- Home

- »

- Communications Infrastructure

- »

-

Data Center Switch Market Size & Share Report, 2026-2033GVR Report cover

![Data Center Switch Market Size, Share, & Trends Report]()

Data Center Switch Market (2026 - 2033) Size, Share, & Trends Analysis By Type (Core Switches, Distribution Switches, Access Switches), By Technology (Ethernet, InfiniBand, Fiber Channel), By Port Speed, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$15.0BMarket Estimate, 2026

$16.3BMarket Forecast, 2033

$34.2BCAGR, 2026–2033

11.1%Data Center Switch Market Summary

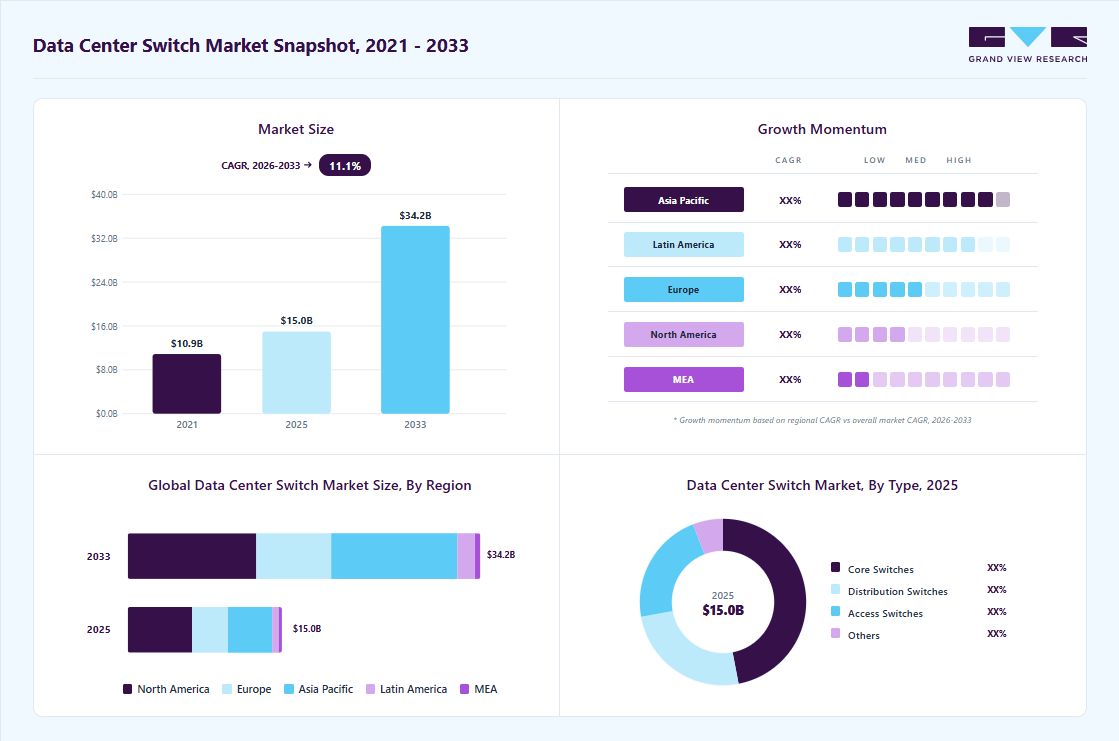

The global data center switch market size was valued at USD 15.0 billion in 2025 and is projected to grow from USD 16.3 billion in 2026 to USD 34.2 billion by 2033, at a CAGR of 11.1% from 2026 to 2033. North America dominated the industry with the largest revenue share of 41.7% in 2025. Due to hyperscale infrastructure expansion, architectural transformation within data centers, and exponential growth in data-intensive workloads. The rapid expansion of hyperscale and colocation data centers led by cloud service providers (CSPs) such as AWS, Microsoft Azure, Google Cloud, and Alibaba Cloud is driving the growth of the market.

Key Market Trends & Insights

- By type: Core switches dominated the market, with a revenue share of 47.0% in 2025.

- By technology: Ethernet segment held the largest market share of 85.8% in 2025.

- By port speed: The >40G to 100 GBPS segment led the market with the largest revenue share of 36.7% in 2025.

- By end-use: Cloud service providers led the market with the largest revenue share of 41.2% in 2025.

