- Home

- »

- Biotechnology

- »

-

Cell Reprogramming Market Size & Share Report, 2026-2033GVR Report cover

![Cell Reprogramming Market (2026 - 2033)Report]()

Cell Reprogramming Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology (Sendai Virus-based Reprogramming, mRNA Reprogramming, Episomal Reprogramming), By Application (Research, Therapeutic), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$440.7MMarket Estimate, 2026

$477.8MMarket Forecast, 2033

$859.5MCAGR, 2026–2033

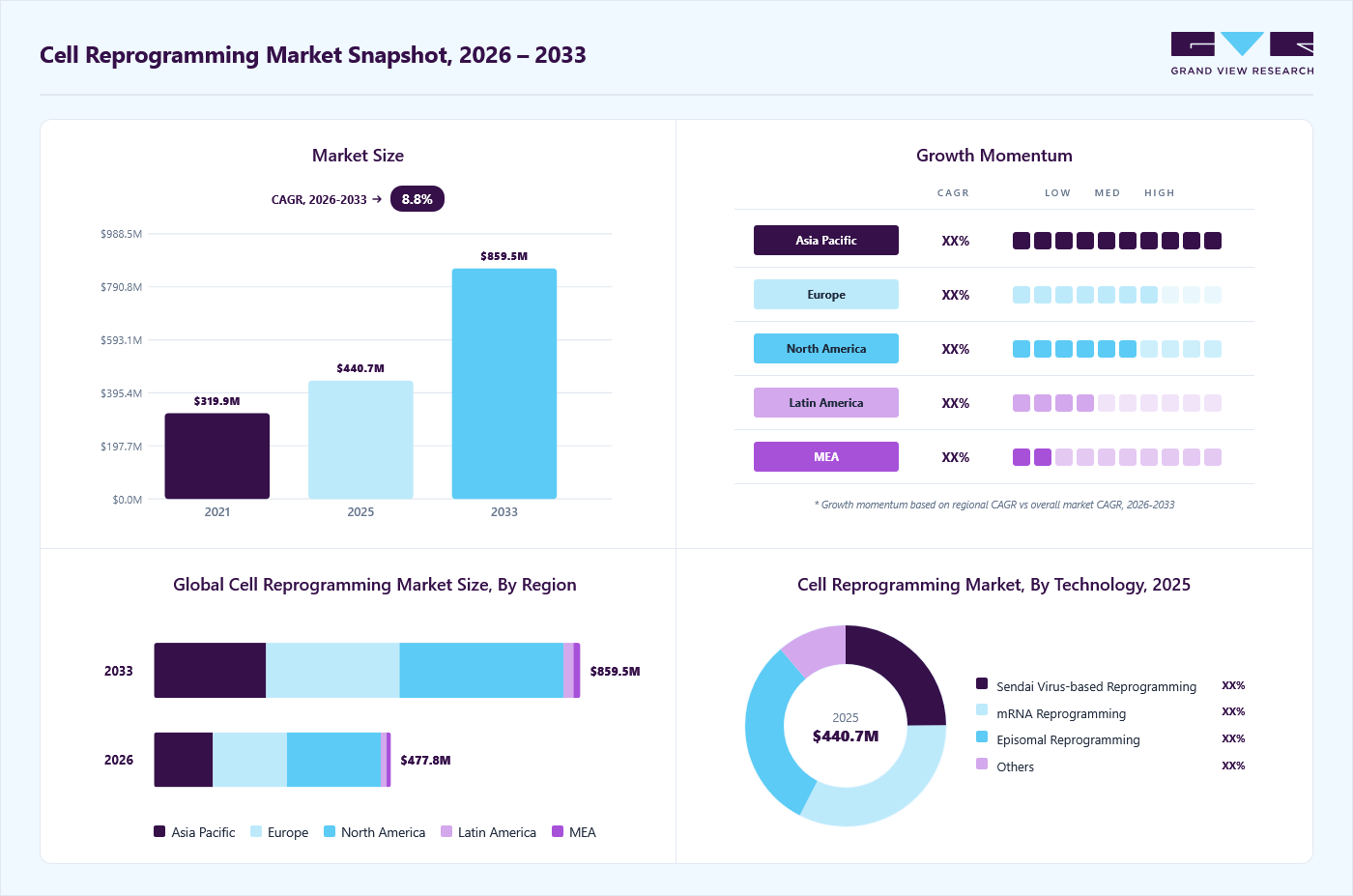

8.8%Cell Reprogramming Market Summary

The global cell reprogramming market size was valued at USD 440.7 million in 2025 and is projected to grow from USD 477.8 million in 2026 to USD 859.5 million by 2033, at a CAGR of 8.8% from 2026 to 2033. North America dominated the global market with the largest revenue share of 39.6% in 2025. This growth is supported by the rising interest in reprogramming technologies, particularly their role in transforming specialized cells into different cell types.

