- Home

- »

- Pharmaceuticals

- »

-

Inhaler Solution Market Size And Share Report, 2026-2033GVR Report cover

![Inhaler Solution Market (2026 - 2033)Report]()

Inhaler Solution Market (2026 - 2033)

Size, Share & Trends Analysis Report By Inhaler Type (Pressurized Metered-Dose Inhalers (pMDIs), Dry-Powder Inhalers (DPIs)), By Drug Class, By Application, By Distribution Channel, By Region, And Segment Forecasts

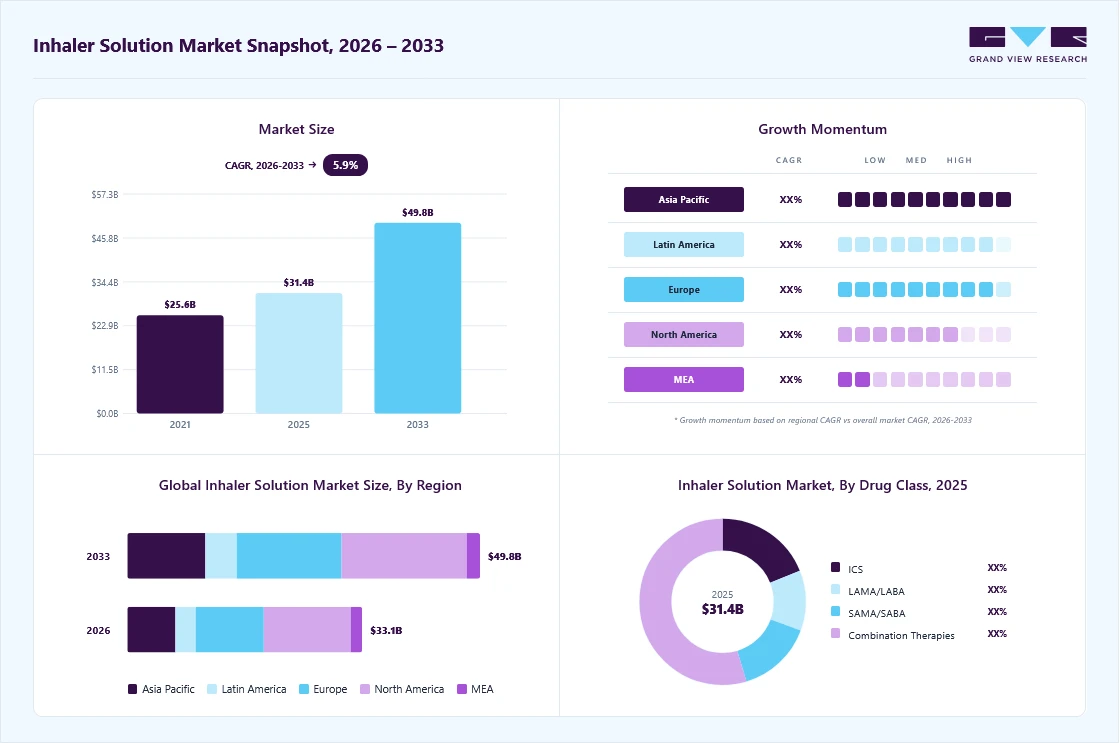

Market Size, 2025

$31.4BMarket Estimate, 2026

$33.1BMarket Forecast, 2033

$49.8BCAGR, 2026–2033

5.9%Inhaler Solution Market Summary

The global inhaler solution market size was valued at USD 31.4 billion in 2025 and is projected to grow from USD 33.1 billion in 2026 to USD 49.8 billion by 2033, at a CAGR of 5.9% from 2026 to 2033. The market in North America dominated with a revenue share of 37.3% in 2025. This growth is primarily driven by the rising prevalence of respiratory disorders such as asthma and chronic obstructive pulmonary disease, increasing exposure to air pollution and tobacco smoke, and growing awareness of early diagnosis and long-term disease management.

