- Home

- »

- Biotechnology

- »

-

Preparative And Process Chromatography Market, 2033GVR Report cover

![Preparative And Process Chromatography Market Size, Share & Trends Report]()

Preparative And Process Chromatography Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Process Chromatography, Preparative Chromatography), By Type (Liquid Chromatography, Gas Chromatography), By End Use, By Region, And Segment Forecasts

Market Size, 2025

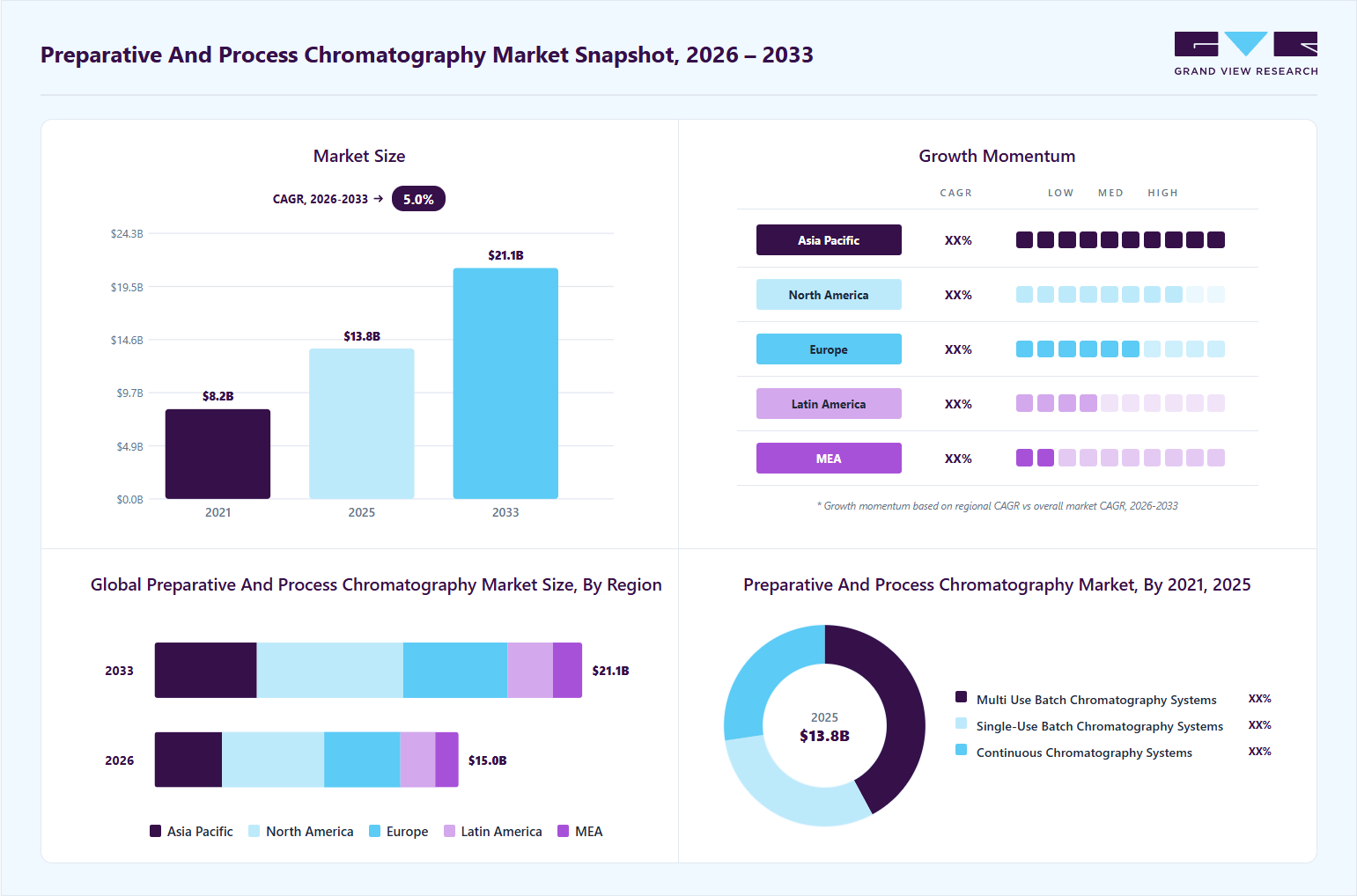

$13.8BMarket Estimate, 2026

$15.0BMarket Forecast, 2033

$21.2BCAGR, 2026–2033

5.0%Preparative And Process Chromatography Market Summary

The global preparative and process chromatography market size was valued at USD 13.78 billion in 2025 and is projected to grow from USD 15.04 billion in 2026 to USD 21.15 billion by 2033, at a CAGR of 5.00% from 2026 to 2033. North America preparative and process chromatography dominated the global market and accounted for the largest revenue share of 33.49% in 2025. The growth of this market is driven by the rising demand and approval of monoclonal antibodies in the pharmaceutical and biotechnology sectors.

