- Home

- »

- Pharmaceuticals

- »

-

Ebola Market Size, Share And Trends Report, 2026-2033GVR Report cover

![Ebola Market (2026 - 2033)Report]()

Ebola Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (By Therapeutic (Product Type, Route of Administration, Procurement Channel), By Diagnostic (Test Type, End Use)), By Region, And Segment Forecasts

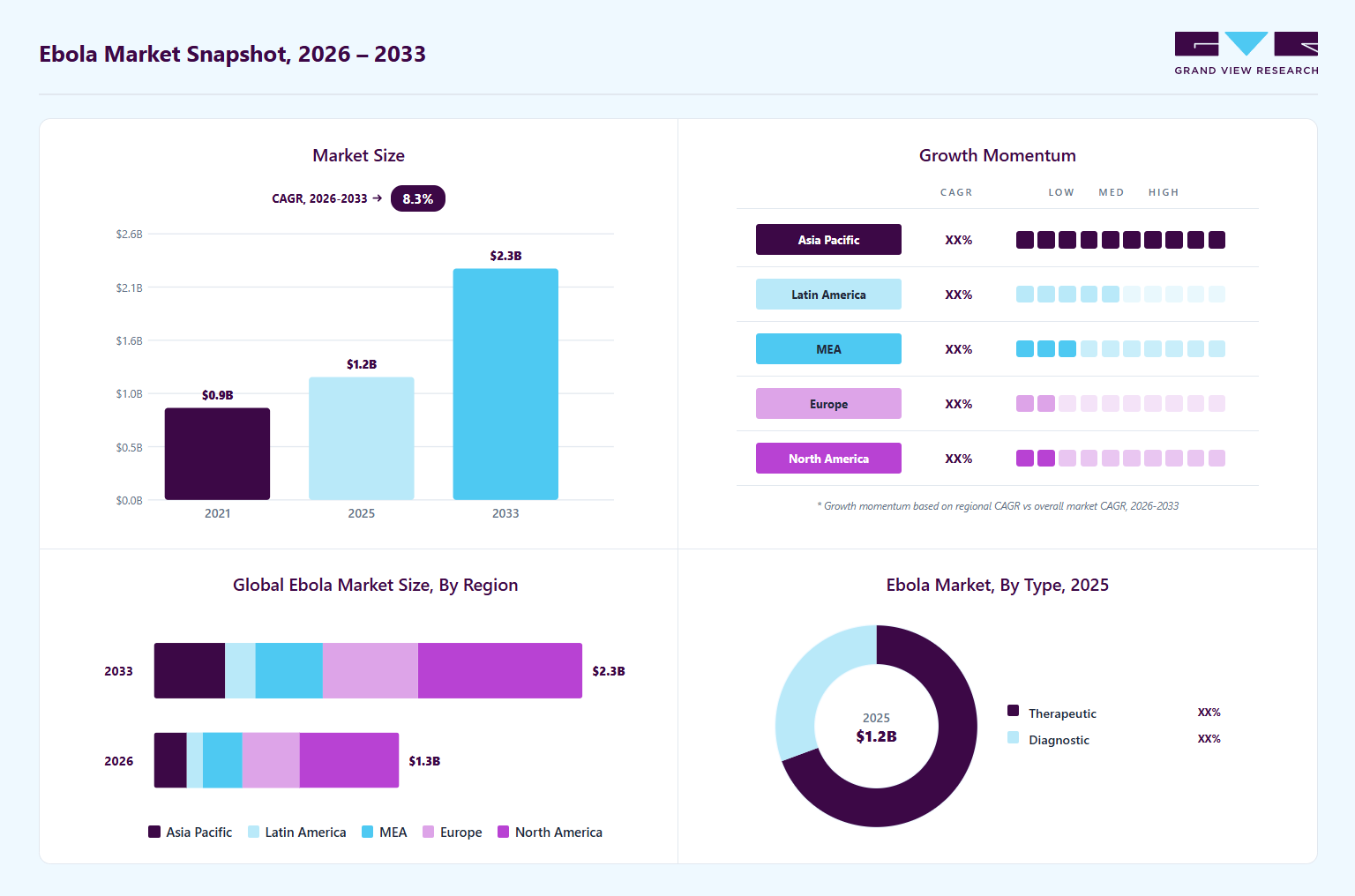

Market Size, 2025

$1.2BMarket Estimate, 2026

$1.3BMarket Forecast, 2033

$2.3BCAGR, 2026–2033

8.3%Ebola Market Summary

The global ebola market size was valued at USD 1.2 billion in 2025 and is projected to grow from USD 1.3 billion in 2026 to USD 2.3 billion by 2033, at a CAGR of 8.3% from 2026 to 2033. The market in North America dominated with a revenue share of 40.9% in 2025. The market is witnessing sustained growth due to the increasing emphasis on outbreak preparedness, preventive immunization programs, and rapid-response healthcare infrastructure across high-risk regions.

