- Home

- »

- IT Services & Applications

- »

-

Cloud Encryption Market Size Report, 2025-2030GVR Report cover

![Cloud Encryption Market Size, Share & Trends Report]()

Cloud Encryption Market (2025 - 2030) Size, Share & Trends Analysis Report By Component (Solution, Services), By Service Model, By Enterprise Size, By Application, By Industry Vertical, By Region, And Segment Forecasts

Market Size, 2024

$3.4BMarket Estimate, 2026

$7.3BMarket Forecast, 2030

$21.2BCAGR, 2025–2030

30.2%Cloud Encryption Market Summary

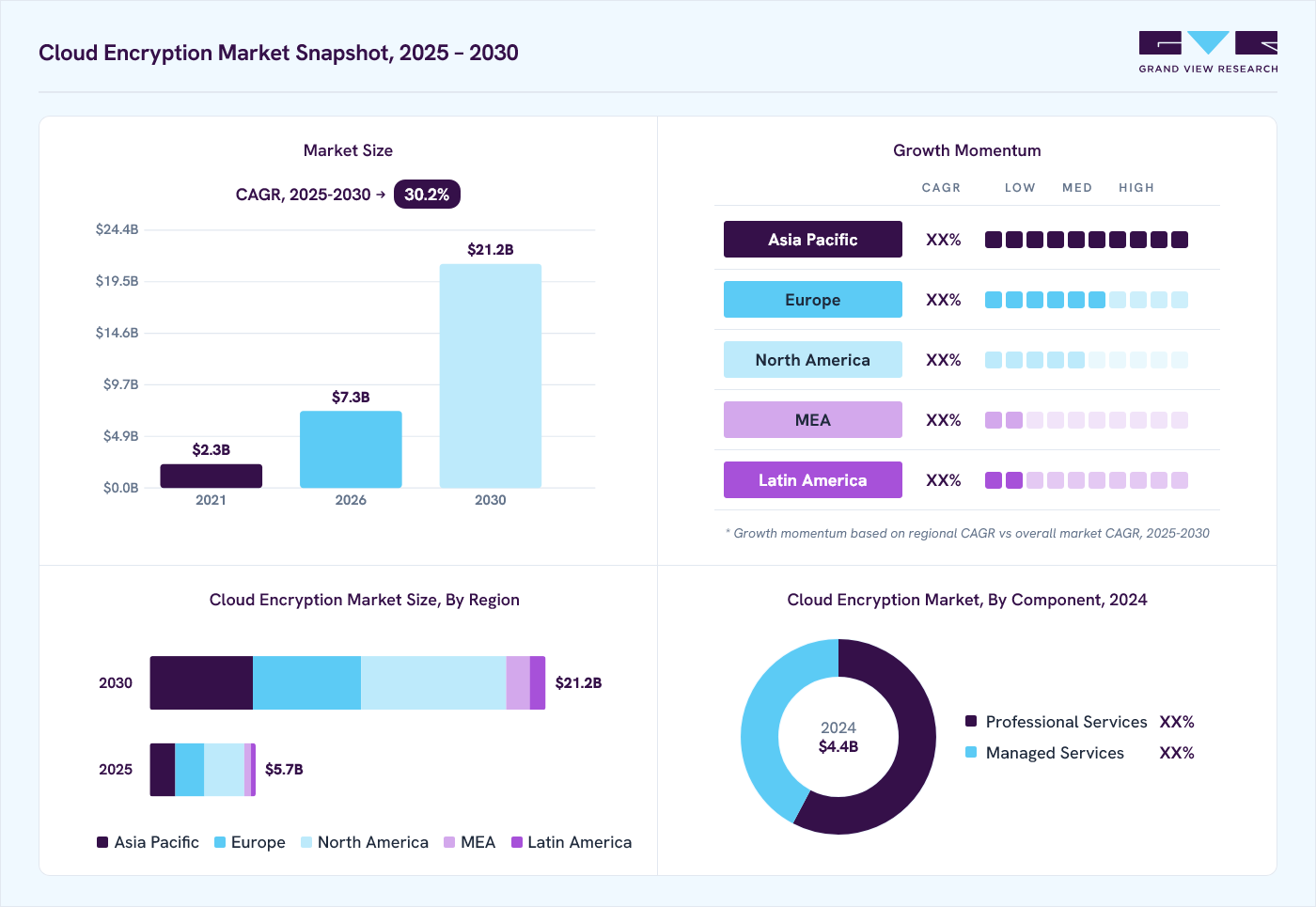

The global cloud encryption market size was valued at USD 4.4 billion in 2024 and is projected to grow from USD 7.3 billion in 2026 to USD 21.2 billion by 2030, at a CAGR of 30.2% from 2025 to 2030. North America dominated the market, accounting for a revenue share of 37.0% in 2024. The rise in cyber threats and sophisticated hacking techniques is a major factor propelling the cloud encryption industry.