Key Market Trends & Insights

- The U.S. led the North American market and held the largest revenue share in 2025.

- Based on product, the process chromatography segment dominated the global market and accounted for the largest revenue share of 59.10% in 2025.

- Based on type, the liquid chromatography segment held the highest market share in 2025.

- On the basis of end use, the pharmaceuticalsegment held the highest market share in 2025.

Market Size & Forecast

- 2025 Market Size: USD 13.78 Billion

- 2026 Market Size: USD 15.04 Billion

- 2033 Projected Market Size: USD 21.15 Billion

- CAGR (2026-2033): 5.00%

- North America: Largest market in 2025

- Asia Pacific: Fastest growing market

")

In addition, the preparative and process chromatography industry is driven by the expanding biopharmaceutical industry, the demand for advanced purification techniques, and the need for more efficient and cost-effective processes. For instance, in September 2025, Samsung Biologics expanded biopharma partnerships through end-to-end CDMO services. The key highlights are end-to-end support from early development to commercial production, robust quality systems that strengthen supply chain resilience, and Samsung Biologics' continued capacity expansion and enhanced flexibility to accommodate complex modalities. Moreover, technological advancements and the development of innovative chromatography products are expected to boost market growth. For instance, in June 2025, Bruker Corporation launched the proteoElute nanoLC system along with PepSep Advanced nLC columns to improve chromatographic resolution, peptide sensitivity, and proteomics analysis performance in ultra-sensitive workflows.

Market Dynamics

The increasing demand for biopharmaceuticals and biologics is a major factor driving the growth of the preparative and process chromatography market. Biopharmaceutical products such as monoclonal antibodies, vaccines, recombinant proteins, insulin, and cell and gene therapies are widely used to treat chronic diseases, cancer, autoimmune disorders, and infectious diseases. These products require highly advanced purification techniques during the manufacturing process to ensure product quality, safety, and effectiveness. Preparative and process chromatography systems are extensively used in downstream bioprocessing to separate and purify biological molecules from complex mixtures.

Technological advancements in chromatography systems are also supporting market expansion. Manufacturers are introducing automated and continuous chromatography systems that improve productivity, reduce processing time, and lower operational costs. In August 2025, WuXi Biologics announced that its WuXiUP platform achieved fully automated continuous drug substance production at pilot scale by integrating membrane chromatography and automated control systems. These advanced systems provide better scalability and efficiency for large-volume biologics production. Furthermore, increasing investments in biopharmaceutical research and development, along with the expansion of contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs), are increasing the use of preparative and process chromatography worldwide. Therefore, the rapid growth of the biopharmaceutical industry continues to create significant opportunities for the preparative & process chromatography market.

One of the major restraints on the growth of the preparative and process chromatography industry is the high cost of chromatography systems, resins, and maintenance. Preparative and process chromatography technologies are extensively used in the purification of biologics, monoclonal antibodies, vaccines, recombinant proteins, and other therapeutic products across the pharmaceutical and biotechnology industries. However, adopting these systems requires substantial capital and operational investment, creating financial challenges for many end users. Large-scale chromatography systems are technologically advanced and incorporate automated software, pumps, detectors, and specialized columns designed to deliver high precision, efficiency, and reproducibility. The procurement, installation, and validation of such systems significantly increase upfront infrastructure costs. In addition, chromatography resins, particularly specialty affinity resins such as Protein A used in monoclonal antibody purification, represent a major share of downstream processing expenses. These resins are highly expensive and require periodic replacement due to limited operational lifespan, thereby increasing recurring production costs.

