- Home

- »

- Next Generation Technologies

- »

-

Cloud Professional Services Market Size Report, 2026-2033GVR Report cover

![Cloud Professional Services Market (2026 - 2033)Report]()

Cloud Professional Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service Type, By Service Model (SaaS, IaaS, PaaS), By Deployment, By Enterprise Size, By End-use, By Region, And Segment Forecasts

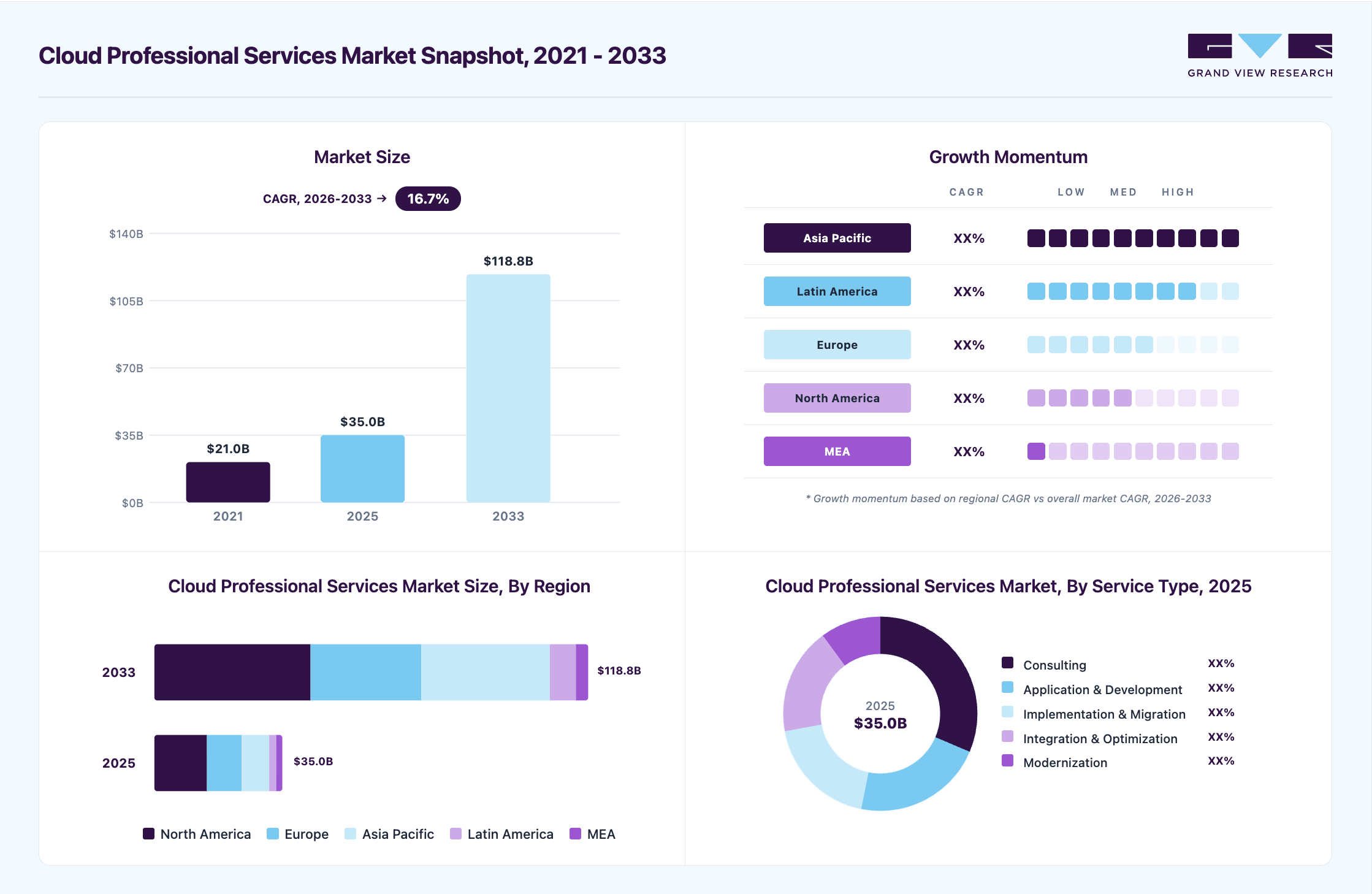

Market Size, 2025

$35.0BMarket Estimate, 2026

$40.2BMarket Forecast, 2033

$118.8BCAGR, 2026–2033

16.7%Cloud Professional Services Market Summary

The global cloud professional services market size was valued at USD 35.0 billion in 2025 and is projected to grow from USD 40.2 billion in 2026 to USD 118.8 billion by 2033, at a CAGR of 16.7% from 2026 to 2033. The market in North America dominated with a revenue share of 41.0% in 2025. The surge in digital transformation across industries is a key driver propelling demand for cloud professional services.

Key Market Trends & Insights

- By service type: The consulting segment accounted for the largest revenue share of 31.4% in 2025.

- By service model: The SaaS segment accounted for the largest share in 2025.

- By deployment: The public segment accounted for the largest share in 2025.

Regional Highlights

- Largest regional market: North America (41.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 35.0 Billion

- Estimated market size in 2026: USD 40.2 Billion

- Projected market size by 2033: USD 118.8 Billion

- CAGR (2026-2033): 16.7%

Organizations increasingly adopt cloud-first strategies to modernize legacy systems, enhance agility, and improve customer experiences. Cloud professional services, including consulting, migration, implementation, and managed services, ensure a seamless transition to cloud platforms. Businesses seek expert partners to guide them through the complexity of hybrid and multi-cloud environments, regulatory compliance, and data sovereignty challenges. According to the Flexera 2025 State of the Cloud Report, 86% of organizations use a multi-cloud strategy, with 70% adopting hybrid cloud, 14% multiple public clouds, and 2% multiple private clouds. Only 12% rely on a single public cloud, and 2% on a single private cloud, highlighting the growing preference for multi-cloud environments.")

