- Home

- »

- Plastics, Polymers & Resins

- »

-

Dissolvable Support Material Polymers Market Report, 2033GVR Report cover

![Dissolvable Support Material Polymers Market (2025 - 2033)Report]()

Dissolvable Support Material Polymers Market (2025 - 2033)

Size, Share & Trends Analysis Report By Product (Polyvinyl Alcohol (PVA), High Impact Polystyrene (HIPS)), By End-use, By Region, And Segment Forecasts

Dissolvable Support Material Polymers Market Summary

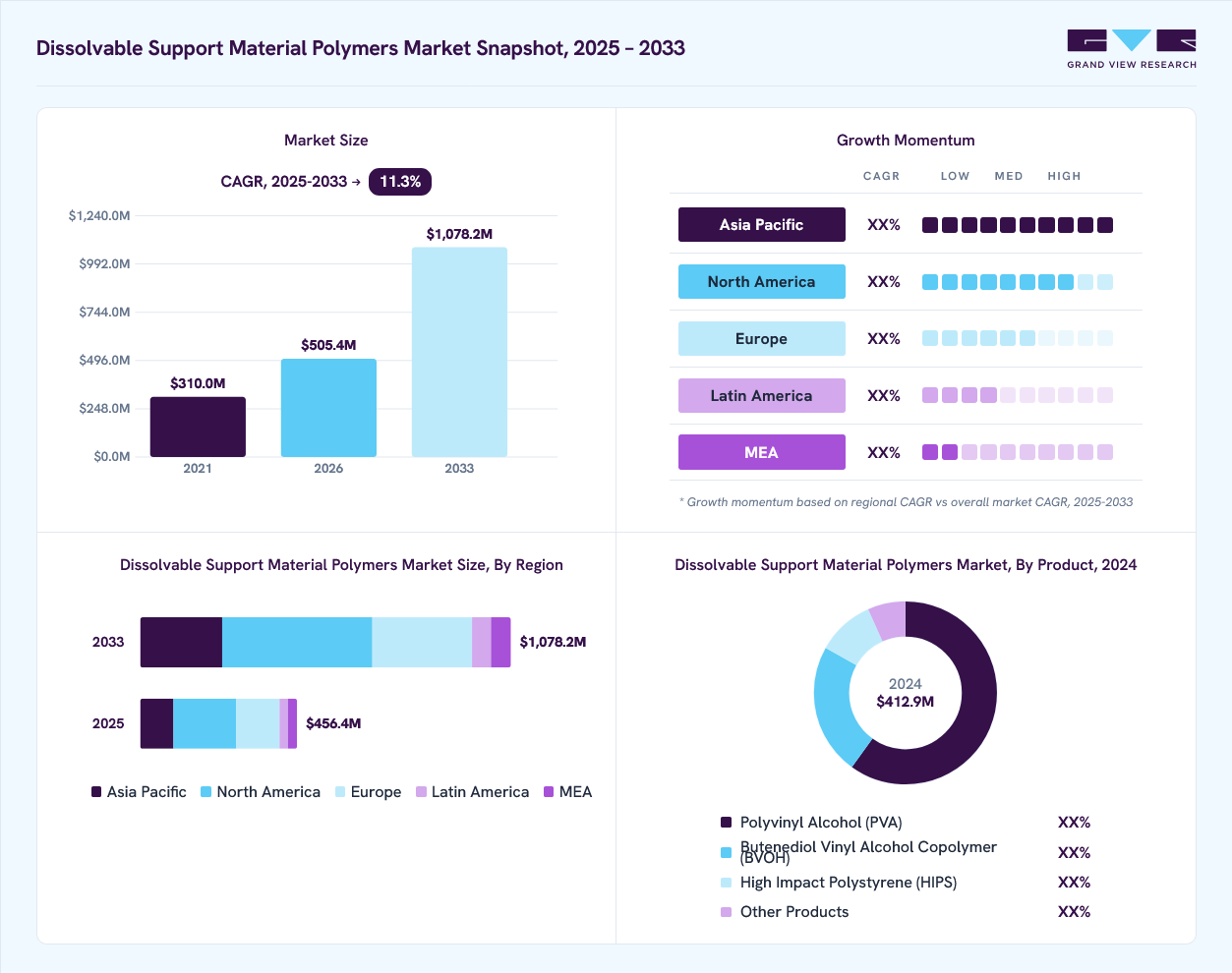

The global dissolvable support material polymers market size was estimated at USD 412.86 thousand in 2024 and is projected to reach USD 1,078.24 thousand by 2033, growing at a CAGR of 11.3% from 2025 to 2033. The growing use of multi-material 3D printing in industries such as healthcare and automotive is driving demand for dissolvable support materials that enable precise, complex designs.

