- Home

- »

- Plastics, Polymers & Resins

- »

-

Primary Pharmaceutical Packaging Market Size Report, 2033GVR Report cover

![Primary Pharmaceutical Packaging Market Size, Share & Trends Report]()

Primary Pharmaceutical Packaging Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Bottles, Blister Packs), By Material (Plastics & Polymers, Glass), By Region (North America, Asia Pacific, Europe, Latin America, MEA), And Segment Forecasts

Market Size, 2025

$113.9BMarket Estimate, 2026

$120.3BMarket Forecast, 2033

$183.3BCAGR, 2026–2033

6.2%Primary Pharmaceutical Packaging Market Summary

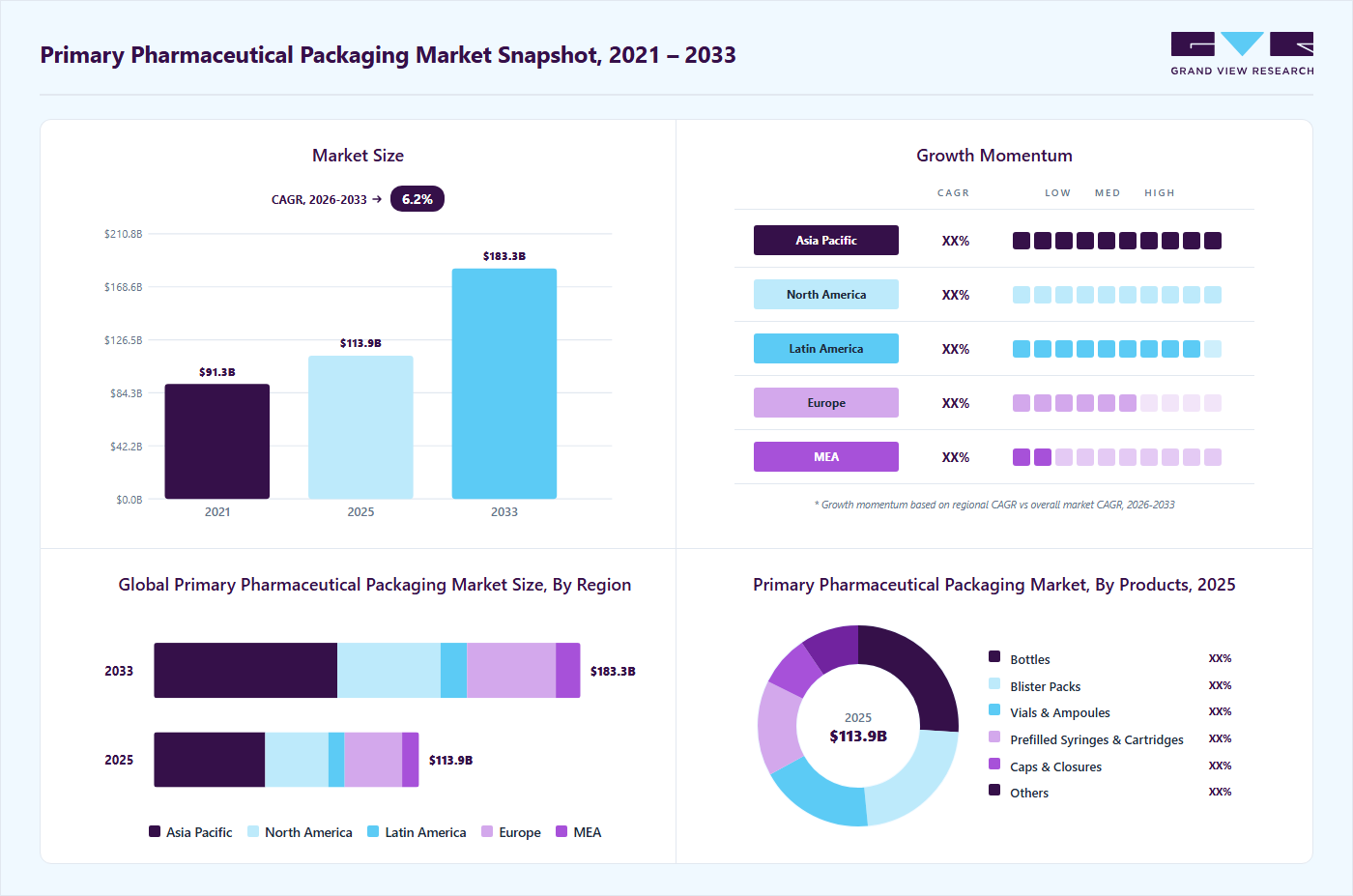

The global primary pharmaceutical packaging market size was valued at USD 113.9 billion in 2025 and is projected to grow from USD 120.3 billion in 2026 to USD 183.3 billion by 2033, at a CAGR of 6.2% from 2026 to 2033. The Asia Pacific primary pharmaceutical packaging market held the largest share of 42.0% of the global market in 2025. The demand for primary pharmaceutical packaging is rising significantly due to the growth of the global pharmaceutical industry and rising medicine consumption across both developed and emerging economies.

Key Market Trends & Insights

- By product, the bottles segment accounted for the largest revenue share of 26.0% in 2025 and is forecasted to grow at a significant CAGR from 2026 to 2033 in terms of revenue.

- By material, the glass segment is expected to grow at a CAGR of 6.6% over the forecast period.

Regional Highlights

- Largest regional market: Asia Pacific (42.0% revenue share, 2025)

- The primary pharmaceutical packaging market in the U.S. is expected to grow at a substantial CAGR of 6.5% from 2026 to 2033.

Market Size & Forecast

- Market size in 2025: USD 113.9 Billion

- Estimated market size in 2026: USD 120.3 Billion

- Projected market size by 2033: USD 183.3 Billion

- CAGR (2026-2033): 6.2%

An aging population, coupled with the rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer, is driving the need for safe and reliable drug delivery systems. In addition, the surge in biologics and specialty drugs has heightened the demand for advanced packaging solutions that ensure product stability and sterility. The expansion of generic drug manufacturing, particularly in countries like India and China, is further fueling packaging requirements. Moreover, the rise in vaccination programs and global immunization initiatives has accelerated the demand for vials, ampoules, and prefilled syringes. Increasing patient awareness regarding drug safety and packaging integrity is also contributing to market growth.

")