Moreover, companies incur ongoing expenditures for system maintenance, cleaning validation, solvent management, regulatory compliance, and skilled workforce requirements. These ongoing operational costs can place significant pressure on manufacturing budgets, particularly for small and mid-sized biotechnology companies and organizations operating in cost-sensitive markets. As a result, high capital and maintenance costs may delay technology adoption, limit infrastructure expansion, and encourage the use of alternative purification approaches. Consequently, the high overall cost burden associated with chromatography systems and consumables acts as a key restraint limiting the broader adoption of preparative and process chromatography solutions globally.

The increasing outsourcing of drug development and manufacturing activities to contractdevelopment and manufacturing organizations (CDMOs) and contract research organizations (CROs) is creating significant opportunities for the process and preparative chromatography market. Pharmaceutical and biotechnology companies are increasingly depending on CDMOs and CROs to reduce operational costs, improve manufacturing efficiency, and speed up product development and commercialization. This growing outsourcing trend is increasing the demand for advanced purification technologies, including process and preparative chromatography systems. Process and preparative chromatography are widely used for the purification of biologics, including monoclonal antibodies, vaccines, recombinant proteins, peptides, and biosimilar. As CDMOs and CROs expand their biologics manufacturing capabilities, the need for efficient, large-scale chromatography systems is also growing. In addition, these organizations require high-quality purification solutions to meet strict regulatory standards and ensure product safety and purity. From a business perspective, this trend is creating growth opportunities for chromatography manufacturers through increased sales of systems, columns, resins, and consumables. The rising demand for scalable, automated, and high-throughput purification technologies is also supporting the adoption of advanced chromatography solutions. Furthermore, the expansion of CDMO facilities in emerging markets is expected to further increase the demand for process and preparative chromatography technologies during the forecast period. In April 2025, Axplora announced a USD 52 million investment to establish a large-scale, high-performance liquid chromatography (HPLC) and continuous chromatography facility in France for peptide purification and biologics manufacturing.

Market Concentration & Characteristics

The market is distinguished by ongoing and rapid innovation to address the increasing complexities of bioprocessing. This includes the development of highly specialized chromatography resins with increased binding capacity, selectivity, chemical stability, and allowing for more precise and efficient purification.In June 2025, Ecolab launched the Purolite AP+50 affinity chromatography resin at the BIO International Convention in the U.S. The resin was developed using advanced Jetted bead manufacturing technology to deliver higher binding capacity, improved durability, shorter lead times, and greater process efficiency for monoclonal antibody purification. This innovation highlights the industry’s focus on developing next-generation chromatography resins that improve purification performance, scalability, and manufacturing productivity in bioprocessing applications. Furthermore, there has been significant progress in integrating advanced automation and digital monitoring systems, which enable real-time control, reduced human error, and improved reproducibility.

Mergers and acquisitions play an important strategic role. Major industry consolidations enable smaller, specialized companies to broaden their technological capabilities, diversify their product offerings, and strengthen their global market presence. Through acquisitions, major bioprocessing and chromatography companies can integrate advanced chromatography resins, columns, filtration technologies, and downstream purification solutions into their existing offerings. These strategic consolidations are helping companies improve manufacturing efficiency and accelerate innovation in biologics purification. In October 2025, Germany-based Merck announced the acquisition of JSR Life Sciences' chromatography business to strengthen its downstream bioprocessing and Protein A chromatography capabilities.

Regulations have a significant impact on the growth and operations of the process and preparative chromatography market, particularly in the pharmaceutical, biotechnology, food, and environmental industries. Regulatory authorities such as the U.S. Food and Drug Administration, European Medicines Agency, and World Health Organization enforce strict quality, safety, and purity standards for biopharmaceuticals, vaccines, monoclonal antibodies, and other therapeutic products. As a result, manufacturers increasingly adopt advanced chromatography systems to ensure accurate purification, contamination control, and compliance with Good Manufacturing Practices (GMP).

Regional expansion is becoming a significant trend in the process and preparative chromatography market as biopharmaceutical manufacturing activities continue to grow across emerging economies. The Asia-Pacific region is witnessing the fastest growth driven by rising investments in biotechnology, increased pharmaceutical production, supportive government initiatives, and the expansion of contract manufacturing organizations. In May 2026, Ecolab Life Sciences opened a new bioprocessing applications laboratory in South Korea to support downstream bioprocess development across the Asia-Pacific region.

