- Home

- »

- Advanced Interior Materials

- »

-

Pneumatic Components Market Size Report, 2026-2027GVR Report cover

![Pneumatic Components Market (2026 - 2033)Report]()

Pneumatic Components Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Valves, Actuators, Air Treatment Components), By End Use (Automotive, F&B, Industrial Manufacturing), By Region, And Segment Forecasts

Market Size, 2025

$27.6BMarket Estimate, 2026

$28.9BMarket Forecast, 2033

$41.0BCAGR, 2026–2033

5.1%Pneumatic Components Market Summary

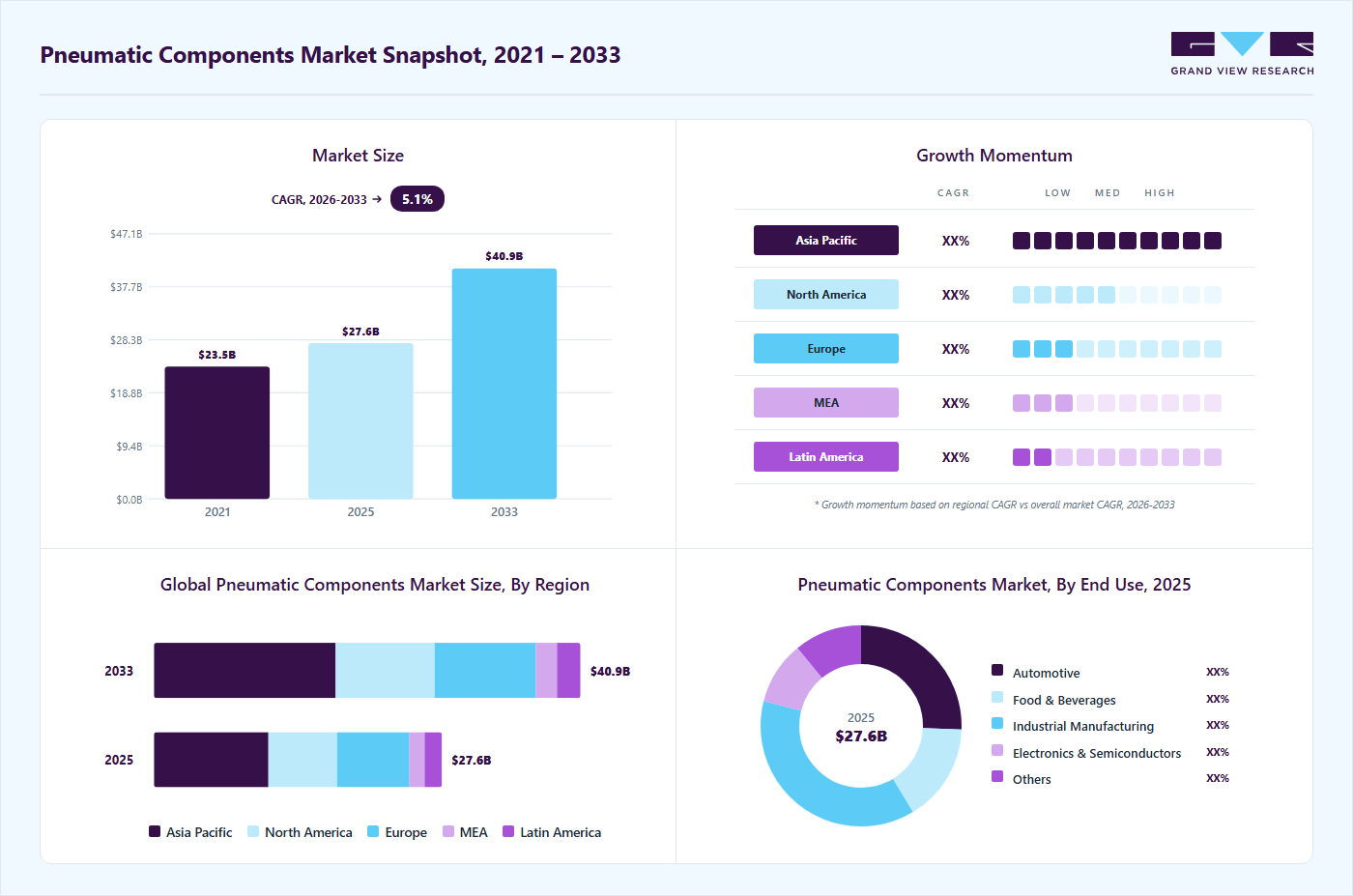

The global pneumatic components market size was valued at USD 27.6 billion in 2025 and is projected to grow from USD 28.9 billion in 2026 to USD 41.0 billion by 2033, at a CAGR of 5.1% from 2026 to 2033, driven by their growing application across industries such as automotive, food and beverage, packaging, pharmaceuticals, and manufacturing. Asia Pacific dominated the global pneumatic components industry with the largest revenue share of 39.8% in 2025. These components, such as valves, actuators, cylinders, and filters, offer cost-effective, durable, and easy-to-maintain solutions for automation and process control.

Key Market Trends & Insights

- By product: Valves dominated the market across all product segments in terms of revenue, accounting for a 37.93% market share in 2025.

- By end use: Industrial manufacturing dominated the market across the application segmentation in terms of revenue, accounting for a 37.56% market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (39.8% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 27.6 Billion

- Estimated market size in 2026: USD 28.9 Billion

- Projected market size by 2033: USD 41.0 Billion

- CAGR (2026-2033): 5.1%

With the shift towards Industry 4.0 and increased focus on efficiency and automation, manufacturers are increasingly adopting pneumatic systems for their reliability and performance in high-speed operations.")

Market Dynamics

The rising adoption of industrial automation and smart manufacturing technologies across industries such as automotive, food & beverage, packaging, electronics, pharmaceuticals, and material handling is a major factor driving the pneumatic components market. Pneumatic systems are widely used in automated industrial operations due to their reliability, fast response time, simple design, and cost-effective operation. Components such as pneumatic cylinders, valves, actuators, filters, regulators, lubricators, and air preparation units play a critical role in controlling motion and improving operational efficiency in manufacturing environments.