Key Market Trends & Insights

- By product type: Vaccine segment held the largest market share of 51.4% in 2025.

- By route of administration: Intramuscular (IM) segment held the largest market share in 2025.

- By procurement channel: Public segment held the largest market share in 2025.

- By test type: Molecular diagnostic tests segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (40.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- 2025 Market Size: USD 1.2 Billion

- Estimated market size in 2026: USD 1.3 billion

- 2033 Projected Market Size: USD 2.3 Billion

- CAGR (2026-2033): 8.3%

Healthcare organizations are prioritizing vaccination strategies to strengthen epidemic containment efficiency and reduce mortality rates during outbreaks. The commercial availability of approved vaccines such as Ervebo and Zabdeno/Mvabea has significantly improved large-scale deployment capabilities across Africa and other vulnerable regions. Expanding cold-chain infrastructure, improvements in emergency healthcare logistics, and rising awareness regarding viral hemorrhagic fever transmission risks are further supporting vaccine accessibility and preparedness initiatives. Healthcare providers are also increasingly focusing on rapid immunization coverage for frontline healthcare workers and vulnerable populations exposed to outbreak environments. For instance, in May 2026, the World Health Organization declared the Ebola disease outbreak in the Democratic Republic of the Congo and Uganda a Public Health Emergency of International Concern (PHEIC) following the rapid spread of the Bundibugyo virus strain. The organization reported 246 suspected cases and 80 suspected deaths across at least 3 health zones in Ituri Province, DRC, as of 16 May 2026. In Uganda, 2 confirmed cases linked to travel from DRC were identified, while 8 out of 13 collected samples tested positive for the Bundibugyo virus. The outbreak also resulted in 4 deaths among healthcare workers, highlighting the urgent need for expanded vaccination coverage, outbreak preparedness, and infection control programs across affected regions.

")

The increasing adoption of rapid molecular diagnostic technologies is another major factor driving the Ebola market. Healthcare institutions are emphasizing early disease detection, real-time surveillance, and rapid patient isolation to improve the efficiency of outbreak containment. RT-PCR molecular diagnostics remain the gold standard for Ebola confirmation, while portable point-of-care testing systems are gaining significant traction in decentralized healthcare environments. Diagnostic manufacturers are investing in automated and multiplex testing platforms capable of detecting multiple hemorrhagic fever pathogens simultaneously. The expansion of biosurveillance infrastructure and mobile laboratory networks across high-risk regions is further strengthening market demand. In addition, healthcare systems are increasingly integrating infectious disease monitoring technologies and emergency response coordination systems to improve laboratory efficiency and outbreak management capabilities. For instance, in May 2026, the Centers for Disease Control and Prevention reported that the Ebola Bundibugyo outbreak in DRC and Uganda had resulted in 11 confirmed cases, 336 suspected cases, and 88 deaths in DRC as of 18 May 2026. The agency also confirmed 2 cases in Uganda, including 1 death linked to travel from DRC, while 8 out of 13 tested samples were positive for the Bundibugyo virus. The outbreak had spread across 9 health zones in Ituri Province, and the CDC noted that the Bundibugyo virus has historically demonstrated mortality rates ranging from 25% to 50%. These developments significantly increased demand for rapid diagnostics, decentralized testing systems, and advanced biosurveillance infrastructure across outbreak-prone regions.

The Ebola market is also benefiting from increasing government focus on border surveillance, emergency preparedness, and international infectious disease monitoring systems to minimize cross-border outbreak transmission risks. Public health agencies are strengthening travel screening programs, quarantine protocols, and healthcare surveillance infrastructure to improve rapid outbreak containment capabilities. Furthermore, growing investments in emergency response coordination, laboratory preparedness, and high-risk contact monitoring are supporting demand for rapid diagnostics, protective equipment, and infection prevention technologies. For instance, in May 2026, the Centers for Disease Control and Prevention announced enhanced travel screening and public health restrictions to prevent Ebola disease transmission into the United States amid the ongoing outbreak in East and Central Africa. The agency implemented a 30-day emergency public health order and imposed entry restrictions on non-U.S. passport holders who had traveled to Uganda, DRC, or South Sudan within the previous 21 days. The CDC also confirmed that 1 American healthcare worker exposed during outbreak response activities in DRC tested positive for Ebola and was transferred to Germany for treatment, while 6 additional high-risk contacts were evacuated for monitoring and care. These developments highlighted the growing importance of coordinated international surveillance systems and emergency preparedness frameworks in strengthening Ebola outbreak management capabilities.