Rapid advancements in technologies such as artificial intelligence (AI), machine learning (ML), big data analytics, and the Internet of Things (IoT) are encouraging enterprises to migrate workloads to the cloud. Cloud professional service providers help design and implement scalable cloud infrastructures that support these technologies. Integrating AI and automation into cloud services also increases operational efficiency and reduces manual intervention, creating new opportunities for professional services to optimize and maintain these intelligent systems.

Many organizations are adopting hybrid and multi-cloud environments to avoid vendor lock-in, increase flexibility, and optimize cost-performance ratios. These complex architectures require professional services for cloud orchestration, workload placement, integration, and monitoring. Cloud professionals help companies manage inter-cloud dependencies and ensure smooth interoperability between private and public clouds, making their role increasingly indispensable.

Market Dynamics

The rapid growth of generative AI, machine learning, advanced analytics, and high-performance computing is significantly increasing demand for cloud professional services. Organizations are modernizing their cloud environments to support compute-intensive AI workloads that require scalable infrastructure, high-speed networking, and GPU-accelerated processing. As enterprises deploy AI applications across functions such as customer service, cybersecurity, predictive maintenance, and business intelligence, they increasingly rely on service providers for cloud architecture design, workload migration, AI model deployment, data engineering, and performance optimization. Additionally, professional service firms help organizations build cloud-native environments capable of managing large data volumes, ensuring operational scalability, improving resource utilization, and enabling secure, efficient, and cost-effective AI infrastructure management across hybrid and multi-cloud ecosystems.

Players operating in the market are strengthening their cloud services to handle intensive AI workloads. For instance, In March 2026, Accenture expanded its partnership with Google Cloud to strengthen cloud security services, integrating AI-driven cybersecurity and unified operations. This collaboration enhances proactive threat detection, supports secure cloud adoption, and reinforces enterprise resilience across multi-cloud environments.

