- Home

- »

- Biotechnology

- »

-

Flow Cytometry Market Size And Share Report, 2026-2033GVR Report cover

![Flow Cytometry Market (2026 - 2033)Report]()

Flow Cytometry Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Instruments, Reagents & Consumables, Software, Accessories, Services), By Technology, By Application (Industrial, Clinical, Cancer), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$5.1BMarket Estimate, 2026

$5.4BMarket Forecast, 2033

$8.2BCAGR, 2026–2033

6.0%Flow Cytometry Market Summary

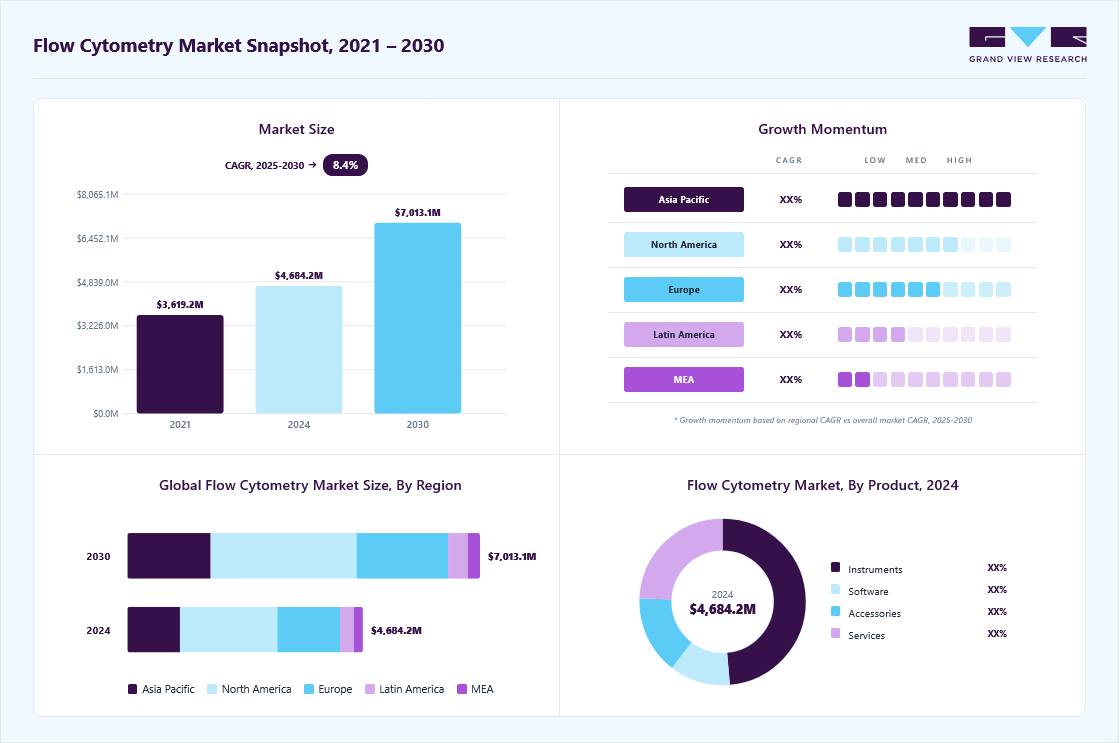

The global flow cytometry market size was valued at USD 5.1 billion in 2025 and is projected to grow from USD 5.4 billion in 2026 to USD 8.2 billion by 2033, at a CAGR of 6.0% from 2026 to 2033. North America dominated the global market with the largest revenue share of 41.0% in 2025. The increasing incidence of cancer, immunodeficiency disorders, and infectious diseases is a key factor propelling market growth.

Key Market Trends & Insights

- By product: Instrument segment led the market with the largest revenue share of 34.5% in 2025.

- By technology: Cell-based segment led the market with the largest revenue share of 72.6% in 2025.

- By application: Clinical segment led the market with the largest revenue share of 46.7% in 2025.

- By end-use: Academic institutes segment led the market with the largest revenue share of 30.3% in 2025.

Regional Highlights

- Largest regional market: North America (41.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The flow cytometry market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market size in 2025: USD 5.1 Billion

- Estimated market size in 2026: USD 5.4 Billion

- Projected market size by 2033: USD 8.2 Billion

- CAGR (2026-2033): 6.0%

In addition, extensive research and development investments in biotechnology, life science, and biopharmaceutical research have contributed to a leveraged demand for flow cytometry instruments. For instance, in February 2023, Cytek Biosciences announced its plan to acquire imaging and flow cytometry business from DiaSorin with an aim to expand its market share in international market.")