Key Market Trends & Insights

- By inhaler type: Pressurized metered-dose inhalers (pMDIs) segment held the largest market share of 51.1% in 2025.

- By drug class: Combination therapies segment held the largest market share of 54.7% in 2025.

- By application: Asthma segment held the largest market share of 53.1% in 2025.

- By distribution channel: Retail pharmacies segment held the largest market share of 49.5% in 2025.

Regional Highlights

- Largest regional market: North America (37.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 31.4 Billion

- Estimated market size in 2026: USD 33.1 Billion

- Projected market size by 2033: USD 49.8 Billion

- CAGR (2026-2033): 5.9%

The growing global prevalence of chronic respiratory diseases, particularly asthma and Chronic Obstructive Pulmonary Disease (COPD), continues to be a primary driver for the inhaler solutions market. According to the World Health Organization (WHO), asthma affects over 262 million people worldwide, and COPD remains the third leading cause of death globally, responsible for millions of lives lost each year. This rising disease burden is not only a global health challenge but also a significant factor in driving the demand for inhaler therapies. Environmental factors, such as increasing urbanization and air pollution, exacerbate these respiratory conditions, creating a more urgent need for inhaler-based treatments. In Southeast Asia, where rapid industrialization and pollution are prevalent, the prevalence of asthma and COPD is increasing, as highlighted by a BMC Public Health study in February 2024. The study shows a clear correlation between environmental pollution and worsening respiratory diseases in the region.These respiratory diseases require ongoing management and are typically treated with inhalers that deliver medication directly to the lungs, making them the preferred method of treatment. As global air quality deteriorates, particularly in densely populated urban areas, the number of patients requiring inhalers grows. In addition, the increasing number of elderly populations, who are more susceptible to chronic respiratory diseases, adds further strain on healthcare systems, pushing up the demand for effective inhaler solutions. According to the WHO, the global aging population is expected to rise dramatically, leading to a corresponding increase in the number of patients suffering from respiratory diseases. The increase in disease prevalence directly correlates with greater market demand, as more patients require chronic disease management and effective symptom control.

")

Improved access to essential medicines and health products is becoming a significant factor supporting the growth of the inhaler solution market, especially in low and middle income countries (LMICs). In July 2025, a report by the Office of the United Nations High Commissioner for Human Rights (OHCHR) underlines that access to medicines remains far from universal: as of 2025, about two billion people worldwide still lack consistent access to essential medicines and health products. The report emphasizes that improving availability, affordability, and distribution of essential medicines including those for chronic diseases such as asthma and COPD is critical.

More specifically, a 2023 study published in the journal related to global health equity noted that although many respiratory medicines including inhaled therapies are listed on the World Health Organization (WHO) Essential Medicines List (EML), their availability and affordability in LMICs remain inconsistent. This indicates that in many underserved regions, prior constraints on access to inhalation therapy are starting to ease, driven by policy emphasis on essential medicines, improvements in supply chain and distribution frameworks, and increased public health prioritization of non-communicable diseases (NCDs).

As access improves both in terms of presence of inhaler drugs/devices in national essential medicines lists and their distribution through public health infrastructure, a larger portion of the population becomes eligible for and capable of using inhaler therapies for asthma and COPD. This expands the addressable market for inhaler devices beyond traditional high income geographies and supports greater market penetration in emerging regions. Such expansion, when combined with rising disease burden and device diversification, strengthens the long term growth potential for inhaler solution providers globally.

Market Concentration & Characteristics

The inhaler solution market shows a high degree of innovation driven by continuous improvements in drug formulations and delivery devices. Companies invest in enhanced aerosol performance to improve lung deposition and therapeutic efficacy. Development of combination therapies supports better symptom control and patient outcomes. Digital enabled inhalers are gaining attention for monitoring adherence and usage patterns. Patient centric design focuses on ease of use and reduced dosing errors. Lifecycle management through reformulations sustains product differentiation. Innovation remains essential for maintaining competitive positioning.