Regional Highlights

- Largest regional market: North America (41.7% in 2025 revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The data center switch market in the U.S. accounted for the largest market revenue share in North America in 2025.

Market Size & Forecast

- Market size in 2025: USD 15.0 Billion

- Estimated market size in 2026: USD 16.3 Billion

- Projected market size by 2033: USD 34.2 Billion

- CAGR (2026-2033): 11.1%

For instance, in April 2025, Emirates Integrated Telecommunications Company, UAE, entered into a hyperscale data center agreement with Microsoft to develop and operate a hyperscale facility with an estimated investment of approximately USD 544.54 million, with Microsoft serving as the anchor tenant. The data center’s capacity will be rolled out in phased tranches to align with demand requirements.")

These operators are scaling multi-region, multi-availability-zone deployments, which significantly increases demand for high-density, low-latency switching solutions, particularly spine-leaf architectures and 100G/200G/400G Ethernet switches. Hyperscale operators require high port density, energy-efficient designs, and support for open networking to reduce total cost of ownership (TCO), thereby accelerating switch upgrades and refresh cycles.

Moreover, the surge in AI/ML workloads and high-performance computing (HPC) deployments also contributes to the growth in the data center switch industry. Training large language models (LLMs) and running AI inference workloads require ultra-low latency, high-bandwidth, and lossless networking. This is driving the adoption of high-speed Ethernet and advanced switching technologies, including RDMA over Converged Ethernet (RoCE), enhanced buffer management, and telemetry-based congestion control. AI-driven infrastructure is significantly increasing east-west traffic inside data centers, reinforcing the need for high-capacity spine switches.

The growth of edge computing and distributed cloud architecture is also contributing to market expansion. As enterprises deploy micro data centers closer to end users to reduce application latency for IoT, autonomous systems, and real-time analytics, demand for compact, power-efficient data center switches with advanced automation capabilities rises. This shift toward decentralized architectures increases the total number of network nodes requiring switching infrastructure. According to Eurostat, 52.74% of EU enterprises used paid cloud services in 2025, while 40.89% adopted at least one advanced cloud solution, indicating they are highly cloud-dependent. The highest levels of cloud dependency were recorded in Finland (65.90%), Denmark (64.98%), the Netherlands (62.00%), and Italy (61.90%), reflecting strong enterprise-level integration of sophisticated cloud technologies in these countries.

Market Dynamics

The rapid commercialization of AI factories, large language model (LLM) training clusters, and GPU-intensive computing environments is significantly driving demand for advanced data center switches. Enterprises and hyperscale cloud providers are increasingly deploying large-scale AI clusters that require ultra-low-latency, high-bandwidth interconnects capable of supporting massive east-west traffic between GPUs, CPUs, and storage systems. As AI workloads continue to scale across training, inference, and agentic AI applications, networking infrastructure is becoming a critical performance bottleneck, thereby increasing the adoption of high-capacity Ethernet and InfiniBand switching solutions.

In addition, several networking and semiconductor vendors are introducing AI-optimized switching platforms to improve AI cluster efficiency and network scalability. For instance, in February 2026, Cisco introduced its Silicon One G300 AI networking chip and next-generation Nexus switching systems designed for AI-scale data centers. The platform delivers 102.4 Tbps switching capacity, supports liquid-cooled networking infrastructure, and improves energy efficiency for hyperscale AI deployments.

The data center switch market faces significant challenges, including high infrastructure deployment costs, complex network integration requirements, and operational challenges associated with upgrading large-scale data center environments. Deploying advanced high-speed switching infrastructure often requires substantial capital investment in Ethernet switches, optical transceivers, high-performance cabling systems, network management software, and AI-optimized networking architectures. For many enterprises and small- to medium-sized data center operators, the high upfront costs associated with migrating from legacy networking environments to 100G, 200G, 400G, and emerging 800G switching infrastructures may limit adoption.

