- Home

- »

- Electronic Devices

- »

-

IoT Microcontroller Market Size & Share Report, 2026-2023GVR Report cover

![IoT Microcontroller Market (2026 - 2033)Report]()

IoT Microcontroller Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (8 Bit, 16 Bit, 32 Bit), By Application (Smart Home, Consumer Electronics, Industrial Automation), By Region (North America, Europe, Asia Pacific), And Segment Forecasts

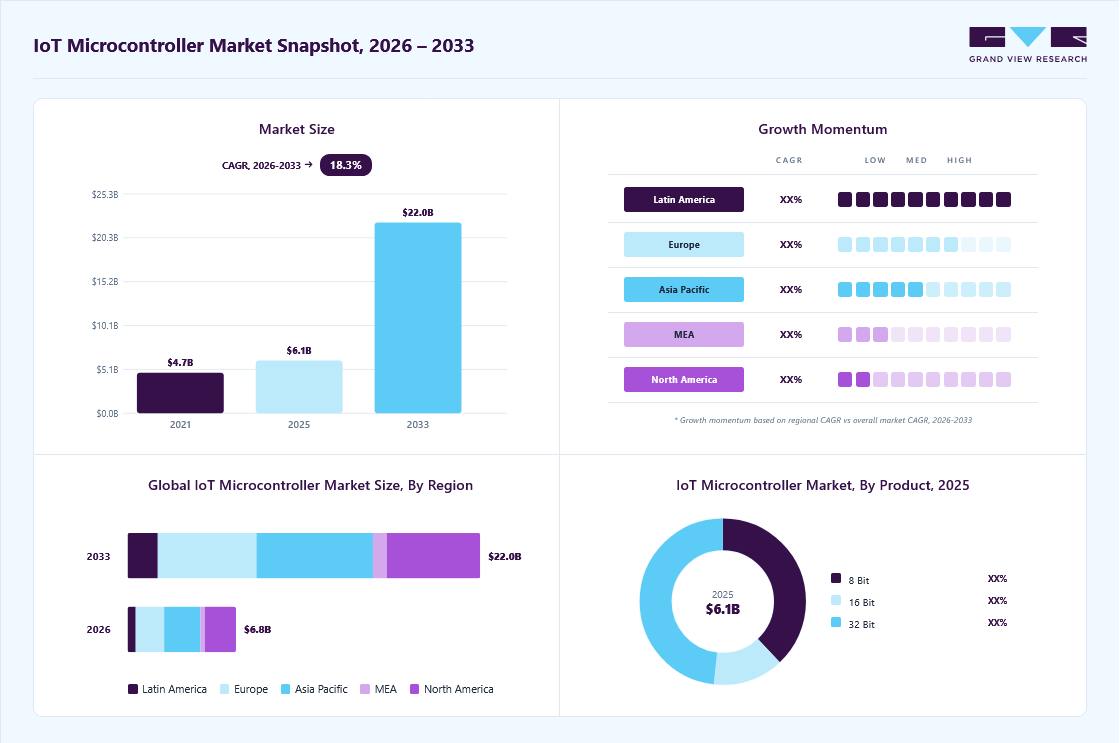

Market Size, 2025

$6.1BMarket Estimate, 2026

$6.8BMarket Forecast, 2033

$22.0BCAGR, 2026–2033

18.3%IoT Microcontroller Market Size & Trends

The global IoT microcontroller market size was valued at USD 6.1 billion in 2025 and is projected to grow from USD 6.8 billion in 2026 to USD 22.0 billion in 2033, at a CAGR of 18.3% from 2026 to 2033. Asia Pacific dominated the market, accounting for a revenue share of 33.3% in 2025. The rapid adoption of Industry 4.0 across China, Japan, South Korea, and India is increasing demand for IoT-enabled manufacturing equipment.

Key Market Trends & Insights

- By product: 32 bit segment dominated the market, with a revenue share of 48.3% in 2025

- By application: Industrial Automation segment held the largest market share of 33.5% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (33.3% revenue share, 2025)

- By country: The IoT microcontroller market in the China held the largest share in the Asia Pacific region in 2025.