The market has moderate to high barriers to entry due to complex formulation and device integration requirements. Development of inhaler solutions demands specialized expertise in aerosol science. High costs associated with clinical trials limit participation by smaller firms. Manufacturing requires precision engineering and strict quality control. Brand loyalty toward established inhaler products restricts rapid market penetration. Distribution access through pharmacies and hospitals presents additional challenges. These factors favor established players with strong capabilities.

Regulatory oversight strongly influences the inhaler solution market through strict quality and safety requirements. Approval processes require comprehensive clinical and device performance data. Consistency in dose delivery and inhaler reliability receives close evaluation. Post approval surveillance focuses on long term safety and product performance. Labeling standards emphasize correct usage instructions and patient safety. Compliance costs affect development timelines and pricing strategies. Regulations shape product design and market entry decisions.

Product substitutes in the inhaler solution market remain limited due to the effectiveness of direct pulmonary drug delivery. Oral and injectable therapies exist for respiratory conditions, but offer a slower onset of action. Nebulizers serve as alternatives in severe cases or for pediatric use. Systemic therapies increase the risk of side effects compared to inhaled treatments. Patient preference favors inhalers for convenience and portability. Substitutes exert moderate competitive pressure. Inhalers remain central to long term respiratory management.

Geographical expansion is a key characteristic of the inhaler solution market as companies seek new patient populations. Emerging regions offer growth potential due to rising respiratory disease prevalence. Urbanization and pollution trends increase demand for inhaler therapies. Expansion strategies focus on strengthening distribution networks. Localization of manufacturing supports cost efficiency and supply stability. Partnerships with regional players improve market access. Global expansion enhances revenue diversification and long term growth.

Inhaler Type Insights

The pressurized metered-dose inhalers (pMDIs) segment dominated the market with the largest revenue share of 51.1% in 2025, driven by the treatment of asthma and chronic obstructive pulmonary disease (COPD). A significant driver for the continued use and growth of pMDIs is their proven effectiveness in delivering precise doses of medication, which is essential for managing chronic respiratory conditions. The increasing global prevalence of asthma and COPD, especially in emerging markets, is further fueling the demand for pMDIs. According to the World Health Organization (WHO),published data in October 2024, the global prevalence of asthma is expected to rise over the next decade, driving demand for effective inhalation therapies such as pMDIs., Asthma is also included in the WHO Global Action Plan for the prevention and control of NCDS and the United Nations 2030 Agenda for Sustainable Development.

The Soft Mist Inhalers (SMIs) segment is projected to grow at the fastest CAGR of 14.3% over the forecast period, due to gained significance as part of the broader shift toward propellant‑free inhalation options, motivated by environmental, clinical, and usability considerations. SMIs generate a slow cloud of aerosol from liquid formulations using mechanical energy eliminating the need for propellants while improving drug delivery efficiency and reducing coordination demands on patients. According to a review published in July 2023, SMIs enable slower, longer aerosol release with lower velocity, resulting in higher lung deposition and less loss in the oropharyngeal region compared with traditional inhalers. As awareness of healthcare’s environmental impact grows, SMIs are increasingly viewed as a viable alternative to propellant‑based devices.

Drug Class Insights

The combination therapies segment dominated the market with the largest revenue share of 54.7% in 2025, driven by strong clinical efficacy and its widespread use in managing moderate to severe chronic obstructive pulmonary disease. ICS/LAMA/LABA combination therapies represent a key treatment option for patients who continue to experience persistent symptoms or frequent exacerbations despite dual therapy. A post hoc analysis of the KRONOS study published in May 2025 demonstrated that ICS/LAMA/LABA therapy, specifically budesonide, glycopyrronium, and formoterol, led to significant improvements in lung function, as measured by FEV₁, and reduced moderate to severe exacerbations compared with ICS/LABA therapy. These outcomes underscore the therapeutic advantage of triple therapy and support its high adoption across clinical settings. However, safety considerations continue to influence treatment decisions. A 2024 systematic review published in SAGE Open Medicine reported that while triple therapy improved quality of life and reduced exacerbations, it was associated with a higher risk of pneumonia compared with dual LAMA/LABA therapy, highlighting the importance of careful patient selection and risk benefit assessment.

