- Home

- »

- Paints, Coatings & Printing Inks

- »

-

Masterbatch Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Masterbatch Market (2026 - 2033)Report]()

Masterbatch Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (White, Black, Color, Additive, Filler, Biodegradable), By Carrier Polymer (Polypropylene, Polyethylene Terephthalate, Polyethylene, Polyvinyl Chloride, Biodegradable Plastics), By End-use, By Region, And Segme

Market Size, 2025

$7.0BMarket Estimate, 2026

$7.4BMarket Forecast, 2033

$10.5BCAGR, 2026–2033

5.0%Masterbatch Market Summary

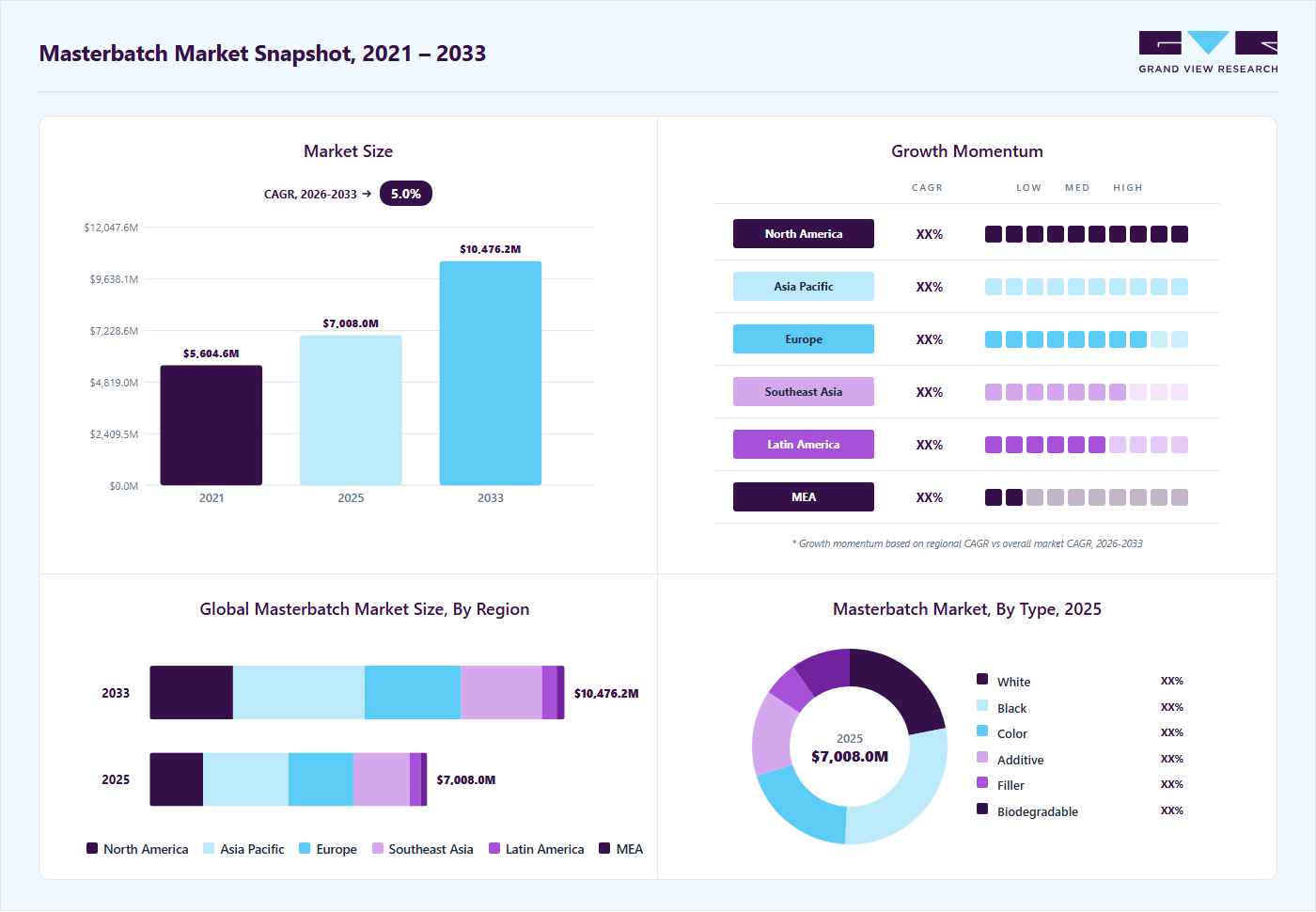

The global masterbatch market size was valued at USD 7.0 billion in 2025 and is projected to grow from USD 7.4 billion in 2026 to USD 10.5 billion by 2033, at a CAGR of 5.0% from 2026 to 2033. The Asia Pacific held the largest revenue share of 30.7% of the global market in 2025. Growing consumption of flexible and rigid plastic packaging across food, beverages, personal care, and household products is driving demand for masterbatches used for coloring, UV stabilization, and functional enhancement.

Key Market Trends & Insights

- By type: Black segment dominated the market, with a revenue share of 28.8% in 2025.

- By carrier polymer: Polypropylene (PP) segment held the largest revenue share of 26.8% in 2025.

- By end use: Packaging segment accounted for the largest revenue share of 27.2% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (30.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

Market Size & Forecast

- Market size in 2025: USD 7.0 Billion

- Estimated market size in 2026: USD 7.4 Billion

- Projected market size by 2033: USD 10.5 Billion

- CAGR (2026-2033): 5.0%

Brand owners are increasingly focusing on product differentiation, shelf appeal, and extended shelf life, which boosts the adoption of high-performance color and additive masterbatches in mass-volume packaging applications. The increasing use of lightweight, durable plastic components in automotive and construction sectors is accelerating masterbatch demand for performance enhancement, including heat resistance, flame retardancy, and weather stability. As manufacturers shift toward cost-efficient and high-strength polymer solutions to meet regulatory and sustainability requirements, masterbatches play a critical role in improving material performance and processing efficiency.

")

Rising regulatory pressure and brand-level sustainability commitments are creating strong opportunities for bio-based, recyclable, and additive masterbatches that support circular economy goals. Manufacturers offering solutions such as carbon-black alternatives, biodegradable carrier resins, and masterbatches compatible with recycled polymers can gain a competitive advantage, as converters increasingly seek materials that maintain performance while reducing environmental impact and compliance risks.