Market Size & Forecast

- Market size in 2025: USD 6.1 Billion

- Estimated market size in 2026: USD 6.8 Billion

- Projected market size by 2033: USD 22.0 Billion

- CAGR (2026-2033): 18.3%

Microcontrollers enable real-time machine monitoring, predictive maintenance, automation, and data processing, helping manufacturers improve operational efficiency, reduce downtime, and enhance production quality. The market is experiencing robust growth, driven by the increasing application of IoT devices in both consumer and industrial applications. A key trend fueling this expansion is the demand for microcontrollers with enhanced power efficiency, processing capability, and connectivity features that support a wide range of IoT applications, from smart home devices to industrial automation systems. The rise of edge computing also plays a pivotal role, as manufacturers seek microcontrollers that enable real-time processing and data analysis at the device level, reducing latency and network dependency. In the industrial domain, the adoption of the IoT microcontrollers industry is heavily influenced by the ongoing digital transformation initiatives within manufacturing, energy, and utility sectors. Industrial IoT applications rely on robust, high-performance microcontrollers to monitor and manage equipment, automate processes, and collect critical operational data. These microcontrollers are essential for smart factory implementations, predictive maintenance, and real-time asset tracking, creating a high demand for processors that can handle complex computations and support multiple sensor connections. This shift presents opportunities for manufacturers to innovate in designing microcontrollers that cater to specific industrial needs, helping drive productivity and reduce operational costs.")

Moreover, advancements in edge computing are accelerating the IoT microcontrollers industry growth. As more companies shift data processing closer to the source to reduce latency and enhance responsiveness, microcontrollers that enable edge processing and local data storage have become crucial. These IoT microcontrollers help streamline data management by allowing devices to make quick decisions without relying on centralized cloud systems, which is particularly valuable in scenarios where low latency is critical, such as healthcare monitoring, autonomous vehicles, and industrial automation. This trend creates opportunities for microcontroller manufacturers to differentiate through innovation in computing capabilities and embedded security features, allowing them to capitalize on the shift towards decentralized processing.

Security remains a major concern, as IoT devices are vulnerable to cyber threats, which can compromise data integrity and user privacy. As a result, there is a growing focus on integrating advanced security protocols directly into IoT microcontrollers, offering features such as data encryption, secure boot, and hardware-based protection against tampering. This demand for secure microcontrollers is driven by both consumer and enterprise sectors, as organizations seek to prevent data breaches and adhere to compliance requirements.

Regulatory frameworks and laws are also shaping the IoT microcontroller market, particularly as governments and regulatory bodies worldwide implement stringent standards to protect data and ensure device interoperability. Regions such as the European Union have established regulations under the General Data Protection Regulation (GDPR) and the Radio Equipment Directive, setting requirements for data privacy, security, and compatibility in IoT devices. Additionally, the U.S. has introduced initiatives to standardize IoT device security, impacting how microcontrollers are designed and integrated. Compliance with these regulations is essential for market players, creating a need for investment in secure and compliant microcontroller solutions.

Market Dynamics

IoT microcontrollers are witnessing strong adoption as they serve as the core processing units that enable sensing, data processing, communication, and control functions in connected devices. These microcontrollers support a wide range of IoT applications across smart homes, industrial automation, healthcare, automotive, consumer electronics, agriculture, and smart city infrastructure. The rapid proliferation of connected devices, increasing adoption of Industry 4.0, expansion of 5G networks, and growing demand for edge computing are driving the need for energy-efficient and high-performance microcontrollers. The increasing integration of Wi-Fi, Bluetooth Low Energy (BLE), Zigbee, Thread, and cellular IoT connectivity within microcontrollers is further simplifying device development and accelerating deployment across diverse end-use industries. As organizations continue to invest in digital transformation and intelligent connected ecosystems, demand for advanced IoT microcontrollers is expected to grow steadily worldwide.