The LAMA/LABA segment is projected to grow at the fastest CAGR of 10.8% over the forecast period. The growth is supported by its expanding role in managing chronic obstructive pulmonary disease and asthma. LAMA/LABA combination therapies provide synergistic bronchodilation by targeting multiple pathways involved in bronchoconstriction, resulting in improved lung function and fewer exacerbations, particularly among patients with moderate to severe COPD. According to a 2025 review of COPD pharmacotherapy and treatment guidelines, LABA/LAMA combinations are increasingly recommended as first line therapy for patients with a high symptom burden, underscoring their importance in contemporary respiratory care. Clinical and real world evidence further supports this growth. A study published in May 2025 found no significant differences in severe exacerbations, mortality, or pneumonia risk across different inhaler devices used for LABA/LAMA fixed dose combinations, enhancing their flexibility and acceptance in routine practice. Moreover, a 2023 to 2024 observational analysis published in October 2024 highlighted a shift toward fixed dose dual or single inhaler therapies, simplifying treatment regimens, improving adherence, and strengthening adoption of LAMA/LABA products.

Application Insights

The asthma segment dominated the market with the largest revenue share of 53.1% in 2025. The segment’s growth is reflecting its position as the most established and widely treated application for inhaler solutions. Asthma represents a substantial global disease burden, with more than 300 million people affected worldwide, according to the Global Initiative for Asthma in May 2024, and prevalence continuing to rise due to air pollution, urbanization, and lifestyle changes. Inhaler solutions, particularly inhaled corticosteroids and combination therapies such as ICS and LABA, form the cornerstone of long-term asthma management. Clinical evidence strongly supports their use, with a study published in August 2025 in The Lancet Respiratory Medicine identifying ICS based therapies as the most effective approach for reducing exacerbations and improving quality of life. Further reinforcing this trend, an analysis published in JAMA in October 2024 found that combination therapies were more effective than monotherapies in lowering asthma related hospitalizations and enhancing lung function, highlighting the critical role of inhalers and treatment adherence in driving the market’s growth.

The cystic fibrosis segment is projected to grow at the second fastest CAGR of 9.0% over the forecast period. This growth is primarily driven by the critical role of inhaled therapies in managing chronic respiratory complications associated with the disease. Cystic fibrosis patients experience persistent lung infections and excessive mucus accumulation, making inhaler and nebulized solutions essential for delivering antibiotics, mucolytics, and airway clearance treatments directly to the lungs. Established inhaled antibiotics such as aztreonam lysine and tobramycin are widely used to manage chronic Pseudomonas aeruginosa infections, with clinical trials demonstrating significant improvements in lung function, reduced bacterial load, and better respiratory symptoms following structured treatment cycles. Long term observational data from cystic fibrosis registries further indicate improved survival outcomes among patients receiving chronic inhaled tobramycin therapy. In addition to these established treatments, ongoing research is expanding the therapeutic landscape, with studies highlighting advanced inhalation delivery systems and emerging gene targeted approaches, including inhalable lipid or nanoparticle based platforms, which are expected to support sustained market growth over the forecast period.

Distribution Channel Insights

The retail pharmacies segment held the largest revenue share in the inhaler solution market in 2025, accounting for 49.5% of the total, supported by their widespread accessibility and expanding role in patient education and disease management. Retail pharmacies serve as a primary point of care for asthma and chronic obstructive pulmonary disease patients, directly influencing treatment adherence and outcomes. Evidence from an interventional study published in June 2024 in Patient Preference and Adherence showed that structured pharmacist led counselling during inhaler dispensing, including device demonstrations and educational materials, led to a statistically significant improvement in inhaler adherence and correct usage, along with better disease control measured by the Asthma Control Test and COPD Assessment Test. Further reinforcing this impact, a study conducted in Belgium found that many patients made critical inhaler technique errors in the absence of pharmacist counselling. In contrast, structured community pharmacist interventions improved correct inhaler use rates by 23 to 37 percent, depending on the device. These factors collectively strengthen the dominance of retail pharmacies in the inhaler solution market.