Key Highlights:

- The U.S. cloud encryption market is projected to grow from 2025 to 2030.

- By component, the solution segment accounted for the largest market share of over 69.0% in 2024 in the market.

- By service model, the infrastructure-as-a-service segment dominated the market and accounted for a revenue share of over 39.0% in 2024 in the market.

- By enterprise size, the large enterprises segment dominated the market and accounted for a revenue share of over 66.0% in 2024 in the cloud encryption industry.

As cybercriminals become more adept at penetrating cloud-based systems, encryption is increasingly being viewed as a non-negotiable line of defense. Modern cyberattacks often aim to steal, tamper with, or ransom sensitive data stored in the cloud. Encryption significantly reduces the likelihood of attackers accessing usable information, making it an essential component of a layered cybersecurity strategy. With cybercrime growing in frequency and impact, both small and large enterprises are prioritizing encryption to protect digital assets.

The increased adoption of hybrid and multi-cloud strategies is accelerating the need for consistent and interoperable encryption solutions. Businesses are increasingly spreading their workloads across public, private, and hybrid clouds to enhance performance, ensure redundancy, and reduce costs. However, managing data security across these diverse environments is complex. Cloud encryption allows organizations to maintain control over their data by securing it regardless of the platform or service provider. This interoperability is crucial for companies that want to ensure end-to-end data protection while maintaining agility in their IT infrastructure.

The growth of the remote workforce and the proliferation of BYOD (Bring Your Own Device) policies have also fueled the demand for cloud encryption. With more employees accessing corporate systems and sensitive data from personal devices and remote locations, the risk of unauthorized access and data leakage has increased significantly. Cloud encryption enables secure access to information by ensuring that data remains protected both in transit and at rest. This is particularly important for organizations seeking to maintain productivity without compromising on security in a distributed work environment.

Furthermore, advancements in encryption technologies such as homomorphic encryption, quantum-safe encryption, and end-to-end encryption have broadened the capabilities and appeal of cloud encryption. These innovations are making it easier to process encrypted data without exposing it and are increasing trust in cloud services. As these technologies mature and become more commercially viable, they are expected to further drive adoption in industries requiring high confidentiality and integrity levels, such as defense, legal services, and research institutions.

Component Insights

The solution segment accounted for the largest market share of over 69.0% in 2024 in the market. The shift toward remote and distributed work environments accelerated the adoption of cloud encryption solutions. As employees increasingly access corporate systems and data from various locations and devices, ensuring secure transmission and storage of information has become critical. Encryption solutions that offer endpoint integration, secure file sharing, and user behavior analytics are gaining traction, enabling organizations to uphold strong data protection policies in a decentralized workforce model. This trend is particularly pronounced among small and medium enterprises (SMEs) that seek cost-effective, easy-to-deploy solutions to maintain security and compliance.

The services segment is anticipated to grow at the highest CAGR during the forecast period. The increasing reliance on managed security services is driving the segment's growth. With the rise in cloud adoption, businesses, especially small and medium enterprises (SMEs), turn to third-party providers for their encryption and data protection needs. Managed service providers (MSPs) offer 24/7 monitoring, automated key management, and ongoing threat detection, all of which alleviate the burden on internal IT teams and ensure a higher level of security. This is particularly critical in sectors such as finance, healthcare, and retail, where sensitive data must be encrypted and monitored continuously to comply with stringent regulatory frameworks.

Service Model Insights

The infrastructure-as-a-service segment dominated the market and accounted for a revenue share of over 39.0% in 2024 in the market. Organizations are migrating their IT infrastructure to IaaS environments like AWS, Azure, and Google Cloud to gain scalability, flexibility, and cost efficiencies. This migration necessitates robust encryption solutions to protect sensitive data stored and processed within these cloud environments. Furthermore, stringent data security regulations and compliance requirements, such as GDPR, HIPAA, and PCI DSS, are compelling organizations to implement strong encryption measures to safeguard their data in the cloud. The rising frequency and sophistication of cyberattacks, including data breaches and ransomware, further accentuate the need for advanced encryption solutions to mitigate these risks. Additionally, the growing awareness of the shared responsibility model in cloud computing, where providers are responsible for the security of the cloud while customers are responsible for security in the cloud, is driving increased adoption of encryption solutions by IaaS users.