The rapid proliferation of IoT-enabled devices across smart homes, industrial automation, healthcare, automotive, and consumer electronics is a major driver for the IoT microcontroller market. Modern connected devices require microcontrollers to perform sensing, data processing, communication, and control functions while maintaining low power consumption. Additionally, the growing adoption of edge computing is increasing demand for advanced microcontrollers capable of processing data locally, reducing latency, and improving real-time decision-making. As organizations continue to invest in digital transformation and connected ecosystems, demand for high-performance and energy-efficient IoT microcontrollers is accelerating globally.

Cybersecurity concerns and increasing device design complexity remain significant restraints for the IoT microcontroller market. As IoT deployments expand, connected devices become more vulnerable to cyberattacks, unauthorized access, and data breaches. Manufacturers must incorporate advanced security features such as secure boot, encryption, authentication protocols, and hardware-based security modules, increasing development costs and design complexity. Furthermore, integrating multiple communication standards, ensuring interoperability, and managing power efficiency requirements can extend product development cycles, creating challenges for device manufacturers and slowing adoption in some applications.

The growing deployment of artificial intelligence (AI)-enabled IoT devices and smart infrastructure projects presents a significant opportunity for the IoT microcontroller market. Industries are increasingly adopting intelligent edge devices capable of performing machine learning inference, predictive maintenance, computer vision, and real-time analytics without relying entirely on cloud connectivity. This trend is driving demand for next-generation microcontrollers with integrated AI accelerators, enhanced processing capabilities, and low-power architectures. Additionally, investments in smart cities, connected transportation systems, smart grids, industrial automation, and digital healthcare infrastructure are creating substantial growth opportunities for advanced IoT microcontroller solutions worldwide.

Analyst Perspective

The IoT microcontroller market sits at the intersection of several transformative technology trends, including the rapid expansion of the Internet of Things (IoT), increasing adoption of edge computing, accelerating deployment of Industry 4.0 technologies, growing demand for smart homes and connected consumer devices, and the emergence of AI-enabled edge intelligence. As organizations seek to process data closer to the source, improve operational efficiency, reduce latency, and enhance automation, microcontrollers have evolved from simple embedded controllers into intelligent processing platforms that enable real-time decision-making and connectivity across billions of devices. The central competitive moat, however, will belong to vendors that successfully integrate ultra-low-power architectures, embedded artificial intelligence capabilities, advanced cybersecurity features, multi-protocol wireless connectivity, and scalable software development ecosystems into a unified IoT platform. Furthermore, increasing adoption across industrial automation, healthcare, automotive electronics, smart infrastructure, and consumer applications will continue to expand opportunities for innovation and differentiation within the global IoT microcontroller ecosystem.

Product Insights

Based on product, the 32 bit segment led the market with the largest revenue share of 48.3% and is expected to grow at the significant CAGR over the forecast period. The segment is witnessing significant growth due to the product’s advanced processing capabilities and versatility, making it suitable for complex IoT applications requiring real-time data processing, such as industrial automation, smart healthcare, and connected vehicles. A primary driver here is the demand for more robust processing power and memory to support advanced IoT functions like machine learning and data analytics. As industries prioritize more sophisticated IoT solutions, 32-bit microcontrollers enable enhanced device functionality and connectivity, positioning this segment for rapid growth. Opportunities in this segment are further supported by advancements in IoT ecosystems, as businesses look to integrate high-performance controllers to drive digital transformation in industries with complex IoT requirements.

The 8 bit segment is expected to grow at a significant CAGR during the forecast period. The segment is experiencing steady growth, primarily driven by cost efficiency and low-power consumption, making it ideal for basic IoT applications. A key driver for this segment is its suitability for simpler devices such as smart meters, wearables, and basic sensors where processing requirements are minimal. Additionally, manufacturers are increasingly focusing on enhancing the efficiency and integration of 8-bit controllers to meet the needs of low-cost IoT devices in emerging markets. Opportunities in this segment also lie in smart homes and consumer electronics, where 8-bit microcontrollers can efficiently perform specific tasks, promoting the adoption of IoT in budget-sensitive applications.