")

The growing clinical preference for monoclonal antibody therapies is significantly contributing to market expansion across Ebola treatment applications. Healthcare providers are increasingly adopting targeted biologic therapies due to their improved therapeutic precision and superior survival outcomes compared to conventional supportive care approaches. Products such as Inmazeb and Ebanga have strengthened confidence in antibody-based treatment protocols during Ebola outbreak response programs. Biopharmaceutical companies are actively expanding infectious disease pipelines focused on next-generation antibody therapies with broader antiviral activity and enhanced treatment durability, while advancements in recombinant biologics manufacturing technologies are improving scalability and accelerating emergency therapeutic deployment capabilities. Rising collaborations among biotechnology companies, healthcare agencies, and infectious disease research institutions are also supporting continued innovation across targeted Ebola therapeutics and immune-based treatment platforms. In May 2026, the Centers for Disease Control and Prevention stated that the Bundibugyo virus outbreak represented the 17th Ebola outbreak in the Democratic Republic of the Congo since 1976 and the country’s second outbreak involving the Bundibugyo strain. The agency noted that most reported infections occurred among individuals aged 20 to 39, while nearly two-thirds of cases involved female patients. The CDC further emphasized that no approved vaccine is currently available for the Bundibugyo virus strain, with treatment primarily consisting of supportive care measures. Additionally, the CDC highlighted its ongoing collaboration with international partners and health ministries in DRC and Uganda through disease surveillance, laboratory diagnostics, infection prevention, and border screening programs, while 41 Laboratory Response Network public health laboratories across the United States remained prepared for Ebola testing and emergency response activities. The organization also referenced the 2014-2016 West African Ebola epidemic, which resulted in nearly 29,000 reported cases globally, reinforcing the need for continued investments in advanced therapeutics, diagnostics, and outbreak preparedness infrastructure worldwide.

Market Concentration & Characteristics

The Ebola market demonstrates a high degree of innovation driven by advancements in recombinant vaccine technologies, monoclonal antibody therapeutics, and rapid molecular diagnostics. Pharmaceutical companies are increasingly utilizing viral vector platforms and precision biologics to improve treatment effectiveness and outbreak response capabilities. Diagnostic innovation centers on portable RT-PCR systems, multiplex testing panels, and rapid antigen-detection technologies for decentralized healthcare environments. Research institutions are also integrating genomic sequencing and biosurveillance tools to improve viral monitoring and outbreak analytics. Companies continue investing in pan-filovirus vaccine development to expand protection against multiple hemorrhagic fever viruses.

The Ebola industry presents substantial barriers to entry due to strict biosafety requirements, high clinical development costs, and complex regulatory frameworks. Product development requires advanced containment laboratories and specialized expertise in infectious disease research and biologics manufacturing. Clinical trials remain operationally challenging due to the sporadic nature of Ebola outbreaks and limited patient availability. Vaccine production and monoclonal antibody manufacturing also require sophisticated cold-chain distribution infrastructure and high-quality bioprocessing capabilities. Market participation remains concentrated among companies with established biodefense expertise and strong infectious disease portfolios. The limited commercial patient base further reduces long-term revenue predictability for smaller biotechnology firms attempting to enter the market.

Regulatory frameworks significantly influence the Ebola industry through stringent product approval standards for safety, efficacy, and emergency deployment readiness. Regulatory agencies continue emphasizing accelerated review pathways for Ebola therapeutics and vaccines during outbreak emergencies. Manufacturers must comply with extensive clinical validation requirements and post-marketing safety monitoring obligations. Diagnostic companies are also required to meet rigorous standards regarding sensitivity, specificity, and biosafety handling protocols. Emergency use authorization mechanisms have improved rapid access to diagnostics and biologic therapies during outbreaks. Regulatory harmonization initiatives among international healthcare organizations are further improving the efficiency of cross-border deployment for Ebola countermeasures and infectious disease technologies.