The platform-as-a-service segment is expected to register a CAGR of 30.3% from 2025 to 2030. Rising concerns about multi-tenancy risks in PaaS environments drive the demand for encryption. Since multiple organizations often share PaaS platforms, isolating and protecting each tenant's data is necessary. Encryption, particularly when combined with robust key management and access control mechanisms, ensures data confidentiality even in shared infrastructure. Customers increasingly expect their PaaS providers to offer tenant-level encryption and fine-grained control over encryption keys, including bring-your-own-key (BYOK) and hold-your-own-key (HYOK) models.

Enterprise Size Insights

The large enterprises segment dominated the market and accounted for a revenue share of over 66.0% in 2024 in the cloud encryption industry. The escalation of data breach risks and sophisticated cyber threats is driving the segment's growth. Large enterprises are often targeted by advanced persistent threats (APTs), ransomware, and insider threats, which can exploit vulnerabilities in cloud-based systems. Encryption acts as a crucial line of defense, rendering data unreadable to unauthorized users even in the event of a breach. This is particularly important as many large companies operate in sectors such as finance, healthcare, and defense, where the impact of data leaks can be catastrophic financially.

The small and medium enterprises (SMEs) segment is expected to register a CAGR of 27.6% from 2025 to 2030. The growing use of third-party cloud applications by SMEs is also pushing the need for encryption. Many SMEs integrate cloud-based tools for HR, accounting, project management, and customer service to streamline their operations. While these tools improve efficiency, they often require businesses to share and store sensitive information on external platforms. Encrypting this data before or during transit to the cloud adds a critical layer of security, mitigating the risk posed by potential vulnerabilities in third-party systems.

Application Insights

The data encryption segment dominated the market and accounted for a revenue share of over 39.0% in 2024 in the cloud encryption industry. The growing availability of advanced encryption technologies, such as homomorphic encryption, quantum-resistant algorithms, and data-centric security platforms, is enhancing the capabilities of the data encryption segment. These innovations offer higher levels of protection without compromising performance or scalability, making them attractive for enterprises seeking both security and operational efficiency. As these technologies become more mature and accessible, organizations are more willing to invest in comprehensive data encryption strategies that align with their cloud transformation goals.

The database encryption segment is expected to register a CAGR of 30.6% from 2025 to 2030. Advancements in homomorphic and format-preserving encryption technologies are making database encryption practical for real-time business applications. These emerging encryption methods allow for computations on encrypted data without needing to decrypt it first, preserving both security and performance. As these technologies mature, they are expected to catalyze further the adoption of cloud database encryption, particularly in sectors like healthcare, finance, and defense, where real-time processing of sensitive data is mission-critical.

Industry Vertical Insights

The BFSI segment accounted for the largest market share of over 31.0% in 2024 in the cloud encryption industry. The trend toward open banking and API-based financial ecosystems is driving the integration of third-party apps and platforms, increasing the attack surface. In such scenarios, cloud encryption is a critical safeguard, enabling secure data sharing across APIs while maintaining confidentiality. As open banking expands globally, the demand for scalable and automated encryption technologies in BFSI will continue to rise in tandem.

")

The IT & telecom segment is anticipated to register the highest CAGR during the forecast period. Rapid digital transformation and the rise of 5G technology further accelerate the need for cloud encryption in this sector. The rollout of 5G networks has led to a significant increase in data traffic and a broader range of connected devices, introducing more vulnerabilities to data breaches. To manage and protect this expanding digital ecosystem, telecom operators are turning to advanced encryption solutions that can scale alongside their networks and support real-time, secure data exchange. The need to protect edge computing architectures and virtualized network functions has also made cloud-native encryption tools indispensable.

Regional Insights

North America held the major share of over 37.0% of the cloud encryption industry in 2024. The increasing number of cyber threats targeting North American businesses has also significantly contributed to the growth of the market. High-profile ransomware attacks, data leaks, and state-sponsored cyber espionage incidents have made organizations more aware of their cybersecurity posture. Encryption is being recognized as a foundational element of data security frameworks, a last line of defense that renders data unusable even if systems are breached. This awareness is driving demand across sectors such as finance, healthcare, retail, and government.

U.S. Cloud Encryption Market Trends

The U.S. cloud encryption market is projected to grow from 2025 to 2030. The increasing use of emerging technologies such as IoT, artificial intelligence (AI), and machine learning in the U.S. is further propelling the cloud encryption market. These technologies generate large amounts of data that are often stored in the cloud, creating a growing need for security measures to protect that data. For example, AI and machine learning models require vast amounts of data for training, much of which is sensitive or proprietary. Cloud encryption provides the necessary security framework to ensure that data is protected during transmission, storage, and processing in the cloud, allowing U.S. organizations to leverage these technologies while maintaining compliance and safeguarding sensitive information.

