- Home

- »

- Distribution & Utilities

- »

-

Offshore Wind Market Size And Share Report, 2026-2033GVR Report cover

![Offshore Wind Market (2026 - 2033)Report]()

Offshore Wind Market (2026 - 2033)

Size, Share & Trends Analysis Report By Installation (Biofuel, Hydrogen Fuel, Power to Liquid Fuel, Gas-to-Liquid), By Capacity (Up to 3 MW, 3 MW to 5 MW, Above 5 MW), By Water Depth, By Region, And Segment Forecasts

Market Size, 2025

$42.3BMarket Estimate, 2026

$45.2BMarket Forecast, 2033

$93.5BCAGR, 2026–2033

10.9%Offshore Wind Market Summary

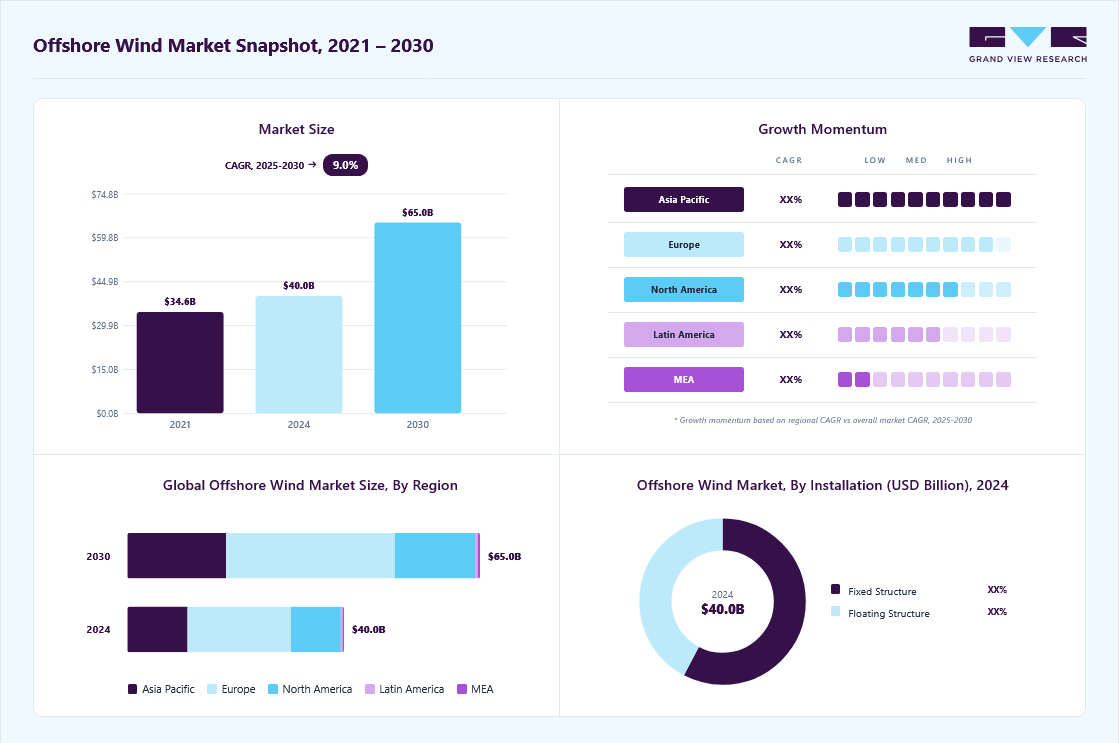

The global offshore wind market size was valued at USD 42.3 billion in 2025 and is projected to grow from USD 45.2 billion in 2026 to USD 93.5 billion by 2033, at a CAGR of 10.9% from 2026 to 2033. Europe dominated the offshore wind market with the largest revenue share of 47.7% in 2025. The market is expected to expand due to growing interest in decreasing the global carbon footprint and increased demand for renewable energy sources.

Key Market Trends & Insights

- By installation: Fixed structure segment held the largest market share of 74.4% in 2025.

- By capacity: Above 5 MW segment held the largest market share of 49.6% in 2025.