The Ebola market has limited direct substitutes due to the severe nature of Ebola virus disease and the requirement for highly specialized treatments and diagnostics. Supportive care therapies, such as fluid replacement, oxygen support, and intensive care interventions, continue to serve as complementary treatment approaches in areas with limited access to advanced biologic therapies. Broad-spectrum antiviral drugs are occasionally explored as investigational alternatives, although targeted monoclonal antibodies demonstrate superior therapeutic outcomes. Conventional laboratory testing methods may substitute for rapid molecular diagnostics in developed healthcare systems, though they generally offer slower turnaround times and lower field adaptability. Preventive infection control measures and surveillance programs help reduce transmission risks but cannot fully replace vaccines or targeted Ebola therapeutics during outbreak management.

The Ebola market is expanding geographically through increasing deployment of vaccines, diagnostics, and surveillance systems across Africa, Asia Pacific, and selected Middle Eastern regions. Healthcare organizations are strengthening laboratory infrastructure and decentralized testing capabilities to improve outbreak preparedness in remote settings. Market participants are also expanding regional partnerships with healthcare providers and distributors to improve access to emergency products. Rising awareness regarding emerging infectious diseases is accelerating the adoption of portable molecular diagnostics outside traditionally endemic regions. Pharmaceutical companies continue to optimize global supply chains and localized manufacturing strategies to improve emergency response efficiency. Increasing integration of infectious disease preparedness protocols within healthcare systems is further supporting long-term geographical market expansion.

Therapeutic

Product Insights

The vaccine segment dominated the Ebola industry, accounting for the largest revenue share of 51.4% in 2025, driven by increasing adoption of preventive immunization programs and the widespread deployment of approved Ebola vaccines during outbreak preparedness initiatives. Commercially available vaccines such as Ervebo and Zabdeno/Mvabea strengthened rapid response capabilities across outbreak-prone regions. Healthcare organizations prioritized vaccination strategies for frontline workers and high-risk populations, supported by strong clinical effectiveness, regulatory approvals, and expanding cold-chain infrastructure, ensuring accessibility in remote settings. Pharmaceutical companies also increased manufacturing scalability to maintain emergency stockpiles and ensure rapid supply during epidemics. Improvements in surveillance and vaccination logistics further supported long-term demand. For instance, in April 2025, the World Health Organization stated Ebola disease had an average case fatality rate of around 50%, with historical mortality ranging from 25% to 90%. It also noted 3 causative viruses, including Ebola, Sudan, and Bundibugyo, and confirmed 2 approved vaccines for Ebola virus disease, reinforcing preventive immunization importance across high-risk regions.

The monoclonal antibodies segment is projected to grow at a CAGR of 15.1% over the forecast period, driven by increasing adoption of targeted biologic therapies and improved clinical outcomes in Ebola virus disease management. Products such as Inmazeb and Ebanga have demonstrated strong survival benefits, supporting wider use during outbreak response. The segment is further supported by advancements in recombinant biologics manufacturing, improved emergency deployment capabilities, and rising preference for high-precision therapies. Research collaborations are also accelerating innovation in next-generation antibody platforms. For instance, in February 2025, Nature Communications reported that monoclonal antibody 3A6 targeted the GP1,2 glycoprotein spike, binding the MPER epitope spanning residues 626-640. It showed strong protection in guinea pig and rhesus macaque models, with structural binding at 2.5 A and 1.27 A resolution. The antibody retained efficacy at low doses, while escape mutations at D632 and P636 confirmed its binding specificity, reinforcing its therapeutic potential for advancing Ebola treatment.

Route of Administration Insights

The Intramuscular (IM) segment dominated the Ebola industry, accounting for the largest revenue share of 66.6% in 2025, driven by the widespread administration of Ebola vaccines such as ERVEBO and Zabdeno/Mvabea through intramuscular delivery. The route supports rapid immunization deployment, simplified administration procedures, and improved accessibility in outbreak-prone, resource-limited regions. Healthcare providers prefer intramuscular administration for large-scale vaccination campaigns due to faster operational execution and reduced dependency on advanced infusion infrastructure. The route also improves treatment adherence and enables efficient implementation of ring vaccination strategies during emergency outbreak response activities. Expanding vaccine stockpiling initiatives and increasing focus on preventive immunization programs are further supporting segment dominance. In addition, the growing availability of portable cold-chain systems and field vaccination infrastructure continues to strengthen the adoption of intramuscular Ebola vaccine administration globally.