Product Insights

The process chromatography segment dominated the preparative and process chromatography market, accounting for the largest revenue share of 59.10% in 2025. These methods are commonly employed in industry to purify a variety of biomolecules. These products require highly efficient purification processes, which are well supported by process chromatography at a large scale. In addition, the expansion of the biopharmaceutical industry and the increasing number of manufacturing facilities are driving higher demand for these systems. Strict regulatory requirements for product safety, consistency, and high purity further strengthen their adoption in industrial applications. Moreover, the growing development of biosimilar and continuous advancements in chromatography technologies have improved efficiency, scalability, and cost-effectiveness. As a result, process chromatography is increasingly becoming a key technology in large-scale pharmaceutical manufacturing.

The preparative chromatography is anticipated to grow at the fastest CAGR of 5.46% over the forecast period. Preparative chromatography is a purification technique used to separate, isolate, and collect specific compounds from a mixture in large quantities. It is widely used in the pharmaceutical, biotechnology, food, chemical, and research industries to purify products such as active pharmaceutical ingredients (APIs), monoclonal antibodies, vaccines, proteins, peptides, and natural compounds. Companies are adopting preparative chromatography to achieve high product purity, quality, and consistency, which are essential in regulated industries such as pharmaceuticals and biotechnology. The technology enables manufacturers to efficiently remove impurities, contaminants, and unwanted by-products, ensuring compliance with strict regulatory standards. In addition, preparative chromatography supports the growing demand for biologics, personalized medicines, and advanced therapies by improving purification efficiency and production yield. Many companies also use this technology because it enhances process reliability, reduces product loss, and supports large-scale manufacturing, making it an important part of modern bioprocessing and chemical production operations.

Type Insights

The liquid chromatography segment accounted for the largest share of 27.52% in 2025 owing to the widespread application across several industries. The segment is driven due to its essential role in pharmaceutical, biotechnology, and specialty chemical applications. It is widely used for separating, identifying, and purifying complex compounds, especially in biologics and advanced drug development. The increasing demand for monoclonal antibodies, vaccines, and other biopharmaceutical products has further highlighted the need for accurate, high-resolution analytical techniques. Manufacturers are supporting this growth by introducing advanced systems with higher sensitivity, improved resolution, and faster analysis capabilities. In May 2025, Agilent Technologies launched the InfinityLab Pro iQ Series, a next-generation liquid chromatography-mass spectrometry platform designed for pharmaceutical and biopharmaceutical applications. The system strengthens impurity profiling, biomolecule analysis, and quality control workflows, enabling higher accuracy and efficiency in regulated analytical environments. Furthermore, companies are developing specialized columns, consumables, and biocompatible systems to improve performance in complex biological applications.

The hydrophobic interaction chromatography segment is expected to witness the fastest growth rate over the estimated time period in 2025. As this technique has demonstrated its advantages in analyzing protein unfolding and folding and isolating complex protein, thus it is becoming more widely used in the protein research field. In the near future, the rising demand for monoclonal antibodies in oncology is expected to promote the utilization of this approach.

End use Insights

The pharmaceutical segment held the largest share 42.18% in 2025, owing to the widespread use of preparative and process chromatography in drug safety assessments and quality control. This expansion is fueled by rising global pharmaceutical production, increased investments in biologics R&D, and stringent regulatory requirements that require chromatography testing for drug purity and efficacy. High-performance liquid chromatography (HPLC) and automated chromatography systems improve precision and throughput, enabling large-scale biopharmaceutical manufacturing. Furthermore, the growing use of single-use chromatography technologies offers cost-effective and scalable options for drug production in accordance with current good manufacturing practices. As a result of the situation and its scope, the need to commercialize and provide access to the most productive, versatile, and novel bioprocessing equipment is anticipated to grow. This is likely to strengthen the pool of companies involved in preparative and process chromatography, promoting market growth even more.

The biotechnology segment is expected to grow at the fastest CAGR over the forecast period.This growth is mainly driven by increased focus on research and development, especially in areas such as protein isolation, personalized medicine, and novel therapeutic solutions. The expanding adoption of advanced biotechnological techniques is further supporting innovation in drug discovery and treatment development. In addition, rising demand for targeted, patient-specific therapies is strengthening the role of biotechnology in modern healthcare, thereby contributing to market expansion.