The growing implementation of Industry 4.0 and factory automation solutions is further accelerating demand for advanced pneumatic systems integrated with sensors, IoT connectivity, and intelligent control technologies. In industries such as automotive manufacturing and packaging, pneumatic components are increasingly preferred for repetitive high-speed operations, assembly line automation, and robotic systems due to their durability and ease of maintenance.

Pneumatic systems rely on compressed air, which can be energy-intensive to generate and maintain, especially in large industrial facilities. Air leakage, pressure drops, and inefficient compressed air systems can significantly increase energy consumption and operational expenses for end users. In addition, pneumatic components require regular maintenance to ensure stable performance and prevent system failures caused by moisture contamination, air leaks, seal wear, and pressure inconsistencies. Components such as valves, cylinders, compressors, and air treatment units are subject to wear and tear under continuous industrial operations, increasing maintenance costs and downtime. Small and medium-sized manufacturers may also face challenges in upgrading legacy pneumatic systems due to capital investment constraints.

Market Concentration & Characteristics

The market growth stage is moderate, and the rate of growth is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as SMC Corporation, Festo, Parker Hannifin, Emerson Electric, and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market, introducing new products, technologies, and products to meet the industry's evolving demands.

While pneumatic components are widely used for their simplicity and cost-effectiveness, they face competition from alternative technologies such as electric actuators, hydraulic systems, and electromechanical drives. Electric actuators, in particular, are gaining popularity due to their precision, energy efficiency, and better control in complex automation tasks.

Hydraulic systems, although more expensive and maintenance-intensive, are preferred in applications requiring higher force and load-bearing capacity. The choice between these technologies often depends on factors such as application requirements, energy efficiency goals, cost constraints, and environmental considerations.