- By water depth: Shallow water (<30 m depth) segment held the largest market share of 49.1% in 2025.

Regional Highlights

- Largest regional market: Europe (47.7% revenue share, 2025)

- By country: Germany held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 42.3 Billion

- Estimated market size in 2026: USD 45.2 Billion

- Projected market size by 2033: USD 93.5 Billion

- CAGR (2026-2033): 10.9%

The growing efforts of government bodies and electrical companies to reduce carbon emissions are the primary market drivers boosting market expansion. The offshore wind industry in the U.S. is predicted to experience significant growth in recent years, with several factors driving this expansion. The rise in the expansion of industrial industry, including wind power, owing to the growing need for a dependable, clean, affordable, and diverse electricity supply, is expected to boost the market growth in the country. For instance, the President of the United States announced a bold plan to install 30 gigawatt-hours (GW) of offshore wind by 2030, which would provide sustainable energy to 10 million homes, along with supporting 77,000 jobs, and encourage private investment throughout the supply chain.")

Offshore wind is a substantial clean energy solution for large population centers seeking to get more of their power from clean sources, and lowering costs makes it more affordable.The country is predicted to drive demand for offshore wind, which is expected to propel the market growth in the coming years.

The increasing intervention of the U.S. Department of Energy’s Bioenergy Technologies and other organizations is projected to fuel the growth of the offshore wind industry in the U.S. over the forecast period. Moreover, the rise in continued research, development, demonstration, and deployment of technologies to eliminate impediments to the widespread installation of offshore wind in the country is likely to drive the market growth in the forecast period.

Market Dynamics

The offshore wind market is experiencing strong growth as countries accelerate investments in renewable energy to meet decarbonization targets and enhance energy security. Rising electricity demand, supportive government policies, and large-scale offshore wind auctions are driving new project developments across Europe, Asia-Pacific, and North America. Technological advancements, including larger turbines and floating offshore wind platforms, are improving energy generation efficiency and expanding deployment in deeper waters. However, the market faces challenges related to high upfront capital costs, supply chain constraints, permitting delays, and grid connection complexities. Despite these hurdles, increasing public and private sector investments, along with declining project costs over the long term, continue to create significant growth opportunities for the offshore wind industry.

Government procurement programs, renewable energy targets, and competitive offshore wind auctions are playing a critical role in accelerating the offshore wind market. Many countries are establishing long-term deployment goals and offering lease auctions, power purchase agreements, and financial incentives to encourage private investment in offshore wind projects. These initiatives reduce investment risks, improve project visibility, and support the development of large-scale offshore wind capacity. As governments seek to strengthen energy security and achieve net-zero emission objectives, public sector support continues to create a strong pipeline of future offshore wind projects worldwide.

In December 2025, Poland completed its first competitive offshore wind auction, awarding support for 3.4 GW of offshore wind capacity in the Baltic Sea. The government-backed auction offered long-term contracts for difference, ensuring revenue stability for developers and strengthening investor confidence. The initiative forms part of Poland’s strategy to expand renewable energy generation and reduce dependence on conventional power sources, highlighting the critical role of government procurement in driving offshore wind market growth.

The offshore wind market is facing increasing financial pressure due to rising capital expenditure and elevated global interest rates. Significant increases in the costs of steel, copper, turbines, foundations, subsea cables, labor, and logistics have substantially increased project development expenses. Higher borrowing costs have made financing large-scale offshore wind projects more expensive, reducing project profitability and delaying final investment decisions. These challenges are particularly impactful for projects that secured power purchase agreements or auction contracts before the recent surge in costs, limiting developers' ability to pass additional expenses to customers. In 2025, Ørsted reported continued pressure on offshore wind project economics due to inflation, supply chain costs, and elevated interest rates affecting the global renewable energy sector. The company highlighted that higher costs for equipment, installation, and financing have increased overall project CAPEX and impacted expected returns on several offshore wind developments.