Key Market Trends & Insights

- By technology: mRNA reprogramming segment led the market with the largest revenue share of 32.6% in 2025.

- By application: Research segment led the market with the largest revenue share of 67.1% in 2025.

- By end-use: Research & academic institutes segment led the market with the largest revenue share of 67.1% in 2025.

Regional Highlights

- Largest regional market: North America (39.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The cell reprogramming market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market size in 2025: USD 440.7 Million

- Estimated market size in 2026: USD 477.8 Million

- Projected market size by 2033: USD 859.5 Million

- CAGR (2026-2033): 8.8%

The increased use of these techniques in cancer research drives market activity, along with a growing number of collaborations and partnerships that aim to accelerate research and development in this area. In January 2023, a collaboration was announced between Automata, a robotics and automation company in the life sciences sector, and bit.bio. This partnership focuses on developing automated systems to support bit. bio's work in cell reprogramming and precision reprogrammed human cells. Collaborations like this reflect how companies leverage automation and technology to improve the efficiency and scalability of cell reprogramming processes, helping expand their use in research and clinical applications. Such efforts streamline workflows, reduce manual errors, and accelerate the production of consistent, high-quality cell lines. These developments also contribute to reprogrammed cells' broader use in disease modeling, toxicity testing, and regenerative medicine. With the demand for reproducible and cost-effective solutions growing, strategic collaborations play a key role in shaping the market landscape.")

An emerging trend significantly impacting the industry is the integration of gene-editing technologies, particularly CRISPR, with reprogramming methods. The ability to precisely edit genes while reprogramming cells enhances reprogrammed cells' accuracy and functionality, offering new possibilities in areas such as disease modeling, regenerative medicine, and personalized treatments. In addition, these technologies enable the creation of disease-specific cell lines for research, which is crucial for understanding complex conditions such as cancer and neurodegenerative diseases. With advancements in gene editing continuing to evolve, they are expected to further drive the adoption of cell reprogramming across various biomedical applications, fostering innovation and expanding market potential.

Furthermore, the industry is experiencing significant advancements driven by innovative technologies and substantial investments. For instance, in September 2024, GC Therapeutics launched with USD 75 million in financing to advance its TFome platform, the world’s first “plug-and-play” induced pluripotent stem cell (iPSC) programming system. This platform integrates synthetic biology, gene editing, cell engineering, and machine learning to streamline the development of cell therapies across various therapeutic areas. Such breakthroughs are accelerating the transition of cell reprogramming technologies from research to clinical applications, expanding their potential in regenerative medicine and personalized treatments.

Market Dynamics

The cell reprogramming market is experiencing robust growth driven by increasing demand for regenerative medicine, stem cell research, disease modeling, and personalized therapies. Advances in induced pluripotent stem cell (iPSC) technology, gene editing tools, and cellular engineering techniques have expanded the potential applications of cell reprogramming across drug discovery, toxicology testing, and tissue regeneration. Growing investments from biotechnology and pharmaceutical companies, along with rising funding for stem cell research, are further supporting market expansion.

The increasing focus on regenerative medicine is a major factor driving the cell reprogramming market. Cell reprogramming technologies, particularly induced pluripotent stem cell (iPSC) platforms, enable the generation of patient-specific cells that can be used for tissue repair, disease treatment, and personalized therapeutic development. Rising prevalence of chronic diseases, neurodegenerative disorders, cardiovascular conditions, and organ failure has intensified the need for advanced treatment approaches. Additionally, growing investments in stem cell research, expanding clinical studies, and increasing collaboration between academic institutions and biotechnology companies are accelerating the adoption of cell reprogramming technologies across therapeutic and research applications.

The cell reprogramming market faces significant challenges related to the technical complexity of reprogramming processes and the substantial costs associated with research, development, and manufacturing. Achieving efficient and stable cellular reprogramming remains difficult, often requiring specialized expertise, sophisticated laboratory infrastructure, and extensive quality control measures. Variability in reprogramming outcomes, concerns regarding genomic instability, and the risk of tumorigenicity further complicate product development. Moreover, stringent regulatory requirements and lengthy validation procedures increase the time and financial resources needed to bring cell-based products to market, limiting broader commercialization.

The growing adoption of personalized medicine and advanced drug discovery platforms presents a significant opportunity for the cell reprogramming market. Reprogrammed cells, particularly patient-derived iPSCs, provide highly relevant models for studying disease mechanisms, screening drug candidates, and predicting patient-specific treatment responses. Pharmaceutical and biotechnology companies are increasingly utilizing these models to improve drug development efficiency and reduce clinical failure rates. Furthermore, advances in gene editing, artificial intelligence-driven cellular analysis, and scalable cell manufacturing technologies are expanding the commercial potential of cell reprogramming across precision therapeutics, regenerative medicine, and translational research applications.