Application Insights

Based on application, industrial automation segment led the market with the largest revenue share of 33.5% in 2025. IoT microcontrollers are driving the segment growth as industries embrace automation for operational efficiency and data-driven insights. The demand for real-time monitoring and control across manufacturing processes is spurring the adoption of IoT microcontrollers, which enable precise control over machinery, predictive maintenance, and streamlined workflows. Increasing investments in smart factories and Industry 4.0 are further supporting growth by opening opportunities to implement robust IoT-enabled systems. Additionally, the integration of IoT microcontrollers in industrial settings supports energy efficiency and productivity improvements, positioning this segment as a vital component of the larger industrial transformation.

The smart home segment is expected to grow at a significant rate during the forecast period. The Smart Home segment is experiencing significant growth as IoT microcontrollers industry become central to interconnected home environments, fueling advancements in device compatibility, energy management, and enhanced security. A primary driver is the increasing consumer demand for convenience and personalized automation, which IoT microcontrollers enable by connecting appliances, lighting, and HVAC systems to unified platforms. Opportunities are expanding as IoT microcontrollers become more affordable and adaptable, enabling seamless integration across various smart devices. Moreover, rising awareness of energy efficiency and the convenience of remote home monitoring further drive the adoption of IoT solutions in the residential sector, strengthening this segment’s growth trajectory

Regional Insights

In the IoT microcontroller industry North America held a market share of over 29% in 2024. The market growth is propelled by the rapid adoption of IoT technologies in sectors like healthcare, automotive, and industrial automation. Major investments in smart city projects and an established tech ecosystem enable the widespread integration of IoT microcontrollers in connected devices. The growth of edge computing and increased R&D investments in IoT technologies are also creating new opportunities, especially in real-time data processing and enhanced network security. The presence of key industry players in the U.S. drives innovation, positioning North America as a pivotal market for IoT advancements.

U.S. IoT Microcontroller Market Trends

The IoT microcontroller industry in the U.S. is growing significantly at a CAGR of 14.6% from 2025 to 2030. With a robust R&D landscape, the U.S. leads in IoT innovation, creating opportunities in data security and analytics applications. Additionally, government and private sector investments in smart infrastructure support sustained growth, positioning the U.S. as a critical market for IoT technology.

Asia Pacific IoT Microcontroller Market Trends

Asia Pacific dominated the IoT microcontroller market with the largest revenue share of 33.3% in 2025. The Asia Pacific IoT microcontroller industry is experiencing rapid growth, primarily driven by extensive IoT adoption in consumer electronics, manufacturing, and smart cities. China and India lead the region with strong government support for digital infrastructure and initiatives to boost IoT in sectors such as transportation and public safety. With a vast manufacturing base and high consumer demand for smart devices, opportunities for IoT microcontrollers are expanding. The region’s drive towards 5G deployment further accelerates IoT connectivity, making Asia Pacific a significant growth area for IoT advancements.

The IoT microcontroller market in the China held the largest share in the Asia Pacific region in 2025. The China IoT microcontroller market is growing swiftly due to the government’s emphasis on smart city projects and the industrial internet. China’s large-scale manufacturing capabilities and focus on digital infrastructure foster rapid IoT integration across sectors. Opportunities abound as the country invests in IoT for public services, energy management, and urban transportation. With the advancement of 5G networks, China is positioned to lead in IoT connectivity, driving demand for powerful microcontrollers to support these ambitious initiatives.

The IoT microcontroller market in India is driven by its digital transformation initiatives, especially in smart agriculture, urban development, and remote healthcare. The government’s focus on ‘Digital India’ and investments in 5G infrastructure create a conducive environment for IoT adoption, fueling IoT microcontrollers industry growth. Opportunities in agriculture and healthcare IoT offer significant growth potential as IoT solutions improve efficiency and accessibility. With a growing tech ecosystem and supportive policies, India is rapidly integrating IoT microcontrollers in key sectors.