The online pharmacies segment is projected to grow at the fastest CAGR of 11.3% over the forecast period, driven by the rapid expansion of digital healthcare platforms and changing patient preferences for convenient access to chronic disease medications. The online or e pharmacy channel for inhalers has gained traction alongside the wider adoption of telemedicine since the COVID-19 pandemic. A February 2025 commentary published in eClinicalMedicine highlighted the growing shift toward online pharmacies and digital prescription services, reflecting increased patient reliance on remote healthcare solutions. Supporting this trend, an April 2023 study evaluating telepharmacy and remote medication counselling reported high adherence rates of 85.4 percent and strong patient satisfaction, indicating that virtual pharmacy services such as remote counselling, digital medication reviews, and automated reminders can effectively support long term inhaler therapy. These services help overcome barriers related to geography, mobility, and convenience, particularly for chronic respiratory conditions. However, concerns around counterfeit products, regulatory oversight, and data privacy remain, positioning online pharmacies as a complementary distribution channel rather than a complete replacement for traditional pharmacy-based inhaler delivery.

Regional Insights

North America inhaler solution marketheld the largest share in 2025, accounting for 37.30% of global revenue, due to a high prevalence of asthma and chronic obstructive pulmonary disease across adult and pediatric populations. Strong clinical adoption of advanced inhaler therapies supports consistent prescription volumes. High awareness of early diagnosis and long-term disease management improves treatment continuity. Widespread availability of branded and combination inhaler solutions strengthens market penetration. Rapid uptake of smart inhalers and patient friendly delivery devices enhances adherence. A mature healthcare infrastructure supports sustained demand across retail and hospital channels.

U.S. Inhaler Solution Market Trends

Inhaler solution market in the U.S. benefits from a large diagnosed respiratory patient pool and high treatment rates. Physicians favor evidence based inhaler therapies aligned with updated clinical guidelines. Strong presence of leading pharmaceutical companies ensures rapid product availability. High adoption of combination therapies supports premium pricing and revenue growth. Digital health integration improves monitoring and adherence outcomes. Broad insurance coverage for respiratory therapies supports long term market stability.

Europe Inhaler Solution Market Trends

Europe represents a well-established inhaler solution market driven by rising respiratory disease burden and aging populations. Clinical preference for maintenance inhaler therapy supports steady prescription volumes. Strong emphasis on preventive care improves early initiation of inhaler treatment. Adoption of dry powder and soft mist inhalers enhances patient convenience. Expanding use of fixed dose combinations supports value growth. Regional focus on standardized treatment pathways supports consistent demand.

The UK inhaler solution market is shaped by high asthma prevalence and structured respiratory care pathways. Strong clinical adherence to guideline recommended inhaler therapies drives consistent utilization. Emphasis on long term disease control supports maintenance inhaler demand. Increasing use of combination therapies improves symptom management outcomes. Retail pharmacies play a key role in patient education and inhaler technique. Ongoing innovation in inhaler devices supports gradual market expansion.

Inhaler solution market in Germany shows steady growth, due to strong diagnosis rates for asthma and chronic obstructive pulmonary disease. High physician confidence in inhaled therapies supports sustained prescribing. Broad availability of advanced inhaler formulations improves treatment personalization. Preference for high quality medical devices strengthens adoption of novel inhalers. Focus on long term disease control supports repeat usage. A well-developed healthcare delivery system ensures stable market performance.

France inhaler solution market is supported by a high prevalence of asthma and chronic obstructive pulmonary disease across urban and semi urban populations. Strong adherence to standardized clinical treatment pathways promotes consistent use of maintenance inhaler therapies. Physicians widely prescribe inhaled corticosteroids and combination inhalers for long term disease control. High patient awareness improves correct inhaler usage and treatment continuity. Broad availability of advanced inhaler devices enhances patient comfort and adherence. The market shows stable growth driven by sustained demand for chronic respiratory management.