Floating offshore wind represents one of the most significant growth opportunities in the offshore wind market, enabling wind energy generation in deep-water areas where traditional fixed-bottom foundations are not technically or economically feasible. As suitable shallow-water sites become increasingly limited, floating platforms allow developers to access stronger and more consistent wind resources located farther offshore. Continued advancements in floating foundation technologies, coupled with supportive government policies and pilot project success, are expected to accelerate commercial deployment. In 2025, the United Kingdom advanced its floating offshore wind ambitions through the Celtic Sea leasing round led by The Crown Estate. The initiative aims to support several gigawatts of floating offshore wind capacity in deep-water regions off the coasts of Wales and Southwest England, areas unsuitable for conventional fixed-bottom turbines.

Analyst Perspective

The offshore wind market is growing as countries invest in clean energy to reduce emissions and strengthen energy security. Larger turbines, improved installation technologies, and growing government support are helping make offshore wind projects more efficient and commercially viable. While high project costs, financing challenges, and supply chain constraints continue to impact project development, long-term demand remains strong. The emergence of floating offshore wind is also opening new opportunities in deeper waters, expanding the market's future growth potential. Overall, offshore wind is becoming an increasingly important part of the global renewable energy mix and is expected to attract significant investment over the coming years.

Capacity Insights

Based on capacity, the above 5 MW segment led the market with the largest revenue share of 49.6% in 2025, due to advanced capacity and low cost. Higher power rating turbines are in high demand in order to make offshore wind power generation more energy-efficient and economically sustainable. Large-scale offshore wind projects benefit from economies of scale, making them more cost-effective in terms of power generation per megawatt-hour (MWh).

The expansion of offshore wind projects with capacities ranging from 3 MW to 5 MW represents a key component of the offshore wind industry. Offshore wind projects ranging from 3 MW to 5 MW provide a good blend of scale and flexibility. They are adaptable to diverse wind conditions and water depths, making them useful for a wide range of applications. These factors are likely to boost the segment demand in the coming years.

Installation Insights

Based on installation, the fixed structure segment led the market with the largest revenue share of 74.4% in 2025, due to a variety of factors, including ease of operation and cost-effectiveness. The growing desire for sustainable energy sources is a crucial driver driving industry expansion, and the fixed structure installation segment is likely to create significant revenue in the coming years.

The wind turbine technological advances segment is projected to grow at the fastest CAGR over the forecast period. The market is expanding due to the growing need for clean energy, and the fixed structure installation segment is likely to play a key role in most nations around the globe in achieving the renewable target.

Water Depth Insights

Based on water depth, the shallow water (<30 M Depth) segment led the market with the largest revenue share of 49.1% in 2025. The presence of considerably less demanding weather and ease of maintenance makes it a suitable choice for the establishment of offshore wind farms.

Moreover, shallow water installations are less expensive than deep-water installations, making them a cost-effective choice for large population centers seeking to source more of their power from clean sources. The offshore wind industry is predicted to expand internationally as investments in renewable energy increase. This factor is expected to boost the shallow water installation industry.

Regional Insights

The offshore wind market in North America is expected to experience at a steady CAGR throughout the forecast period, driven by a combination of recovery efforts post-pandemic and the increasing focus on sustainability. A combination of supportive policies, technological advancements, and a growing demand for clean energy propels the North American market. Federal initiatives, such as the Inflation Reduction Act, have provided tax incentives and funding programs that bolster the sector.

U.S. Offshore Wind Market Trends

The offshore wind market in the U.S. is anticipated to grow at a significant CAGR during the forecast period. In addition, several U.S. states have set ambitious renewable energy targets, further stimulating investment and development in offshore wind projects. Technological innovations, including the development of larger and more efficient turbines, have enhanced the feasibility and cost-effectiveness of offshore wind energy. These advancements enable the harnessing of stronger and more reliable wind resources in deeper sea locations, expanding the potential for offshore wind deployment.

Asia Pacific Offshore Wind Market Trends

The offshore wind market in Asia Pacific is experiencing robust growth, driven by a confluence of factors. Foremost among these is the strong commitment of regional governments to renewable energy targets. Countries like China, Japan, South Korea, and Taiwan have implemented policies and incentives to promote offshore wind development, aiming to diversify their energy mix and reduce carbon emissions. This policy support has attracted significant investments from both domestic and international stakeholders, fostering an environment conducive to the expansion of offshore wind projects.