Key Market Trends & Insights

- North America dominated the global dissolvable support material polymers industry with the largest revenue share of 39.99% in 2024.

- The dissolvable support material polymers industry in Canada is expected to grow at a substantial CAGR of 12.5% from 2025 to 2033.

- By product, the High Impact Polystyrene (HIPS) segment is expected to grow at a considerable CAGR of 11.8% from 2025 to 2033 in terms of revenue.

- By end use, the medical & healthcare segment is expected to grow at a considerable CAGR of 12.1% from 2025 to 2033 in terms of revenue.

Market Size & Forecast

- 2024 Market Size: USD 412.86 thousand

- 2033 Projected Market Size: USD 1,078.24 thousand

- CAGR (2025-2033): 11.3%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Manufacturers are adopting these polymers to reduce post-processing time and improve overall production efficiency.The dissolvable support material polymers industry is moving from niche prototyping into mainstream production as additive manufacturing shifts toward end use parts.")

Material innovation is focusing on faster, cleaner dissolution and broader compatibility with engineering-grade feedstocks, while service models that bundle consumables with post-processing solutions are gaining traction. This evolution is enabling more complex geometries and integrated assemblies that were previously impractical, driving OEMs and contract manufacturers to consider dissolvable supports as a standard workflow element.

Drivers, Opportunities & Restraints

The primary commercial driver is the operational efficiency and quality improvement that dissolvable supports deliver compared with manual removal. For industries that require tight tolerance and surface consistency, such as medical devices and aerospace components, the ability to eliminate mechanical finishing reduces labor inputs, scrap risk, and time to market. Regulatory and certification pressures that favor reproducible, low contamination post-processing further encourage adoption, especially where part cleanliness and repeatability are critical.

There is a clear opportunity to capture value by developing application-specific chemistries and service ecosystems. Suppliers that offer rapid dissolution chemistries, closed-loop solvent recovery, or certified biocompatible formulations can command premium positions. Partnerships with printer manufacturers to certify support materials, and with large end users to co-develop scale up processes, open pathways to recurring revenue through consumables, maintenance contracts, and technical services. Tailoring solutions for high-volume manufacturing could unlock substantial new demand.

Widespread adoption is constrained by technical and supply chain realities that raise the total cost of ownership for some users. Compatibility issues with high-performance build polymers, potential residues or byproducts from dissolution, and the need for dedicated wash equipment increase capital and operating expenses. In addition, specialty polymer feedstock supply is concentrated and can be volatile, and concerns about solvent handling, waste treatment, and regulatory compliance create barriers for manufacturers evaluating conversion from traditional support removal methods.

Market Concentration & Characteristics

The market growth stage of the dissolvable support material polymers industry is high, and it accelerating in pace. The market exhibits slight fragmentation, with key players dominating the industry landscape. Major companies such as Sekisui Specialty Chemicals, Mitsubishi Chemical Corporation, Wacker Chemie AG, and others, play a significant role in shaping the market dynamics. These leading players often drive innovation within the market, introducing new products, technologies, and applications to meet evolving industry demands.

Innovation in dissolvable support polymers is now as much about systems integration as it is about chemistry. Recent material advances, such as BVOH, demonstrate much faster, cleaner dissolution and lower moisture sensitivity than legacy PVA, which reduces handling risk and shortens post-processing cycles. At the same time, OEMs and post processing vendors are building certified wash stations, solvent recovery systems, and validated process workflows that turn a material into a repeatable production capability for regulated verticals. These combined material and equipment improvements are shifting dissolvable supports from a prototyping convenience to a certified production enabler for industries that demand traceability and low contamination.

The market for dissolvable supports faces a varied substitute set that competes on cost, speed, and operational footprint. Breakaway supports remain the lowest capital route for many users because they require no solvents or special wash equipment, while HIPS dissolved in d-limonene and specialized soluble waxes serve as established alternatives where chemistry and part finishing requirements differ. Advances in support-minimizing software, improved part orientation strategies, and automated mechanical removal cells also erode some use cases by reducing the need for any sacrificial material. Suppliers must therefore compete not just on dissolution performance but on total process economics, certification, and ease of integration.

Product Insights

Polyvinyl Alcohol (PVA) dominated the market across the product segmentation in terms of revenue, accounting for a market share of 59.87% in 2024, and it is forecasted to grow at a 11.5% CAGR from 2025 to 2033. Increasing demand for greener, easily recyclable manufacturing workflows is strengthening PVA’s commercial position because its water solubility and biodegradability simplify part separation end-of-life processing.