Flow cytometry plays a crucial role in diagnosing cancer and immunodeficiency diseases, and the increasing prevalence of these conditions is expected to drive market growth in the coming years. The adverse effects of chemotherapy and radiation therapy in cancer treatment have led physicians to favor autologous and allogeneic stem cell therapies, further boosting the demand for flow cytometry. According to the American Cancer Society, approximately 1.9 million new cancer cases were diagnosed in the U.S. in 2022, with nearly 600,000 deaths attributed to the disease. This rising burden underscores the need for advanced diagnostic tools like flow cytometry, which enables precise immune cell characterization and aids in treatment monitoring.

In addition to cancer diagnostics, flow cytometry is instrumental in identifying and characterizing immune cells in patients with Primary Immunodeficiency Diseases (PID). According to NCBI data from 2022, the global prevalence of PID ranges from 0.81 to 30.5 per 100,000 people. Technology is invaluable in detecting genetic defects associated with immune disorders and validating new genetic abnormalities. Moreover, flow cytometry is widely used to monitor immune responses following stem cell transplantation, making it an essential tool in organ transplantation procedures. The World Health Organization (WHO) estimates that approximately 50,000 stem cell transplants are performed globally each year, further driving the adoption of flow cytometry in clinical and research settings.

The increasing prevalence of hematological disorders is another major factor fueling the demand for flow cytometry. According to NCBI statistics, bleeding disorders affect approximately 1 in 1,000 individuals worldwide, with hemophilia A, hemophilia B, and Von Willebrand disease being the most common types. Flow cytometry provides critical insights into blood cell populations, aiding in the diagnosis and management of these conditions. Its ability to analyze complex cellular interactions in hematological malignancies and immune disorders has made it an indispensable tool in both diagnostic laboratories and research institutions. As the incidence of hematological and immune-related diseases continues to rise, the market for flow cytometry is expected to expand significantly.

Market Dynamics

The Flow Cytometry Market is witnessing significant growth driven by the rising burden of cancer, infectious diseases, autoimmune disorders, and hematological conditions that require accurate cellular characterization for diagnosis, prognosis, and treatment monitoring. Growing investments in precision medicine, immuno oncology research, and advanced cell-based therapies are increasing the adoption of flow cytometry technologies across clinical, academic, and biopharmaceutical settings. Market expansion is further supported by the increasing use of flow cytometry in drug discovery, biomarker validation, and immune response assessment, enabling researchers to generate detailed cellular data for research and clinical applications. In addition, technological advancements in spectral flow cytometry, automation, and analytical software are enhancing operational efficiency and expanding multiplexing capabilities. These innovations are encouraging manufacturers to introduce next generation platforms with improved performance and workflow integration. For instance, in May 2025, Cytek Biosciences advanced the commercialization of its full spectrum flow cytometry portfolio through the introduction of the Aurora Evo platform, designed to improve throughput, workflow automation, and data quality. These developments are contributing to broader technology adoption and supporting the continued expansion of the global Flow Cytometry Market.

The increasing adoption of immunotherapy and cell based research is driving growth in the Flow Cytometry Market. Flow cytometry plays a critical role in immune cell characterization, immunophenotyping, biomarker identification, and treatment response monitoring, making it an essential tool in oncology, immunology, and regenerative medicine research. The growing number of clinical trials focused on immune checkpoint inhibitors, CAR T cell therapies, and personalized treatment approaches is increasing demand for advanced flow cytometry platforms capable of analyzing complex cellular populations. Biopharmaceutical companies and research institutions are expanding investments in cell-based studies to accelerate therapeutic development and improve clinical outcomes. Furthermore, technology enables rapid and high content analysis of cellular responses, supporting drug discovery and translational research activities. The growing emphasis on next generation immune profiling technologies is further strengthening demand for advanced flow cytometry solutions across research and clinical settings. For instance, in March 2025, Beckman Coulter Life Sciences launched the CytoFLEX mosaic Spectral Detection Module, enabling full spectrum data acquisition across all lasers and supporting high parameter immune cell analysis for complex research applications. Such developments are strengthening the role of flow cytometry in advanced therapeutic research and supporting market growth.