Technological advancements are also propelling the market forward. Innovations in turbine design, such as the development of larger and more efficient turbines, have enhanced the feasibility and cost-effectiveness of offshore wind energy. In addition, the region's extensive coastlines and favorable wind conditions provide an ideal setting for offshore wind farms. The combination of supportive policies, technological progress, and natural advantages positions the Asia-Pacific region as a significant player in the global offshore wind industry.

Europe Offshore Wind Market Trends

Europe dominated the offshore wind market with the largest revenue share of 47.7% in 2025, driven by ambitious climate policies, technological advancements, and regional cooperation. The European Union's Renewable Energy Directive, adopted in 2023, sets a target for renewables to comprise at least 42.5% of the energy mix by 2030, necessitating substantial increases in wind capacity. To support this, the European Commission introduced the European Wind Power Action Plan in October 2023, aiming to streamline wind energy deployment by expediting permitting processes and enhancing auction designs. Furthermore, collaborative initiatives like the North Seas Energy Cooperation foster integrated offshore energy grids, linking wind farms across northern Europe to optimize energy production and distribution.

Germany Offshore Wind Market Trends

The offshore wind market in Germany held the largest share in the Europe region in 2025.

Latin America Offshore Wind Market Trends

The offshore wind market in Latin America is poised for significant growth, driven by favorable natural conditions, supportive government policies, and increasing demand for renewable energy. Countries like Brazil and Colombia are at the forefront, leveraging their extensive coastlines and strong wind resources to develop offshore wind projects. Brazil, for instance, has initiated legislative processes to regulate offshore energy, aiming to allocate seabed areas for wind projects. At the same time, Colombia has attracted interest from multiple international and local companies for its offshore wind initiatives. These developments are part of broader national strategies to diversify energy sources and reduce carbon emissions.

Middle East & Africa Offshore Wind Market Trends

The offshore wind market in Middle East & Africa is gaining momentum, driven by a combination of abundant natural resources, strategic policy shifts, and technological advancements. Countries like Saudi Arabia, the United Arab Emirates (UAE), and Oman are exploring offshore wind projects to diversify their energy portfolios and reduce reliance on fossil fuels. The region's vast coastlines along the Red Sea and Arabian Gulf offer favorable wind conditions, making them ideal for offshore wind development. In addition, initiatives like Saudi Arabia's Vision 2030 and the UAE's renewable energy targets are fostering an environment conducive to renewable energy investments.

Key Offshore Wind Company Insights

The global offshore wind industry is a highly competitive market due to the presence of major industries across the region, as these companies are comparatively concentrated and fiercely competitive, along with acquisitions, mergers, and collaborations.

Key Offshore Wind Companies:

The following are the leading companies in the offshore wind market.

-

General Electric

-

Vestas

-

Shanghai Electric Wind Power Equipment Co.

-

Siemens Gamesa

-

Doosan Heavy Industries and Construction

-

Hitachi

-

Rockwell Automation

-

Nordex SE

-

Hyundai Motor Group

-

Schneider Electric

-

Zhejiang Windey Co.

-

Taiyuan Heavy Industry Co.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (General Electric; Vestas; Siemens Gamesa; Equinor ASA; Shanghai Electric Wind Power Equipment Co.; Schneider Electric)

- Invest in larger turbine platforms and next-generation offshore wind technologies.

- Expand project pipelines through government auctions, strategic partnerships, and long-term power purchase agreements.

- Strengthen global manufacturing, installation, and service networks to support large-scale deployments.

- Strong brand recognition and established relationships with utilities, developers, and governments.

- Extensive offshore project experience and proven technology performance.

- Large manufacturing capacity, global supply chains, and strong financial resources.

- High exposure to supply chain disruptions, raw material cost inflation, and project delays.

- Significant capital requirements for R&D, manufacturing expansion, and project development.

- Margin pressure from competitive bidding processes and rising financing costs.