Key drivers include stringent regulatory requirements for drug safety, which mandate high-quality, contamination-free packaging solutions. The increasing adoption of biologics and injectable drugs is boosting demand for specialized packaging formats such as prefilled syringes and sterile vials. Growth in contract manufacturing organizations (CMOs) and pharmaceutical outsourcing is also expanding the need for scalable packaging solutions. In addition, the rise of e-commerce in pharmaceuticals has increased the importance of durable and tamper-evident packaging. Technological advancements in materials such as high-barrier plastics and glass alternatives are further supporting market growth. The need for extended shelf life and protection from environmental factors like moisture and oxygen is another critical factor.

Governments worldwide are implementing strict regulations and guidelines to ensure drug safety, efficacy, and traceability, which directly impact primary pharmaceutical packaging standards. Regulatory bodies such as the FDA and EMA enforce compliance with Good Manufacturing Practices (GMP) and serialization requirements, boosting demand for high-quality packaging solutions. In emerging economies, governments are supporting domestic pharmaceutical production through incentives and policy frameworks, indirectly driving packaging demand. Initiatives promoting healthcare access and affordability are increasing drug consumption, thereby expanding packaging needs. In addition, regulations focusing on anti-counterfeiting measures, such as track-and-trace systems, are encouraging the adoption of advanced packaging technologies.

The market is witnessing rapid innovation, particularly in the development of smart and sustainable packaging solutions. Technologies such as RFID tags, QR codes, and tamper-evident features are being integrated to enhance traceability and patient safety. There is a growing shift toward eco-friendly materials, including biodegradable plastics and recyclable glass alternatives, in response to environmental concerns. Prefilled syringes and auto-injectors are gaining popularity due to their convenience and reduced risk of dosing errors. Advances in material science are enabling the development of high-barrier packaging that extends drug shelf life.

Market Concentration & Characteristics

The primary pharmaceutical packaging industry exhibits a moderately consolidated structure, with a mix of large multinational players and regional manufacturers. Leading companies dominate through extensive product portfolios, global distribution networks, and strong compliance capabilities. However, the presence of numerous small and medium-sized enterprises catering to niche and regional demands adds a level of fragmentation.