Market Concentration & Characteristics

The industry demonstrates a high degree of innovation, largely driven by its transformative applications in regenerative medicine, disease modeling, and drug discovery. Scientific progress in induced pluripotent stem cells (iPSCs), direct lineage reprogramming, and genome editing technologies is driving research momentum. Academic institutions and biotech firms are exploring novel reprogramming techniques, such as non-integrating vectors and small-molecule approaches, to enhance safety and efficiency. While commercial translation is still in early stages, innovations in cell fate manipulation and personalized cell-based therapies continue to push the technological frontier.

The industry is characterized by strong collaboration across academia, research hospitals, and emerging biotechnology firms. Partnerships are focused on translational research, clinical validation, and platform development. Public-private consortia and joint ventures are also prominent, supporting GMP-grade reprogramming and quality-controlled production for clinical applications. Additionally, collaborations with CDMOs and CROs are growing to streamline process development and regulatory compliance, particularly for scalable cell manufacturing and international clinical trial support.

Regulatory frameworks play a crucial role in shaping the pace and direction of the cell reprogramming industry. Guidelines concerning genomic stability, vector safety, and long-term efficacy present high entry barriers. However, initiatives such as the FDA’s RMAT designation and Japan’s fast-track approvals for regenerative medicine offer more defined regulatory pathways. Compliance with global GMP and GTP standards remains critical for clinical translation and commercialization. Regulatory alignment across regions is also emerging, facilitating smoother international development.

Product expansion remains at a nascent but active stage, with most cell reprogramming-based therapies in early clinical or preclinical development. Efforts are focused on applications for neurodegenerative diseases, cardiovascular repair, and rare genetic disorders. Advances in autologous and allogeneic iPSC-derived therapies, alongside exploration of in vivo reprogramming strategies, support a pipeline of diversified therapeutic candidates. However, the lack of standardized protocols and scalability challenges continues to limit rapid product diversification in commercial pipelines.

Regional expansion is dynamic, with North America, Europe, and East Asia leading in R&D and clinical activities. Countries like the U.S., Japan, China, and the UK are investing heavily in research infrastructure and translational programs. Emerging regions in Southeast Asia and the Middle East are gaining traction through government-backed biotech initiatives and cross-border academic collaborations. Multinational firms are forming alliances with local research institutions and regulatory bodies to enable regional market entry and expand global trial networks.

Analyst Perspective

The cell reprogramming market is moving from an early-stage innovation landscape into a more structured translational ecosystem, where scientific progress is increasingly being evaluated through clinical and commercial viability. Strong momentum from induced pluripotent stem cell (iPSC) research, coupled with expanding use cases in disease modeling, regenerative therapies, and drug screening, is reshaping the competitive environment. However, scalability, reproducibility, and manufacturing standardization remain key bottlenecks that slow broader adoption. At the same time, rising partnerships between biotech firms, pharmaceutical companies, and academic institutions are accelerating technology validation and pipeline development. Overall, the market is expected to evolve steadily, with value creation concentrated among players that can effectively bridge laboratory breakthroughs with clinically scalable and regulator-ready solutions.

Emerging Trends and Innovations Shaping the Cell Reprogramming Market

Integration of AI and Machine Learning in Cell Reprogramming

The industry is evolving rapidly, with several technological advancements playing a key role in driving progress. A significant development is the integration of artificial intelligence (AI) and machine learning into reprogramming processes. AI technologies are being increasingly applied to optimize reprogramming protocols, predict genetic outcomes, and enhance gene editing techniques. For example, in October 2024, Shift Bioscience, a UK-based biotech company, completed a USD 16 million seed funding round to advance its AI-powered platform for cellular reprogramming. This platform utilizes generative AI models to predict gene-based interventions capable of safely rejuvenating human cells, offering promising implications for regenerative medicine and age-related disease therapies. These innovations reduce the time and costs associated with reprogramming cells, making the process more scalable and applicable to various therapeutic areas.

Advancements in Genome Editing Tools Enhancing Cell Reprogramming

Advances in genome editing tools such as CRISPR, prime editing, and base editing are significantly transforming the landscape of cell reprogramming. These technologies enable more precise and controlled genetic modifications, which are crucial for applications in gene therapy, personalized medicine, and regenerative medicine. In 2023, Prime Medicine demonstrated breakthroughs in prime editing, showcasing its ability to correct genetic mutations with enhanced precision and safety in reprogrammed cells. The development of their PASSIGE platform, which allows the insertion of large genetic sequences into cells, further improves gene-editing techniques. These innovations are opening new possibilities for treating a wide range of complex diseases, from genetic disorders to cancer, solidifying genome editing as a key driver in the evolution of cell reprogramming.

