- Home

- »

- Plastics, Polymers & Resins

- »

-

Pharmaceutical Cold Chain Packaging Market Report, 2033GVR Report cover

![Pharmaceutical Cold Chain Packaging Market Size, Share & Trends Report]()

Pharmaceutical Cold Chain Packaging Market (2025 - 2033) Size, Share & Trends Analysis Report By Material (Plastic, Paper, Metal), By Product (Small Boxes, Pallets, Large Sized Pallet Containers), By End Use, By Region, And Segment Forecasts

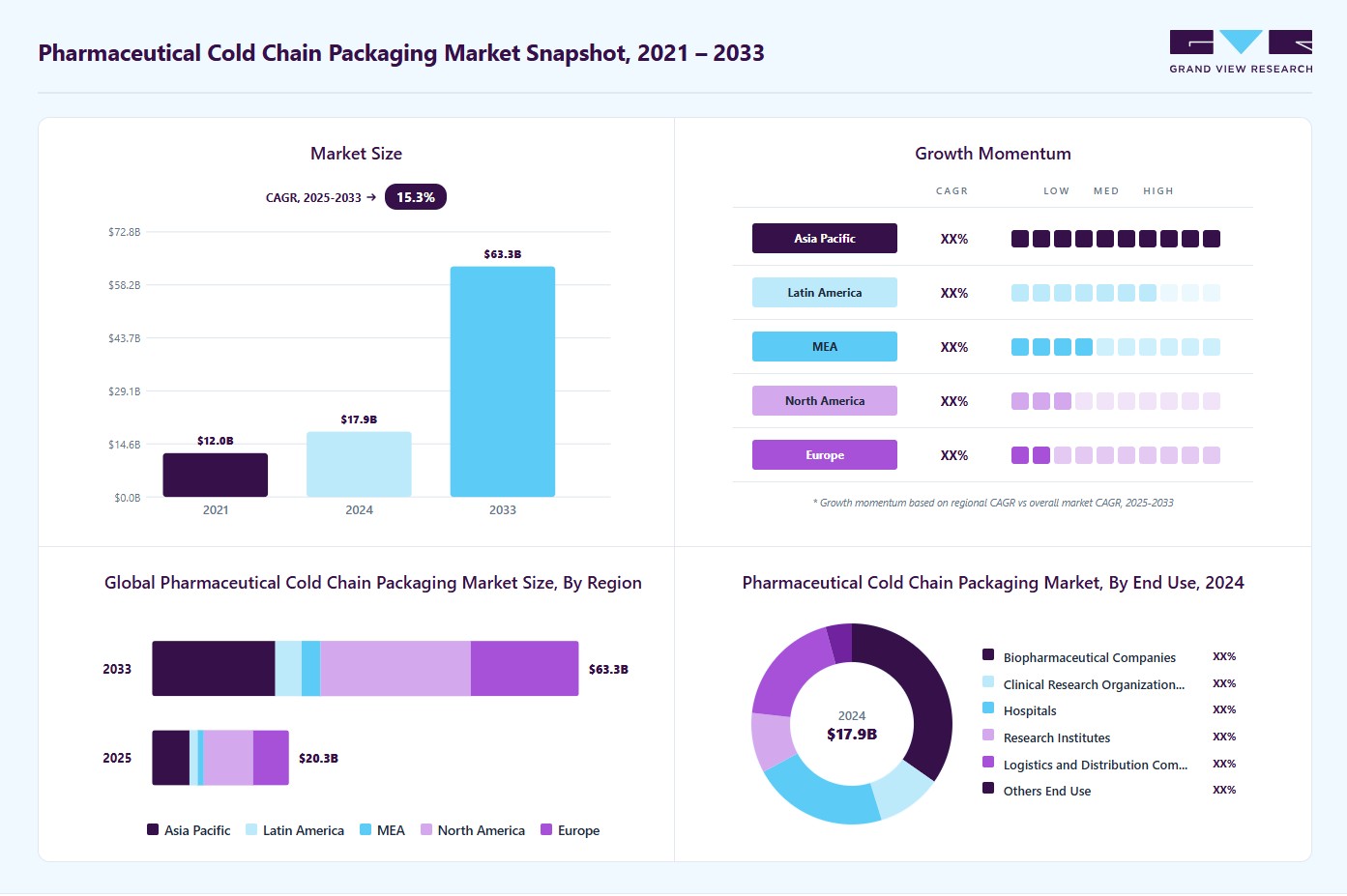

Market Size, 2024

$17.9BMarket Estimate, 2026

$20.3BMarket Forecast, 2033

$63.3BCAGR, 2025–2033

15.3%Pharmaceutical Cold Chain Packaging Market Summary

The global pharmaceutical cold chain packaging market size was estimated at USD 17.93 billion in 2024 and is projected to reach USD 63.30 billion by 2033, growing at a CAGR of 15.3% from 2025 to 2033. The market is driven by the rising demand for temperature-sensitive biologics, vaccines, and specialty drugs that require strict thermal protection during storage and transportation.

Key Market Trends & Insights

- North America dominated the pharmaceutical cold chain packaging market with the largest revenue share of over 36.0% in 2024.

- The pharmaceutical cold chain packaging market in China is expected to grow at a substantial CAGR of 16.8% from 2025 to 2033.

- By material, the paper segment is expected to grow at a considerable CAGR of 16.4% from 2025 to 2033 in terms of revenue.

- By product, the pallets segment is expected to grow at a considerable CAGR of 15.9% from 2025 to 2033 in terms of revenue.

- By end use, the hospitals segment is expected to grow at a considerable CAGR of 16.5% from 2025 to 2033 in terms of revenue.

Market Size & Forecast

- 2024 Market Size: USD 17.93 Billion

- 2033 Projected Market Size: USD 63.30 Billion

- CAGR (2025-2033): 15.3%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Additionally, stringent regulatory guidelines for maintaining product integrity and safety are fueling investments in advanced cold chain packaging solutions. Biologics, including monoclonal antibodies and cell & gene therapies, are highly sensitive to temperature fluctuations and must be stored between 2°C to 8°C or even at ultra-low temperatures of -80°C. For instance, during the COVID-19 pandemic, vaccines from Pfizer-BioNTech and Moderna highlighted the critical role of advanced cold chain packaging systems, such as insulated shippers and phase change materials, to ensure safe delivery worldwide. The continued growth of biologics pipelines is fueling investments in robust packaging solutions that can handle