Strategic collaborations, mergers, and acquisitions are common as companies aim to expand their technological capabilities and geographic reach. High entry barriers due to regulatory compliance and capital-intensive manufacturing processes limit new entrants. Innovation and product differentiation play a crucial role in maintaining a competitive advantage. Overall, while top players hold significant market share, regional competition remains strong.

The threat of substitutes in the primary pharmaceutical packaging industry is relatively low due to the critical role packaging plays in ensuring drug safety and efficacy. However, some substitution exists between materials, such as glass being replaced by high-performance plastics in certain applications. Advanced polymer-based packaging solutions are gaining traction as alternatives to traditional glass due to their durability and lightweight properties. Despite this, glass remains indispensable for certain drugs, especially biologics, due to its inert nature. Innovations in packaging formats may also shift demand between product types, such as vials to prefilled syringes. Regulatory approvals and compatibility requirements limit rapid substitution. Overall, while material substitution is evolving, complete replacement threats remain minimal.

Product Insights

The bottles segment recorded the largest market revenue share of 26.0% in 2025, due to its extensive use across a wide range of oral solid and liquid formulations. Plastic and glass bottles are widely preferred for tablets, capsules, syrups, and suspensions owing to their cost-effectiveness, durability, and ease of handling. Their compatibility with high-speed filling and sealing processes makes them ideal for large-scale pharmaceutical production. In addition, bottles offer strong protection against moisture and contamination, especially when combined with advanced closure systems. The growing demand for over-the-counter (OTC) drugs and generic medicines further supports segment dominance. Their widespread availability and adaptability across multiple drug types continue to reinforce their leading position in the market.

Prefilled syringes and cartridges are expected to witness significant growth due to the rising demand for biologics, injectable drugs, and self-administration systems. These formats enhance patient convenience, reduce dosing errors, and minimize the risk of contamination compared to traditional vial-and-syringe methods. The increasing prevalence of chronic diseases such as diabetes and autoimmune disorders is driving demand for injectable therapies, thereby boosting this segment. In addition, the growing adoption of home healthcare and self-injection devices is accelerating market expansion. Pharmaceutical companies are also focusing on ready-to-use drug delivery systems to improve efficiency and patient compliance. Technological advancements in materials and design, along with strong regulatory support for safe drug delivery, are further fueling growth in this segment.

Material Insights

The plastics & polymers segment accounted for the largest market share of 46.61% in 2025 and is expected to grow at a CAGR of 6.3% over the forecast period. The plastics & polymers segment holds a significant market share due to its versatility, cost-effectiveness, and wide applicability across various drug formats. Materials such as polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET) are extensively used for bottles, containers, closures, and blister packs owing to their lightweight nature and strong barrier properties. These materials offer excellent resistance to moisture, chemicals, and breakage, making them suitable for both solid and liquid formulations. In addition, plastics enable flexible design and compatibility with high-speed manufacturing processes, improving operational efficiency. The growing demand for unit-dose and tamper-evident packaging further supports segment growth.

The glass segment is expected to grow at a CAGR of 6.6% over the forecast period, primarily driven by its superior chemical inertness and high barrier properties. Glass is widely preferred for sensitive formulations such as biologics, injectables, and vaccines, as it does not react with drug components and ensures product stability. The increasing demand for sterile packaging formats like vials, ampoules, and prefilled syringes is significantly supporting segment expansion. In addition, the rise in global vaccination programs and injectable drug usage is boosting the need for high-quality glass packaging. Pharmaceutical companies continue to rely on glass due to its proven safety, transparency, and regulatory acceptance. Innovations such as strengthened and lightweight glass are further enhancing its usability. Despite competition from advanced polymers, glass remains a critical material for high-value and sensitive drug applications, driving its continued growth.

Region Insights

Asia Pacific dominated the market and accounted for the largest revenue share of over 42.0% in 2025, due to its large pharmaceutical manufacturing base and cost advantages. Countries like India and China are major hubs for generic drug production, driving significant demand for packaging materials. Rapid urbanization, increasing healthcare expenditure, and expanding access to medicines further contribute to market growth. The region also benefits from favorable government policies supporting pharmaceutical exports. Rising investments in healthcare infrastructure and growing domestic consumption are strengthening demand. In addition, the presence of numerous packaging manufacturers enhances supply chain efficiency. The increasing focus on quality standards is also boosting the adoption of advanced packaging solutions.