Market Concentration & Characteristics

The masterbatch market is moderately consolidated, with a mix of large multinational players and numerous regional manufacturers competing across commodity and specialty segments. Global leaders benefit from strong R&D capabilities, broad product portfolios, and long-term relationships with polymer processors, enabling them to serve high-volume packaging, automotive, and construction applications. However, regional players remain competitive by offering cost-effective solutions, localized supply, and customized formulations tailored to specific end-use requirements.

Industry competition is primarily driven by product performance, consistency, pricing, and technical support, rather than branding alone. Demand is characterized by high volume consumption in color masterbatches and faster growth in additive and specialty masterbatches that enhance functionality and sustainability. The market exhibits strong customer stickiness due to qualification processes and formulation-specific requirements, while innovation in sustainable and high-performance masterbatches continues to shape competitive differentiation.

Type Insights

The black segment dominated the global industry with the largest revenue share of 28.8% in 2025. The widespread use of carbon black masterbatches in packaging, automotive, and construction plastics drives segment dominance due to their superior UV resistance, electrical conductivity, and cost-effectiveness. Consistent demand from pipes, films, and molded components requiring durability and long service life reinforces the strong market position of black masterbatches.

The white segment is expected to grow significantly with a CAGR of 7.1% during the forecast period. Rising demand for high-opacity, brightness, and cost-efficient pigmentation in flexible packaging, consumer goods, and agricultural films is driving the growth of white masterbatches. Increased use of titanium dioxide–based solutions to enhance aesthetics, UV protection, and material performance across high-volume plastic applications continues to support strong adoption.

Carrier Polymer Insights

The polypropylene (PP) segment dominated the global industry with the largest revenue share of 26.8% in 2025. The extensive use of polypropylene across packaging, automotive, consumer goods, and industrial applications drives strong demand for PP-based masterbatches due to their excellent compatibility, processability, and cost efficiency. High consumption volumes and widespread adoption in injection molding and extrusion processes reinforce PP’s dominant position as a carrier polymer.