Market Concentration & Characteristics

The data center switch market is moderately concentrated, with the presence of large networking equipment providers, cloud infrastructure vendors, semiconductor companies, and specialized data center networking solution providers alongside emerging software-defined networking (SDN) and AI-driven infrastructure companies. Leading companies maintain strong market positions through extensive switching portfolios, high-performance Ethernet solutions, strategic partnerships with hyperscale cloud providers and colocation operators, advanced silicon architectures, and integrated network management capabilities. These players offer comprehensive solutions, including Ethernet switches, InfiniBand switches, spine-leaf architectures, top-of-rack (ToR) switches, modular core switches, AI fabric networking solutions, network operating systems, and automated network orchestration platforms, creating competitive advantages through ultra-low latency, high bandwidth capacity, scalability, energy efficiency, and operational reliability. High barriers to entry arise from the need for advanced semiconductor and networking expertise, significant investment in R&D and ASIC development, interoperability requirements with complex IT environments, and the technical complexity associated with supporting hyperscale and AI-driven data center infrastructures.

In terms of market characteristics, the industry is highly technology-intensive and characterized by rapid innovation in artificial intelligence (AI) networking, high-speed Ethernet technologies, software-defined networking (SDN), network automation, and cloud-scale data center architectures. The increasing deployment of AI workloads, hyperscale cloud computing infrastructure, edge data centers, and high-performance computing (HPC) environments is a major demand driver. Organizations are rapidly adopting 100G, 200G, 400G, and emerging 800G switching technologies to support bandwidth-intensive applications, GPU clusters, and east-west traffic growth within modern data centers. Moreover, the market is characterized by strong emphasis on low-latency connectivity, network scalability, power efficiency, automation, and seamless integration with cloud and hybrid IT environments. Enterprises and cloud service providers increasingly prioritize intelligent, programmable switching solutions to optimize network performance, reduce operational complexity, support AI and machine learning workloads, improve data throughput, and enhance the efficiency of next-generation digital infrastructure.

Type Insights

The core switches segment led the market with the largest revenue share of 47.0% in 2025, due to the growing need for centralized traffic orchestration, ultra-high backplane capacity, and multi-domain network convergence within large enterprise and carrier-grade data centers. As organizations consolidate IT environments, integrate hybrid multi-cloud frameworks, and interconnect geographically dispersed data centers, core switches act as the backbone layer enabling high-throughput Layer 3 routing, MPLS/VXLAN support, and large-scale route table management.

The access switches segment is anticipated to grow at the fastest CAGR during the forecast period, owing to the increasing need for high-density server connectivity and workload aggregation at the rack level, particularly in enterprise private data centers and hybrid cloud environments. As organizations modernize IT infrastructure, there is a growing deployment of Top-of-Rack (ToR) switches to support virtualization, containerized applications, and hyperconverged infrastructure (HCI), which require efficient server-to-switch connectivity with low oversubscription ratios.

Technology Insights

The ethernet segment accounted for the largest market revenue share of 85.8% in 2025, driven by cost-per-bit efficiency, a broad interoperability ecosystem, and a continuous standardization roadmap that ensures long-term scalability. Unlike alternative interconnect technologies, Ethernet benefits from IEEE-driven standard evolution (25G/50G/100G/400G and beyond), enabling predictable upgrade paths while maintaining backward compatibility, an essential factor for enterprises managing heterogeneous infrastructure.

The infiniband segment is expected to grow at the fastest CAGR during the forecast period, due to the escalating demand for deterministic, ultra-low-latency, high-message-rate performance, and near-linear scalability in tightly coupled compute clusters. Research institutions, national supercomputing facilities, and AI-focused data centers increasingly rely on InfiniBand fabrics for massively parallel processing environments where microsecond-level latency consistency and high throughput are mission-critical.

Port Speed Insights

The >40G to 100 GBPS segment accounted for the largest market revenue share of 36.7% in 2025, owing to the need for balanced performance-to-cost optimization in mid-scale data center deployments and enterprise modernization initiatives. Organizations operating private clouds, financial trading platforms, and latency-sensitive enterprise applications are increasingly standardizing on 100G uplinks and aggregation layers to accommodate growing workload density without transitioning immediately to higher-cost 400G infrastructure.

The >100 GBPS segment is expected to grow at the fastest CAGR during the forecast period, due to the rapid densification of compute and storage resources within next-generation data centers, where rack power exceeding 30-50 kW necessitates ultra-high-capacity network fabrics to prevent bottlenecks. As server platforms increasingly incorporate multi-core CPUs, high-bandwidth memory architectures, and multiple accelerator cards per node, aggregate traffic per rack has surged, compelling operators to deploy 200G, 400G, and emerging 800G switching to maintain oversubscription targets in the fabric.