The high cost associated with flow cytometry instruments, reagents, software, and laboratory infrastructure remains a key restraint for the flow cytometry market. Advanced systems equipped with spectral analysis, automated workflows, and high parameter detection capabilities require substantial capital investment, limiting adoption among small research laboratories, academic institutions, and healthcare facilities operating under budget constraints. In addition to acquisition costs, organizations must incur ongoing expenses related to maintenance contracts, calibration procedures, software upgrades, and specialized consumables. The operation of sophisticated flow cytometry platforms also requires trained personnel capable of handling instrument setup, data acquisition, and complex result interpretation. These factors can increase total ownership costs and create barriers to technology adoption, particularly in emerging markets. Industry participants continue to face challenges related to affordability and resource availability. Several academic research organizations reported growing pressure on laboratory budgets amid changing research funding environments, influencing purchasing decisions for high value analytical instruments. Such cost related constraints may limit broader market penetration across resource constrained settings.

The increasing integration of artificial intelligence and automated data analysis platforms presents a significant opportunity for the Flow Cytometry Market. Modern flow cytometry experiments generate large and complex datasets that require extensive analysis and interpretation. Artificial intelligence driven tools can improve workflow efficiency by automating data processing, identifying cellular populations, reducing analysis time, and enhancing result consistency. The adoption of these technologies is becoming increasingly important as researchers and clinical laboratories conduct high parameter and large-scale studies that generate millions of cellular events. Automated analytical solutions also help address workforce limitations by reducing dependence on highly specialized personnel for routine data evaluation tasks. As laboratories seek greater operational efficiency and standardized reporting capabilities, demand for intelligent software solutions is expected to increase. For instance, in March 2025, Thermo Fisher Scientific highlighted its Connect Platform strategy to improve laboratory data interoperability and create connected research environments that support advanced analytics, automation, and future AI enabled applications. These initiatives are expected to strengthen the foundation for automated data analysis across life science research workflows. Consequently, such developments are creating growth opportunities by improving accessibility, productivity, and scalability within flow cytometry applications.

Market Concentration & Characteristics

Market growth stage is high, and pace is accelerating. The market is characterized by a high degree of innovation owing to the rapid technological advancements. In addition, incorporation of automation and multi-processing technologies in flow cytometry are expected to have positive impact on its adoption during the forecast period.

The flow cytometry industry is experiencing rapid innovation, with advancements in spectral analysis, artificial intelligence-driven data processing, and microfluidic-based cytometry. These innovations enhance sensitivity, throughput, and automation, making the technology more accessible for clinical and research applications, including cancer diagnostics, immunology, and drug discovery. For instance, In October 2023, Sony Corporation launched the FP7000 spectral cell sorter, designed to facilitate high-speed, high parameter sorting with over 44 colors and streamlined workflows. This innovative system integrates patented spectral technology-based optics, advanced electronics, and fluidics.

Mergers and acquisitions in the flow cytometry industry are increasing as key players seek to expand their technological capabilities and market presence. Companies are acquiring firms specializing in advanced reagents, software, and automation solutions, enhancing product portfolios and strengthening their competitive edge in precision medicine and diagnostics.

Regulatory frameworks significantly influence the flow cytometry industry, ensuring product safety and efficacy. Compliance with FDA, CE, and other regulatory standards is essential for market entry. Stricter guidelines for clinical diagnostics, laboratory workflows, and data management impact product development, approval timelines, and adoption rates.

Continuous advancements in flow cytometry have led to the development of high-dimensional cytometers, single-cell analysis platforms, and AI-powered software solutions. Expanding product offerings to include multiplex assays, automated sample processing, and user-friendly interfaces is increasing adoption across research institutions, hospitals, and diagnostic laboratories worldwide.

The flow cytometry industry is expanding globally, with increasing adoption in emerging markets across Asia-Pacific, Latin America, and the Middle East. Government initiatives, growing healthcare infrastructure, and rising investment in biotechnology and clinical research are driving market penetration, making flow cytometry more accessible in developing regions.

Analyst Perspective

The flow cytometry market is positioned for sustained growth, supported by increasing demand for advanced cellular analysis across research, clinical diagnostics, immunology, and biopharmaceutical applications. The expanding adoption of immunotherapy, cell and gene therapies, and precision medicine is strengthening the need for high parameter flow cytometry technologies capable of delivering detailed cellular insights. Ongoing advancements in spectral flow cytometry, automation, and data analytics are improving workflow efficiency and expanding application areas. In addition, growing investments in life science research and translational medicine are accelerating technology adoption. Market participants that focus on innovation, software integration, and application expansion are expected to strengthen their competitive position over the forecast period.