Growth of Organoid Development in Cell Reprogramming Applications

Organoid development is also gaining significant traction within the field of cell reprogramming. These 3D miniature, simplified versions of organs provide more accurate disease models and are increasingly used in disease modeling, drug discovery, and personalized treatments. In September 2023, Stanford University's Kuo Lab received an Arc Institute Ignite Award to collaborate on developing novel organoid technologies, reflecting the growing interest and investment in this area. Organoids enable researchers to test new therapies on human-like tissues rather than relying on animal testing, making them a critical tool in accelerating research and treatment development. With continuous advancements, organoid technologies are expected to revolutionize disease research and treatment, offering highly personalized solutions and improving clinical trial effectiveness. The integration of organoid development with reprogrammed cells is expanding the potential of cell reprogramming across various therapeutic applications.

Technology Insights

Based on technology, the mRNA reprogramming segment led the market with the largest revenue share of 32.6% in 2025. This dominance can be attributed to the growing preference for non-integrating methods that minimize the risk of insertional mutagenesis. mRNA-based reprogramming offers a safer and more efficient approach for generating induced pluripotent stem cells (iPSCs) without altering the host genome. Researchers and developers increasingly favor this method for its high reprogramming efficiency, rapid expression, and suitability for clinical-grade applications. Its scalability and compatibility with Good Manufacturing Practice (GMP) standards have further supported its widespread adoption in regenerative medicine and therapeutic development.

The Sendai virus-based reprogramming segment is expected to grow at a significant CAGR over the forecast period. This growth can be attributed to the method's efficiency and ability to generate induced pluripotent stem cells (iPSCs) without integrating into the host genome. The Sendai virus-based reprogramming approach is recognized for maintaining high reprogramming efficiency while minimizing the risk of genomic alterations, making it particularly attractive for therapeutic applications. In addition, advancements in virus-free reprogramming protocols and improvements in the delivery of reprogramming factors are expected to further drive the adoption of this technology in clinical and research settings. Researchers are increasingly utilizing this method to develop disease models, explore regenerative therapies, and accelerate drug discovery, reinforcing its growth potential in the market.

Application Insights

Based on application, the research segment led the market with the largest revenue share of 67.1% in 2025. This dominance is driven by the extensive use of cell reprogramming techniques, such as induced pluripotent stem cells (iPSCs), in studying cell biology, disease modeling, and drug discovery. These techniques provide researchers with a versatile platform for investigating cellular mechanisms and developing novel therapies. Several academic and research institutions, such as Gladstone Institutes and the Salk Institute for Biological Studies, actively employ reprogramming technologies to explore regenerative treatments and improve disease modeling capabilities. This widespread use reinforces the importance of cell reprogramming in both fundamental and translational research.

The therapeutic segment is projected to grow at the fastest CAGR during the forecast period. This rapid growth is driven by the increasing application of cell reprogramming techniques in developing treatments for various diseases, including neurodegenerative disorders, heart diseases, and genetic conditions. The ability to reprogram cells into specific cell types offers promising potential for regenerating damaged tissues and repairing organs. Researchers are particularly focused on how these techniques can be used to create personalized therapies and improve the effectiveness of treatments for conditions that currently have limited therapeutic options. Along with the rise in scientific research surrounding cell reprogramming therapeutics, businesses are making significant strides to commercialize these technologies. For instance, Asgard Therapeutics AB received approval from the U.S. Patent & Trademark Office for a patent related to reprogramming cells into dendritic cells, which is expected to protect and promote innovation in the field until 2038. This development is anticipated to drive demand for reprogramming technology and further contribute to market growth.

End-use Insights

Based on end use, the research & academic institutes segment led the market with the largest revenue share of 67.1% in 2025. This significant share is due to the increasing adoption of cell reprogramming techniques, such as induced pluripotent stem cells (iPSCs), in academic and research settings for various applications, including disease modeling, drug discovery, and stem cell research. Research and academic institutions are leveraging these technologies to deepen their understanding of cellular mechanisms, explore potential treatments, and develop personalized therapies. The ability to generate patient-specific cell lines has further enhanced the value of cell reprogramming in drug testing and disease modeling, enabling more accurate and predictive outcomes. Prominent research institutions such as the Harvard Stem Cell Institute, the Salk Institute for Biological Studies, and the Gladstone Institutes are at the forefront of exploring the therapeutic potential of reprogrammed cells, driving innovation in areas like regenerative medicine and targeted cancer therapies. With the demand for more personalized and precise research continuing to grow, the research & academic institutes segment is expected to maintain its leadership in the market.