Large-scale cloud migration and digital transformation initiatives often involve significant upfront investments, which can limit adoption among cost-sensitive organizations. Enterprises must allocate substantial budgets for cloud consulting, application modernization, infrastructure redesign, cybersecurity implementation, employee training, and integration with existing legacy systems. Additional expenses related to data migration, compliance management, workload testing, and operational downtime further increase overall project costs. Small and medium-sized businesses, in particular, may face financial challenges in justifying the return on investment during the early stages of cloud transformation. Moreover, complex multi-cloud and hybrid cloud deployments require continuous optimization and specialized expertise, increasing long-term operational expenses. These financial barriers can delay cloud adoption and reduce demand for professional cloud transformation services.

Market Concentration & Characteristics

The cloud professional services market is moderately concentrated, with large multinational players maintaining significant market share due to their extensive global delivery capabilities, deep partnerships with major cloud providers, broad service portfolios, and long-standing enterprise relationships. These companies typically offer end-to-end cloud transformation services, including cloud consulting, migration, application modernization, DevOps, cybersecurity, data engineering, FinOps, and managed cloud operations. High entry barriers exist because enterprises increasingly demand multi-cloud expertise, industry-specific compliance capabilities, certified cloud talent, and the ability to manage large-scale, mission-critical transformation programs across complex hybrid IT environments.

In terms of market characteristics, the industry is highly technology-driven and continuously evolving, with a strong focus on artificial intelligence, automation, cloud-native architectures, cybersecurity, and platform engineering. Demand is primarily driven by enterprise digital transformation initiatives, AI adoption, migration from legacy infrastructure, and increasing adoption of hybrid and multi-cloud environments. Organizations are also prioritizing cloud cost optimization, operational resilience, and regulatory compliance, further increasing reliance on specialized professional services providers. Additionally, the market is characterized by long-term strategic engagements, recurring managed service contracts, and strong vendor stickiness due to the complexity of cloud ecosystems, integration dependencies, and operational continuity requirements. Strategic alliances with hyperscalers such as Amazon Web Services, Microsoft, and Google also play a critical role in shaping competition, partner ecosystems, and customer acquisition strategies within the market.

Service Type Insights

The consulting segment dominated the cloud professional services market, accounting for a 31.4% revenue share in 2025, driven by the increasing complexity of cloud adoption strategies, as organizations seek expert guidance to navigate multi-cloud and hybrid environments, ensure compliance with evolving regulations, and optimize cost structures. Businesses leverage consulting services to align cloud migration with digital transformation objectives, integrate advanced technologies such as AI, IoT, and analytics into cloud ecosystems, and modernize legacy systems without disrupting operations. Moreover, the rapid pace of cloud innovation, coupled with industry-specific customization needs, is fueling demand for consultants who can provide tailored roadmaps, risk mitigation strategies, and change management support to accelerate time-to-value and enhance competitive advantage.

The service model and development segment is anticipated to grow at the highest CAGR during the forecast period due to the rising need for cloud-native service model creation, modernization, and integration that can scale seamlessly to meet dynamic business demands. Organizations increasingly turn to cloud platforms to build microservices-based architectures, leverage containerization, and implement serverless computing for faster deployment cycles and improved performance. The demand for API-driven ecosystems, low-code/no-code development tools, and DevOps-enabled workflows is also accelerating, enabling faster innovation while reducing operational bottlenecks.

Service Model Insights

The SaaS segment dominated the market and accounted for the largest revenue share in 2025, driven by the increasing preference for subscription-based software delivery that reduces upfront capital expenditure and simplifies IT management. Organizations are adopting SaaS to quickly access industry-specific service models, ensure automatic updates with minimal downtime, and benefit from built-in scalability that supports fluctuating workloads. The growing need for secure, globally accessible collaboration tools to support remote and hybrid workforces is also driving adoption, alongside the integration of advanced features such as embedded analytics, AI-driven insights, and compliance-ready frameworks.