Product Insights

Based on product, the instrument segment led the market with the largest revenue share of 34.5% in 2025 with owing to higher penetration driven by technological developments. For instance, in June 2023, BD announced launch of an automated instrument which is designed to prepare samples for clinical diagnostics through flow cytometry, enabling the smoother processing and workflow. The progress in technology, leading to cost-effectiveness, improved accuracy, and portability, is expected to pave the way for future growth opportunities. In addition, focus of companies for development and manufacturing of instruments with rapid turnaround time are also estimated to have positive impact on the growth of instrument segment during the forecast period.

The software segment is expected to witness at a significant CAGR during the forecast period. In flow cytometry, software plays a crucial role in controlling and acquiring data from cytometers, analyzing information, and offering statistical insights. In research applications, the software is employed for cell acquisition and data analysis, while in clinical diagnosis, it aids in disease diagnosis through the analysis of patients' samples. The broad spectrum of applications is anticipated to propel the market in years to come. In addition, the introduction of new products by key companies is identified as a significant factor that is expected to fuel the growth of this segment over the forecast period. For instance, in February 2023, Agilent announced launch of NovoCyte Flow Cytometer System Software which encompasses updated regulatory compliances for biopharmaceutical and pharmaceutical manufacturing.

Technology Insights

Based on technology, the cell-based segment led the market with the largest revenue share of 72.6% in 2025. This segment plays a pivotal role in drug discovery, allowing researchers to analyze physiological cell characteristics and extract valuable biological information. The increasing adoption of multi-parameter flow cytometry, particularly in rare cell analysis, is expected to further drive demand in the coming years. This advanced technology is widely utilized in clinical studies, facilitating the examination of various cell types, including tumor cells in peripheral blood, endothelial cells, tumor stem cells, and hematopoietic progenitor cells. Beyond cancer research, cell-based flow cytometry is integral in understanding disease mechanisms and target identification, providing essential insights for precision medicine and therapeutic development. As research in oncology, immunology, and regenerative medicine continues to advance, the demand for sophisticated cell-based assays is anticipated to grow significantly.

The bead-based assays segment is expected to grow at a exponential CAGR over the forecast period, driven by advancements in molecular engineering and monoclonal antibody production. These assays are particularly useful in infectious disease research, where they facilitate rapid and precise detection of pathogens and immune responses. Unlike traditional cell-based assays, bead-based flow cytometry offers advantages such as cost-efficiency, minimal sample requirements, and faster turnaround times, making it a preferred choice for high-throughput screening applications. The technology employs indirect or sandwich immunoassay formats to accurately assess antibody levels in biological fluids, enhancing diagnostic and research capabilities. With continuous improvements in fluorescent bead technologies, automation, and multiplexing capabilities, bead-based assays are becoming increasingly versatile, enabling researchers to conduct simultaneous detection of multiple analytes in a single test. As the demand for rapid and reliable diagnostic solutions rises, particularly in infectious disease management and vaccine development, the bead-based assays segment is expected to experience significant market expansion.

Application Insights

Based on applications, the clinical segment led the market with the largest revenue share of 46.7% in 2025, driven by expanding research and development (R&D) activities in cancer and infectious disease diagnostics, including ongoing efforts related to COVID-19. The increasing R&D investments in the biotechnology and pharmaceutical industries are creating a conducive environment for market expansion. Furthermore, strategic growth initiatives by key industry players and the introduction of innovative flow cytometry solutions for clinical applications are expected to fuel segment growth. For instance, in July 2023, Discovery Life Sciences launched novel flow cytometry clinical trial services, enhancing capabilities in genomics, proteomics, and molecular pathology. These advancements are strengthening the role of flow cytometry in clinical diagnostics, treatment monitoring, and personalized medicine, further propelling market demand.

The research segment is projected to grow at the fastest CAGR during the forecast period, due to the increasing adoption of flow cytometry in cell culture, disease research, and drug discovery. Over the years, flow cytometry has become an indispensable tool in biomedical research, enabling precise analysis of cell populations, immune responses, and disease mechanisms. The rising prevalence of cancer and hematologic disorders, along with the growing demand for novel therapies, has significantly increased the need for flow cytometry in preclinical and translational research. In addition, surging R&D investments in the pharmaceutical and biotechnology sectors are fostering innovation, driving further adoption of advanced flow cytometry techniques in drug development, immunology, and regenerative medicine. As the demand for high-throughput, high-resolution cellular analysis grows, the research segment is set to experience significant expansion in the coming years.