The Intravenous (IV) segment is projected to grow at a CAGR of 11.36% over the forecast period, driven by the increasing adoption of monoclonal antibody therapies for Ebola virus treatment. Intravenous administration enables rapid systemic drug delivery and optimized therapeutic bioavailability during severe Ebola infections requiring immediate clinical intervention. Products such as Inmazeb and Ebanga rely on IV infusion protocols to achieve effective antiviral activity and improved survival outcomes. Healthcare institutions are increasingly integrating advanced infusion-based biologic therapies into infectious disease treatment programs and emergency care systems. Advancements in portable infusion technologies, critical care monitoring systems, and biologics administration capabilities are further supporting segment growth. Rising clinical preference for targeted immune-based therapies and the increasing development of pan-filovirus monoclonal antibody platforms are expected to accelerate demand for intravenous administration across outbreak management settings.

Procurement Channel Insights

The public segment dominated the market with the largest revenue share of 83.9% in 2025, due to the high dependence on public health procurement programs for Ebola vaccines, therapeutics, and diagnostic technologies. International health organizations, national healthcare agencies, and outbreak response institutions remain the primary purchasers of Ebola-related medical countermeasures. The segment benefits from large-scale stockpiling initiatives, emergency preparedness programs, and centralized procurement mechanisms that strengthen the efficiency of outbreak response. Public healthcare systems also invest significantly in laboratory surveillance infrastructure and rapid diagnostic deployment capabilities across high-risk regions. In addition, large vaccination campaigns and emergency therapeutic distribution programs continue to support strong procurement volumes through public sector channels. The specialized nature of Ebola management and the limited routine commercial demand further reinforce public procurement dominance in the global market landscape.

The private segment is projected to grow at the fastest CAGR of 10.6% over the forecast period, driven by increased participation from private healthcare providers, biotechnology firms, and specialized diagnostic laboratories in infectious disease management. Private sector organizations are expanding investments in rapid molecular testing technologies, biologics manufacturing, and advanced laboratory services for emerging infectious diseases. The segment is also benefiting from rising adoption of high-performance diagnostic platforms and specialized infectious disease treatment capabilities within private healthcare networks. Pharmaceutical companies continue to strengthen strategic collaborations with private distributors and healthcare institutions to improve commercial access to Ebola therapeutics and diagnostics. Growing awareness regarding outbreak preparedness among corporate healthcare systems and travel medicine providers is further supporting segment expansion. Increasing integration of private laboratory infrastructure into regional biosurveillance networks is expected to create additional long-term growth opportunities.

Diagnostic

Test Type Insights

The molecular diagnostic Tests segment dominated the Ebola market with the largest revenue share of 59.2% in 2025 due to the widespread clinical adoption of RT-PCR technologies for accurate Ebola virus confirmation and outbreak surveillance activities. Molecular diagnostics remain the gold standard for Ebola detection due to their high sensitivity and specificity, and their ability to detect infections at early disease stages. Healthcare providers and public health laboratories continue to prioritize molecular testing platforms to improve patient isolation efficiency and outbreak containment. The segment is also benefiting from increasing deployment of automated RT-PCR systems, multiplex pathogen panels, and portable molecular testing technologies across decentralized healthcare settings. Expanding laboratory modernization initiatives and growing integration of genomic surveillance systems are further strengthening market demand. In addition, increased focus on detecting multiple filovirus strains, including Bundibugyo virus and Sudan virus, continues to support the adoption of advanced molecular diagnostic platforms.

The rapid diagnostic tests segment is projected to grow at a CAGR of 15.5% over the forecast period, driven by increasing demand for decentralized, point-of-care Ebola testing solutions in outbreak-prone regions. Rapid diagnostic tests offer faster turnaround times, simplified operational workflows, and reduced dependence on centralized laboratory infrastructure, making them highly suitable for remote healthcare environments. Healthcare organizations are increasingly adopting rapid antigen testing technologies to improve early outbreak detection and accelerate emergency response coordination. The segment is also benefiting from ongoing advancements in portable diagnostic platforms and multiplex rapid testing capabilities for viral hemorrhagic fever detection. Growing investments in field-deployable diagnostics and mobile healthcare systems are further supporting segment growth. Rising emphasis on real-time surveillance and rapid screening during epidemic situations is expected to accelerate the adoption of rapid Ebola diagnostic technologies globally.