Regional Insights

North America Preparative and Process Chromatography Market Trends

North America dominated the market with a revenue share of 33.49% in 2025, due to a strong expansion in the biopharmaceutical and life sciences industries, along with increasing demand for highly purified biologics such as monoclonal antibodies, vaccines, recombinant proteins, and gene therapies. The region has a well-established pharmaceutical manufacturing base, and companies are continuously investing in advanced purification technologies to improve product quality, yield, and regulatory compliance. In addition, strict guidelines from regulatory authorities, such as the U.S. Food and Drug Administration (FDA), are pushing manufacturers to adopt high-precision chromatographic techniques, such as preparative HPLC and process chromatography systems, for impurity profiling and quality assurance.

U.S. Preparative and Process Chromatography Market Trends

The preparative and process chromatography industry in the U.S. is a significant and rapidly growing segment. Increasing investments in biopharmaceutical R&D, advances in chromatography technology, and stringent regulatory frameworks established by agencies such as the FDA to ensure drug safety and purity is fueling the growth of the market. For instance, in September 2025, GSK planned to invest USD 30 billion in R&D and manufacturing in the U.S. over the next five years. This includes a USD 1.2 billion investment in laboratories, including chromatography, in the U.S. Furthermore, the market benefits from a strong presence of key industry players, advanced healthcare infrastructure, and rising demand for high-purity biologics, monoclonal antibodies, and vaccines that necessitate efficient downstream purification procedures.

Europe Preparative and Process Chromatography Market Trends

The preparative and process chromatography industry in Europe is witnessing strong growth, driven by rising demand for biopharmaceutical products and advanced purification technologies. The growing production of biologics, including monoclonal antibodies, vaccines, recombinant proteins, and advanced therapies, has created a strong need for efficient, scalable separation techniques. The growth of contract manufacturing and contract development organizations is also contributing significantly, as these companies are investing in advanced downstream processing capabilities to support increasing outsourcing activities in the pharmaceutical industry.

The UK preparative and process chromatography market is witnessing significant growth, fueled by increasing investments in the life sciences sectors. The market is driven by technological advancements and collaborations between academia and industry to accelerate drug discovery and manufacturing processes. For instance, in May 2025, BioNTech UK Ltd. Granted an agreement with the UK Government to expand the Company's R&D activities for innovative medicines in the UK. BioNTech agreed to invest up to USD 1.33 billion over the next ten years as part of the agreement. The UK Government will support the Company's efforts with a grant of up to USD 171.66 million over ten years, one of the most significant grants in UK history for a pharmaceutical company. The grant is part of the UK government's mission to strengthen the life sciences sector and support innovative companies to accelerate medical progress.

Germany's preparative and process chromatography market is growing, owing to rising demand for high-purity compounds in pharmaceuticals, biotechnology, and research laboratories. The market benefits from advances in column technology, resin development, and automation, all of which improve compound isolation scalability and efficiency. The regulatory emphasis on product quality and safety in Germany's thriving pharmaceutical sector drives the adoption of these chromatography techniques. Furthermore, the growing use of preparative chromatography in food, environmental testing, and chemical industries promotes market growth. Preparative high-performance liquid chromatography (HPLC) is an essential technological advancement in the purification of biologics such as monoclonal antibodies, peptides, and proteins, ensuring physiologically active therapeutic proteins and removing contaminants.

Asia Pacific Preparative and Process Chromatography Market Trends

Asia Pacific is expected to grow at the fastest CAGR over the forecast period. The developing pharmaceutical and biotechnology sectors support the expected growth. The market in the region is driven by increasing investments in pharmaceutical manufacturing infrastructure and expanding contract research and manufacturing services (CRAMS) across countries such as China, India, Japan, and South Korea are further accelerating regional growth. Government initiatives supporting domestic drug production and biosimilar development are also strengthening the market landscape. Moreover, rising clinical trial activity, coupled with the rapid adoption of advanced separation and purification technologies in bioprocessing, is enhancing demand for chromatography solutions across the region.

The China preparative and process chromatography market is growing rapidly, driven by the country’s increasing investments in biopharmaceutical manufacturing and research, with a particular focus on biologics such as monoclonal antibodies and vaccines. China is building global-standard good manufacturing practice (GMP) facilities, which further increase the demand for advanced chromatography systems for downstream processing and purification. Growing expansion of chromatography across the China is the major key trends supporting market expansion. The product range includes upstream bioprocess cell culture, disposable liquid handling, downstream processes such as chromatography, ultrafiltration, and filtration units, and process development services. In addition, rising regulatory standards and the expansion of the biotechnology and pharmaceutical sectors in China contribute to the robust growth in preparative and process chromatography applications.