Europe Cloud Encryption Market Trends

The cloud encryption market in Europe is expected to grow during the forecast period. The widespread adoption of multi-cloud and hybrid cloud strategies is another significant factor driving the cloud encryption market in Europe. As organizations adopt more complex cloud architectures to meet their specific business needs, the demand for encryption solutions that can protect data across various cloud environments is growing. This includes not only public cloud providers like AWS, Microsoft Azure, and Google Cloud but also private and hybrid clouds, which require encryption capabilities to ensure that data is secure regardless of where it is stored or processed. With these complex, distributed cloud environments, the need for flexible, scalable encryption solutions is becoming more pronounced, driving market growth.

The cloud encryption market in the Germany is grow during the forecast period. The expansion of e-commerce and digital services in Germany has also played a pivotal role in driving the growth of the cloud encryption market. As more businesses move to online platforms, they collect and process a large volume of customer data, ranging from personal details to payment information. The surge in e-commerce transactions, especially during the COVID-19 pandemic, has heightened concerns about the security of customer data. Cloud encryption provides an essential layer of protection for e-commerce platforms, ensuring that sensitive information is safeguarded during transactions and securely stored in the cloud. This growing need for secure, encrypted cloud environments to support the e-commerce boom is a major driver of the cloud encryption market in Germany.

Asia Pacific Cloud Encryption Market Trends

The demand for cloud encryption in the Asia Pacific is expected to register the highest CAGR of 32.2% from 2025 to 2030. The surge in digital payments and e-wallet usage across APAC is another critical factor driving the cloud encryption market. Digital payment systems, mobile wallets, and online banking platforms are experiencing rapid adoption in countries like China, India, and Southeast Asian nations. As these platforms store and process highly sensitive financial information, such as credit card details and personal identification data, encryption becomes essential to prevent financial fraud, identity theft, and other malicious activities. The growing demand for secure digital payment systems is directly fueling the need for cloud encryption solutions to protect financial transactions and customer data across cloud platforms.

The cloud encryption market in China is projected to grow during the forecast period. China’s growing reliance on cloud computing in sectors such as manufacturing and education is fueling the demand for cloud encryption. As industries in China transition towards smart manufacturing and Industry 4.0, vast amounts of data are generated through IoT devices, sensors, and industrial automation systems. This data, which often includes proprietary information, intellectual property, and operational data, needs to be securely stored and transmitted to ensure its integrity. Similarly, the education sector in China is increasingly adopting cloud-based learning platforms, which store sensitive student data. Cloud encryption is critical in both these sectors to ensure that data remains secure and protected from unauthorized access or tampering.

Key Cloud Encryption Company Insights

Some of the key companies operating in the market IBM Corporation, and Thales Group, among others are some of the leading participants in the cloud encryption market.

-

IBM Corporation is a multinational technology company. With a diverse portfolio encompassing hardware, software, and consulting services, IBM has been a pioneer in the tech industry, contributing significantly to advancements in data processing and enterprise solutions. IBM Cloud offers a comprehensive suite of encryption services designed to safeguard data across hybrid and multi-cloud environments. Central to these components is IBM Cloud Hyper Protect Crypto Services, an as-a-service key management and encryption solution that provides customers with full control over their encryption keys. This service utilizes FIPS 140-2 Level 4 certified hardware security modules (HSMs) to ensure the highest level of security for sensitive data.

-

Thales Group is a global technology company that specializes in digital and "deep tech" innovations, including big data, artificial intelligence, connectivity, cybersecurity, and quantum technology. Thales offers a comprehensive suite of cloud encryption solutions designed to protect sensitive data across various cloud environments. These solutions enable organizations to apply data protection where needed, ensuring compliance and safeguarding data as it is used, transferred, or stored in the cloud. Thales's cloud encryption components are integrated with robust key management systems, providing centralized control over encryption keys and policies.

HyTrust Inc., and Trend Micro Inc., Inc are some of the emerging market participants in the cloud encryption industry.

-

HyTrust Inc. is a cybersecurity company specializing in data protection and compliance solutions for virtualized and multi-cloud environments. The company developed software solutions designed to secure data across hybrid infrastructures, focusing on encryption, key management, and security policy enforcement. HyTrust's flagship product, HyTrust DataControl, provides comprehensive encryption and key management solutions for virtual machines (VMs) and cloud workloads. The platform offered granular encryption, securing data from creation to decommissioning, and supported both Windows and Linux environments.