End Use Insights

The cloud service providers segment accounted for the largest market revenue share of 41.2% in 2025, driven by the aggressive multi-tenant service expansion and the continuous rollout of new cloud-native offerings such as serverless computing, managed Kubernetes, database-as-a-service (DBaaS), and industry-specific cloud platforms. CSPs operate on a consumption-based revenue model, which requires elastic network architectures that dynamically scale bandwidth across compute clusters without service degradation. The increasing monetization of advanced services-such as real-time analytics, edge cloud integration, and sovereign cloud deployments-necessitates resilient, high-availability switching fabrics with advanced traffic engineering and multi-region failover capabilities.

The telecommunication industry segment is expected to grow at the fastest CAGR over the forecast period, owing to the ongoing virtualization of core and transport networks through Network Functions Virtualization (NFV) and cloud-native 5G standalone (SA) deployments. Telecom operators are transforming legacy hardware-based network elements into software-defined, containerized network functions running inside centralized and distributed data centers, which significantly increases internal data traffic and demands carrier-grade switching infrastructure.

Regional Insights

North America dominated the global data center switch market with the largest revenue share of 41.7% in 2025, driven bysustained capital expenditure from hyperscale operators and colocation providers seeking infrastructure resilience and geographic redundancy. The region’s strong venture capital ecosystem and high concentration of digital-native enterprises accelerate the buildout of multi-tenant facilities, particularly in secondary markets to mitigate power and land constraints in Tier I cities.

U.S. Data Center Switch Market Trends

The data center switch market in the U.S. accounted for the largest market revenue share in North America in 2025, driven by large-scale federal and defense-related cloud modernization programs, including secure government cloud frameworks and classified data infrastructure upgrades. High-performance switching adoption is also rising due to the expansion of fintech, healthtech, and autonomous systems ecosystems, which require low-latency, high-availability networking backbones.

Europe Data Center Switch Market Trends

The data center switch market in Europe is anticipated to register at a significant CAGR from 2026 to 2033, driven by stringent data sovereignty regulations and cross-border data localization mandates, compelling enterprises to deploy regionally distributed cloud and colocation facilities. The expansion of green data center initiatives aligned with EU sustainability directives is also accelerating infrastructure refresh cycles, favoring energy-efficient switching technologies

The UK data center switch market is expected to grow at a rapid CAGR during the forecast period, owing to the rapid expansion of fintech startups and digital banking platforms is increasing requirements for agile, high-performance switching infrastructure within colocation and enterprise facilities.

The data center switch market in Germany held a substantial market share in Europe in 2025, due to the strong industrial digitalization under Industry 4.0 initiatives, where manufacturing enterprises are deploying private data centers to support automation, robotics, and real-time analytics. The country’s robust automotive and engineering sectors require high-availability IT infrastructure for simulation and digital twin applications, increasing demand for advanced switching systems.

Asia Pacific Data Center Switch Market Trends

The data center switch market in Asia Pacific is anticipated to grow at the fastest CAGR during the forecast period, driven byrapid urban digitalization, rising internet penetration, and the proliferation of digital payment ecosystems across emerging economies. Governments across the region are investing heavily in smart city infrastructure and national cloud programs, driving localized data center development.

The Japan data center switch market is expected to grow at a rapid CAGR during the forecast period, driven by enterprise IT resilience strategies emphasizing disaster recovery and business continuity, particularly in earthquake-prone regions. Corporations are increasingly adopting distributed data center models to ensure operational redundancy, leading to network modernization initiatives.

The data center switch market in China held a substantial share in Asia Pacific in 2025, due to state-backed initiatives to redistribute computing workloads to inland regions with lower energy costs. Massive investments by domestic cloud giants and telecom operators in greenfield hyperscale campuses are accelerating the deployment of large-scale network equipment.

Key Data Center Switch Company Insight

Key players operating in the data center switch industry are Arista Networks, Cisco Systems, Hewlett Packard Enterprise Development LP, Dell Technologies, Extreme Networks, Juniper Networks. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals.

Key Data Center Switch Companies:

The following key companies have been profiled for this study on the data center switch market

- Arista Networks

- Broadcom

- Cisco Systems

- Cumulus Networks

- Dell Technologies

- Extreme Networks

- Hewlett Packard Enterprise Development LP

- Huawei Technologies

- Infinera

- Juniper Networks

- NEC Corporation

- Netgear, Inc.