Suppliers who can certify medical-grade and high-purity PVA for sensitive applications, while reducing humidity sensitivity in storage and print environments, will capture premium share. Recent lab-scale demonstrations that use PVA to enable fully recyclable printed electronics underscore fresh adjacent use cases beyond supports, which expand buyer interest from prototyping into tooling and low duty cycle production.

The High Impact Polystyrene (HIPS) segment is anticipated to grow at a substantial CAGR of 11.8% through the forecast period. The market is driven by HIPS compatibility with high temperature engineering build plastics and a well-established solvent removal process using d-limonene, making it the preferred soluble support for ABS and similar materials at scale.

This compatibility reduces rework and surface remediation costs on complex assemblies, and creates a clear value proposition for industrial users adopting dual extrusion systems. Manufacturers that streamline solvent handling and recovery and certify limonene-based wash stations will lower operating friction and accelerate adoption in production workshops.

End Use Insights

Aerospace and Defense dominated the market across the end use segmentation in terms of revenue, accounting for a market share of 20.83% in 2024, and it is forecasted to grow at a 11.5% CAGR from 2025 to 2033. The aerospace and defense sector is driving demand for dissolvable supports through a need for intricate internal geometries, topology-optimized components, and rapid on-demand replacement parts that cannot tolerate manual support removal.

Defense primes and OEMs are actively qualifying polymer additive workflows that integrate soluble supports to reduce labor and preserve critical tolerances for flight hardware and ground systems. Companies that can demonstrate process traceability, material certification, and closed loop post processing for regulated aerospace environments will become preferred suppliers as additive moves from tooling into certified end parts.

The Medical & Healthcare segment is expected to expand at a substantial CAGR of 12.1% through the forecast period. In the medical sector, the unique driver is regulatory and biocompatibility pressure that favors water-soluble, residue free supports because clinical devices and surgical guides demand exceptionally clean surfaces and reproducible post-processing.

PVA and other certified dissolvable chemistries enable complex patient-specific geometries and internal channels without mechanical finishing, which reduces contamination risk and shortens clinical production cycles. Vendors that invest in certified cleanroom wash systems and validated material lots for regulatory submissions will unlock hospital and contract manufacturing business at scale.

Regional Insights

North America dissolvable support material polymers industry held the largest share of 39.99% in terms of revenue of the global market in 2024. The region’s driver is a mature industrial additive ecosystem that combines high enterprise adoption of industrial FDM and pellet extrusion printers with strong service networks for post processing, making dissolvable supports commercially attractive for scale manufacturing. Established contract manufacturers and OEMs favor water soluble chemistries because they reduce manual finishing costs and enable tighter quality control across distributed production sites. Given the prevalence of certified supply chains and expectations for traceability, material suppliers that offer validated process packages and service support gain rapid credibility with large buyers.

U.S. Dissolvable Support Material Polymers Market Trends

The dissolvable support material polymers industry growth in the U.S. is being fueled by regulated end uses and defense modernization programs that demand on-demand, low touch post processing for complex parts. Hospitals, medical device contract manufacturers and defense primes are prioritizing workflows that remove human variability and contamination risk, which elevates the value of dissolvable supports for clinical and mission critical components. Suppliers who can demonstrate regulatory readiness, solvent handling best practice and integration with validated wash equipment win procurement conversations.

Europe Dissolvable Support Material Polymers Market Trends

The European dissolvable support material polymers industry demand is being shaped by stringent environmental expectations and a strong push toward circular manufacturing, which favors water-soluble supports that simplify material recovery and minimize mechanical waste. Procurement teams across automotive and medical clusters are increasingly scoring vendors on lifecycle impacts and closed-loop capabilities, so dissolvable chemistries paired with solvent recovery and recycling services stand out. Companies that present certified environmental compliance and documented end-of-life pathways gain a competitive preference.

Asia Pacific Dissolvable Support Material Polymers Market Trends

Asia Pacific dissolvable support material polymers industry is anticipated to grow at the fastest CAGR of 11.9% over the forecast period. Rapid industrialization and investment in domestic additive manufacturing capacity are driving adoption across APAC, where electronics, automotive and tooling sectors scale 3D printing from prototyping into production. Cost sensitive manufacturers in the region prefer support materials that cut labor and cycle time while fitting into automated post processing cells, which accelerates uptake of faster dissolving chemistries and certified wash stations. Strategic suppliers that localize supply, technical service and solvent recovery will capture mindshare as onshore production volumes rise.

