- Home

- »

- Disinfectants & Preservatives

- »

-

Magnesium Oxide Market Size, Growth Report, 2026-2033GVR Report cover

![Magnesium Oxide Market (2026 - 2033)Report]()

Magnesium Oxide Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Dead Burned Magnesia (DBM), Caustic Calcined Magnesia (CCM)), By Application (Agriculture, Pharmaceuticals), By Region, And Segment Forecasts

Market Size, 2025

$5.9BMarket Estimate, 2026

$6.2BMarket Forecast, 2033

$9.3BCAGR, 2026–2033

5.8%Magnesium Oxide Market Summary

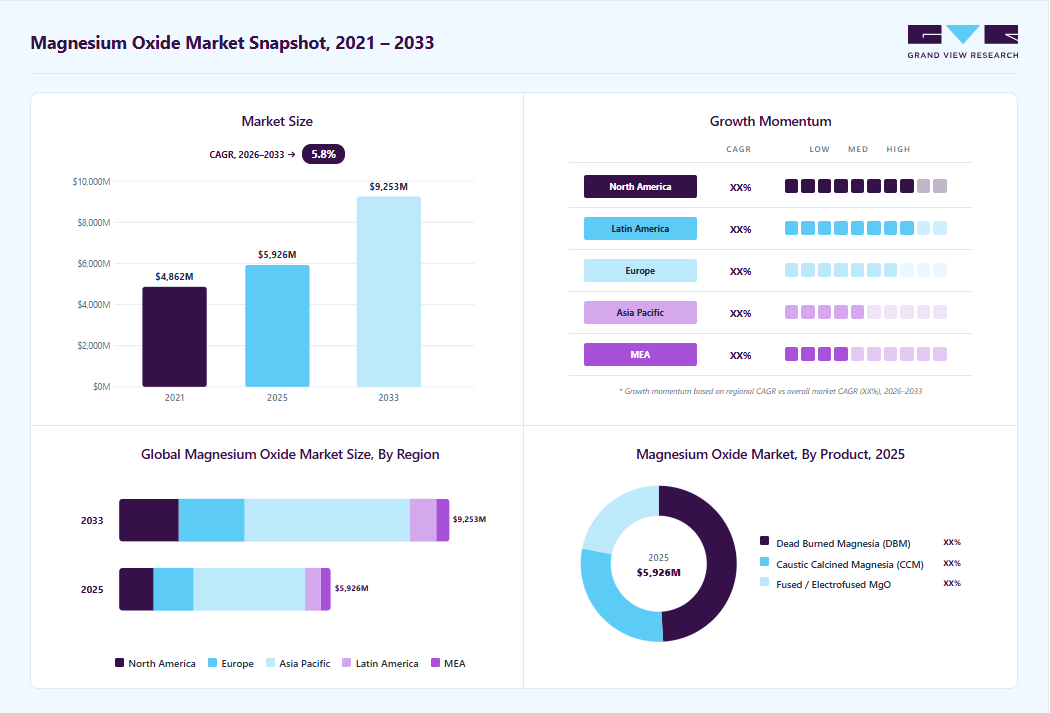

The global magnesium oxide market size was valued at USD 5.9 billion in 2025 and is projected to grow from USD 6.2 billion in 2026 to USD 9.3 billion by 2033, at a CAGR of 5.8% from 2026 to 2033. Asia Pacific dominated the global market, accounting for the largest revenue share of 52.6% in 2025 This growth is driven by the increasing/growing demand of the steel, cement, and ceramics sectors, particularly in emerging economies, which continue to drive magnesium oxide (MgO) consumption through its use in high-temperature refractory linings.

Key Market Trends & Insights

- By product: Fused/ electrofused MgO segment is expected to grow at the fastest CAGR of 8.1% from 2026 to 2033 in terms of revenue.

- By application: Agriculture segment held the largest revenue share of 32.6% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (52.6% revenue share, 2025)

- Fastest-growing regional market: North America (highest CAGR, 2026-2033)

- By country: The China magnesium oxide industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 5.9 Billion

- Estimated market size in 2026: USD 6.2 Billion

- Projected market size by 2033: USD 9.3 Billion

- CAGR (2026-2033): 5.8%

Moreover, the global shift toward sustainable manufacturing, environmental protection, and agricultural productivity elevated the demand for reactive and high-purity MgO in water treatment, emissions control, and soil enhancement. Furthermore, increasing innovation in pharmaceuticals, specialty chemicals, and advanced materials is expanding its functional scope. Backed by continuous technological advancement, process optimization, and vertical integration, magnesium oxide remains a strategically vital material enabling durability, efficiency, and sustainability across global value chains.