- NVIDIA

- Pluribus Networks

- Super Micro Computer, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Arista Networks, Cisco Systems, Hewlett Packard Enterprise Development LP, Dell Technologies, Juniper Networks

- Expanding AI-ready Ethernet switching platforms, software-defined networking (SDN), and cloud-scale data center fabric architectures.

- Investing in high-speed 400G/800G switching technologies, AI networking fabrics, network automation, and intelligent telemetry capabilities.

- Strengthening partnerships with hyperscale cloud providers, semiconductor vendors, telecom operators, and AI infrastructure companies to support next-generation data center deployments.

- Strong global enterprise and hyperscale customer presence with extensive networking infrastructure ecosystems.

- Broad end-to-end portfolios covering Ethernet switches, AI networking fabrics, network management software, automation platforms, and integrated data center infrastructure solutions.

- Strong engineering expertise, advanced ASIC integration capabilities, and large-scale deployment experience supporting AI and cloud infrastructure expansion.

- High infrastructure deployment and upgrade costs may limit adoption among SMEs and regional data center operators.

- Legacy networking architectures and complex multi-vendor integration requirements may increase deployment timelines and operational complexity.

- Large organizational structures may reduce flexibility in addressing niche networking requirements and rapidly evolving AI infrastructure demands.

Emerging Players: Cumulus Networks, Extreme Networks, Supermicro, Infinera

- Focusing on open networking architectures, AI-driven switching ecosystems, programmable networking software, and high-performance interconnect solutions.

- Developing energy-efficient switching platforms, merchant silicon-based architectures, and cloud-native networking solutions optimized for hyperscale and AI workloads.

- Expanding modular and scalable networking deployments supporting edge computing, AI clusters, and distributed cloud environments.

- Faster innovation cycles and greater flexibility in deploying specialized AI networking and programmable infrastructure solutions.

- Strong specialization in merchant silicon, optical networking, software-defined networking, and high-bandwidth interconnect technologies.

- Easier adaptability to emerging AI infrastructure requirements, open networking trends, and cloud-native networking ecosystems.

- Limited enterprise networking ecosystem scale and smaller global deployment footprints compared to established networking leaders.

- Dependence on OEM partnerships, cloud providers, and channel ecosystems for broader market penetration.

- Lower brand visibility among traditional enterprise customers and limited resources for supporting highly complex multinational deployments.

Recent Development

-

In July 2025, Arista Networks introduced a new suite of AI-enabled enterprise networking solutions, expanding its portfolio across switching, Wi-Fi 7 access points, and WAN capabilities. The updated campus portfolio includes compact switches with enhanced Power over Ethernet (PoE) functionality, along with a broader range of cost-efficient Wi-Fi 7 indoor and outdoor access points tailored for branch environments. These enhancements are designed to support emerging IoT use cases, including Electronic Shelf Label (ESL) applications, while strengthening AI-driven network performance and scalability.

-

In July 2025, Hewlett Packard Enterprise Development LP finalized its acquisition of Juniper Networks, Inc. This strategic move strengthens HPE’s position in the expanding AI and hybrid cloud market by adding a comprehensive, cloud-native, and AI-powered networking portfolio. The integration of Juniper’s technologies enables HPE to offer a modern, end-to-end networking stack, reinforcing its ability to deliver advanced, AI-driven IT solutions.

-

In February 2025, Cisco Systems unveiled a new family of data center Smart Switches designed to redefine conventional network architectures by integrating networking and security services into a single compact platform. Powered by programmable AMD Pensando data processing units (DPUs), the switches operate as high-capacity, multifunctional service-hosting systems, enabling more streamlined and efficient data center designs. The first integrated solution, Smart Switch with Cisco Hypershield, embeds security directly into the network fabric, introducing a fabric-native security model tailored for AI-driven data center environments.