-

Trend Micro Inc. is a global cybersecurity company. The company specializes in developing security software for servers, containers, cloud computing environments, networks, and endpoints. Trend Micro provides comprehensive solutions designed to secure data across hybrid and multi-cloud environments. Their components include the Trend Cloud One platform, which delivers a unified suite of security services encompassing workload security, container security, file storage security, and network security. This platform ensures that data is encrypted both at rest and in transit, adhering to industry standards and best practices to protect sensitive information.

Key Cloud Encryption Companies:

The following are the leading companies in the cloud encryption market. These companies collectively hold the largest market share and dictate industry trends.

- IBM Corporation

- Thales Group

- Google LLC

- Broadcom Inc.

- Cisco Systems Inc.

- Trend Micro Inc.

- Palo Alto Networks

- Check Point Software Technologies

- Fortinet Inc.

- Wiz

- CipherCloud Inc.

- HyTrust Inc.

- Netskope Inc.

- Amaryllo

Recent Developments

-

In February 2025, Google LLC launched quantum-safe digital signatures in its Cloud Key Management Service (Cloud KMS). The Cloud KMS post-quantum cryptography (PQC) roadmap includes plans to support NIST’s post-quantum cryptography standards across both software and hardware. This advancement enables customers to securely perform quantum-resistant key import and exchange, encryption and decryption, as well as digital signature creation.

-

In September 2023, Amaryllo launched its groundbreaking Encryption App featuring Private Cloud Storage. This launch represents a major advancement in digital security, establishing a new industry standard for protecting sensitive information and elevating user privacy. The state-of-the-art app allows users to securely and effortlessly share encrypted files, supported by advanced user verification directly from their mobile devices.

-

In June 2023, Thales Group launched the CipherTrust Data Security Platform, available through a cloud-based, subscription-as-a-service model. This platform helps customers minimize the impact of external threats and streamline operations by simplifying data security across both on-premises and cloud environments. Through the use of CCKM, a multi-cloud encryption key management solution, customers can centralize key lifecycle management while transitioning sensitive data to the cloud.

Cloud Encryption Market Report Scope

Report Attribute

Details

Market size in 2024

USD 4.4 billion

Estimated market size in 2026

USD 7.3 billion

Projected market size by 2030

USD 21.2 billion

Growth rate

CAGR of 30.2% from 2025 to 2030

Actual data

2018 - 2024

Forecast period

2025 - 2030

Quantitative units

Revenue in USD billion and CAGR from 2025 to 2030

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, service model, enterprise size, application, industry vertical, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

IBM Corporation; Thales Group; Google LLC; Broadcom Inc.; Cisco Systems Inc.; Trend Micro

Inc.; Palo Alto Networks; Check Point Software

Technologies; Fortinet Inc.; Wiz; CipherCloud Inc.; HyTrust Inc.; Netskope Inc.; Amaryllo

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cloud Encryption Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global cloud encryption market report based on component, service model, enterprise size, application, industry vertical, and region:

-

Component Outlook (Revenue, USD Billion, 2018 - 2030)

-

Solution

-

Services

-

Professional Services

-

Managed Services

-

-

-

Service Model Outlook (Revenue, USD Billion, 2018 - 2030)

-

Infrastructure-as-a-Service

-

Software-as-a-Service

-

Platform-as-a-Service

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2018 - 2030)

-

Large Enterprises

-

Small and Medium Enterprises (SMEs)

-

-

Application Outlook (Revenue, USD Billion, 2018 - 2030)

-

Data Encryption

-

Database Encryption

-

File Encryption

-

Application Encryption

-

-

Industry Vertical Outlook (Revenue, USD Billion, 2018 - 2030)

-

Retail

-

Healthcare

-

IT & Telecom

-

BFSI

-

Aerospace & Defense

-

Government & Public Utilities

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global cloud encryption market size was valued at USD 4.4 billion in 2024 and is estimated at USD 7.3 billion for 2026.

The global cloud encryption market is expected to grow at a CAGR of 30.2% from 2025 to 2030, reaching USD 21.2 billion by 2030.

The software-as-a-service segment dominated the market and accounted for a revenue share of over 37.0% in 2024 in the cloud encryption market. The rise in cyber threats targeting SaaS platforms has spurred demand for cloud encryption in this segment

Some key players operating in the market include Salesforce Inc., SAP SE, Appian Corporation Inc., Dell Technologies, IBM Corporation, Blue Yonder Group, Inc., Verint Systems Inc., Thomas Bravo, Open Text Corporation, Pegasystems Inc.

Factors such growing trend of remote and hybrid work models and the rise of 5G and edge computing are anticipated to accelerate the market growth.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.