The biotechnology & pharmaceutical companies segment is projected to register the fastest CAGR during the forecast period. This growth is driven by the increasing application of cell reprogramming techniques in drug discovery, personalized medicine, and therapeutic development. These techniques enable companies to develop patient-specific models, improving drug testing accuracy and efficiency. For instance, in December 2024, Sumitomo Chemical and Sumitomo Pharma established a joint venture named RACTHERA Co., Ltd., focused on regenerative medicine and cell therapy. The collaboration aims to accelerate the development and commercialization of iPSC-based treatments by combining pharmaceutical expertise with industrial engineering capabilities. Such initiatives highlight the expanding role of biotechnology and pharmaceutical companies in shaping the future of the cell regeneration market.

Regional Insights

North America dominated the cell reprogramming market with the largest revenue share of 39.6% in 2025. The high revenue share is supported by the presence of major companies in the region. In addition, many firms are taking strategic steps to grow their business and strengthen their role in the market. For instance, in July 2023, Stem Genomics SAS and Pluristyx, Inc. entered into a partnership along with an equity investment in Stem Genomics. This collaboration is designed to offer a smoother process for checking the genetic quality of Pluristyx's pluripotent stem cell (PSC) lines, using the iCS-digital PSC assay developed by Stem Genomics. Such efforts continue to support the growth of the cell reprogramming market in North America.

U.S. Cell Reprogramming Market Trends

The cell reprogramming market in the U.S. held the largest share in the North America region in 2025. The U.S. cell reprogramming market is experiencing significant growth, driven by strong research activities and substantial investments in regenerative medicine. The increasing focus on personalized medicine and the application of cell reprogramming techniques, such as CRISPR and iPSC, in drug discovery and therapy development, is fueling market expansion. The presence of leading biotechnology companies, research institutions, and a favorable regulatory environment further supports innovation in the sector. In addition, the growing demand for more effective treatments for chronic diseases and collaborations between biotech firms and research organizations continue to strengthen the U.S.'s role in advancing cell reprogramming technologies.

Asia Pacific Cell Reprogramming Market Trends

Asia Pacific cell reprogramming market is projected to grow at the highest CAGR of 9.17% during the forecast period. This growth is driven by factors such as the rising prevalence of chronic conditions, widespread adoption of products for analysis and visualization, advancements in technology, and increased investments in R&D. In addition, numerous companies are expanding their studies based on multiomics, further supporting market expansion. For example, in February 2023, Novo Nordisk A/S and Heartseed, Inc. made a significant advancement by administering the first dose in their Phase 1/2 clinical study (LAPiS Study) for HS-001, a cell therapy aimed at treating heart failure. HS-001, derived from iPSCs, uses purified heart muscle cell clusters to potentially restore heart function in patients with advanced heart failure. Such developments highlight the growing focus on regenerative medicine in the Asia Pacific region, driving the market's growth during the forecast period.

Japan cell reprogramming market dominated the Asia Pacific region in 2024. The country’s strong focus on regenerative medicine, coupled with significant government support and a well-established biotechnology sector, has driven the growth of cell reprogramming technologies. Japan’s aging population and increasing healthcare demands have further fueled the need for advanced therapeutic solutions, such as iPSCs. Prominent research institutions, such as RIKEN, a renowned research institution in Japan, and Kyoto University, continue to lead innovations in stem cell research. RIKEN has significantly contributed to the development of iPSCs, while Kyoto University has been involved in the clinical applications of iPSC technologies. These efforts further drive the growth of the cell reprogramming market in Japan.

China cell reprogramming market is driven by substantial government support, strategic investments, and a rapidly advancing biotechnology sector. The country has strongly emphasized stem cell research and regenerative medicine, fostering innovations in cell reprogramming technologies. Institutions such as Tsinghua University and companies like Boya Life are at the forefront of developing iPS cell-based therapies for cardiovascular diseases and neurological disorders. These advancements are further supported by government funding and policies that promote collaboration between the academic, research, and private sectors. With a large population and growing healthcare needs, China plays a crucial role in the growth of the cell reprogramming market.

Europe Cell Reprogramming Market Trends

Europe cell reprogramming industry is supported by robust research efforts, academic leadership, and a regulatory environment that encourages innovation in regenerative medicine. Countries such as Germany, the UK, and France are advancing stem cell research, particularly in developing and applying induced pluripotent stem (iPS) cells for disease modeling and potential therapeutic use. Research institutions and universities across the region are actively engaged in exploring cell reprogramming technologies, while the European Medicines Agency (EMA) provides a supportive regulatory framework that facilitates clinical trials and early-stage commercialization of cell-based therapies.

In addition, cross-border collaborations funded under initiatives like Horizon Europe promote targeted cell reprogramming research. Partnerships between academic centers and biotechnology firms further drive innovation in treating degenerative, cardiovascular, and neurological disorders. Together, these factors are strengthening Europe’s contribution to the global expansion of the cell reprogramming market.