stringent thermal requirements.With the globalization of the pharmaceutical industry, products are increasingly being manufactured in one region and distributed across multiple continents. This has intensified the need for reliable cold chain packaging solutions that can withstand long transit times, diverse climatic conditions, and multiple handling points. For example, Indian pharmaceutical manufacturers, who are among the largest exporters of generic drugs and vaccines, heavily depend on high-performance cold chain packaging to reach markets in North America, Europe, and Africa. As international trade volumes grow, particularly in emerging markets, demand for advanced cold chain packaging technologies such as vacuum-insulated panels, smart containers, and real-time monitoring systems is expected to surge.

")

Regulatory authorities such as the U.S. FDA, European Medicines Agency (EMA), and World Health Organization (WHO) mandate strict guidelines for the storage, handling, and transport of temperature-sensitive pharmaceuticals. Compliance with Good Distribution Practices (GDP) and Good Manufacturing Practices (GMP) necessitates the adoption of validated cold chain packaging solutions that ensure consistent product integrity.

Advancements in cold chain packaging technologies, combined with growing emphasis on sustainability, are accelerating market expansion. Packaging solutions are becoming smarter, lighter, and eco-friendlier, offering extended thermal protection while reducing carbon footprint. Companies are adopting reusable insulated containers, recyclable phase change materials, and AI-enabled monitoring systems to enhance performance and efficiency. For example, Pelican BioThermal and Sonoco ThermoSafe offers reusable systems that not only meet strict temperature requirements but also align with the pharmaceutical industry's sustainability goals. These innovations not only help reduce costs over time but also appeal to regulators and consumers seeking greener supply chain practices.

Market Concentration & Characteristics

The industry is innovation-driven, with continuous advancements in insulated containers, phase change materials, vacuum-insulated panels, and IoT-enabled monitoring systems. Smart packaging solutions, capable of providing real-time temperature, location, and humidity data, are transforming the efficiency of pharmaceutical supply chains. Additionally, sustainability trends are shaping product development, with companies increasingly adopting reusable and recyclable packaging solutions to reduce waste and meet corporate ESG goals.