End Use Insights

The government & public health agencies segment dominated the market, accounting for the largest revenue share of 41.7% in 2025, due to the central role of public health institutions in Ebola outbreak surveillance, vaccination deployment, emergency preparedness, and infectious disease management programs. Government laboratories and public health agencies remain the primary providers of large-scale diagnostic testing, outbreak monitoring, and therapeutic distribution in high-risk regions. The segment benefits from increased investments in biosurveillance infrastructure, laboratory modernization, and emergency response systems designed to enhance the efficiency of epidemic containment. Public healthcare organizations also maintain extensive procurement activities involving vaccines, monoclonal antibody therapies, and rapid molecular diagnostic technologies. In addition, centralized disease monitoring frameworks and international outbreak coordination activities continue supporting strong segment dominance. The recurring threat of Ebola outbreaks across endemic regions further reinforces the critical operational role of public health agencies within the global market.

The diagnostic laboratories segment is projected to grow at the second-fastest CAGR of 14.2% over the forecast period, driven by the increasing adoption of advanced molecular testing technologies and the expansion of infectious disease surveillance networks. Diagnostic laboratories are strengthening capabilities in RT-PCR testing, genomic sequencing, and multiplex pathogen detection to improve the efficiency of Ebola outbreak monitoring. The segment is also benefiting from the rising deployment of automated laboratory systems and portable molecular diagnostic platforms across regional healthcare networks. Private and hospital-based laboratories are increasingly participating in emergency preparedness initiatives and infectious disease analytics programs. Growing demand for rapid turnaround times and decentralized diagnostic capabilities is further accelerating investment in laboratory infrastructure modernization. In addition, expanding integration between laboratory data systems and real-time biosurveillance platforms is expected to support long-term growth in the Ebola diagnostics market.

Regional Insights

North America held the largest Ebola market share of 40.9% in 2025 due to the strong presence of advanced biotechnology and infectious disease companies. The region maintains extensive adoption of Ebola vaccines, monoclonal antibodies, and molecular diagnostics across healthcare systems. Clinical laboratories continue integrating advanced RT-PCR testing platforms for outbreak preparedness applications. Pharmaceutical companies are expanding biologics manufacturing and infectious disease research activities throughout the region. The United States is the largest contributor to regional market revenue. Continuous innovation in vaccine technologies and rapid diagnostic platforms supports long-term market expansion.

U.S. Ebola Market Trends

The U.S. represents the largest country-level market within North America for Ebola therapeutics and diagnostics. The country maintains an advanced clinical research infrastructure focused on the management of emerging infectious diseases. Commercial availability of approved Ebola vaccines and antibody therapies supports strong product penetration across healthcare institutions. Diagnostic laboratories continue to integrate automated molecular testing platforms into infectious disease surveillance systems. Biotechnology companies are strengthening research collaborations involving viral hemorrhagic fever countermeasures. Rising emphasis on rapid outbreak preparedness continues to support sustained market demand.

Europe Ebola Market Trends

Europe maintains a significant share of the Ebola industry through advanced pharmaceutical innovation and strong infectious disease surveillance capabilities. Healthcare systems across the region continue emphasizing rapid molecular diagnostic deployment and laboratory modernization. The market benefits from increasing adoption of biologics and recombinant vaccine technologies. Diagnostic manufacturers are strengthening partnerships focused on portable testing systems for infectious disease applications. Research institutions continue expanding viral surveillance and outbreak analytics programs. The presence of advanced biotechnology clusters supports continuous product development activities.

The UK Ebola market is characterized by increasing focus on infectious disease diagnostics and biologic treatment innovation. Healthcare institutions continue emphasizing rapid laboratory detection capabilities for high-risk viral infections. Biotechnology companies are expanding antibody-based therapy research and molecular diagnostic development activities. Hospitals are integrating advanced RT-PCR systems into infectious disease surveillance networks. Clinical laboratories continue strengthening outbreak preparedness and emergency response efficiency. Continuous investment in healthcare technology modernization supports market growth.

The Ebola market in Germany is growing. Germany represents a technologically advanced market for Ebola diagnostics and therapeutics in Europe. The country maintains strong expertise in molecular diagnostics and laboratory automation technologies. Healthcare providers are increasingly adopting rapid RT-PCR testing systems for outbreak preparedness. Biopharmaceutical companies continue expanding biologics research and advanced manufacturing capabilities. Research institutions are strengthening collaborations focused on viral surveillance and infectious disease analytics. The presence of leading diagnostic manufacturers supports continued market innovation.

The France Ebola market maintains a stable position, supported by strong clinical research capabilities and infectious disease expertise. The country emphasizes rapid outbreak response readiness within hospital and laboratory systems. Diagnostic laboratories continue to increase their adoption of molecular testing technologies for hemorrhagic fever detection. Pharmaceutical organizations are strengthening biologics research involving targeted antiviral therapies. Healthcare institutions are integrating advanced surveillance protocols into infectious disease management programs. Continuous improvements in laboratory modernization support long-term market development.