")

Key opportunities in the magnesium oxide industry are increasing due to demand across various end-use industries, including environmental, construction, agriculture, and healthcare. With the increasing global emphasis on sustainable materials, MgO’s eco-friendly profile plays a significant role in carbon capture, wastewater treatment, and soil enhancement, presenting major growth opportunities. The construction industry’s shift toward fire-resistant and energy-efficient materials further fuels the adoption of MgO boards and cement. Additionally, its use in animal feed, fertilizers, and pharmaceuticals benefits from the growing focus on nutrition and health. Technological advancements in production efficiency and the development of high-purity, reactive grades also open new possibilities in electronics, refractories, and specialty chemicals, making MgO a key material in the transition toward greener and high-performance applications.

The global MgO market continues to face a range of structural and operational challenges that influence its long-term growth trajectory. A key concern is the volatility in magnesite prices, which directly impacts production economics and pricing stability. Stringent environmental regulations governing mining and calcination processes have increased compliance costs and restricted supply in several regions. Persistent quality inconsistencies among producers, particularly in developing markets, affected product performance and end-user confidence. Moreover, competition from alternative materials such as calcium oxide and other refractory substitutes presents an ongoing threat to market share.

Market Dynamics

Magnesium oxide is widely used in refractory linings for steel furnaces, cement kilns, glass plants, and metallurgical processing units due to its superior heat resistance and chemical stability. Rising steel production across both developed and emerging economies is driving higher demand for refractory-grade magnesium oxide. The expansion of infrastructure projects, industrial construction activities, and automotive manufacturing continues to support steel consumption, underscoring the need for high-performance refractory materials.

Industrial growth across the Asia Pacific and the Middle East is further driving investments in high-temperature processing facilities and metallurgical operations. Steel manufacturers are increasingly adopting durable refractory solutions capable of operating under extreme thermal conditions, which is expected to sustain long-term demand for magnesium oxide-based materials over the forecast period.

The production of magnesium oxide involves calcination at extremely high temperatures, making the manufacturing process highly energy-intensive. Rising fuel and electricity prices are placing significant pressure on production costs and reducing margin stability for manufacturers across major producing regions.

In addition, increased environmental scrutiny of industrial emissions and mining activities is driving higher compliance costs and operational expenditures. These cost-related pressures, combined with fluctuations in transportation and raw material costs, continue to create challenges for market participants in the magnesium oxide industry.

Market Concentration & Characteristics

The presence of several multinational chemical companies with well-established production, distribution, and purification capabilities characterizes the global magnesium oxide market. Leading players, such as Israel Chemical Ltd. (ICL), Martin Marietta Magnesia Specialties, Premier Magnesia, and Grecian Magnesite, dominate the market through their extensive product portfolios, diverse magnesia offerings, and global supply networks. These companies leverage advanced technologies and regulatory compliance expertise to cater to the demand.

The magnesium oxide industry demonstrates limited price elasticity, as production costs are closely tied to raw material and energy inputs. Product standardization is moderate, with differentiation largely based on purity, reactivity, and end-use specialization. Regional markets often operate in supply clusters near resource bases, leading to localized competition and logistical interdependence. Overall, the industry combines high capital intensity, resource dependency, and technological specialization, creating a structure that favors scale efficiency and long-term contractual relationships over short-term price competition.

Product Insights

The dead burned magnesia dominated the global magnesium oxide industry, accounting for the largest revenue share of 49.1% in 2025. This is primarily due to its exceptional thermal stability, density, and resistance to chemical attack, which make it indispensable for refractory applications such as steelmaking, cement production, and glass manufacturing. Unlike caustic or fused magnesia, DBM is produced by calcining magnesite at very high temperatures (typically above 1,800 °C), resulting in a highly sintered, inert, and low-reactivity material that can withstand extreme conditions inside furnaces and kilns. Its superior structural integrity at high temperatures ensures longer refractory lining life, reduced maintenance downtime, and lower operational costs, key economic drivers for industries dependent on high-temperature processes.