The UK cell reprogramming market is driven by its strong academic infrastructure, government-supported research initiatives, and expanding biotechnology sector. Leading universities and research institutions in the UK are at the forefront of advancing cell reprogramming technologies, particularly in developing induced pluripotent stem (iPS) cells for therapeutic applications. The UK government has provided targeted funding and established strategic programs to support regenerative medicine, fostering innovation in disease modeling and cell-based therapies. Regulatory frameworks from the Medicines and Healthcare products Regulatory Agency (MHRA) facilitate clinical research and the early-stage development of reprogrammed cell therapies. In addition, the UK is actively engaged in European collaborations focused on cell reprogramming, with biotechnology companies working alongside academic centers to translate research into clinical solutions for neurological, cardiovascular, and degenerative diseases. These factors collectively enhance the UK's role in driving the cell reprogramming market forward.

Germany cell reprogramming market is driven by its advanced research infrastructure, government-backed funding, and strong academic-industry collaborations. The country's well-established biotechnology ecosystem supports the development of induced pluripotent stem (iPS) cell technologies, with institutions like the Fraunhofer Institute and the Max Planck Institute playing key roles in stem cell research and regenerative medicine. Germany's regulatory environment, overseen by the Federal Institute for Drugs and Medical Devices (BfArM), ensures clear pathways for clinical research and the commercialization of cell-based therapies. The country's focus on regenerative medicine is further supported by public-private partnerships that drive innovation. Germany's aging population and increasing prevalence of chronic conditions like neurological and cardiovascular diseases also contribute to the growing demand for cell reprogramming-based therapies.

Middle East & Africa Cell Reprogramming Market Trends

The Middle East and Africa cell reprogramming market is driven by increasing investments in biotechnology and healthcare innovation. Several countries in the region, including the UAE, Saudi Arabia, and South Africa, are making strides in advancing stem cell research and regenerative medicine. Government-backed initiatives and partnerships with international research institutions are fostering the development of cell reprogramming technologies, particularly in areas like disease modeling and regenerative therapies. In addition, the growing demand for advanced medical treatments and a rising healthcare burden due to chronic diseases are propelling interest in cell-based therapies. While the regulatory landscape across MEA is still evolving, there is a clear focus on creating frameworks that support the safe application and commercialization of cell reprogramming technologies. With the region continuing to invest in healthcare innovation and research, its role in the cell reprogramming market is expected to expand, particularly with more collaborations and clinical trials being initiated.

Saudi Arabia cell reprogramming market is driven by its substantial investments in biotechnology and regenerative medicine. The country's Vision 2030 initiative, which emphasizes healthcare innovation and scientific research, is fueling the development of cutting-edge technologies, including cell reprogramming. Saudi Arabia's government has been instrumental in funding stem cell research and fostering partnerships with international research institutions to promote advancements in regenerative therapies. Key research institutions and universities are focused on exploring induced pluripotent stem (iPS) cells for disease modeling and potential therapeutic applications. In addition, the rising demand for advanced medical treatments and the country's growing healthcare needs further drive the adoption of cell-based therapies. With Saudi Arabia continuing to strengthen its biotechnology infrastructure and regulatory frameworks, its role in the cell reprogramming market is expected to grow, particularly with more clinical trials and research collaborations emerging.

The UAE cell reprogramming market is driven by substantial investments in biotechnology, healthcare innovation, and a strong commitment to advancing regenerative medicine. The UAE government has been instrumental in supporting stem cell research and fostering international collaborations. Key institutions like the United Arab Emirates University and the Abu Dhabi Stem Cells Centre are at the forefront of advancing stem cell technologies, while the opening of GMP-certified facilities in Dubai further strengthens the region's biotechnology infrastructure. The growing demand for advanced medical treatments and innovative therapies, combined with the UAE's robust regulatory environment, positions the country as a regional leader in cell reprogramming and regenerative medicine.

Key Cell Reprogramming Company Insights

Key players are undertaking various strategic initiatives to maintain their market presence. In addition, numerous strategic initiatives enable market players to strengthen their business avenues. In addition, several market players are acquiring smaller players to strengthen their market position. This strategy enables companies to increase their capabilities, expand their product portfolios, and improve their competencies.

Key Cell Reprogramming Companies:

The following key companies have been profiled for this study on the cell reprogramming market.

-

Thermo Fisher Scientific Inc.

-

Allele Biotechnology and Pharmaceuticals Inc.

-

ALSTEM

-

STEMCELL Technologies

-

Merck KGaA

-

Bio-Techne

-

REPROCELL Inc.

-

Lonza

-

FUJIFILM Corporation (Fujifilm Cellular Dynamics)

-

Mogrify Limited

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g., Thermo Fisher Scientific Inc.; Merck KGaA; Lonza; STEMCELL Technologies; Bio-Techne)

- Focus on expanding integrated cell reprogramming workflows including iPSC generation kits, culture media, reprogramming vectors, growth factors, and downstream differentiation solutions. Strengthen presence through acquisitions, partnerships with biotech firms, and expansion of GMP-compliant stem cell manufacturing and cell therapy support services. Invest in scalable automation, standardized reprogramming platforms, and clinical-grade stem cell solutions.