End-use Insights

Based on end-use, the academic institutes segment led the market with the largest revenue share of 30.3% in 2025, driven by the extensive use of flow cytometry in cell biology and molecular diagnostics. This technology enables researchers to assess various cellular parameters, including physical properties, biomarker identification, and cell lineage determination using specific antibodies. It plays a crucial role in analyzing cell type, maturation stage, and functional characteristics, making it an essential tool in fields such as molecular biology, immunology, pathology, plant biology, and marine biology. With increasing emphasis on research and development activities, the segment is expected to witness significant growth over the forecast period, further solidifying the role of flow cytometry in academic and scientific research.

The clinical testing labs segment is projected to grow at the fastest CAGR during the forecast period, fueled by the rising demand for cost-effective diagnostic solutions for diseases like cancer and immunodeficiency disorders. Flow cytometry is widely utilized in clinical diagnostics, treatment monitoring, and therapeutic decision-making, particularly in oncology and immunology. The market’s expansion is also supported by an increasing number of industrial collaborations and strategic partnerships, aimed at improving accessibility to advanced flow cytometry services. For instance, in May 2023, BD India partnered with Sehgal Path Lab to establish a clinical flow cytometry center in Mumbai, enhancing diagnostic capabilities and expanding the reach of high-precision cellular analysis. These developments underscore the growing role of flow cytometry in clinical laboratories, further driving market growth.

Regional Insights

North America dominated the flow cytometry market with the largest revenue share of 41.0% in 2025. This strong market position is driven by the presence of a highly advanced healthcare system and a thriving pharmaceutical and biotechnology industry, particularly in the United States. The growing demand for flow cytometry solutions in clinical diagnostics, drug discovery, and biomedical research has significantly contributed to market expansion. Moreover, substantial R&D investments in oncology, immunology, and infectious diseases have further fueled the demand for flow cytometry instruments. Increased public-private partnerships supporting cancer research have played a pivotal role in boosting market growth. For example, in December 2023, AlleSense was commissioned to enhance cancer diagnostics using cutting-edge flow cytometry technologies, receiving an initial investment of USD 2.5 million.

U.S. Flow Cytometry Market Trends

The flow cytometry market in the U.S. held the largest share in the North America region in 2025, driven by high cancer prevalence and extensive R&D initiatives aimed at developing novel therapies. The government's proactive funding initiatives and regulatory support for next-generation diagnostic technologies have created lucrative market opportunities. The adoption of automated flow cytometry platforms in clinical laboratories and hospitals is expected to further strengthen market expansion.

Europe Flow Cytometry Market Trends

The flow cytometry market in Europe is witnessing significant growth, largely due to rising demand in countries with strong biotechnology sectors, including Germany, the UK, and Italy. The COVID-19 pandemic also accelerated the adoption of flow cytometry technologies, as countries like Italy, France, the UK, and Germany ramped up vaccine development and infectious disease research. This trend has reinforced demand for high-throughput flow cytometry solutions across the region.

The UK flow cytometry market is expanding due to strategic collaborations between government bodies and private players, leading to the launch of innovative products. These partnerships are fostering the adoption of flow cytometry in clinical and research settings, boosting market penetration.

The flow cytometry market in France is projected to grow at a steady CAGR from 2026 to 2033, driven by the increasing acceptance of flow cytometry in academic and research institutions. In addition, artificial intelligence (AI) integration into flow cytometry workflows is expected to enhance automation and efficiency, driving further adoption.

The Germany flow cytometry market is set for substantial growth due to the strong presence of key players and their continuous strategic initiatives. The country’s leading role in pharmaceutical R&D, particularly in vaccine development during the COVID-19 pandemic, has led to a sustained demand for flow cytometry solutions in both clinical and research applications.

Asia Pacific Flow Cytometry Market Trends

The flow cytometry market in the Asia Pacific is expected to witness at a significant CAGR from 2026 to 2033, fueled by the expanding pharmaceutical and biotechnology sectors in emerging economies such as China and India. The rising burden of chronic diseases and the increasing use of flow cytometry devices in oncology, immunology, and infectious disease diagnostics are key growth drivers. Furthermore, continuous innovations in cancer and infectious disease research are expected to accelerate market expansion across the region.

The China flow cytometry market is expected to grow at a substantial CAGR from 2026 to 2033, as leading companies adopt both organic and inorganic growth strategies to maintain a competitive edge. Increasing government-funded R&D initiatives in precision medicine and immunotherapy are projected to drive demand for advanced flow cytometry instruments and reagents.

The flow cytometry market in Japan accounted for the largest market revenue share in Asia Pacific in 2025, primarily due to its strong R&D focus and continuous introduction of new technologies in flow cytometry applications. With increasing government and private investments in biomedical research, the demand for high-throughput flow cytometry solutions is rising across research institutions and pharmaceutical companies.