The fused/electrofused MgO segment is expected to grow at the fastest CAGR of 8.1% during the forecast period, driven by its superior purity, density, and performance characteristics compared to other MgO grades. The increasing demand for advanced refractories to support high-temperature industrial processes, coupled with the ongoing modernization of steel manufacturing facilities and stricter quality standards, is accelerating adoption. Additionally, the shift toward energy-efficient furnaces and longer-lasting refractory linings positions electrofused MgO as a preferred material, ensuring both operational efficiency and reduced maintenance costs. This combination of technological advantages and industrial demand resilience underpins its strong future growth trajectory.

Application Insights

The agriculture segment dominated the global magnesium oxide market, accounting for the largest revenue share of 32.6% in 2025. Agriculture is the largest application segment for magnesium oxide, due to its critical dual role in both crop and livestock production. In farming, MgO serves as an effective soil amendment, improving acidic soils by raising the pH and supplying essential magnesium, a key element in chlorophyll production and photosynthesis. Its high reactivity and neutralizing value make it particularly valuable in regions facing soil magnesium depletion, such as parts of Asia, Latin America, and sub-Saharan Africa. Additionally, the global shift toward sustainable agriculture and precision nutrition has driven up demand for consistent, high-quality magnesium inputs-making MgO an indispensable part of modern agricultural systems.

The pharmaceuticals segment is expected to grow at the fastest CAGR of 8.2% during the forecast period, driven by its increasing use in antacids, dietary supplements, and mineral fortification products. Rising awareness of digestive health and the growing prevalence of gastrointestinal disorders are fueling demand for magnesium oxide-based formulations. Additionally, its role in cardiovascular health and bone-strengthening supplements has expanded its adoption across both prescription and over-the-counter medications. This trend is further reinforced by the aging population and the rising focus on preventive healthcare, positioning magnesium oxide as a critical ingredient in pharmaceutical innovation.

Regional Insights

Asia Pacific dominated the global magnesium oxide market with a 52.6% revenue share in 2025 due to its strong resource base, massive industrial demand, and rapid economic development. The region, particularly China, holds the world’s largest magnesite reserves and production capacity, giving it a structural advantage in both raw material availability and cost competitiveness. Additionally, Asia-Pacific’s large agricultural sector, especially in China, India, and Southeast Asia, drives significant demand for MgO in fertilizers, soil conditioners, and animal feed.

The China magnesium oxide market dominated Asia Pacific with a revenue share of 37.8% in 2025. This growth can be attributed to the country’s abundant magnesite reserves, large-scale production capacity, and deeply integrated industrial base. It serves as both the world’s significant producer and consumer, driven by strong demand from its steel, cement, glass, and agriculture sectors. With government support for domestic mining and processing, China benefits from cost advantages, established supply chains, and export strength, making it the central hub of global MgO supply and pricing influence.

North America Magnesium Oxide Market Trends

The North America magnesium oxide industry is expected to grow at the fastest CAGR of 7.1% during the forecast period, due to tightening environmental regulations, renewal ofinfrastructure, and the expanding focus on sustainable agriculture. The region’s industrial base, especially in the steel, cement, and environmental sectors, continues to rely heavily on MgO for refractory linings, flue-gas sulfurization, and wastewater treatment due to its superior thermal resistance and neutralizing capacity. However, the agriculture sector has emerged as the dominant application, largely because of the growing emphasis on soil health, pH correction, and magnesium enrichment in crop production.

U.S. Magnesium Oxide Market Trends

The U.S. magnesium oxide industry dominated North America, accounting for the largest revenue share of 79.7% in 2025. This growth is supported by the rising demand from both the agricultural and industrial sectors. Agriculture remains the dominant application, driven by the country’s large livestock industry and the increasing need for soil enhancement in magnesium-deficient farmlands. Farmers and feed manufacturers rely on MgO for its efficiency in correcting soil acidity and preventing metabolic disorders, such as grass tetany, in cattle.