The Japan preparative and process chromatography market is driven by Japan's advanced pharmaceutical and biotechnology industries, increasing demand for high purity compounds, and growing generics and solid dosage forms sectors. There is increasing demand for highly pure compounds used in the production of biologics, vaccines, and other complex medicines, which require efficient separation and purification technologies. The rising production of generic drugs and solid dosage forms is also supporting market growth as manufacturers focus on cost-effective and high-quality manufacturing processes.

Latin America Preparative and Process Chromatography Market Trends

The Latin America preparative and process chromatography industry is growing, owing to the region's increasing investment in drug development, biologics manufacturing, and academic research has increased the demand for efficient purification technologies. Countries such as Brazil, Mexico, and Argentina are seeing increased adoption of advanced chromatography systems as regulatory standards tighten and quality control becomes more important. In addition, the growing trend of contract manufacturing and outsourcing in the life sciences industry contributes to market expansion.

Middle East and Africa Preparative and Process Chromatography Market Trends

The Middle East and Africa preparative and process chromatography industry is growing as biotechnology, pharmaceutical, and research sectors prioritize high-purity separations and quality assurance. Governments are focusing on developing healthcare infrastructure, local manufacturing, and regulatory frameworks that require more stringent purification and analytical standards. Further, countries such as Saudi Arabia and UAE, are emerging as investment hubs for chromatography equipment and consumables, due to public initiatives and the need to support domestic biologics and pharmaceutical production. Advanced chromatography techniques, particularly liquid chromatography, are becoming more widely used throughout the region, with new applications in food safety, environmental testing, and diagnostics.

Key Preparative And Process Chromatography Company Insights

Key players operating in the market are undertaking various initiatives to strengthen their market presence and increase the reach of their technology and services. Strategies such as expansion activities and partnerships are playing a key role in propelling the market growth. The following are the leading companies in the preparative and process chromatography market. These companies collectively hold the largest market share and dictate industry trends.

Key Preparative And Process Chromatography Companies:

The following key companies have been profiled for this study on the preparative and process chromatography market.

-

GE HealthCare

-

Danaher Corporation

-

Merck KGaA

-

Bio-Rad Laboratories, Inc.

-

Thermo Fisher Scientific Inc.

-

Shimadzu Corporation

-

Agilent Technologies, Inc.

-

Waters Corporation

-

Axplora (Novasep Holding S.A.S)

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: GE HealthCare

- Focus on integrated chromatography ecosystems combining instruments, resins, consumables, and software platforms

- Strong emphasis on biologics purification workflows and end-to-end downstream solutions

- Continuous investment in automation, digital chromatography systems, and high-throughput purification technologies

- Strong global installed base across pharmaceutical and biotechnology companies

- Advanced and validated product portfolios covering both analytical and process-scale chromatography.

- High R&D capability enabling innovation in resin chemistry, column technology, and automation.

- High cost of instruments and systems limits adoption in price-sensitive and emerging markets.

- Complex product ecosystems require long implementation and training cycles.

- Strong dependence on large pharma clients increases exposure to procurement cycles and budget shifts.

Emerging Players: Axplora

- Focus on niche biomarker assays and specialized pathology solutions.

- Expansion through collaborations, regional partnerships, and targeted market penetration.

- Development of cost-effective and customizable tissue diagnostics products for mid-sized laboratories.

- High flexibility in designing customized chromatography and purification workflows.

- Strong capability in cost-efficient solutions for small and mid-scale bioprocessing needs.

- Faster adaptation to new biologics modalities such as cell and gene therapies

- Limited global reach and lower brand recognition compared to established competitors.

- Smaller financial capacity for large-scale R&D and commercialization activities.

- Dependence on external partnerships for distribution and market expansion.

Recent Developments

-

In February 2026, Waters Corporation introduced next-generation microflow LC columns with MaxPeak Premier Technology. The solution delivers higher analytical sensitivity while significantly reducing sample and solvent consumption. Designed for biopharma and life sciences applications, the innovation supports more efficient, sustainable, and high-performance liquid chromatography workflows across advanced research and quality control environments.

-

In September 2025, Agilent Technologies introduced the Altura Ultra Inert HPLC Columns designed for advanced bio therapeutic applications. The launch enhances peptide and oligonucleotide analysis by improving sensitivity, peak shape, and reducing analyte-surface interactions.