China’s dissolvable support material polymers industry is driven by the national push to localize advanced manufacturing and shorten supply chains, which creates strong demand for integrated additive solutions including dissolvable supports that enable complex part geometries at scale. Large equipment vendors and filament producers are rapidly qualifying new chemistries and bundling them with turnkey post processing equipment to support high-volume consumer electronics and industrial printing. Market entrants that partner with domestic printer OEMs and provide regulatory and environmental compliance for wash processes can scale rapidly in China’s fast moving industrial landscape.

Key Dissolvable Support Material Polymers Company Insights

The dissolvable support material polymers industry is highly competitive, with several key players dominating the landscape. Major companies include Sekisui Specialty Chemicals, Mitsubishi Chemical Corporation, Wacker Chemie AG, and others.

The dissolvable support material polymers industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their types.

Key Dissolvable Support Material Polymers Companies:

The following are the leading companies in the dissolvable support material polymers market. These companies collectively hold the largest market share and dictate industry trends.

- Sekisui Specialty Chemicals

- Mitsubishi Chemical Corporation

- Wacker Chemie AG

- Chang Chun Petrochemicals

- Ningxia Dadi Circular Development

- Sinopec

- Kuraray Co. Ltd.

- Anhui Wanwei Group

- Celanese

- Nippon Synthetic Chemical

Recent Developments

-

In April 2025, Mitsubishi Chemical Corporation (MCC) obtained ISCC PLUS certification for several of its polyvinyl alcohol products, confirming their sustainable use of recycled and biomass raw materials throughout the supply chain, including manufacturing. This certification allows MCC to manage these products using the mass balance method, ensuring proper sustainability practices. The company’s achievement strengthens its commitment to environmentally responsible production.

-

In February 2023,Mitsubishi Chemical Group announced its decision to build a new facility at its Okayama Plant to increase production capacity of its specialty polyvinyl alcohol resins, GOHSENX and Nichigo G-Polymer. The new plant began operations in October 2024.

Dissolvable Support Material Polymers Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 456.41 thousand

Revenue forecast in 2033

USD 1,078.24 thousand

Growth rate

CAGR of 11.3% from 2025 to 2033

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD Thousand, Volume in Tons, and CAGR from 2025 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Global Dissolvable Support Material Polymers Market Report Segmentation

Product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; France; UK; Spain; Italy; China; Japan; India; South Korea; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Sekisui Specialty Chemicals; Mitsubishi Chemical Corporation; Wacker Chemie AG; Chang Chun Petrochemicals; Ningxia Dadi Circular Development; Sinopec; Kuraray Co. Ltd.; Anhui Wanwei Group; Celanese; Nippon Synthetic Chemical

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Dissolvable Support Material Polymers Market Report Segmentation

This report forecasts revenue & volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global dissolvable support material polymers market report based on product, end use, and region:

-

Product Outlook (Volume, Tons; Revenue, USD Thousand, 2021 - 2033)

-

Polyvinyl Alcohol (PVA)

-

Butenediol Vinyl Alcohol Copolymer (BVOH)

-

High Impact Polystyrene (HIPS)

-

Other Products

-

-

End Use Outlook (Volume, Tons; Revenue, USD Thousand, 2021 - 2033)

-

Aerospace & Défense

-

Automotive & Transportation

-

Medical & Healthcare

-

Consumer Goods & Electronics

-

Other End Uses

-

-

Regional Outlook (Volume, Tons; Revenue, USD Thousand, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Frequently Asked Questions About This Report

The global dissolvable support material polymers market size was estimated at USD 412.86 thousand in 2024 and is expected to reach USD 456.41 thousand in 2025.

The global dissolvable support material polymers market is expected to grow at a compound annual growth rate of 11.3% from 2025 to 2033 to reach USD 1,078.24 thousand by 2033.

Polyvinyl Alcohol (PVA) dominated the dissolvable support material polymers market across the product segmentation in terms of revenue, accounting for a market share of 59.87% in 2024 and is forecasted to grow at 11.5% CAGR from 2025 to 2033.

Some key players operating in the dissolvable support material polymers market include Sekisui Specialty Chemicals, Mitsubishi Chemical Corporation, Wacker Chemie AG, Chang Chun Petrochemicals, Ningxia Dadi Circular Development, Sinopec, Kuraray Co. Ltd., Anhui Wanwei Group, Celanese, and Nippon Synthetic Chemical.

The growing use of multi-material 3D printing in industries such as healthcare and automotive is driving demand for dissolvable support materials that enable precise, complex designs. Manufacturers are adopting these polymers to reduce post-processing time and improve overall production efficiency.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.