Europe IoT Microcontroller Market Trends

The IoT microcontroller industry in Europe is growing significantly at a CAGR of 17.4% from 2025 to 2030. The Europe market is expanding as the region emphasizes energy efficiency and regulatory compliance across industries. Growth in the automotive sector, particularly in electric and autonomous vehicles, is boosting the demand for high-performance IoT microcontrollers capable of supporting complex functions. Additionally, government initiatives for sustainable development encourage the adoption of IoT solutions in energy and environmental monitoring, opening new opportunities for IoT microcontroller applications. Europe’s focus on digital transformation and industry standards further strengthens its IoT ecosystem, supporting steady market growth.

The IoT microcontroller market in the UK is witnessing increased IoT microcontroller adoption driven by advancements in smart city infrastructure and digital healthcare initiatives. As the country prioritizes IoT-enabled solutions for energy management and healthcare modernization, the demand for advanced microcontrollers grows.

The Germany IoT microcontroller market is propelled by its industrial manufacturing strength, with high demand for IoT integration in production and logistics. As Industry 4.0 continues to reshape German manufacturing, IoT microcontrollers play a critical role in enabling smart machinery and predictive maintenance.

Key IoT Microcontroller Company Insights

Some of the key players in the IoT microcontroller industry include Broadcom; Espressif Systems (Shanghai) Co., Ltd; Holtek Semiconductor Inc.; Infineon Technologies; Microchip Technology Inc.; Nuvoton Technology Corporation; NXP Semiconductors; Silicon Laboratories; STMicroelectronics; Texas Instruments Incorporated; and Renesas Electronics Corporation. Companies in the market are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In September 2024, STMicroelectronics announced a strategic collaboration with Qualcomm Technologies International to enhance industrial and consumer IoT solutions with edge AI capabilities. This partnership will integrate Qualcomm’s advanced AI-powered wireless connectivity technologies, starting with a Bluetooth, Wi-Fi, Thread combo system-on-a-chip, with ST’s leading microcontroller ecosystem. Developers will benefit from seamless connectivity and software integration into STM32 general-purpose MCUs, enabling rapid adoption through ST’s extensive global sales channels.

-

In May 2024, Renesas Electronics Corporation, a global microcontrollers solution provider announced the acquisition of Sequans Communications, a fabless semiconductor company. This strategic move aims to strengthen Renesas' position in the IoT microcontroller market, particularly in 5G/4G cellular IoT technologies. The acquisition is expected to finalize by the first quarter of 2024, pending regulatory approvals.

Key IoT Microcontroller Companies

The following key companies have been profiled for this study on the IoT microcontroller market.

-

Broadcom

-

Espressif Systems (Shanghai) Co., Ltd

-

Holtek Semiconductor Inc.

-

Infineon Technologies

-

Microchip Technology Inc.

-

Nuvoton Technology Corporation

-

NXP Semiconductors

-

Silicon Laboratories

-

STMicroelectronics

-

Texas Instruments Incorporated

-

Renesas Electronics Corporation

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (NXP Semiconductors, STMicroelectronics, Microchip Technology, Texas Instruments, Infineon Technologies, Renesas Electronics)

- Established players focus on developing comprehensive microcontroller portfolios spanning 8-bit, 16-bit, and 32-bit architectures.

- Their strategies emphasize integration of wireless connectivity, embedded security, edge AI capabilities, and low-power designs for industrial, automotive, healthcare, smart home, and consumer electronics applications.

- They invest heavily in R&D, software ecosystems, developer tools, and strategic partnerships with OEMs and IoT platform providers.

- These companies benefit from strong brand recognition, extensive intellectual property portfolios, advanced semiconductor manufacturing capabilities, global distribution networks, and long-standing customer relationships.

- Their ability to provide end-to-end hardware, software, security, and connectivity solutions enables them to support large-scale IoT deployments across multiple industries.

- High R&D expenditures, complex product portfolios, and extended product development cycles can reduce responsiveness to niche market requirements.

- They also face challenges from semiconductor supply chain fluctuations, pricing pressures, and increasing competition from lower-cost regional suppliers and emerging architectures such as RISC-V.

Emerging Players (Espressif Systems, Silicon Laboratories, GigaDevice, Nordic Semiconductor)

- Emerging players focus on specialized IoT microcontrollers featuring integrated Wi-Fi, Bluetooth Low Energy (BLE), Matter, Thread, AI acceleration, and ultra-low-power architectures.