Product Insights

Valves dominated the market across all product segments in terms of revenue, accounting for a 37.93% market share in 2025, and is forecasted to grow at a 4.9% CAGR from 2026 to 2033, due to their central role in controlling air flow, pressure, and direction within pneumatic systems. They are essential for regulating system performance and ensuring precise operation in a wide range of industrial applications, from assembly lines to packaging systems. Their versatility, relatively low cost, and critical function in system automation make them a high-demand component. In addition, the ongoing need to maintain and replace valves in existing systems contributes to their strong market share.

The actuators segment is anticipated to grow at a substantial CAGR of 5.7% through the forecast period. Actuators are experiencing the fastest growth in the market due to surging demand for automation and motion control across industries. As companies seek to improve operational efficiency and reduce manual intervention, pneumatic actuators are increasingly used in robotics, manufacturing lines, and material handling systems. Their ability to convert compressed air into mechanical motion makes them ideal for precise, repetitive tasks, particularly in automotive, electronics, and food processing industries. Technological advancements such as compact designs, smart sensors, and energy-efficient models are further accelerating their adoption.

End Use Insights

Industrial manufacturing dominated the market across the application segmentation in terms of revenue, accounting for a 37.56% market share in 2025, and is forecast to grow at a 4.9% CAGR from 2026 to 2033. As manufacturers strive to improve productivity, reduce downtime, and ensure consistent quality, pneumatic systems offer an efficient and economical solution for tasks such as material handling, clamping, pressing, and assembly. The expansion of industries such as electronics, machinery, and consumer goods, especially in emerging economies, is further accelerating demand. In addition, the integration of IoT and Industry 4.0 practices is driving the need for advanced pneumatic components with real-time monitoring and control capabilities.

The electronics & semiconductors segment is projected to grow at a robust 5.9% CAGR over the forecast period. The Electronics & Semiconductors segment’s growth is propelled by the sector’s rapid capital investment cycle and precision manufacturing requirements. Increasing global fabrication capacity, especially in the Asia Pacific and North America, is driving demand for cleanroom-compatible pneumatic valves and actuators that support wafer handling, packaging, and test applications with minimal contamination risk. Stringent quality standards in semiconductor assembly further reinforce pneumatic systems as cost-efficient alternatives to electric actuation for high-throughput, repetitive tasks.

Regional Insights

The Asia Pacific pneumatic components industry held the largest share in the global market, accounting for 39.75% of the revenue in 2025, and is expected to grow at the fastest CAGR of 6.1% over the forecast period. Asia Pacific is driven by its robust industrial ecosystem and accelerating pace of automation. Countries across the region, particularly China, India, Japan, and South Korea, are undergoing extensive industrialization, with rising demand for automation in manufacturing, electronics, packaging, and automotive sectors. The widespread availability of low-cost raw materials and skilled labor, combined with government initiatives such as “Make in India” and “Smart Manufacturing” in South Korea, is further driving growth. In addition, the growing trend toward smart factories and Industry 4.0 integration is driving demand for advanced, energy-efficient pneumatic solutions. This region benefits from both strong domestic consumption and export-oriented production, making it the dominant market globally.

China's pneumatic components industry is expected to grow in the coming years, as it is home to the world’s largest manufacturing base and a high concentration of end user industries, such as automotive, electronics, textiles, and heavy machinery, that rely heavily on pneumatic automation. The government's “Made in China 2025” policy promotes the adoption of advanced technologies, including smart pneumatic systems, across industrial sectors. As labor costs rise, Chinese manufacturers are increasingly investing in automation to maintain productivity and competitiveness. The ongoing expansion of high-speed rail, electric vehicle production, and semiconductor manufacturing also increases demand for precision pneumatic components.