Data Center Switch Market Report Scope

Report Attribute

Details

Market size in 2025

USD 15.0 Billion

Estimated market size in 2026

USD 16.3 billion

Projected market size by 2033

USD 34.2 billion

Growth rate

CAGR of 11.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Type, technology, port speed, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Arista Networks; Broadcom; Cisco Systems; Cumulus Networks; Dell Technologies; Extreme Networks; Hewlett Packard Enterprise Development LP; Huawei Technologies; Infinera; Juniper Networks; NEC Corporation; Netgear, Inc.; NVIDIA; Pluribus Networks; Super Micro Computer, Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Switch Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global data center switch market report based on type, technology, port speed, end use, and region.

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Core Switches

-

Distribution Switches

-

Access Switches

-

Others

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Ethernet

-

InfiniBand

-

Fiber Channel

-

Others

-

-

Port Speed Outlook (Revenue, USD Billion, 2021 - 2033)

-

Less than 10 GBPS

-

>10G to 40 GBPS

-

>40G to 100 GBPS

-

>100 GBPS

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Enterprises

-

Telecommunication Industry

-

Government Organizations

-

Cloud Service Providers

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

AI networking infrastructure and hyperscale switch deployment assessment

Analysis of AI-driven networking adoption trends across hyperscale cloud providers, enterprise AI data centers, colocation facilities, and high-performance computing (HPC) environments.

Evaluation of Ethernet fabric architectures, InfiniBand deployments, GPU cluster interconnect requirements, and ultra-low-latency switching capabilities supporting AI and accelerated computing workloads.

Identified high-growth AI networking deployment opportunities and hyperscale infrastructure investment trends.

Supported expansion strategies targeting AI factories, GPU-intensive computing environments, and cloud-scale networking ecosystems.

Highlighted evolving bandwidth, latency, and network scalability requirements across modern AI data center infrastructures.

Edge data center and distributed computing networking opportunity analysis

Assessment of switching requirements for edge data centers, modular facilities, telecom edge deployments, and distributed cloud computing environments.

Analysis of compact, energy-efficient, and low-latency switching solutions supporting 5G, IoT, and real-time analytics applications.

Identified emerging growth opportunities in decentralized and edge computing infrastructure markets.

Supported expansion strategies targeting telecom, industrial IoT, and low-latency networking environments.

Highlighted demand trends for scalable and compact edge networking architectures.

Data center interconnect (DCI) and metro networking opportunity analysis

Evaluation of DCI switching technologies supporting long-distance data transfer, metro connectivity, and disaster recovery environments.

Analysis of low-latency optical transport integration and high-bandwidth interconnect architectures.

Identified emerging opportunities in interconnect and distributed data infrastructure ecosystems.

Supported network expansion strategies for geographically distributed cloud and enterprise operations.

Highlighted the increasing demand for resilient and high-capacity DCI infrastructures.

Frequently Asked Questions About This Report

The global data center switch market is expected to grow at a compound annual growth rate of 11.1% from 2026 to 2033 to reach USD 34.2 billion by 2033.

North America dominated the industry with the largest revenue share of 41.7% in 2025.

The data center switch market in Asia Pacific is anticipated to grow at the fastest CAGR during the forecast period.

The ethernet segment accounted for the largest market revenue share of 85.8% in 2025, driven by cost-per-bit efficiency, a broad interoperability ecosystem, and a continuous standardization roadmap that ensures long-term scalability.

The >40G to 100 GBPS segment accounted for the largest market revenue share of 36.7% in 2025 and >100 GBPS segment is expected to grow at the fastest CAGR during the forecast period.

The cloud service providers segment accounted for the largest market revenue share of 41.2% in 2025

The global data center switch market size was estimated at USD 14.9 billion in 2025 and is expected to reach USD 16.3 billion in 2026.

Some key players operating in the data center switch market include Arista Networks, Broadcom, Cisco Systems, Cumulus Networks, Dell Technologies, Extreme Networks, Hewlett Packard Enterprise Development LP, Huawei Technologies, Infinera, Juniper Networks, NEC Corporation, Netgear, Inc., NVIDIA, Pluribus Networks, Super Micro Computer, Inc.

The global data center switch market is driven by hyperscale infrastructure expansion, architectural transformation within data centers, and exponential growth in data-intensive workloads.

The core switches segment dominated the market and accounted for the revenue share of 47.0% in 2025 while the access switches segment is anticipated to grow at the fastest CAGR during the forecast period.

About the Author(s)

Communications Infrastructure Research Team

Technology · Communications InfrastructureThis report was authored by the communications infrastructure research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communications infrastructure segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.