- Many emphasize cost-effective solutions, rapid product innovation, developer-friendly software frameworks, and targeted applications such as wearables, smart home devices, edge AI, and battery-powered sensors.

- Emerging companies offer greater flexibility, faster innovation cycles, competitive pricing, and specialization in next-generation IoT technologies.

- Their focus on connectivity integration, energy efficiency, and simplified development environments enables rapid adoption among startups, device manufacturers, and smart device developers.

- Limited manufacturing scale, smaller sales and support networks, and lower financial resources may restrict their ability to compete for large global contracts.

- Dependence on third-party foundries, narrower product portfolios, and lower brand recognition can also affect long-term scalability and market penetration compared with established semiconductor leaders.

IoT Microcontroller Market Scope

Report Attribute

Details

Market size value in 2025

USD 6.1 billion

Estimated market size in 2026

USD 6.8 billion

Projected market size by 2033

USD 22.0 billion

Growth rate

CAGR of 18.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product; application; region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Broadcom; Espressif Systems (Shanghai) Co., Ltd; Holtek Semiconductor Inc.; Infineon Technologies; Microchip Technology Inc.; Nuvoton Technology Corporation; NXP Semiconductors; Silicon Laboratories; STMicroelectronics; Texas Instruments Incorporated; Renesas Electronics Corporation

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global IoT Microcontroller Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends from 2021 to 2033 in each of the sub-segments. For the purpose of this study, Grand View Research has segmented the global IoT microcontroller market report based on product, application, and region:

-

Product Outlook (Revenue; USD Billion, 2021 - 2033)

-

8 Bit

-

16 Bit

-

32 Bit

-

-

Application Outlook (Revenue; USD Billion, 2021 - 2033)

-

Industrial Automation

-

Smart Home

-

Consumer Electronics

-

Smartphones

-

Wearables

-

Others

-

-

Others

-

-

Regional Outlook (Revenue: USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

The IoT microcontroller market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each IoT microcontroller segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Product

Revenue capture definition

8-Bit

8-bit microcontrollers are low-cost, low-power processing units that handle simple control and monitoring tasks in IoT devices. They are commonly used in basic sensors, smart meters, home appliances, and other applications requiring limited computing power and memory while maintaining high energy efficiency.

16-Bit

16-bit microcontrollers offer moderate processing capabilities and improved performance compared to 8-bit devices. They are widely used in industrial controls, medical equipment, automotive electronics, and connected devices that require enhanced data processing, precision control, and efficient power management.

32-Bit

32-bit microcontrollers are high-performance processing units designed for advanced IoT applications. They support complex computations, real-time data processing, artificial intelligence functions, enhanced security features, and multiple connectivity protocols, making them ideal for smart homes, industrial automation, healthcare, automotive, and edge computing applications.

Segment - Application

Revenue capture definition

Industrial Automation

Industrial automation refers to the use of IoT microcontrollers in manufacturing equipment, robotics, process control systems, sensors, and industrial machinery. These microcontrollers enable real-time monitoring, predictive maintenance, machine-to-machine communication, and operational efficiency improvements in smart factories.

Smart Home

Smart home applications utilize IoT microcontrollers in connected devices such as smart lighting, thermostats, security systems, smart locks, appliances, and voice-controlled assistants. Microcontrollers facilitate device communication, automation, energy management, and remote control functionalities.

Consumer Electronics

Consumer electronics applications include smartphones, wearable devices, gaming accessories, smart speakers, personal health trackers, and entertainment systems. IoT microcontrollers provide device control, connectivity, sensor integration, power management, and user-interface functionality.

Others

The "Others" segment includes healthcare devices, automotive electronics, smart agriculture systems, smart city infrastructure, energy management solutions, environmental monitoring equipment, logistics tracking systems, and connected retail technologies.

Estimation Model

Layer

Question

Analysis

Connected Device Addressable Layer

Who requires IoT microcontrollers?