Asia Pacific Inhaler Solution Market Trends

Inhaler solution market in APAC is expected to register a significant CAGR of 7.0% over the forecast period, due to rapidly rising respiratory disease incidence. Urbanization and increasing air pollution levels elevate demand for inhaler therapies. Improving access to diagnostic services supports earlier treatment initiation. Growing awareness of chronic disease management increases long term inhaler use. Expanding middle class populations drive higher healthcare spending. Entry of multinational and regional players enhances product availability.

Japan inhaler solution market benefits from an aging population with a high burden of chronic respiratory conditions. Strong physician preference for maintenance inhaler therapy supports consistent demand. High patient compliance improves treatment outcomes and repeat usage. Advanced inhaler device adoption aligns with patient convenience needs. Strong focus on quality and precision therapy supports premium products. Stable healthcare utilization patterns ensure steady market growth.

Inhaler solution market in China is expanding due to a large patient population affected by asthma and chronic obstructive pulmonary disease. Rising urban air pollution increases respiratory symptom prevalence. Improving diagnosis rates support higher inhaler prescription volumes. Greater acceptance of inhaled maintenance therapy enhances long term usage. Expansion of retail pharmacy networks improves access to inhaler products. Local manufacturing and international brand presence support competitive pricing.

Latin America Inhaler Solution Market Trends

Inhaler solution market in Latin America is expanding due to increasing respiratory disease burden and improving diagnosis rates. Urban air pollution and smoking prevalence contribute to rising asthma and chronic obstructive pulmonary disease cases. Growing awareness of inhaled therapy supports higher adoption of maintenance treatments. Expanding access to healthcare services increases prescription volumes. Entry of international pharmaceutical companies improves product availability. The market demonstrates gradual growth with a rising focus on long term respiratory care.

Brazil inhaler solution market represents one of the largest inhaler solution markets in Latin America, driven by a high prevalence of asthma and chronic obstructive pulmonary disease. Urbanization and environmental exposure increase demand for inhaled therapies. Improved clinical diagnosis supports earlier initiation of inhaler treatment. Strong physician preference for inhaled corticosteroids and combination therapies drives utilization. Expanding retail pharmacy networks improve patient access to inhaler solutions. Market growth remains steady with increasing emphasis on chronic disease management.

Middle East & Africa Inhaler Solution Market Trends

Inhaler solution market in MEA shows gradual growth driven by increasing diagnosis of asthma and chronic obstructive pulmonary disease. Rising urbanization contributes to higher respiratory risk exposure. Growing awareness of inhaled therapy improves treatment uptake. Expansion of private healthcare facilities increases access to branded inhalers. Retail pharmacies play an important role in medication availability. Market growth remains steady across key urban centers.

Saudi Arabia inhaler solution market is supported by rising respiratory disease prevalence linked to environmental conditions. Increasing awareness of long term asthma and chronic obstructive pulmonary disease management drives inhaler adoption. Strong presence of multinational pharmaceutical brands improves product availability. Preference for combination therapies supports higher value prescriptions. Expanding retail pharmacy networks enhance patient access. Focus on preventive respiratory care supports consistent demand.

Key Inhaler Solution Company Insights

Boehringer Ingelheim maintains a strong position in the inhaler solution market through its extensive respiratory portfolio and expertise in chronic obstructive pulmonary disease. GSK and AstraZeneca hold significant market shares supported by established asthma and COPD inhaler brands and global distribution. Novartis and Chiesi Farmaceutici strengthen their presence through differentiated inhaled therapies and sustained investment in respiratory research. Mundipharma and Orion Corporation focus on targeted portfolios and regional markets. Aptar Pharma, Vectura Group, and Kindeva Drug Delivery contribute through advanced inhaler device technologies, formulation development, and manufacturing capabilities, driving innovation and market growth.

Key Inhaler Solution Companies:

The following are the leading companies in the inhaler solution market. These companies collectively hold the largest market share and dictate industry trends.