North America Pneumatic Components Market Trends

North America pneumatic components industry is a technologically advanced and innovation-driven market, characterized by early adoption of smart manufacturing practices and high standards for energy efficiency and safety. Market growth is supported by the widespread adoption of industrial IoT (IIoT), the increasing use of collaborative robots, and the retrofitting of older manufacturing facilities. Pneumatic components are widely used in automotive, aerospace, food & beverage, and pharmaceuticals industries where clean, reliable, and precise motion control is critical. The rising emphasis on reshoring manufacturing and enhancing domestic production capabilities post-pandemic further strengthens the market. In addition, North America is seeing increased demand for integrated pneumatic systems with real-time diagnostics and predictive maintenance features.

U.S. Pneumatic Components Market Trends

The U.S. pneumatic components industry leads the North American market with its strong base of high-tech and heavy manufacturing industries. The country's advanced infrastructure and significant investments in R&D contribute to the development and adoption of innovative pneumatic technologies. U.S. manufacturers are increasingly integrating smart sensors and controllers into pneumatic systems to improve operational visibility and efficiency. Key sectors such as automotive assembly, packaging, food processing, and life sciences are adopting pneumatic components for their durability and precision. Moreover, government support for domestic manufacturing and clean energy transitions is encouraging the use of energy-efficient pneumatic systems.

Europe Pneumatic Components Market Trends

Europe pneumatic components industry is a mature yet evolving market, characterized by high technological sophistication and strong regulatory frameworks. European manufacturers prioritize sustainable, efficient production practices, which align with the development of eco-friendly, energy-saving pneumatic components. The region benefits from a highly skilled workforce and a strong presence of major pneumatic equipment manufacturers, such as Festo (Germany) and Norgren (UK). Demand is particularly high in industries such as pharmaceuticals, automotive, food and beverage, and packaging, where hygiene, precision, and automation are crucial. The European Green Deal and industrial decarbonization goals are also pushing companies to upgrade to more energy-efficient pneumatic systems.

Key Pneumatic Components Company Insights

The pneumatic components industry is highly competitive, with several key players dominating the landscape. Major companies include SMC Corporation, Festo SE & Co. KG, Parker Hannifin Corporation, Emerson Electric Co., and others. The pneumatic components industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Pneumatic Components Companies:

The following key companies have been profiled for this study on the pneumatic components market.

- SMC Corporation.

- Festo SE & Co. KG

- Parker Hannifin Corporation.

- Emerson Electric Co.

- Norgren, Inc. (IMI, PIC)

- Bosch Rexroth AG

- Airtac International Group.

- JELPC (Ningbo Jiaerling Pneumatic Machinery Co., Ltd.)

- Zhaoqing Fangda pneumatic Co. Ltd

- Camozzi Group

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: SMC Corporation, Festo SE & Co. KG, Emerson Electric Co., Parker Hannifin Corporation, Bosch Rexroth AG, IMI plc, Aventics (Emerson), CKD Corporation

- Strong investments in industrial automation, smart pneumatics, and Industry 4.0-enabled motion control systems

- Expansion of energy-efficient pneumatic actuators, valves, FRLs, and intelligent air management systems

- Integration of IoT-enabled monitoring, predictive maintenance, and automation software into pneumatic solutions

- Extensive global distribution, aftermarket service, and OEM partnership networks

- Strong global brand recognition and diversified industrial automation portfolios

- Advanced engineering expertise in motion control and pneumatic system integration

- High operational reliability, product durability, and automation capabilities

- Established customer base across automotive, packaging, electronics, and manufacturing industries

- High dependence on industrial capital expenditure and manufacturing activity cycles

- Premium pricing compared to regional pneumatic component suppliers

- Exposure to increasing competition from electric actuation technologies

Emerging Players: AirTAC International Group, Metal Work Pneumatic, Camozzi Automation, Janatics India Pvt. Ltd., Pneumax S.p.A.