Preparative And Process Chromatography Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 13.78 billion

Market size value in 2026

USD 15.04 billion

Revenue forecast in 2033

USD 21.15 billion

Growth rate

CAGR of 5.00% from 2026 to 2033

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, type, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Sweden; Denmark; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

GE Healthcare; Danaher Corporation; Merck KGaA; Bio-Rad Laboratories Inc.; Thermo Fisher Scientific Inc.; Shimadzu Corporation; Agilent Technologies; Waters Corporation; Axplora (Novasep Holding S.A.S)

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Preparative And Process Chromatography Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global preparative and process chromatography market report on the basis of product, type, end use, and region:

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Process Chromatography

-

System

-

Multi Use Batch Chromatography Systems

-

Single-Use Batch Chromatography Systems

-

Continuous Chromatography Systems

-

-

Consumables

-

Reagents

-

Resins

-

Affinity Resins

-

Ion-exchange Resins

-

Size-exclusion Resins

-

Hydrophobic Interaction Resins

-

Reversed Phase Resins

-

Mixed mode/Multi-mode Resins

-

-

Columns

-

Prepacked Columns

-

Automated Columns

-

Manual Columns

-

-

-

Service

-

-

Preparative Chromatography

-

System

-

Semi-Preparative Chromatography Systems

-

Other Chromatography Systems

-

-

Consumables

-

Reagents

-

Resins

-

Affinity Resins

-

Affinity Resins

-

Ion-exchange Resins

-

Size-exclusion Resins

-

Hydrophobic Interaction Resins

-

Reversed Phase Resins

-

Mixed-mode/Multi-mode Resins

-

-

Columns

-

Prepacked Columns

-

Empty Columns

-

-

-

Service

-

-

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Liquid Chromatography

-

HPLC

-

Flash/Column Chromatography

-

Ion-exchange chromatography

-

Size-exclusion chromatography

-

Affinity chromatography

-

-

Gas Chromatography

-

Thin Layer Chromatography

-

Paper Chromatography

-

Gel-permeation (Molecular Sieve) Chromatography

-

Hydrophobic Interaction Chromatography

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Pharmaceutical

-

Biotechnology

-

Food

-

Nutraceutical

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021- 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Sweden

-

Norway

-

Denmark

-

-

Asia Pacific

-

Japan

-

China

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Bioprocessing & Purification Demand Analysis

Assessment of chromatography demand across monoclonal antibodies, vaccines, recombinant proteins, gene therapies, and other biologics manufacturing applications.

Identifies high-growth application areas and future demand drivers.

Resin & Consumables Adoption Analysis

Evaluation of protein A resins, ion exchange, affinity, hydrophobic interaction, and mixed-mode chromatography media usage trends.

Supports product positioning and identifies recurring revenue opportunities.

Biopharma Manufacturing Capacity Assessment

Analysis of biopharmaceutical production facilities, CDMOs, and biologics manufacturing expansion across key regions.

Highlights capacity-driven demand and expansion opportunities.

Continuous Processing & Technology Innovation Landscape

Assessment of continuous chromatography, membrane chromatography, automation solutions, and next-generation purification technologies.

Identifies emerging technology trends and future innovation opportunities.

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The process chromatography segment dominated the preparative and process chromatography market, accounting for the largest revenue share of 59.10% in 2025

Key factors that are driving the market growth include increasing investments by the government to enhance R&D, growing use of chromatography techniques in the food and nutraceuticals industry, and increasing demand for biopharmaceutical products.

The global preparative and process chromatography market size was estimated at USD 13.8 billion in 2025 and is expected to reach USD 15.0 billion in 2026.

Some of the key players operating in the preparative and process chromatography market include GE Healthcare, Pall Corporation, Merck KGaA, Bio Rad Laboratories, Thermo Fisher Scientific Inc., Shimadzu Corporation, Agilent Technologies, Waters Corporation, Novasep Holding S.A.S, and Chiral Technologies, Inc.

The liquid chromatography segment accounted for the largest share of 27.52% in 2025 owing to the widespread application across several industries.

The pharmaceutical segment held the largest share 42.18% in 2025, owing to the widespread use of preparative and process chromatography in drug safety assessments and quality control.

The global preparative and process chromatography market is expected to grow at a compound annual growth rate of 5.0% from 2025 to 2033 to reach USD 21.2 billion by 2033.

North America dominated the preparative & process chromatography market with a share of 33.5% in 2024. This is attributable to the rise in major strategic mergers and acquisitions undertaken by key market players.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.