The PaaS is expected to grow significantly during the forecast period as businesses increasingly seek agile platforms that streamline the entire service model lifecycle, from coding to deployment, without the burden of managing underlying infrastructure. Rising demand for real-time data processing, advanced analytics, and AI/ML model deployment pushes organizations toward PaaS solutions offering integrated development environments, managed databases, and seamless scalability. The segment is further propelled by the growing need to support multi-cloud interoperability, facilitate continuous integration and continuous delivery (CI/CD) pipelines, and enable faster prototyping of innovative products.

Deployment Insights

The public segment dominated the market and accounted for the largest revenue share in 2025 due to its cost-efficiency, flexibility, and ease of provisioning, which make it particularly attractive for startups, SMEs, and enterprises seeking rapid scalability without large infrastructure investments. The ability to instantly access a vast range of computing resources on demand and global availability through distributed data centers supports faster market expansion and disaster recovery readiness. Public cloud environments also drive adoption through their robust partner ecosystems, offering pre-integrated services and third-party service models that accelerate innovation.

Hybrid is expected to grow at a significant CAGR during the forecast period as organizations seek to balance the control and customization of private infrastructure with the scalability and innovation of public cloud environments. This model is favored for enabling seamless data and workload portability, allowing businesses to optimize performance by running mission-critical service models public while leveraging cloud resources for burst capacity or specialized workloads. The growth is further fueled by the need to support edge computing initiatives, enable unified management across diverse environments, and accommodate complex governance or sovereignty requirements without compromising agility.

Enterprise Size Insights

The large enterprise segment dominated the market and accounted for the largest revenue share in 2025 as multinational corporations increasingly require sophisticated, enterprise-grade cloud solutions to manage vast and complex IT ecosystems. These organizations leverage cloud professional services to orchestrate global operations, integrate disparate business units, and implement advanced governance frameworks that ensure consistent performance across multiple regions. Rising demand for high-availability architectures, advanced cybersecurity frameworks, and compliance with diverse international regulations is also driving adoption.

The SMEs segment is expected to grow at a significant CAGR during the forecast period as smaller businesses increasingly turn to cloud solutions to compete with larger players by leveraging enterprise-grade capabilities without the associated infrastructure burden. Many SMEs adopt cloud professional services to streamline IT operations, improve speed-to-market, and access advanced digital tools that would otherwise be cost-prohibitive. The availability of tailored service packages, pay-as-you-go pricing models, and industry-specific cloud solutions lowers entry barriers and encourages adoption.

End Use Insights

The BSFI segment dominated the market and accounted for the largest revenue share in 2025 as financial institutions increasingly adopt cloud solutions to power real-time transaction processing, enhance digital banking experiences, and enable advanced fraud detection through AI-driven analytics. The sector is leveraging cloud platforms to support open banking initiatives, integrate fintech partnerships, and deliver personalized financial services at scale. Moreover, the need for high-speed data processing to comply with evolving risk management and reporting standards drives adoption and the ability to rapidly launch new digital products while maintaining stringent security and encryption protocols to safeguard sensitive customer data.

The healthcare segment is expected to grow significantly over the forecast period as healthcare providers and life sciences organizations increasingly adopt cloud solutions to support telemedicine platforms, enable remote patient monitoring, and streamline collaboration across care teams. The growing use of cloud-based systems to integrate electronic health records (EHR) from multiple sources improves interoperability and clinical decision-making. In addition, the sector is leveraging cloud infrastructure to accelerate medical research through high-performance computing, support AI-driven diagnostics, and facilitate large-scale genomic data analysis. The ability to securely share data across stakeholders while meeting stringent healthcare compliance requirements further propels adoption.