Emerging Players (Doosan Heavy Industries and Construction; Hitachi; Rockwell Automation; Hyundai Motor Group; Zhejiang Windey Co.; Taiyuan Heavy Industry Co.)

- Focus on regional offshore wind opportunities and niche technology offerings.

- Expand presence through partnerships with developers, utilities, and established OEMs.

- Invest in component manufacturing, automation solutions, and supporting offshore wind infrastructure.

- Greater flexibility in adopting new technologies and business models.

- Strong regional market knowledge and access to local supply networks.

- Ability to target specialized segments such as automation, electrical systems, foundations, and offshore equipment.

- Limited global project references and offshore wind track record.

- Smaller production scale and lower financial capacity compared to market leaders.

- Dependence on partnerships and third-party developers for project participation.

Recent Developments

-

For Instance, in February 2023, Siemens Gamesa announced its plan to develop a substantial offshore nacelle manufacturing facility in New York State. The facility will be built at the Port of Coeymans. It would represent a $500 million investment in the community and generate over 420 direct jobs.

Offshore Wind Market Report Scope

Report Attribute

Details

Market Definition

The offshore wind market refers to the installation of wind turbines in offshore waters to generate electricity, with market size measured based on newly installed capacity and associated installation revenues across fixed-bottom and floating wind projects.

Market size in 2025

USD 42.3 billion

Estimated market size in 2026

USD 45.2 billion

Projected market size by 2033

USD 93.5 billion

Growth rate

CAGR of 10.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Billion, Capacity in MW and CAGR from 2026 to 2033

Report coverage

Revenue forecast, capacity forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Installation, capacity, water depth, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; The Netherlands; China; India; Japan; South Korea; Australia; Malaysia; Singapore; Thailand; Vietnam; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

General Electric; Vestas; Shanghai Electric Wind Power Equipment Co.; Siemens Gamesa; Doosan Heavy Industries and Construction; Hitachi; Rockwell Automation; Equinor ASA; Hyundai Motor Group; Schneider Electric; Zhejiang Windey Co.; Taiyuan Heavy Industry Co.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Offshore Wind Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. Forthis study, Grand View Research has segmented the global offshore wind market report based on installation, capacity, water depth, and region:

-

Installation Outlook (Volume, MW; Revenue, USD Billion, 2021 - 2033)

-

Fixed Structure

-

Floating Structure

-

-

Capacity Outlook (Volume, MW; Revenue, USD Billion, 2021 - 2033)

-

Up to 3 MW

-

3 MW to 5 MW

-

Above 5 MW

-

-

Water Depth Outlook (Volume, MW;Revenue, USD Billion, 2021 - 2033)

-

Shallow Water (<30 M Depth)

-

Transitional Water (30-60 M Depth)

-

Deepwater (More than 60 M Depth)

-

-

Regional Outlook (Volume, MW; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Malaysia

-

Singapore

-

Thailand

-

Vietnam

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Research Methodology

The offshore wind market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each offshore wind segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Installation

Revenue capture definition

Fixed Structure

Captures the value of offshore wind capacity installed using fixed-bottom foundations such as monopiles, jackets, gravity-based structures, and tripods anchored directly to the seabed.

Floating Structure

Includes offshore wind projects deployed on floating platforms secured by mooring systems, primarily in deeper waters where fixed-bottom foundations are not technically feasible.

Segment - Capacity

Revenue capture definition

Up to 3 MW

Covers offshore wind installations utilizing turbines with a rated capacity of up to 3 MW.

3 MW to 5 MW

Represents offshore wind projects employing turbines with a rated capacity ranging from 3 MW to 5 MW.

Above 5 MW

Revenue generated from installation of high-capacity offshore wind turbines exceeding 5 MW, including utility-scale and next-generation turbine deployments.

Segment - Water Depth

Revenue capture definition

Shallow Water (<30 M Depth)

Accounts for offshore wind projects installed in waters less than 30 meters deep, where fixed-bottom foundation technologies are most commonly used.

Transitional Water (30-60 M Depth)

Includes offshore wind developments located in water depths between 30 and 60 meters, requiring specialized foundation and installation solutions.