The polyethylene (PE) segment is expected to grow at the fastest CAGR of 7.2% during the forecast period. Rapid growth in flexible packaging, agricultural films, and stretch and shrink applications is accelerating demand for PE-based masterbatches. Increasing use of LDPE and LLDPE in lightweight, high-performance films, along with rising sustainability-driven film innovations, supports the strong growth of PE as a carrier polymer.

End-use Insights

The packaging segment dominated the industry with the largest revenue share of 27.2% in 2025. The high-volume use of plastics in flexible and rigid packaging across food, beverages, and consumer goods drives dominant demand for masterbatches used for coloration, protection, and functional enhancement. Continuous focus on shelf appeal, product differentiation, and extended shelf life sustains strong masterbatch consumption in packaging applications.

Automotive & Transportation is expected to grow significantly with a CAGR of 7.0% during the forecast period. Increasing adoption of lightweight plastic components to improve fuel efficiency and meet emission regulations is driving growth in automotive and transportation applications. Masterbatches enabling heat resistance, UV stability, and aesthetic consistency are increasingly used in interior and exterior vehicle components, supporting sustained market expansion.

Regional Insights

Asia Pacific masterbatch market led the global industry with a 30.7% revenue share in 2025. Rapid industrialization, expanding packaging demand, and strong growth in consumer goods manufacturing drive market expansion across Asia Pacific. High plastic consumption volumes, cost-competitive production, and increasing investments in automotive and infrastructure support the region’s leading growth momentum.

The China masterbatch market dominated Asia Pacific with a revenue share of 47.7% in 2025. China’s large-scale plastic manufacturing base and strong demand from the packaging, consumer goods, and automotive sectors drive robust masterbatch consumption. Rapid capacity expansion, cost-efficient production, and increasing focus on functional and specialty masterbatches to meet quality and sustainability requirements support continued market growth.

North America Masterbatch Market Trends

The masterbatch industry in North America is expected to grow at a CAGR of 5.5% during the forecast period. Strong demand from packaging, automotive, and construction industries drives masterbatch consumption, supported by advanced polymer processing capabilities and high adoption of specialty additives. Regulatory focus on performance, safety, and sustainability further accelerates demand for high value masterbatch solutions.

U.S. Masterbatch Market Trends

The masterbatch industry in the U.S. is driven by high consumption of plastics in packaging and automotive applications, along with strong demand for high-performance and specialty masterbatches. Innovation in sustainable materials and advanced polymer processing strengthens demand across end-use industries.

Europe Masterbatch Market Trends

Themasterbatch industry in Europe accounted for a global revenue share of 23.4% in 2025. Stringent environmental regulations and circular economy initiatives are driving the adoption of sustainable, recyclable, and specialty masterbatches. The region’s strong automotive and packaging sectors, combined with innovation in lightweight and high-performance plastics, support steady market growth.

Germany’s strong automotive and industrial manufacturing base drives demand for high-performance masterbatches used in engineered plastics. Emphasis on lightweighting, quality standards, and sustainable material solutions reinforces consistent market growth.

Middle East & Africa Masterbatch Market Trends

The masterbatch industry in the Middle East is driven by the growing investments in construction, infrastructure, and packaging, supported by expanding polymer production capacity. Rising urbanization and increasing adoption of plastic packaging in food and consumer goods further support market growth.

Latin America Masterbatch Market Trends

Themasterbatch industry in Latin America is driven by expanding food packaging, agriculture, and consumer goods industries, which are driving demand for color and additive masterbatches. Improving manufacturing capabilities and rising plastic consumption across key economies support gradual market expansion.

Key Masterbatch Company Insights

Key players such as Schulman, Inc., Ampacet Corporation, Cabot Corporation, and Clariant AG dominate the masterbatch market through strong global manufacturing footprints, broad color and additive portfolios, and continuous innovation in high-performance and sustainable masterbatch solutions.

-

Schulman, Inc. is a leading player in the masterbatch market, recognized for its comprehensive portfolio of color and additive masterbatches serving packaging, automotive, consumer goods, and industrial applications. The company leverages strong formulation expertise, global manufacturing capabilities, and customer-centric customization to deliver consistent product performance and long-term value across high-volume and specialty plastic applications.