The pharmaceutical cold chain packaging industry operates on a global scale, supporting manufacturers and distributors across developed and emerging markets. However, its globalized nature makes it highly sensitive to risks such as supply chain disruptions, geopolitical conflicts, and raw material shortages. For example, COVID-19 highlighted the need for robust and scalable cold chain infrastructure to handle vaccine surges. As a result, industry players focus on resilience-building strategies like regionalized production, partnerships with logistics providers, and digital integration of supply networks.

Material Insights

The plastic segment recorded the largest market revenue share of over 74.0% in 2024. Plastic is the most widely used material in pharmaceutical cold chain packaging due to its durability, lightweight nature, and superior insulation properties. High-performance plastics such as polyethylene (PE), polypropylene (PP), polyurethane (PU), and expanded polystyrene (EPS) are commonly used in insulated containers, gel packs, and bubble wraps for maintaining temperature-sensitive drugs, vaccines, and biologics. Advanced engineered plastics, like vacuum-insulated panels (VIPs) with plastic linings, also ensure long shelf-life for specialty pharmaceuticals during long-haul transportation.

The paper segment is expected to grow at the fastest CAGR of 16.4% during the forecast period. Paper and paperboard materials are gaining prominence in pharmaceutical cold chain packaging, especially for secondary and tertiary packaging applications such as corrugated boxes, insulated liners, and outer cartons. Innovations in coated and laminated paperboards enhance insulation performance, enabling their use alongside gel packs and phase change materials (PCMs). The primary driving factor for paper is the increasing demand for sustainable and eco-friendly packaging solutions.

Product Insights

The small boxes segment recorded the largest market revenue share of over 42.0% in 2024. Small boxes are primarily used for packaging and transporting temperature-sensitive pharmaceutical products such as vaccines, biologics, blood samples, and personalized medicines in smaller volumes. These boxes are generally insulated with materials like expanded polystyrene (EPS), polyurethane (PU), or vacuum-insulated panels (VIPs), and often incorporate phase change materials (PCMs) or dry ice to maintain the required temperature range. They are widely adopted for last-mile delivery in pharmaceutical e-commerce and direct-to-patient models. The expansion of e-pharmacy platforms and home healthcare services is making small box solutions indispensable for maintaining cold chain integrity over shorter transit durations.

The pallets segment is expected to grow at the fastest CAGR of 15.9% during the forecast period. Pallets are widely used for bulk transportation of pharmaceutical products such as vaccines, APIs, and finished drugs across long distances. These pallets are often made of plastic or composite materials and can be fitted with insulated covers or pallet shippers to protect products against temperature fluctuations. They are designed to facilitate efficient loading and unloading in warehouses, airports, and seaports, making them a critical component of large-scale pharmaceutical supply chains. The increasing globalization of pharmaceutical supply chains and cross-border trade in biologics are fueling demand for pallet-based cold chain packaging.

End Use Insights

The biopharmaceutical companies segment recorded the largest market share of over 34.0% in 2024. Biopharmaceutical companies are the primary users of cold chain packaging, as they deal with temperature-sensitive drugs, vaccines, biologics, cell and gene therapies, and monoclonal antibodies that require stringent temperature controls. With products often having a narrow stability window, these companies invest heavily in advanced cold chain packaging solutions such as insulated shippers, phase-change materials, and IoT-enabled tracking systems. The demand is driven by the increasing development of biologics and personalized medicines, which are more temperature-sensitive than traditional drugs.

The hospital segment is projected to grow at the fastest CAGR of 16.5% during the forecast period. Hospitals are critical end users as they directly handle the administration and storage of cold chain pharmaceuticals, particularly vaccines, insulin, blood products, and oncology drugs. Hospitals often use portable insulated containers and small-scale refrigerated packaging for efficient patient-level distribution. Growth is primarily driven by the rising demand for vaccines, blood products, and chronic disease treatments requiring cold chain management. The surge in hospital-based immunization programs and increased patient volumes, especially in urban and developing regions, further fuels this segment.