Deepwater (More than 60 M Depth)

Covers offshore wind installations in waters deeper than 60 meters, where floating foundation technologies are increasingly deployed to harness wind resources.

Estimation Model

Layer Name

Key Question

Description

Offshore Wind Project Pipeline Layer

What forms the demand base?

Identify announced, under-construction, and commissioned offshore wind projects across key regions. Assess planned capacity additions, government targets, auction awards, developer pipelines, and project timelines to establish the addressable installation base.

Installation & Structure Layer

What type of installations are being deployed?

Evaluate installed capacity by fixed structure and floating structure. Assess suitability based on water depth, seabed conditions, distance from shore, technology maturity, and project economics.

Turbine Capacity & Water Depth Layer

What technical factors shape installation value?

Analyze offshore wind installations by turbine capacity range and water depth category. Higher-capacity turbines and deeper-water projects generally involve larger equipment, specialized foundations, complex installation requirements, and higher project value.

Revenue Conversion & Validation Layer

How is market size calculated and validated?

Convert installed capacity in MW into market revenue using average installation cost per MW across structure type, turbine capacity, water depth, region, and project complexity. Validate estimates through project-level data, auction results, developer announcements, CAPEX benchmarks, and regional offshore wind deployment trends.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Growth Opportunity Assessment

Conducted a comprehensive assessment of growth opportunities across fixed-bottom and floating offshore wind projects, evaluating capacity addition trends, project pipelines, emerging offshore wind markets, deepwater development potential, and investment activity. The study also analyzed government targets, auction programs, grid expansion initiatives, and future deployment prospects across key regions.

Enabled identification of high-growth markets, supported investment prioritization, informed expansion strategies, and highlighted future revenue opportunities across the offshore wind value chain.

Technology Benchmarking Assessment

Evaluated offshore wind technologies based on foundation type, turbine capacity, water depth suitability, installation requirements, operational performance, project economics, and commercial maturity. The assessment compared fixed-bottom and floating offshore wind technologies while analyzing advancements in turbine design, foundation systems, and installation methodologies.

Supported technology selection, investment evaluation, project planning, and identification of commercially viable offshore wind solutions across different deployment environments.

Competitive Landscape Assessment

Detailed competitive landscape analysis covering offshore wind turbine manufacturers, project developers, EPC contractors, and technology providers. The study profiled key participants based on geographic presence, project portfolio, installed capacity, technology capabilities, strategic partnerships, manufacturing footprint, investment activity, and expansion initiatives.

Enabled evaluation of competitive positioning, market leadership, technology differentiation, strategic capabilities, and growth strategies adopted by key participants in the offshore wind market.

Frequently Asked Questions About This Report

The offshore wind market size was estimated at USD 42.3 billion in 2025 and is expected to reach USD 45.2 billion in 2026.

The offshore wind market is expected to grow at a CAGR of 10.9% from 2026 to 2033 to reach USD 93.5 billion by 2033.

Germany dominated the Europe region market with a revenue share of 34.0% in 2025.

Based on installation, the fixed structure segment accounted for largest revenue share of 74.4% in 2025.

Based on capacity, the above 5 MW segment accounted for largest revenue share of 49.6% in 2025.

The key players operating in the offshore wind market are General Electric; Vestas; Shanghai Electric Wind Power Equipment Co.; Siemens Gamesa; Doosan Heavy Industries and Construction; Hitachi; Rockwell Automation; Equinor ASA; Hyundai Motor Group; Schneider Electric; Zhejiang Windey Co.; Taiyuan Heavy Industry Co.; and others.

The offshore wind market is driven by supportive government policies, renewable energy targets, growing demand for clean electricity, technological advancements in turbine systems, and increasing investments in large-scale offshore wind projects.

The Europe region dominated the offshore wind market with a revenue share of 47.7% in 2025.

Asia Pacific is anticipated to register the fastest CAGR of 11.1% over the forecast period.

About the Author(s)

Distribution & Utilities Research Team

Energy & Power · Distribution & UtilitiesThis report was authored by the distribution & utilities research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the distribution & utilities segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.