Regional Insights

North America dominated the global cloud professional services market with the largest revenue share of 41.0% in 2025, driven by cloud adoption maturity, advanced enterprise IT infrastructures, and a strong ecosystem of hyperscale cloud providers such as AWS, Microsoft Azure, and Google Cloud. There's an increasing demand for migration and integration services as large enterprises modernize their operations and unify public systems with SaaS platforms. In addition, the region is witnessing growing investments in multi-cloud and hybrid cloud strategies, enabling organizations to enhance flexibility, scalability, and resilience. The presence of leading consulting and IT service firms further accelerates innovation and adoption of advanced cloud solutions across industries.

U.S. Cloud Professional Services Market Trends

The cloud professional services market in the U.S. is expected to grow significantly during the forecast period from 2026 to 2033, due to the surge in federal government cloud modernization projects and growing investments in digital public infrastructure. The financial services, life sciences, and healthcare industries heavily invest in cloud-based solutions that require strict compliance and high availability, driving a surge in demand for domain-specific consulting, cloud governance, and managed services.

Asia Pacific Cloud Professional Services Market Trends

Asia Pacific held a significant share in the global market in 2025, due to rapid digitalization among emerging economies, government-led smart city projects, and rising demand from cloud-first startups. Diverse regulatory landscapes across countries push businesses to invest in cloud services that offer scalable compliance solutions. Furthermore, increasing adoption of AI, big data analytics, and IoT across industries is driving demand for advanced cloud professional services in the region. The expansion of local data centers by global and regional cloud providers is also enhancing service accessibility, performance, and data sovereignty compliance.

The cloud professional services market in China held a substantial market share in 2025, due to the rise of homegrown cloud providers and government initiatives such as New Infrastructure that promote digital upgrades across transportation, education, and health. Cloud professional services are essential in helping businesses localize service models, navigate strict cybersecurity laws, and integrate with China's unique digital ecosystem. Furthermore, the dominance of domestic cloud platforms and restrictions on foreign technology providers are driving demand for locally tailored consulting, migration, and managed services. Increasing investments in AI, 5G, and industrial internet initiatives are also accelerating the need for scalable and high-performance cloud architectures across key sectors.

Japan cloud professional services market is expected to grow rapidly in the coming years, driven by the acceleration of cloud adoption in manufacturing, banking, and public services, especially in response to an aging workforce. Cloud professional services are helping enterprises build low-maintenance, AI-ready infrastructures that support robotic process automation (RPA), smart supply chains, and digital citizen services. In addition, strong government initiatives such as the “Society 5.0” vision and digital transformation policies are encouraging enterprises to modernize legacy systems through cloud integration. The growing presence of domestic IT leaders and partnerships with global cloud providers is further accelerating localized, secure, and compliance-driven cloud deployments.

Europe Cloud Professional Services Market Trends

The cloud professional services market in Europe is anticipated to register considerable growth from 2026 to 2033 due to increasing focus on sovereign cloud strategies and GDPR-aligned cloud compliance. As companies navigate fragmented data regulations across EU countries, cloud professional services are being used to implement governance frameworks, regional data centers, and audit trails.

The UK cloud professional services market is expected to grow rapidly in the coming years. Financial institutions and public sector agencies are investing in cloud professional services to align with FCA, NHS, and ICO guidelines. Moreover, the growing fintech and healthtech ecosystem demands customized multi-cloud strategies to support rapid innovation and user-centric design. In addition, organizations are prioritizing data residency and sovereignty requirements following evolving regulatory frameworks, driving demand for secure and compliant cloud architectures. The increasing adoption of AI-driven analytics and open banking initiatives is further fueling the need for advanced cloud consulting, integration, and managed services across the UK.

The cloud professional services market in Germany held a substantial market share in 2025 due to the rise of Industry 4.0 initiatives, which emphasize cloud-based automation, smart manufacturing, and predictive analytics. German enterprises, especially in automotive and industrial sectors, leverage cloud professional services to enable secure connectivity between machines, systems, and sensors across global production lines. In addition, stringent local data protection laws are creating demand for cloud consultants with regional legal expertise.