Region Insights

North America dominated the market and accounted for the largest revenue share of over 36.0% in 2024. This positive outlook is due to its strong base of biopharmaceutical companies and advanced logistics infrastructure. The region has the largest share of biologics, cell & gene therapies, and specialty pharmaceuticals, which are all highly temperature sensitive. The U.S. and Canada also enforce strict regulatory frameworks (FDA, Health Canada) requiring validated cold chain packaging solutions, pushing companies to adopt high-performance insulated shippers, phase-change materials, and IoT-enabled tracking. The region’s high R&D investment in biotechnology and personalized medicine further adds to the demand for reliable cold chain packaging.

U.S. Pharmaceutical Cold Chain Packaging Market Trends

The U.S. is home to major pharmaceutical and biotech companies such as Pfizer, Moderna, Amgen, and Johnson & Johnson, all of which rely on robust cold chain solutions. The U.S. also has one of the world’s largest clinical trial ecosystems, requiring validated packaging solutions to transport investigational drugs nationwide. For example, the Pfizer-BioNTech and Moderna COVID-19 vaccines set new benchmarks in cold chain packaging with ultra-low temperature requirements. Logistics providers like UPS Healthcare and FedEx developed advanced insulated packaging with real-time tracking to ensure timely vaccine delivery.

Europe Pharmaceutical Cold Chain Packaging Market

Europe’s growth in pharmaceutical cold chain packaging market is due to the presence of leading pharmaceutical and biotech companies, particularly in biologics and vaccines. The European Medicines Agency (EMA) enforces strict guidelines for maintaining pharmaceutical integrity, which fuels demand for innovative packaging solutions. Europe is also a hub for clinical trials, with countries such as Germany, Switzerland, and the UK conducting thousands of trials annually, requiring validated cold chain packaging to distribute investigational products across multiple trial sites. Additionally, Europe’s aging population and rising prevalence of chronic diseases create strong demand for specialty medicines that depend on cold chain packaging.

Germany drives the European cold chain packaging market as one of the continent’s largest pharmaceutical producers and exporters. It is home to industry giants such as BioNTech, Bayer, and Merck KGaA, which are deeply involved in biologics, vaccines, and specialty therapies. Germany is also a hub for clinical trials and R&D collaborations across Europe, requiring secure and validated packaging to transport investigational medicinal products. The country’s high regulatory standards, combined with strong government support for healthcare infrastructure, ensure widespread adoption of advanced cold chain packaging.

Asia Pacific Pharmaceutical Cold Chain Packaging Market

Asia Pacific region is expected to grow at the fastest CAGR of 6.0% over the forecast period, owing to its rapidly expanding pharmaceutical manufacturing base and increasing healthcare demand. Countries such as China, India, South Korea, and Japan are major producers of generic drugs, vaccines, and biologics, all requiring robust cold chain systems. Rising incidences of chronic diseases and government vaccination campaigns have amplified the need for temperature-controlled packaging.

Key Pharmaceutical Cold Chain Packaging Market Company Insights

The competitive environment of the pharmaceutical cold chain packaging industry is characterized by the presence of both global leaders and specialized regional players, creating a moderately consolidated yet highly competitive market. Established companies such as Sonoco ThermoSafe, Pelican BioThermal, and Sofrigam dominate with strong portfolios in temperature-controlled packaging solutions, while niche players focus on innovative, sustainable, and cost-efficient products to capture market share.

Strategic collaborations with pharmaceutical companies, logistics providers, and healthcare institutions are common, as players aim to strengthen distribution networks and ensure compliance with stringent regulatory requirements from bodies such as the FDA and EMA. Additionally, sustainability trends are reshaping competition, with growing focus on recyclable, reusable, and eco-friendly cold chain packaging solutions.

-

In July 2025, Nordic Cold Chain Solutions launched the Nordic Express Pack, the first cold chain packaging designed for GLP-1 medications. Compact and space-saving, it improves freight efficiency, supports high-volume pharma distribution, and features irreversible temperature indicators for integrity assurance. ISTA-certified testing proves its reliability in extreme conditions, offering a fast, easy, and cost-effective solution for GLP-1 therapies.

-

In April 2025, Cold Chain Technologies launched the CCT Tower Elite, a 1600L reusable pallet shipper for pharma logistics. It offers 120+ hours of precise temperature control (-60°C to +20°C), fits Euro & US pallets, features IoT monitoring, and is supported by CCT’s global hub network, emphasizing efficiency and sustainability.