Latin America Flow Cytometry Market Trends

The flow cytometry market in Latin America is estimated to grow at a notable CAGR from 2026 to 2033, driven by rising public-private partnerships that support biomedical research and diagnostic advancements. The region’s aging population and increasing prevalence of chronic diseases are also contributing to market expansion.

The Brazil flow cytometry market is witnessing growth due to increased private and public investments in the pharmaceutical and biotechnology sectors. The country’s emphasis on expanding research infrastructure and enhancing diagnostic capabilities further supporting the demand for advanced flow cytometry solutions.

Middle East and Africa Flow Cytometry Market Trends

The flow cytometry market in the MEA is projected to grow at a steady CAGR from 2026 to 2033. However, factors such as limited investments in biotechnology, high costs of flow cytometry systems, and fewer R&D activities in the pharmaceutical and biotech industries may restrict market expansion. Despite these challenges, growing healthcare infrastructure and increased demand for localized testing are driving moderate growth.

The Saudi Arabia flow cytometry market is expected to grow at a significant CAGR over the forecast period, driven by an increasing prevalence of chronic diseases, rising demand for advanced diagnostic tools, and falling sequencing costs. As government and private sector investments in healthcare and research expand, the adoption of flow cytometry solutions in clinical laboratories and research institutions is expected to rise steadily.

Key Flow Cytometry Company Insights

Established players in the flow cytometry industry such as Danaher; BD; Sysmex Corp.; Agilent Technologies, Inc.; Apogee Flow Systems Ltd.; Bio-Rad Laboratories, Inc.; Thermo Fisher Scientific, Inc.; Stratedigm, Inc.; Miltenyi Biotec; Cytek Biosciences; Sony Group Corporation (Sony Biotechnology Inc.) are strategically positioning themselves for sustained growth. Their activities include continuous research and development initiatives, strategic partnerships and acquisitions, and a focus on expanding their product portfolios. By leveraging their experience and market presence, these players aim to maintain leadership positions and adapt to evolving industry trends in the competitive landscape of flow cytometry.

In the flow cytometry industry, emerging players are actively engaging in strategic activities to establish their presence. These activities include innovative product development, strategic collaborations, and market expansions. By focusing on such strategies, these players aim to capitalize on the growing demand for flow cytometry solutions.

Key Flow Cytometry Companies:

The following key companies have been profiled for this study on the flow cytometry market.

-

Danaher

-

BD

-

Sysmex Corporation

-

Agilent Technologies, Inc.

-

Apogee Flow Systems Ltd.

-

Bio-Rad Laboratories, Inc.

-

Thermo Fisher Scientific, Inc.

-

Stratedigm, Inc.

-

Miltenyi Biotec

-

Cytek Biosciences

-

Sony Group Corporation (Sony Biotechnology Inc.)

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Danaher, BD, Sysmex Corporation, Agilent Technologies, Bio-Rad Laboratories, Thermo Fisher Scientific, Miltenyi Biotec, Sony Biotechnology)

- Expand flow cytometry portfolios through continuous investments in spectral flow cytometry, cell sorting technologies, automation, software analytics, and high parameter cell analysis. Strengthen market position through product launches, acquisitions, strategic collaborations, and expansion of research and clinical applications. Enhance global distribution networks and integrated solutions spanning instruments, reagents, software, and services across academic institutes, hospitals, biopharmaceutical companies, and clinical laboratories.

- Strong brand recognition and established customer relationships across research and clinical settings. Broad product portfolios covering flow cytometers, cell sorters, reagents, consumables, software, and support services. Extensive global commercial infrastructure, regulatory expertise, and financial resources that support product innovation and market expansion.

- High operational and research expenditures associated with developing advanced flow cytometry platforms. Intense competition requiring continuous technological innovation and product differentiation. Dependence on research funding, capital equipment budgets, and regulatory requirements that may influence purchasing decisions.

Emerging Players (Cytek Biosciences, Apogee Flow Systems, Stratedigm)

- Focus on specialized segments including spectral flow cytometry, small particle analysis, extracellular vesicle research, and high sensitivity cell analysis. Develop differentiated technologies that address evolving research requirements and complex cellular profiling applications. Expand market presence through strategic partnerships, distributor networks, technology innovation, and targeted commercialization initiatives within academic and biotechnology research environments.