- Strong global distribution networks, broad and validated product portfolios, high regulatory compliance capability, and deep integration into pharmaceutical and academic research ecosystems. Ability to provide end-to-end solutions from reprogramming to differentiation enhances customer retention and recurring revenues.

- High operational costs, complex regulatory and manufacturing requirements, and slower adaptability to niche or rapidly evolving reprogramming technologies. Limited flexibility in highly customized or experimental workflows compared to smaller innovators.

Emerging Players (e.g., FUJIFILM Corporation (Fujifilm Cellular Dynamics); REPROCELL Inc.; Allele Biotechnology and Pharmaceuticals Inc.; ALSTEM; Mogrify Limited)

- Focus on proprietary cell reprogramming platforms, iPSC generation technologies, direct cell conversion approaches, and disease-specific cell model development. Emphasize innovation in non-integrating methods, transgene-free reprogramming, and scalable cell therapy manufacturing solutions. Expand through collaborations with pharma companies and translational research institutes.

- High innovation intensity, strong IP portfolios in reprogramming and cell conversion technologies, and ability to rapidly translate research-grade protocols into therapeutic and industrial applications. Strong positioning in regenerative medicine and personalized cell therapy development.

- Limited large-scale manufacturing infrastructure compared to global life science giants, dependence on partnerships and funding, and regulatory and commercialization challenges in scaling therapeutic applications.

Recent Developments

-

In June 2026, NewLimit had raised $435 million to advance its cellular reprogramming research and to initiate its first human clinical trials. The funding was directed toward developing partial reprogramming approaches targeting age-related diseases and supporting key preclinical and translational studies. This investment also strengthened its efforts to expand research capabilities and progress toward clinical validation.

-

In March 2025, RegCell, Inc., a biotechnology company developing first-in-class therapies for autoimmune diseases and transplantation using its epigenetic reprogramming platform based on the natural biology of regulatory T-cells (Tregs), had announced the closing of an oversubscribed seed funding round along with its transition to a U.S.-based company.

Cell Reprogramming Market Report Scope

Report Attribute

Details

Market size in 2025

USD 440.7 million

Estimated market size in 2026

USD 477.8 million

Projected market size by 2033

USD 859.5 million

Growth rate

CAGR of 8.8% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

Thermo Fisher Scientific Inc.; Allele Biotechnology and Pharmaceuticals Inc.; ALSTEM; STEMCELL Technologies; Merck KGaA; Bio-Techne; REPROCELL Inc.; Lonza; FUJIFILM Corporation (Fujifilm Cellular Dynamics); Mogrify Limited

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cell Reprogramming Market Report Segmentation

This report forecasts revenue growth at the global, regional and country levels and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cell reprogramming market report on the basis of technology, application, end-use, and region:

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Sendai Virus-based Reprogramming

-

mRNA Reprogramming

-

Episomal Reprogramming

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Research

-

Therapeutic

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Research & Academic Institutes

-

Biotechnology & Pharmaceutical Companies

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

The cell reprogramming market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each cell reprogramming segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Technology

Revenue capture definition

Sendai Virus-based

Reprogramming

Revenue is generated through the sale of Sendai virus vectors, reprogramming kits, cell culture reagents, and related services used to generate induced pluripotent stem cells (iPSCs). This technology is widely adopted due to its high reprogramming efficiency and non-integrating nature, making it suitable for research and therapeutic development applications.

mRNA Reprogramming

Revenue is captured from mRNA-based reprogramming kits, synthetic mRNA products, transfection reagents, and associated services that enable efficient generation of iPSCs without genomic integration. Demand is driven by increasing interest in clinically compatible and safer cell reprogramming approaches.

Episomal Reprogramming

Revenue is derived from episomal plasmids, vector systems, reprogramming reagents, and supporting services used to create iPSCs through non-viral methods. The segment benefits from growing demand for cost-effective and integration-free reprogramming technologies in regenerative medicine and stem cell research.

Others

Revenue is generated from alternative cell reprogramming technologies including lentiviral vectors, retroviral methods, protein-based reprogramming, microRNA-mediated reprogramming, and emerging genome engineering approaches designed to improve reprogramming efficiency and cell quality.

Segment - Application

Revenue capture definition

Research

Revenue is generated through the use of cell reprogramming technologies in disease modeling, developmental biology, stem cell research, drug discovery, toxicology studies, and functional genomics. Academic institutions, research organizations, and biotechnology companies represent major contributors to this segment.