Identify end-use industries deploying connected devices, including industrial automation, smart homes, consumer electronics, healthcare, automotive, agriculture, energy, and smart cities. Assess the volume of IoT-enabled devices requiring embedded processing, sensing, and communication capabilities to establish the total addressable market for IoT microcontrollers.

Technology Readiness & Integration Layer

Which applications can deploy IoT microcontrollers?

Evaluate the adoption of wireless connectivity technologies (Wi-Fi, Bluetooth, Zigbee, Thread, LPWAN, Cellular IoT), edge computing requirements, sensor integration needs, and power efficiency demands. Analyze application readiness across industries to determine potential deployment opportunities for IoT microcontrollers.

Adoption & Connected Device Expansion Layer

Who actively invests in IoT-enabled solutions?

Analyze investments by manufacturers, smart home solution providers, consumer electronics companies, automotive OEMs, healthcare device manufacturers, utilities, and smart city developers. Assess growth in connected device shipments, digital transformation initiatives, and Industry 4.0 deployments to identify active adopters of IoT microcontrollers.

Monetization Layer

How much revenue is generated?

Quantify revenue generated from 8-bit, 16-bit, and 32-bit microcontroller sales across various applications. Evaluate revenues from integrated connectivity-enabled MCUs, AI-capable microcontrollers, industrial-grade processors, development platforms, and long-term supply agreements supporting IoT device production worldwide.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

IoT Microcontroller Ecosystem & Market Opportunity Assessment

Assessed demand for 8-bit, 16-bit, and 32-bit microcontrollers, integrated wireless connectivity solutions, embedded security technologies, edge AI processors, software development platforms, and supporting semiconductor ecosystems across key industries in Latin America.

Supports market entry and expansion strategies by identifying underserved opportunities, evaluating competitive dynamics, assessing technology gaps, and uncovering growth potential across the IoT microcontroller value chain.

Regional Semiconductor Manufacturing & IoT Deployment Assessment

Analyzed regional semiconductor production capabilities, electronics manufacturing ecosystems, IoT adoption rates, government digitalization initiatives, connectivity infrastructure, and investment trends across Asia Pacific and Latin America.

Helps investors, semiconductor manufacturers, and technology providers identify attractive growth markets, optimize regional expansion strategies, strengthen supply chain planning, and capitalize on emerging IoT deployment opportunities.

Competitive Benchmarking & Innovation Landscape Assessment

Assessed product portfolios, technology strategies, AI integration capabilities, security features, software ecosystems, and go-to-market approaches of leading and emerging IoT microcontroller vendors worldwide.

Helps stakeholders benchmark competitors, identify differentiation opportunities, evaluate acquisition or partnership prospects, and develop effective market positioning strategies.

Frequently Asked Questions About This Report

The global IoT microcontroller market size was estimated at USD 5.55 million in 2024 and is expected to reach USD 6.08 million in 2025.

The global IoT microcontroller market is expected to grow at a compound annual growth rate of 16.3% from 2025 to 2030 to reach USD 12.94 billion by 2030.

The 32-bit product segment accounted for the largest market share of over 48% in 2024. The 32-bit microcontroller segment is witnessing significant growth due to its advanced processing capabilities and versatility, making it suitable for complex IoT applications requiring real-time data processing, such as industrial automation, smart healthcare, and connected vehicles.

Some key players operating in the IoT microcontroller market include Broadcom, Espressif Systems (Shanghai) Co., Ltd; Holtek Semiconductor Inc.; Infineon Technologies; Microchip Technology Inc.; Nuvoton Technology Corporation; NXP Semiconductors; Silicon Laboratories; STMicroelectronics; Texas Instruments Incorporated; and Renesas Electronics Corporation among others.

Key factors that are driving the IoT microcontroller market growth include the IoT Microcontroller market is experiencing robust growth, driven by the increasing application of IoT devices in both consumer and industrial applications. A key trend fueling this expansion is the demand for microcontrollers with enhanced power efficiency, processing capability, and connectivity features that support a wide range of IoT applications, from smart home devices to industrial automation systems.

About the Author(s)

Electronic Devices Research Team

Semiconductors & Electronics · Electronic DevicesThis report was authored by the electronic devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic devices segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.