Europe Magnesium Oxide Market Trends

The Europemagnesium oxide industry accounted for a global revenue share of 18.9% in 2025. The regional market is expanding due to strong demand from the steel, cement, and glass industries, as well as the region’s focus on sustainable and energy-efficient manufacturing. The rising use of MgO in environmental applications, such as wastewater treatment and emissions control, aligns with the stringent EU sustainability directives. Additionally, growth in agriculture, pharmaceuticals, and advanced materials is driving diversification beyond traditional refractories. Continuous R&D investments and innovation in high-purity and reactive MgO grades further enhance product performance. Europe’s emphasis on quality, circular economy practices, and domestic supply security firmly supports the market’s steady upward trajectory.

The Germany magnesium oxide market is growing steadily, fueled by the country’s advanced industrial landscape, strong environmental policies, and commitment to sustainable manufacturing. Industrial applications clearly dominate, with MgO being a critical material in the production of high-quality refractories used in Germany’s steel, cement, and glass industries. The country’s push toward energy efficiency and carbon reduction has intensified the demand for durable, heat-resistant materials that extend furnace life and improve operational performance roles that MgO fulfills exceptionally well.

Middle East & Africa Magnesium Oxide Market Trends

In the Middle East, the magnesium oxide industry is growing gradually but with strong long-term potential, supported by the region’s expanding industrial base and increasing focus on environmental sustainability. Industrial applications are the dominant segment, particularly in steel, cement, and desalination industries-sectors that form the backbone of regional infrastructure development.

Latin America Magnesium Oxide Market Trends

In Latin America, the magnesium oxide industry is expanding steadily, driven mainly by growth in agriculture and construction. Agriculture is the dominant application, as countries like Brazil, Argentina, and Chile rely heavily on MgO for soil correction and as a magnesium supplement in animal feed. The region’s widespread soil acidity and nutrient depletion make MgO an essential input for improving crop yields and livestock health.

Key Magnesium Oxide Company Insights

The global magnesium oxide market is led by a few vertically integrated producers, including Premier Magnesia, Israel Chemical Ltd. (ICL), Martin Marietta Magnesia Specialties, and Grecian Magnesite.

Premier Magnesia is one of the few companies with full ownership of its magnesia ore source and downstream manufacturing chain. Based in Gabbs, Nevada, U.S., the company has operated its magnesia mine and processing plant for over 50 years, marketing high-purity calcined magnesium oxide (MgO) and magnesium hydroxide products under the MAGOX brand.

Key Magnesium Oxide Companies:

The following are the leading companies in the magnesium oxide market. These companies collectively hold the largest market share and dictate industry trends.

- Israel Chemical Ltd. (ICL)

- Martin Marietta Magnesia Specialties

- Premier Magnesia

- Grecian Magnesite

- NEDMAG B.V.

- Magnezit Group

- Haicheng Guangling Refractory Manufacturing Co. LTD

- YINGKOU MAGNESITE CHEMICAL IND GROUP CO., LTD

- Bhavani Chemicals

- Ube Material Industries Ltd

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Israel Chemical Ltd. (ICL); Martin Marietta Magnesia Specialties; Premier Magnesia; Grecian Magnesite; NEDMAG B.V.; Magnezit Group; Ube Material Industries Ltd

- Expand production capabilities for refractory-grade and high-purity magnesium oxide products to support growing industrial demand.

- Strengthen vertically integrated mining and processing operations while investing in energy-efficient technologies and long-term industrial partnerships.

- Established mining resources, large-scale processing infrastructure, and diversified product portfolios serving multiple industrial applications.

- Integrated supply chains and strong technical expertise support product consistency and broad customer reach across global markets.

- Energy-intensive manufacturing operations increase exposure to fluctuations in fuel and electricity costs.

- Environmental compliance obligations associated with mining and emissions management continue to increase operational complexity.

Emerging Players: Haicheng Guangling Refractory Manufacturing Co., LTD; YINGKOU MAGNESITE CHEMICAL IND GROUP CO., LTD; Bhavani Chemicals

- Focus on regional production expansion and competitive supply capabilities targeting steel, refractory, and industrial processing sectors.

- Enhance local distributor relationships and develop application-specific magnesium oxide grades for regional industrial customers.

- Competitive manufacturing cost structures and operational flexibility within regional industrial markets.

- Ability to address customized refractory and processing requirements through tailored magnesium oxide solutions.

- Limited international distribution reach and smaller manufacturing scale compared to multinational producers.

- Challenges related to scaling operations and meeting evolving international environmental and quality standards.