Therapeutic

Revenue is captured from cell reprogramming products and services utilized in regenerative medicine, cell therapy development, tissue engineering, personalized medicine, and advanced therapeutic research. Growing investments in iPSC-based therapies and precision medicine are driving demand within this segment.

Segment - End Use

Revenue capture definition

Research & Academic Institutes

Revenue is derived from universities, government-funded laboratories, stem cell research centers, and academic institutions purchasing reprogramming kits, vectors, reagents, and related services for basic and translational research activities.

Biotechnology & Pharmaceutical

Companies

Revenue is generated through the procurement of cell reprogramming technologies, custom cell engineering services, and iPSC development platforms by biotechnology and pharmaceutical companies engaged in drug discovery, disease modeling, regenerative medicine research, and cell therapy development.

Estimation Model

Top Down

Parent Market Model

Segmentation

Validation

Forecasting

Commodity Flow Analysis: Market size was estimated using revenues of key cell reprogramming companies, supported by company reports, investor presentations, distributor insights, premium databases, and primary research.

Parent Market & Penetration-Based Analysis: The cell reprogramming market was derived from the regenerative medicine and cell therapy market using penetration rates, industry benchmarks, funding trends, and adoption levels.

Country-Level Segment Share Modeling: Market shares were estimated using country-specific adoption patterns, healthcare infrastructure, reimbursement scenarios, product penetration rates, and weighted regional calculations.

Data Triangulation & Validation Model: Market estimates were validated through secondary research, primary interviews, company-level revenue assessments, and demand-side adoption analysis to ensure consistency and accuracy.

Forecasting & CAGR Modeling: Market forecasts and CAGR were projected using historical trends, technology adoption, product innovation, healthcare expenditure, regulatory developments, and regression-based trend analysis.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cell Reprogramming Market Landscape & Technology Adoption Analysis

Developed a tailored assessment of the global cell reprogramming market across key technologies including Sendai virus-based, mRNA-based, episomal, and other emerging reprogramming approaches. The analysis also covers applications in research and therapeutic development, along with end-use segmentation across academic institutes and biotechnology & pharmaceutical companies. Emphasis is placed on induced pluripotent stem cell (iPSC) generation, transgene-free approaches, and advancements in non-integrating reprogramming systems.

Enables stakeholders to understand evolving stem cell engineering technologies, identify high-growth non-viral and clinically compatible reprogramming platforms, evaluate adoption trends in regenerative medicine and disease modeling, and assess long-term therapeutic potential in personalized medicine and cell-based therapies.

Competitive Landscape & iPSC Platform Benchmarking Assessment

Delivered a customized benchmarking of leading cell reprogramming solution providers, including life science tool companies and specialized stem cell technology firms. The study evaluates reprogramming efficiency, safety profiles, scalability, GMP-compliance readiness, differentiation capabilities, and proprietary iPSC generation platforms.

Provides actionable insights into competitive positioning, technology differentiation, intellectual property strength, and platform maturity, helping clients identify collaboration opportunities, licensing potential, and emerging leaders in regenerative medicine and stem cell engineering markets.

Therapeutic & Translational Research Opportunity Assessment

Conducted a focused evaluation of cell reprogramming applications in regenerative medicine, disease modeling, drug discovery, and personalized therapy development. The analysis also assessed clinical translation pathways, scalability challenges, and integration of iPSC-derived models in precision medicine workflows.

Supports strategic decision-making by identifying high-value therapeutic opportunities, enabling prioritization of investment in regenerative medicine pipelines, improving translational research strategies, and strengthening long-term positioning in next-generation cell therapy and personalized healthcare ecosystems.

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

the mRNA reprogramming segment led the market with the largest revenue share of 32.6% in 2025.

the research segment led the market with the largest revenue share of 67.1% in 2025.

the research & academic institutes segment led the market with the largest revenue share of 67.1% in 2025.

The global cell reprogramming market size was estimated at USD 440.7 million in 2025 and is expected to reach USD 477.8 million in 2026.

The global cell reprogramming market is expected to grow at a compound annual growth rate of 8.8% from 2026-2033 to reach USD 859.5 million by 2033.

Some key players operating in the cell reprogramming market include Thermo Fisher Scientific, Inc., Allele Biotech, ALSTEM, STEMCELL Technologies Inc., Merck KGaA, Bio-Techne, REPROCELL, Lonza, FUJIFILM Corporation (Fujifilm Cellular Dynamics), and Mogrify Limited, among others

The growth of the cell reprogramming market can be attributed to the growing focus on cell reprogramming technology, increasing adoption of cell reprogramming in cancer research, and emphasis on collaboration and partnerships among key players in the market.

North America dominated the cell reprogramming market with a share of 39.6% in 2025. This major share can be supported by ongoing iPSC technology advancements and the availability of functional cells for pre-clinical drug testing.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.