Key Cloud Professional Services Company Insights

Some of the key companies operating in the market, include Accenture, Amazon Web Services, Inc., Atos SE, Capgemini, Cognizant, Fujitsu, Google Cloud, among others are some of the leading participants in the cloud professional services market.

-

In March 2026, Accenture expanded its partnership with Google Cloud to strengthen cloud security services, integrating AI-driven cybersecurity and unified operations. This collaboration enhances proactive threat detection, supports secure cloud adoption, and reinforces enterprise resilience across multi-cloud environments.

-

In June 2025, Atos SE announced the completion of a data center migration project for IGM Financial Inc., a Canada-based wealth and asset management firm. The transformation involved migrating IGM’s assets to a modern, cloud-native infrastructure built on Microsoft Azure and Google Cloud Platform (GCP). The new environment enhances operational efficiency, speed, and scalability. Leveraging Atos’ expertise in agile, scalable architecture, the solution strengthens risk mitigation and improves reporting and issue remediation visibility.

-

In November 2024, Accenture acquired Award Solutions, a U.S.-based firm specializing in training and consulting for advanced wireless and network technologies such as 5G, the Internet of Things (IoT), and cloud-based solutions. This acquisition strengthens Accenture’s capabilities in next-generation connectivity and enhances its ability to support clients in adopting and scaling emerging technologies across industries.

Key Cloud Professional Services Companies:

The following key companies have been profiled for this study on the cloud professional services market.

- Accenture

- Amazon Web Services, Inc.

- Atos SE

- Capgemini

- Cognizant

- Fujitsu

- Google Cloud

- HCL Technologies Limited

- IBM Corporation

- Infosys Limited

- Microsoft Corporation

- NTT DATA

- Oracle

- SAP SE

- TATA Consultancy Services Limited

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Accenture; IBM; Capgemini; Infosys; Tata Consultancy Services; Cognizant; Wipro

- Building end-to-end cloud transformation ecosystems integrating consulting, migration, cybersecurity, AI, FinOps, and managed services under unified delivery platforms.

- Expanding strategic partnerships with hyperscalers such as Amazon Web Services, Microsoft, and Google to strengthen multi-cloud implementation capabilities.

- Leveraging global delivery centers and offshore talent models to scale enterprise cloud modernization projects cost-effectively across regions and verticals.

- Long-standing enterprise relationships and deep integration into mission-critical IT environments create high customer retention and strong recurring revenue streams.

- Extensive certified cloud talent pools, global delivery infrastructure, and broad industry expertise enable execution of large-scale, multi-region transformation programs.

- Ability to provide end-to-end transformation services from consulting and migration to managed cloud operations and AI deployment.

- Large organizational structures can slow innovation cycles and reduce agility in rapidly evolving cloud-native and generative AI markets.

- High service costs and complex engagement models may limit adoption among SMEs and mid-market enterprises.

- Integration complexity across acquired platforms and consulting practices can sometimes create inconsistent customer experiences and delivery inefficiencies.

Emerging Players: Rackspace Technology; AHEAD; Slalom; Nordcloud; Caylent

- Focusing on cloud-native, API-driven, and AI-enabled service models designed specifically for agile digital transformation initiatives.

- Delivering lightweight, faster deployment frameworks and industry-specific accelerators that reduce migration timelines and operational complexity.

- Building flexible consumption-based and outcome-driven pricing models to attract mid-market and digital-native enterprises.

- Greater agility and faster deployment of modern cloud-native solutions compared to larger traditional consulting firms.

- Modern delivery methodologies and highly automated implementation frameworks improve customer experience and deployment speed.

- Ability to rapidly adapt service offerings around emerging technologies such as generative AI, MLOps, and platform engineering.

- Limited global delivery scale and smaller consulting workforces can restrict ability to execute large multi-country enterprise transformation programs.