- Focus on cost-effective pneumatic automation solutions and regional market expansion

- Increasing emphasis on compact, energy-efficient, and application-specific pneumatic components

- Expansion into small and medium-sized industrial automation applications

- Strengthening distributor partnerships and localized technical support capabilities

- Competitive pricing and flexibility in customized pneumatic system configurations

- Strong responsiveness to localized manufacturing and automation requirements

- Growing adoption in packaging, textile, food processing, and general manufacturing industries

- Ability to cater to niche and mid-scale automation projects efficiently

- Comparatively lower global market penetration and brand visibility

- Limited financial scale for large R&D and international expansion investments

- Lower diversification compared to multinational automation technology providers

Recent Developments

-

In April 2025, SMC Corporation announced the launch of the 3-Port Solenoid Valve Modular Type/Residual Pressure Release Valve. This valve helps save space and reduce piping labor.

-

In March 2024, Festo introduced the ELGD-TB (tooth belt) and ELGD-BS (ball screw) axes, designed for high-load bearing and compact size. These axes are suitable for applications requiring high precision and repeatability.

Pneumatic Components Market Report Scope

Report Attribute

Details

Market size in 2025

USD 27.6 billion

Estimated Market size in 2026

USD 28.9 billion

Projected Market size by 2033

USD 41.0 billion

Growth rate

CAGR of 5.1% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Global Transparent Plastic Market Report Segmentation

Product, end use, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; India; Japan; South Korea

Key companies profiled

SMC Corporation.; Festo SE & Co. KG; Parker Hannifin Corporation.; Emerson Electric Co.; Norgren, Inc. (IMI, PIC); Bosch Rexroth AG; Airtac International Group.; JELPC (Ningbo Jiaerling Pneumatic Machinery Co., Ltd.); Zhaoqing Fangda pneumatic Co. Ltd; Camozzi Group

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pneumatic Components Market Report Segmentation

This report forecasts revenue & volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the pneumatic components market report based on product, end use, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Valves

-

Actuators

-

Air Treatment Components

-

Others

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Food & Beverages

-

Industrial Manufacturing

-

Electronics & Semiconductors

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Central & South America

-

Middle East & Africa

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed market estimates and forecasts for the pneumatic components market across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Country-level demand analysis covering automotive, packaging, electronics, food & beverage, pharmaceuticals, material handling, and industrial manufacturing sectors.

Identify high-growth regional markets and industrial automation investment hotspots. Support regional expansion planning, distributor network optimization, and demand forecasting.

Competitive Benchmarking

Detailed benchmarking of leading pneumatic component manufacturers based on product portfolio, automation capabilities, energy efficiency, IoT integration, regional presence, aftermarket services, and strategic initiatives.

Enable competitive intelligence and technology benchmarking. Support product positioning, partnership evaluation, and innovation strategy development.

Opportunity Assessment

Identification of emerging growth opportunities driven by Industry 4.0 adoption, warehouse automation growth, increasing use of robotic systems, and rising investments in energy-efficient industrial automation technologies.

Prioritize high-growth applications and investment opportunities. Support innovation roadmap development and long-term strategic planning.

Frequently Asked Questions About This Report

The valves dominated segment accounted for the largest share of 37.9% in 2025.

Industrial manufacturing segment held the highest market share of 37.6% in 2025.

The global pneumatic components market size was estimated at USD 27.6 billion in 2025 and is expected to reach USD 28.9 billion in 2026.

The global pneumatic components market is expected to grow at a compound annual growth rate of 5.1% from 2026 to 2033 to reach USD 41.0 billion by 2033.

Asia Pacific dominated with a 39.8% revenue share in 2025.

Some key players operating in the pneumatic components market include SMC Corporation, Festo SE & Co. KG, Parker Hannifin Corporation, Emerson Electric Co., Norgren, Inc. (IMI, PIC), Bosch Rexroth AG, Airtac International Group, JELPC (Ningbo Jiaerling Pneumatic Machinery Co., Ltd.), Zhaoqing Fangda pneumatic Co. Ltd, and Camozzi Group.

Key factors include growing application across industries such as automotive, food and beverage, packaging, pharmaceuticals, and manufacturing.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.