- Strong focus on innovation and rapid adoption of emerging flow cytometry technologies. Greater operational flexibility and ability to address specialized research requirements. Expertise in niche applications such as spectral flow cytometry, nanoparticle detection, and advanced multiparametric cellular analysis.

- Limited global reach and lower brand recognition compared with established industry leaders. Dependence on successful commercialization, distributor expansion, and continued technology adoption for growth. Challenges associated with scaling manufacturing capacity, expanding service infrastructure, and competing against diversified market participants with broader product portfolios.

Recent Developments

-

In January 2025, BD (Becton, Dickinson and Company) and Biosero, a developer of laboratory automation solutions, announced a collaboration to integrate robotic arms with BD's flow cytometry instruments. This partnership aims to automate manual processes in drug discovery and development, enhancing efficiency and throughput in laboratory workflows.

-

In March 2024, Beckman Coulter Life Sciences received 510(k) clearance from the FDA to distribute its DxFLEX Clinical Flow Cytometer in the U.S. This advancement makes high-complexity flow cytometry testing more accessible to laboratories without the need for additional expense.

-

In January 2024, Cytek Biosciences, Inc. agreed with the Centre for Genomic Regulation (CRG) and Pompeu Fabra University (UPF) to foster technological innovation and accelerate discoveries in the scientific community. The collaboration underscores the significant impact of Cytek's spectral flow cytometry technology, paving the way for expansion into new applications.

Flow Cytometry Market Report Scope

Report Attribute

Details

Market size in 2025

USD 5.1 billion

Estimated Market Size in 2026

USD 5.4 billion

Projected Market Size by 2033

USD 8.2 billion

Growth rate

CAGR of 6.0% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, technology, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

Danaher, BD, Sysmex Corporation, Agilent Technologies, Inc., Apogee Flow Systems Ltd., Bio-Rad Laboratories, Inc., Thermo Fisher Scientific, Inc., Stratedigm, Inc., Miltenyi Biotec, Cytek Biosciences, Sony Group Corporation (Sony Biotechnology Inc.).

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Flow Cytometry Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global flow cytometry market report based on product, technology, application, end-use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Instruments

-

Cell Analyzers

-

Cell Sorters

-

-

Reagents & Consumables

-

Software

-

Accessories

-

Services

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Cell-based

-

Bead-based

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Research

-

Pharmaceutical

-

Drug Discovery

-

Stem Cell

-

In Vitro Toxicity

-

-

Apoptosis

-

Cell Sorting

-

Cell Cycle Analysis

-

Immunology

-

Cell Viability

-

Others

-

-

Industrial

-

Clinical

-

Cancer

-

Organ Transplantation

-

Immunodeficiency

-

Hematology

-

Autoimmune Disorders

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercial Organizations

-

Biotechnology Companies

-

Pharmaceutical Companies

-

CROs

-

-

Hospitals

-

Academic Institutes

-

Clinical Testing Labs

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

Segment Definition

Segment - Product

Revenue capture definition

Instruments

Revenue is primarily captured through the sale of sepsis diagnostic analyzers, molecular testing systems, blood culture instruments, and automated microbiology platforms used for pathogen detection, antimicrobial susceptibility testing, and clinical decision support in hospital and laboratory settings.

Reagents & Consumables

Revenue flows from recurring purchases of assay kits, blood culture media, molecular test cartridges, reagents, controls, calibrators, sample preparation materials, and other consumables required for routine sepsis screening, pathogen identification, and biomarker analysis.

Software

Revenue is captured through licensing and subscription based software solutions that support diagnostic data management, result interpretation, laboratory workflow optimization, antimicrobial stewardship programs, clinical reporting, and integration with hospital information systems.

Accessories

Revenue originates from supporting components and ancillary products including sample handling devices, incubation modules, barcode systems, specimen collection accessories, connectivity hardware, and instrument enhancement products used alongside sepsis diagnostic platforms.

Services

Revenue flows from installation, validation, maintenance, calibration, technical support, operator training, consulting, software upgrades, and service agreements that ensure regulatory compliance, optimal instrument performance, and uninterrupted

Segment - Technology

Revenue capture definition

Cell-based

Revenue is primarily captured from flow cytometry systems, reagents, assay kits, software, and related services used for the analysis, characterization, sorting, and quantification of intact cells in applications including immunophenotyping, cell viability assessment, cancer research, stem cell studies, and clinical diagnostics.

Bead-based

Revenue flows from bead-based flow cytometry assays, multiplex testing kits, calibration beads, quality control materials, and associated analytical solutions used for protein quantification, cytokine profiling, biomarker detection, and multiplexed sample analysis in research and diagnostic laboratories.