-

In January 2025, DS Smith launched TailorTemp, a fibre-based temperature-controlled packaging solution, at Pharmapack Europe 2025. This innovative product was designed to support the sustainability goals of pharmaceutical and biotech companies by maintaining controlled temperatures during the storage and transport of delicate medicinal products. TailorTemp is made from recyclable corrugated cardboard and can keep products cool for up to 36 hours.

Key Pharmaceutical Cold Chain Packaging Companies:

The following are the leading companies in the pharmaceutical cold chain packaging market. These companies collectively hold the largest market share and dictate industry trends.

- Sonoco Thermosafe

- Sealed Air

- Peli BioThermal Limited

- CSafe

- Intelsius

- Cryoport Systems, LLC

- Envirotainer

- SkyCell AG

- va-Q-tec AG

- Inmark Global Holdings, LLC

- Smurfit Westrock

- Insulated Products Corporation

- Chill-Pak

- Practical Packaging Solutions, Inc.

- TESSOL

- The Wool Packaging Company Limited

- Thermal Packaging Solutions Ltd.

- Hanchett Paper Company

- Topa Thermal

- Sofrigam

Pharmaceutical Cold Chain Packaging Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 20.31 billion

Revenue forecast in 2033

USD 63.30 billion

Growth rate

CAGR of 15.3% from 2025 to 2033

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion, Volume in Kilotons, and CAGR from 2025 to 2033

Report coverage

Revenue forecast, volume forecast, competitive landscape, growth factors, and trends

Segments covered

Material, product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Sonoco Thermosafe; Sealed Air; Peli BioThermal Limited; CSafe; Intelsius; Cryoport Systems, LLC; Envirotainer; SkyCell AG; va-Q-tec AG; Inmark Global Holdings, LLC; Smurfit Westrock; Insulated Products Corporation; Chill-Pak; Practical Packaging Solutions, Inc.; TESSOL; The Wool Packaging Company Limited; Thermal Packaging Solutions Ltd.; Hanchett Paper Company; Topa Thermal; Sofrigam

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pharmaceutical Cold Chain Packaging Market Report Segmentation

This report forecasts revenue growth at a global, regional & country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pharmaceutical cold chain packaging market report based on material, product, end use, and region:

- Material Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Plastic

-

Polyethylene (PE)

-

Polypropylene (PP)

-

Polyethylene Terephthalate (PET)

-

Expanded Polystyrene (EPS)

-

Polyurethane (PU)

-

Others

-

-

Paper

-

Metal

-

Others

-

-

Product Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Small Boxes

-

Pallets

-

Large Sized Pallet Containers

-

Others

-

-

End Use Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Biopharmaceutical Companies

-

Clinical Research Organizations

-

Hospitals

-

Research Institutes

-

Logistics and Distribution Companies

-

Others

-

-

Region Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The global pharmaceutical cold chain packaging market was estimated at around USD 17.93 billion in the year 2024 and is expected to reach around USD 20.31 billion in 2025.

The global pharmaceutical cold chain packaging market is expected to grow at a compound annual growth rate of 15.3% from 2025 to 2030 to reach around USD 63.30 billion by 2033.

Biopharmaceutical companies segment emerged as the dominating end use segment in the pharmaceutical cold chain packaging market due to their reliance on temperature-sensitive biologics, vaccines, and cell & gene therapies that demand strict thermal protection.

The key players in the pharmaceutical cold chain packaging market include Sonoco Thermosafe; Sealed Air; Peli BioThermal Limited; CSafe; Intelsius; Cryoport Systems, LLC; Envirotainer; SkyCell AG; va-Q-tec AG; Inmark Global Holdings, LLC; Smurfit Westrock; Insulated Products Corporation; Chill-Pak; Practical Packaging Solutions, Inc.; TESSOL; The Wool Packaging Company Limited; Thermal Packaging Solutions Ltd.; Hanchett Paper Company; Topa Thermal; and Sofrigam.

The market is driven by the rising demand for temperature-sensitive biologics, vaccines, and specialty drugs that require strict thermal protection during storage and transportation.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.