- Lower brand recognition and fewer long-term enterprise relationships compared to established global consulting firms.

- Heavy reliance on hyperscaler partnerships may create dependency risks and narrower service diversification.

- Smaller firms may face profitability and scalability challenges while competing against large vendors with bundled end-to-end enterprise service portfolios.

Cloud Professional Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 35.0 billion

Estimated market size in 2026

USD 40.2 billion

Projected market size by 2033

USD 118.8 billion

Growth rate

CAGR of 16.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Service type, service model, deployment, enterprise size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Accenture; Amazon Web Services, Inc.; Atos SE; Capgemini; Cognizant; Fujitsu; Google Cloud; HCL Technologies Limited; IBM Corporation; Infosys Limited; Microsoft Corporation; NTT DATA; Oracle; SAP SE; TATA Consultancy Services Limited

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cloud Professional Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the cloud professional services market report based on service type, service model, deployment, enterprise size, end use, and region:

-

Service Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Consulting

-

Application & Development

-

Integration & Optimization

-

Implementation & Migration

-

Modernization

-

-

Service Model Outlook (Revenue, USD Billion, 2021 - 2033)

-

SaaS

-

IaaS

-

PaaS

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Public

-

Private

-

Hybrid

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Small & Medium Enterprises

-

Large Enterprise

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT & Telecom

-

Government

-

Healthcare

-

Manufacturing

-

Retail & E-commerce

-

Energy & Utility

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cloud professional services opportunity assessment for a digital transformation and IT consulting provider

- Assessment of cloud professional services demand across major regions and industries

- Analysis of enterprise adoption trends for cloud migration, application modernization, DevOps, FinOps, cybersecurity, and managed cloud services

- Benchmarking of major cloud service providers, consulting firms, hyperscaler partnerships, and delivery capabilities

- Identified high-growth cloud service segments and regional opportunities

- Supported service portfolio positioning and expansion strategy

- Highlighted key enterprise adoption drivers, operational challenges, and regulatory trends

Customized cross-segmentation analysis for cloud professional services by service type and enterprise size

- Conducted cross-segmentation analysis of cloud professional services by service type and organization size

- Assessed adoption differences across BFSI, healthcare, retail, manufacturing, and public sector verticals

- Identified high-adoption cloud service categories driving enterprise transformation

- Highlighted enterprise segments with the strongest cloud spending potential

- Supported strategic understanding of cloud maturity and service penetration across industries

Cloud transformation and market entry assessment for a managed cloud services provider

- Analysis of regional cloud spending trends across the MEA region

- Evaluation of enterprise requirements for hybrid cloud, multi-cloud management, cybersecurity, AI-ready infrastructure, and regulatory compliance

- Assessment of channel partnerships, delivery models, and competitive intensity across target regions

- Identified attractive regional market expansion opportunities

- Supported GTM, alliance, and partner ecosystem strategy

- Enabled strategic expansion into high-growth cloud transformation and managed services markets

Frequently Asked Questions About This Report

The SaaS held the largest revenue share in 2025.

The public held the largest share in 2025.

North America dominated with a 41.0% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Factors such as a surge in digital transformation across industries and increasing adoption of cloud-first strategies to modernize legacy systems, enhance agility, and improve customer experiences are driving the growth of the cloud professional services market.

The global cloud professional services market size was estimated at USD 35.4 billion in 2025 and is expected to reach USD 40.1 billion in 2026.

The global cloud professional services market is expected to grow at a compound annual growth rate of 16.7% from 2026 to 2033 to reach USD 118.8 billion by 2033.

The consulting segment accounted for the largest revenue share of 31.4% in 2025.

Key players include Accenture; Amazon Web Services, Inc.; Atos SE; Capgemini; Cognizant; Fujitsu; Google Cloud; HCL Technologies Limited; IBM Corporation; Infosys Limited; Microsoft Corporation; NTT DATA; Oracle; SAP SE; TATA Consultancy Services Limited, and others.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.