Asia Pacific Ebola Market Trends

The Asia Pacific Ebola industry is expected to grow at the fastest CAGR of 11.8% over the forecast period, driven by the increasing adoption of rapid molecular diagnostics and outbreak preparedness systems. Healthcare providers are strengthening infectious disease surveillance infrastructure across densely populated urban areas. Biotechnology companies are expanding regional manufacturing and distribution partnerships for vaccines and biologics. Clinical laboratories continue to integrate automated testing platforms to improve operational efficiency. Expanding healthcare modernization initiatives continue to support strong, long-term market opportunities.

The Japan Ebola market is growing. Japan maintains a technologically advanced healthcare environment supporting the adoption of Ebola diagnostics and biologics. The country emphasizes precision molecular diagnostics and high-quality laboratory infrastructure. Research organizations are expanding infectious disease monitoring capabilities across public health networks. Pharmaceutical companies continue evaluating advanced biologic platforms for emerging viral diseases. Hospitals are integrating rapid testing systems into emergency preparedness protocols. Continuous innovation in healthcare technologies supports stable market expansion.

The Ebola market in China is growing. China is witnessing increasing demand for infectious disease surveillance and rapid molecular testing technologies. Healthcare institutions are strengthening laboratory preparedness capabilities for high-risk viral outbreaks. Domestic biotechnology companies are expanding vaccine research and biologics manufacturing activities. Clinical laboratories continue to adopt automated RT-PCR systems to improve testing efficiency. The market benefits from increasing integration of decentralized diagnostic infrastructure across urban healthcare systems. Growing healthcare modernization efforts continue supporting long-term market growth.

Latin America Ebola Market Trends

Latin America is gradually expanding its Ebola preparedness capabilities through improved diagnostic and surveillance infrastructure. Healthcare systems continue to emphasize rapid outbreak detection and efficient laboratory response. The market is witnessing increasing adoption of portable molecular testing technologies in urban healthcare centers. Hospitals and diagnostic laboratories are strengthening infectious disease management protocols. Pharmaceutical distributors are expanding regional access to vaccines and emergency therapeutics. Growing focus on healthcare preparedness supports moderate long-term market development.

The Brazil Ebola market leads the region in Ebola preparedness due to its large healthcare infrastructure. Diagnostic laboratories are increasingly adopting molecular testing technologies for emerging infectious disease applications. Healthcare institutions continue strengthening surveillance and outbreak response capabilities. Biotechnology research organizations are expanding infectious disease diagnostic development activities. Hospitals are integrating advanced laboratory systems within emergency preparedness frameworks. Continuous improvements in healthcare infrastructure support future market expansion.

Middle East & Africa Ebola Market Trends

Middle East & Africa represents a strategically important Ebola industry due to ongoing outbreak risks across several African countries. Healthcare organizations are strengthening decentralized diagnostic and surveillance capabilities across high-risk regions. The market is witnessing increasing deployment of portable RT-PCR systems and rapid diagnostic kits. Clinical adoption of Ebola vaccines and monoclonal antibody therapies continues expanding across treatment centers. Laboratory accessibility and infectious disease monitoring efficiency continue improving across the region. Rising emphasis on emergency response infrastructure supports continued market growth.

The Saudi Arabia Ebola market is growing. Saudi Arabia is strengthening infectious disease preparedness capabilities through advanced healthcare modernization initiatives. The country continues to expand its laboratory infrastructure focused on rapid viral detection technologies. Hospitals are increasingly integrating molecular diagnostic platforms within emergency response systems. Healthcare institutions emphasize surveillance readiness for imported infectious disease risks associated with international travel. Pharmaceutical distributors are strengthening access to advanced biologics and diagnostic solutions. Continuous improvements in clinical laboratory capabilities support gradual market expansion.

Key Ebola Company Insights

The Ebola market remains moderately consolidated, with a limited number of biotechnology, pharmaceutical, and diagnostic companies holding significant market shares due to the highly specialized nature of Ebola therapeutics and diagnostics. Merck & Co. maintains a leading market position through the commercial success of ERVEBO, while Regeneron Pharmaceuticals holds a strong competitive presence in monoclonal antibody therapeutics with Inmazeb. Johnson & Johnson continues to expand its vaccine portfolio through the Zabdeno/Mvabea regimen, strengthening its competitive positioning in preventive immunization. Diagnostic companies such as Cepheid, BioFire Diagnostics, and Altona Diagnostics maintain substantial market presence through advanced RT-PCR and molecular testing platforms. Market participants are prioritizing strategic collaborations, biologics innovation, manufacturing scalability, and global commercialization initiatives to strengthen outbreak response capabilities. Companies are also expanding infectious disease research partnerships, regional distribution networks, and next-generation biologics development strategies to improve the efficiency of rapid deployment and long-term competitive positioning in high-risk markets.