Segment - Application

Revenue capture definition

Research

Revenue is primarily captured from flow cytometry instruments, reagents, software, and services utilized in basic research, pharmaceutical development, cell biology studies, immunology investigations, and translational research activities conducted by academic and research institutions.

Industrial

Revenue flows from flow cytometry solutions deployed in industrial applications including biotechnology manufacturing, bioprocess monitoring, quality assurance, environmental testing, food safety assessment, and microbial analysis across commercial production environments.

Clinical

Revenue is captured through the use of flow cytometry platforms, assays, consumables, and associated services for disease diagnosis, prognosis, treatment monitoring, and patient management across hospitals, diagnostic laboratories, and specialized clinical settings.

Segment - End-Use

Revenue capture definition

Commercial Organizations

Revenue is primarily captured from the procurement of flow cytometry instruments, reagents, software, and related services by biotechnology companies, pharmaceutical companies, and contract research organizations for drug discovery, cell therapy development, biomarker research, and clinical trial activities.

Hospitals

Revenue flows from the adoption of flow cytometry systems, diagnostic assays, consumables, and support services used for disease diagnosis, treatment monitoring, immunophenotyping, transplantation testing, and routine clinical laboratory operations.

Academic Institutes

Revenue is captured through purchases of flow cytometry platforms, research reagents, analytical software, and training services utilized in basic research, translational studies, life science investigations, and educational programs conducted by universities and research centers.

Clinical Testing Labs

Revenue originates from investments in flow cytometry instruments, testing reagents, data management solutions, an

Estimation Model

The Flow Cytometry Market size was estimated using a bottom up approach that involved identifying key manufacturers, benchmarking their flow cytometry product portfolios, and assessing revenues generated from relevant instruments, reagents, software, and services. Market revenues were further segmented by technology based on adoption rates and application trends, followed by aggregation of segment level estimates and validation through market share analysis of leading industry participants to derive the overall market size.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Flow Cytometry Technology Adoption Analysis

Assessment of adoption trends across conventional, spectral, and imaging flow cytometry technologies, including utilization patterns across research, clinical, and biopharmaceutical applications.

Helps identify high growth technology segments and investment opportunities across evolving cellular analysis workflows.

Cell and Gene Therapy Research Landscape Assessment

Analysis of flow cytometry utilization in immunotherapy, CAR T cell development, stem cell research, regenerative medicine, and immune profiling applications.

Supports opportunity identification across advanced therapeutic development and precision medicine initiatives.

Clinical and Diagnostic Application Evaluation

Evaluation of flow cytometry adoption across oncology, hematology, immunodeficiency disorders, autoimmune diseases, transplantation monitoring, and infectious disease diagnostics.

Tracks emerging clinical demand areas and supports strategic expansion into high value diagnostic applications.

Spectral Flow Cytometry and Innovation Landscape

Assessment of advancements in spectral flow cytometry, automation, artificial intelligence enabled analytics, high parameter cell analysis, and next generation software platforms.

Identifies future innovation opportunities, competitive differentiation factors, and technology driven growth areas.

Competitive Benchmarking and Product Portfolio Analysis

Comparative assessment of instrument capabilities, spectral technologies, cell sorting platforms, software solutions, and strategic initiatives of leading market participants.

Supports competitive intelligence, partnership evaluation, and market positioning decisions.

Frequently Asked Questions About This Report

The global flow cytometry market size was estimated at USD 5.1 billion in 2025 and is expected to reach USD 5.4 billion in 2026.

The global flow cytometry market is expected to grow at a compound annual growth rate of 6.0% from 2026 to 2033 to reach USD 8.2 billion by 2033.

Some key players operating in the flow cytometry market include Danaher, BD, Sysmex Corp., Agilent Technologies, Inc., Apogee Flow Systems Ltd., Bio-Rad Laboratories, Inc., Thermo Fisher Scientific, Inc., Stratedigm, Inc., DiaSorin S.p.A., Miltenyi Biotec, Sony Biotechnology, Inc.

Key factors driving the flow cytometry market growth include the rising R&D investments in the biotechnology sector and technological advancements in the field of flow cytometry for introducing new and improved analytical tools, such as microfluidic flow cytometry, for point-of-care testing.

North America dominated the flow cytometry market with the largest revenue share of 41.0% in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Cell-based segment led the market with the largest revenue share of 72.6% in 2025.

Instrument segment led the market with the largest revenue share of 34.5% in 2025.

Clinical segment led the market with the largest revenue share of 46.7% in 2025.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.