Recent Developments

-

On October 22, 2025, Canada Nickel Company Inc. expanded its collaboration with NetCarb to explore low‑carbon industrial clusters that can produce magnesium products (by‑products of carbon sequestration processes), signaling innovation in sustainable magnesium supply chains.

-

In Dec 2024, RHI opened a new automatic plant to serve the booming electric-arc-furnace steel sector; this facility uses automation and sustainable processing (reducing any chromite in magnesia-chrome bricks)

-

In March 2024, RHI Magnesita (Austria), the significant refractory producer, announced an agreement to acquire Resco Group, a refractory manufacturer, for approximately USD 430 million. The deal significantly increases RHI’s North American production footprint, enabling ~50% of U.S. sales to be produced locally rather than imported.

Magnesium Oxide Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 6,238.3 million

Revenue forecast in 2033

USD 9,252.8 million

Growth rate

CAGR of 5.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2018 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, and region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

Israel Chemical Ltd. (ICL); Martin Marietta Magnesia Specialties; Premier Magnesia; Grecian Magnesite; NEDMAG B.V.; Magnezit Group; Haicheng Guangling Refractory; Yingkou Magnesite Chemical Industrial Group; Bhavani Chemicals; Ube Material Industries Ltd

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Magnesium Oxide Market Report Segmentation

This report forecasts volume & revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global magnesium oxide market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Dead Burned Magnesia (DBM)

-

Caustic Calcined Magnesia (CCM)

-

Fused/Electrofused MgO

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Agriculture

-

Industrial

-

Building and Construction

-

Pharmaceuticals

-

Environmental (FGD, Wastewater, Flue Gas)

-

Other Applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Competitive Benchmarking

Comparative analysis of magnesium oxide producers based on mining integration, refractory specialization, production scale, operational efficiency, and regional presence.

Supports supplier assessment and competitive intelligence through improved visibility into manufacturer capabilities and market positioning.

Cross-Segmentation

Detailed assessment of magnesium oxide consumption across refractory, steel, cement, agriculture, and environmental applications.

Helps identify high-growth industrial application areas and strategic expansion opportunities.

Opportunity Assessment

Evaluation of growth opportunities associated with steel industry expansion, industrial infrastructure development, and rising demand for advanced refractory materials.

Enables identification of long-term investment themes aligned with global industrial and metallurgical growth trends.

Frequently Asked Questions About This Report

Asia Pacific dominated with a 52.6% revenue share in 2025.

North America is the fastest-growing region over the forecast period.

Dead burned magnesia segment held the largest share (over 49.0%) in 2025, while fused/ electrofused MgO is the fastest-growing product.

The agriculture segment dominated the magnesium oxide market with a 32.6% revenue share in 2025, magnesium oxide market is being propelled by strong demand across refractory, steel, and construction sectors, reinforced by its expanding use in environmental, agricultural, and healthcare applications. Growing emphasis on high-performance materials, operational efficiency, and sustainable manufacturing continues to drive market momentum, while advances in high-purity and reactive MgO grades are unlocking new opportunities in advanced industrial and green technologies.

Key players include Israel Chemical Ltd. (ICL); Martin Marietta Magnesia Specialties; Premier Magnesia; Grecian Magnesite; NEDMAG B.V.; Magnezit Group; Haicheng Guangling Refractory; Yingkou Magnesite Chemical Industrial Group; Bhavani Chemicals; Ube Material Industries Ltd.

The magnesium oxide market is primarily driven by rising demand from refractory, steel, and construction industries, coupled with its growing use in environmental, agricultural, and healthcare applications. Increasing focus on high-performance materials, process efficiency, and sustainable manufacturing further accelerates MgO adoption across industrial value chains. Additionally, technological advancements in high-purity and reactive grades are expanding its role in next-generation industrial and green solutions.

The global magnesium oxide market size was valued at USD 5.9 billion in 2025 and is estimated at USD 6.2 billion for 2026.

The global magnesium oxide market is expected to grow at a CAGR of 5.8% from 2026 to 2033, reaching USD 9.3 billion by 2033.

About the Author(s)

Disinfectants & Preservatives Research Team

Bulk Chemicals · Disinfectants & PreservativesThis report was authored by the disinfectants & preservatives research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the disinfectants & preservatives segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.