- Boehringer Ingelheim

- GSK

- AstraZeneca

- Novartis

- Chiesi Farmaceutici

- Mundipharma

- Orion Corporation

- Aptar Pharma

- Vectura Group

- Kindeva Drug Delivery

Recent Developments

-

In October 2025, Aptar Pharma’s HeroTracker Sense, a Bluetooth-enabled add-on sensor for pMDIs, received 510(k) clearance from the U.S. Food and Drug Administration (FDA). This device enables standard metered-dose inhalers to be transformed into smart devices, improving patient adherence through real-time digital dose tracking.

-

In October 2025, GSK announced positive Phase III data for a next-generation low-carbon version of its salbutamol MDI, using a new propellant. This version is positioned for regulatory submission and is expected to be launched around 2026 as part of GSK’s commitment to sustainability.

-

In December 2023, Kindeva announced a collaboration with Orbia Fluorinated Solutions (Koura) to convert existing pMDI inhaler products to low-GWP propellant (HFA-152a). This initiative aims to create more environmentally friendly inhalers in line with global sustainability targets.

Inhaler Solution Market Report Scope

Report Attribute

Details

Market size in 2025

USD 31.4 billion

Estimated market size in 2026

USD 33.1 billion

Projected market size by 2033

USD 49.8 billion

Growth rate

CAGR of 5.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Inhaler type, drug class, application, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Malaysia; Indonesia; Laos; Cambodia; Myanmar; Vietnam; Yemen; Pakistan; Brazil; Argentina; Chile; South Africa; Saudi Arabia; UAE; Kuwait

Key company profiled

Boehringer Ingelheim; GSK; AstraZeneca; Novartis; Chiesi Farmaceutici; Mundipharma; Orion Corporation; Aptar Pharma; Vectura Group; Kindeva Drug Delivery.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Inhaler Solution Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global inhaler solution market report based on inhaler type, drug class, application, distribution channel, and region:

-

Inhaler Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Pressurized Metered-Dose Inhalers (pMDIs)

-

Dry-Powder Inhalers (DPIs)

-

Soft Mist Inhalers (SMIs)

-

-

Drug Class Outlook (Revenue, USD Million, 2021 - 2033)

-

ICS

-

LAMA/LABA

-

SAMA/SABA

-

Combination Therapies

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Asthma

-

Chronic Obstructive Pulmonary Disease (COPD)

-

Cystic Fibrosis

-

Others

-

-

Distribution ChannelOutlook (Revenue, USD Million, 2021 - 2033)

-

Retail Pharmacies

-

Institutional / Hospital Pharmacies

-

Public

-

Private

-

-

Online Pharmacies

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

Malaysia

-

Indonesia

-

Myanmar

-

Laos

-

Cambodia

-

Vietnam

-

Yemen

-

Pakistan

-

-

Latin America

-

Brazil

-

Argentina

-

Chile

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global inhaler solution market size was valued at USD 31.4 billion in 2025 and is estimated at USD 33.1 billion for 2026.

The global inhaler solution market is expected to grow at a CAGR of 5.9% from 2026 to 2033, reaching USD 49.8 billion.

North America dominated with a 37.3% revenue share in 2025.

Key factors that are driving the market growth include the rising prevalence of respiratory disorders such as asthma and chronic obstructive pulmonary disease, increasing exposure to air pollution and tobacco smoke, and growing awareness of early diagnosis and long-term disease management

Pressurized metered-dose inhalers (pMDIs) segment led with a 51.1% revenue share in 2025, while Soft Mist Inhalers (SMIs) is the fastest-growing segment.

Combination therapies segment led with a 54.7% revenue share in 2025, while LAMA/LABA is the fastest-growing area.

Asthma segment led with a 53.1% revenue share in 2025 and cystic fibrosis is the fastest-growing.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Boehringer Ingelheim; GSK; AstraZeneca; Novartis; Chiesi Farmaceutici; Mundipharma; Orion Corporation; Aptar Pharma; Vectura Group; Kindeva Drug Delivery.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.