-

Ampacet Corporation is a prominent masterbatch manufacturer with a strong focus on color, special effects, and functional additive solutions for the plastics industry. The company’s competitive strength lies in its advanced R&D capabilities, broad global presence, and ability to develop application-specific masterbatches that support product differentiation, processing efficiency, and sustainability objectives across diverse end-use markets.

Key Masterbatch Companies:

The following key companies have been profiled for this study on the masterbatch market.

- Schulman, Inc.

- Ampacet Corporation

- Cabot Corporation

- Clariant AG

- Global Colors Group

- Hubron International Ltd.

- Penn Color, Inc.

- Plastiblends India Ltd.

- Tosaf Group

- PolyOne Corporation

Recent Developments

- In January 2024, Hubron International Ltd. and Black Swan Graphene Inc. entered a commercial agreement to expedite the use of Black Swan's graphene products. Hubron, a specialist in plastic masterbatch and conductive compounds, incorporates graphene to improve functionality in masterbatch solutions. This collaboration aims to integrate graphene into various sectors such as automotive, construction, and packaging, leveraging Hubron's market reach and expertise in masterbatch production.

Masterbatch Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 7.0 billion

Estimated Market size in 2026

USD 7.4 billion

Projected Market size by 2033

USD 10.5 billion

Growth rate

CAGR of 5.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2018 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in kilotons, revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, carrier polymers, end-use, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; Southeast Asia; Brazil; Argentina

Key companies profiled

Schulman, Inc.; Ampacet Corporation; Cabot Corporation; Clariant AG; Global Colors Group; Hubron International Ltd.; Penn Color; Plastiblends India Ltd.; Tosaf Group PolyOne Corporation

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Masterbatch Market Report Segmentation

This report forecasts volume & revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global masterbatch market report based on type, carrier polymer, end-use, and region:

-

Type Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

White

-

Black

-

Color

-

Additive

-

Filler

-

Biodegradable

-

-

Carrier Polymer Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Polypropylene (PP)

-

Polyethylene (PE)

-

Polyvinyl Chloride (PVC)

-

Polyethylene Terephthalate (PET)

-

Biodegradable Plastics

-

-

End-use Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Packaging

-

Building & Construction

-

Consumer Goods

-

Automotive & Transportation

-

Agriculture

-

Other End Users

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Southeast Asia

-

Malaysia

-

Thailand

-

Vietnam

-

Singapore

-

Indonesia

-

Philippines

-

Rest of Southeast Asia

-

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Frequently Asked Questions About This Report

Asia Pacific dominated the market with a 30.7% revenue share in 2025.

Asia Pacific remains the leading regional growth engine due to rapid industrialization, expanding packaging demand, and cost-competitive production infrastructure.

Black dominated the global masterbatch market with the largest revenue share of 28.8% in 2025. The widespread use of carbon black masterbatches in packaging, automotive, and construction plastics drives segment dominance due to their superior UV resistance, electrical conductivity, and cost-effectiveness. Consistent demand from pipes, films, and molded components requiring durability and long service life reinforces the strong market position of black masterbatches.

Some of the key players operating in the masterbatch market include Schulman, Inc., Ampacet Corporation, Cabot Corporation, Clariant AG, Global Colors Group., Hubron International Ltd., etc.

Growing consumption of flexible and rigid plastic packaging across food, beverages, personal care, and household products is driving demand for masterbatches used for coloring, UV stabilization, and functional enhancement. Brand owners are increasingly focusing on product differentiation, shelf appeal, and extended shelf life, which boosts adoption of high-performance color and additive masterbatches in mass-volume packaging applications.

The global masterbatch market is expected to grow at a compound annual growth rate of 5.0% from 2026 to 2033 to reach USD 10.5 billion by 2033.

Polypropylene (PP) held a dominant revenue share in 2025 due to its versatility, while Polyethylene (PE) is the fastest-growing segment with a 7.2% CAGR.

The packaging segment held the highest share with 27.2% in 2025, while Automotive & Transportation is expected to grow at a significant CAGR of 7.0% from 2026 to 2033.

The global masterbatch market size was estimated at USD 7.0 billion in 2025 and is expected to reach USD 7.4 billion in 2026.

About the Author(s)

Paints, Coatings & Printing Inks Research Team

Bulk Chemicals · Paints, Coatings & Printing InksThis report was authored by the paints, coatings & printing inks research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the paints, coatings & printing inks segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.