaco systems, bulk manual surgery packages (MSICS kits), and basic ad-hoc technical support services.

Estimation Model

Phase

Key Question

Process Steps

Data Sources

Scope Definition

What is being assessed?

1. Define Cataract Surgery Device Categories

2. Scope Clinical Applications

3. Set Geographic Boundaries

4. Align on base year & forecast horizon (2026-2030)

ASCRS, ESCRS, AAO

Build the Product Base

How large is the total addressable market?

1. Profile Surgical Facilities & Tiering

2. Estimate Total Annual Procedure Volumes

3. Apply Device Utilization & Mix Splits

4. Model Capital Equipment Installed Base

National surgical registries, healthcare reimbursement databases

Estimate Penetration

What portion is transitioning to next-generation/premium systems?

1. Assess Premium IOL & Material Adoption

2. Map Conventional vs Femtosecond Laser (FLACS) Splits

3. Evaluate Digital Architecture Integration

4. Factor in Reimbursement & Out-of-Pocket Constraints

Survey data and interviews with ophthalmic surgeons and ASC directors; distributor survey feedback

Revenue Conversion

How does unit volume become market revenue?

1. Collect Average Selling Prices (ASP)

2. Segment by revenue streams

3. Apply end-use channel share

4. Triangulate and validate

Hospital procurement/tender archives, distributor pricing sheets, import/export databases

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Device Maintenance & Infrastructure Requirements Analysis

Conducted a comprehensive technology assessment of the cataract surgery devices market, focusing on advancements in phacoemulsification systems, femtosecond cataract lasers (FLACS), surgical microscopes with intraoperative tools, and intraocular lens (IOL) delivery platforms. The analysis evaluated emerging trends such as AI-enabled surgical planning software, digitally-connected OR ecosystems, ergonomic fluidics management systems for chamber stability, and high-performance consumable materials. It further assessed the impact of these innovations on surgical safety, procedural efficiency (time-in-OR), patient outcomes (e.g., visual acuity, astigmatism management), and surgeon adoption. Additionally, the study reviewed ongoing R&D activities, product launches, global regulatory developments, and investments in next generation preoperative and intraoperative diagnostic and surgical technologies.

This analysis enables stakeholders to understand evolving technology trends shaping the cataract surgery device industry. It helps identify high-growth innovation areas, emerging competitive advantages, and future investment prospects. The findings support product development, strategic planning, technology adoption, and long-term market positioning across the ophthalmic surgery ecosystem.

Competitive Analysis

Conducted a detailed competitive assessment of leading cataract surgery device manufacturers, technological advancements, pricing strategies, geographic presence, service capabilities, patent portfolios, and product positioning innovations. The analysis examined competitive positioning across equipment and consumable segments while evaluating key differentiators such as manufacturing excellence, clinical support, R&D strategy, customer training programs, and global expansion initiatives influencing market dynamics.

This analysis enables stakeholders to evaluate competitive positioning, benchmark key market participants, and identify growth opportunities within the cataract surgery device market. It supports strategic decision-making related to mergers and acquisitions, partnerships, portfolio diversification, and planning for marketing, operations, and emerging healthcare markets.

Macroeconomic Analysis

Conducted a macroeconomic analysis of country-level opportunities within the cataract surgery device market across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The analysis evaluated healthcare infrastructure, cataract prevalence and surgical volume trends, private payer models for standalone vs. premium procedures, regulatory environments, and investments in advanced medical technologies. It further assessed country-specific economic drivers, system installation trends, healthcare spending patterns, and expansion opportunities for advanced platforms.

This analysis enables stakeholders to understand regional growth potential and market attractiveness across key geographic areas in the cataract surgery device industry. It supports expansion, investment, and strategic partnerships while providing insights into healthcare infrastructure readiness, reimbursement landscapes, and procedural volume trends driven by aging populations. The findings support regional geographic expansion and market penetration strategies within the global cataract surgery device industry.

Frequently Asked Questions About This Report

Some key players operating in the global cataract surgery devices market include Alcon Inc., Johnson & Johnson Vision, Bausch +Lomb, Carl Zeiss Meditec, HOYA Surgical Optics, NIDEC Co., Ltd, Rayner, STAAR Surgical, LENSAR, Inc., Ophtec BV.

Key drivers of the cataract surgery devices market include the rising prevalence of cataracts due to aging populations, advancements in surgical technologies such as femtosecond lasers and premium intraocular lenses, and the growing adoption of outpatient and minimally invasive procedures that improve patient outcomes and reduce recovery time.

North America dominated with a 38.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Phacoemulsification accounted for the largest revenue share in 2025, while femtosecond laser-assisted cataract surgery (FLACS) is the fastest-growing segment.

50 years & above segment held the largest revenue share in 2025, while 19-50 years segment is the fastest-growing area.

Hospitals held the largest revenue share in 2025, while ambulatory surgical centers (ASCs) is the fastest-growing area.

The global cataract surgery devices market size was valued at USD 7.5 billion in 2025 and is expected to reach a value of USD 8.0 billion in 2026.

The global cataract surgery devices market is expected to grow at a compound annual growth rate of 5.7% from 2026 to 2033 to reach USD 11.7 billion by 2033.

The intraocular lenses (IOL) devices segment accounted for the largest revenue share of 56.4% in 2025, due to the rising incidence of cataracts, an increasing demand for premium lenses, and technological advancements that have led to better visual outcomes and patient satisfaction.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.