Key Ebola Companies

The following key companies have been profiled for this study on the ebola market.

-

Merck & Co.

-

Johnson & Johnson

-

Regeneron Pharmaceuticals

-

Ridgeback Biotherapeutics

-

Cepheid

-

altona Diagnostics

-

OraSure Technologies

-

BioFire Diagnostics

-

Bavarian Nordic

-

Gilead Sciences

Recent Developments

-

In January 2026, Merck and the Coalition for Epidemic Preparedness Innovations (CEPI) launched a USD 30 million partnership to develop a more affordable Ervebo Ebola vaccine. The initiative aimed to improve manufacturing efficiency, increase yield, simplify production, extend shelf life, and enable standard refrigeration storage globally.

-

In September 2025, Regeneron Pharmaceuticals announced that it had donated up to 500 doses of its Ebola treatment Inmazeb (atoltivimab, maftivimab, and odesivimab-ebgn) to the World Health Organization for use in low- and lower-middle income countries most at risk of outbreaks. The supply was also being urgently deployed to the Democratic Republic of Congo to support an ongoing outbreak response.

-

In September 2025, the National Institute of Biomedical Research (INRB) and Ridgeback Biotherapeutics responded to the 16th Ebola outbreak in the Democratic Republic of Congo after its declaration on 4 September 2025. The response involved deploying an emergency medical team within 4 days of the outbreak declaration and treating confirmed patients at Bulape General Hospital. As of the report date, 25 laboratory-confirmed cases had been identified, including 14 deaths, with patients presenting symptoms such as fever, vomiting, asthenia, and hemorrhage in Bulape and Mweka health zones in Kasai Province.

Ebola Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.2 billion

Estimated market size in 2026

USD 1.3 billion

Projected market size by 2033

USD 2.3 billion

Growth rate

CAGR of 8.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, trends

Segments covered

Type, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key company profiled

Merck & Co.; Johnson & Johnson; Regeneron Pharmaceuticals; Ridgeback Biotherapeutics; Cepheid; altona Diagnostics; OraSure Technologies; BioFire Diagnostics; Bavarian Nordic; Gilead Sciences

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Ebola Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global Ebola market report based on type and region:

-

Type Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Therapeutic

-

Product Type

-

Vaccine

-

ERVEBO

-

Zabdeno/Mvabea

-

-

Monoclonal Antibodies

-

Inmazeb

-

Ebanga

-

-

Supportive Care Therapies

-

-

Route of Administration

-

Intravenous (IV)

-

Intramuscular (IM)

-

Other

-

-

Procurement Channel

-

Public

-

Private

-

-

-

Diagnostic

-

Test Type

-

Molecular Diagnostic Tests

-

RT-PCR Molecular Diagnostic Tests

-

Real-Time RT-PCR Assays

-

Others

-

-

Rapid Diagnostic Tests

-

Immunodiagnostic Assays

-

Others

-

-

End Use

-

Hospitals & Clinics

-

Diagnostic Laboratories

-

Government & Public Health Agencies

-

Research Institutes

-

NGOs & International Health Organizations

-

-

-

-

Regional Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global ebola market size was valued at USD 1.2 billion in 2025 and is estimated at USD 1.3 billion for 2026.

North America dominated with a 40.9% revenue share in 2025.

Key factors include the increasing emphasis on outbreak preparedness, preventive immunization programs, and rapid-response healthcare infrastructure across high-risk regions.

The vaccine segment led with a 51.4% revenue share in 2025.

The intramuscular segment held the largest revenue share in 2025.

The public segment held the largest revenue share in 2025.

The molecular diagnostic tests segment held the largest revenue share in 2025.

The global ebola market is expected to grow at a CAGR of 8.3% from 2026 to 2033, reaching USD 2.3 billion by 2033.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Merck & Co.; Johnson & Johnson; Regeneron Pharmaceuticals; Ridgeback Biotherapeutics; Cepheid; altona Diagnostics; OraSure Technologies; BioFire Diagnostics; Bavarian Nordic; Gilead Sciences

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.