China Primary Pharmaceutical Packaging Market Trends

The primary pharmaceutical packaging market in China is driven by its massive pharmaceutical production capacity and strong government support for healthcare reforms. The country is focusing on upgrading manufacturing standards, which is increasing demand for high-quality packaging solutions. Growth in biologics and specialty drugs is further driving the need for advanced packaging formats. Domestic companies are investing heavily in automation and innovation to remain competitive. Export-oriented production also necessitates compliance with international packaging standards. Sustainability initiatives are gaining traction, encouraging eco-friendly packaging adoption. The expansion of healthcare coverage continues to boost pharmaceutical consumption.

North America Primary Pharmaceutical Packaging Market Trends

The primary pharmaceutical packaging market in North America represents a mature market with high demand for advanced and compliant packaging solutions. The presence of leading pharmaceutical companies and strict regulatory frameworks drives innovation in packaging technologies. Increasing use of biologics and personalized medicine is fueling demand for specialized packaging formats. The region is also witnessing strong adoption of smart packaging technologies for traceability. High healthcare expenditure and strong R&D investments support market growth. In addition, the trend toward sustainable packaging is gaining momentum. Contract manufacturing and outsourcing further contribute to demand.

The U.S. primary pharmaceutical packaging market is characterized by stringent FDA regulations and a strong focus on drug safety and serialization. The high adoption of biologics and injectable drugs is driving demand for vials, ampoules, and prefilled syringes. Technological advancements and innovation in packaging materials are key growth factors. The country also leads in the adoption of smart packaging solutions. Increasing investments in pharmaceutical R&D are further boosting demand. Sustainability initiatives are encouraging the shift toward recyclable materials. The presence of major market players strengthens competitive dynamics.

Europe Primary Pharmaceutical Packaging Market Trends

The primary pharmaceutical packaging market in Europe is driven by strict regulatory standards and a strong emphasis on sustainability. The region is witnessing increased demand for eco-friendly packaging solutions due to environmental regulations. Growth in biologics and specialty pharmaceuticals is boosting demand for advanced packaging formats. Countries like Germany and France are leading in pharmaceutical innovation, supporting market growth. The adoption of serialization and anti-counterfeiting measures is widespread. In addition, the region benefits from a well-established healthcare infrastructure. Continuous investments in R&D are further driving innovation.

Germany primary pharmaceutical packaging market is a key contributor to the European market due to its strong pharmaceutical and packaging industries. The country emphasizes high-quality manufacturing and compliance with stringent regulations. Demand for advanced packaging solutions is driven by the growth of biologics and specialty drugs. Germany is also at the forefront of sustainable packaging innovations. The presence of leading packaging manufacturers supports market expansion. Export-oriented pharmaceutical production further boosts demand. Technological advancements in packaging processes are enhancing efficiency.

Key Primary Pharmaceutical Packaging Company Insights

The competitive landscape of the market is characterized by the presence of established global players alongside regional manufacturers, creating a moderately consolidated yet competitive environment. Leading companies focus on expanding their product portfolios across glass, plastics, and advanced drug delivery systems such as prefilled syringes to cater to evolving pharmaceutical needs. Competition is largely driven by compliance with stringent regulatory standards, product quality, and innovation in high-barrier and sterile packaging solutions. Strategic initiatives such as mergers, acquisitions, and partnerships are commonly adopted to enhance technological capabilities and strengthen global presence. In addition, companies are increasingly investing in sustainable packaging materials and smart packaging technologies to gain a competitive edge. While large players dominate high-value segments like biologics packaging, regional firms remain competitive in cost-sensitive and generic drug packaging markets, maintaining a balanced industry structure.

-

In April 2025, Amcor plc announced the successful completion of its all-stock combination with Berry Global. Through this combination, Amcor enhances its position as a global leader in consumer and healthcare packaging solutions, with the unique materials science and innovation capabilities required to revolutionize product development and meet customers' and consumers' sustainability aspirations.

-

In October 2024, Gerresheimer AG launched the Gx Elite RTF syringe platform, offering silicone oil-free, tungsten-free, and low-particle solutions, improving compatibility for advanced drug formulations and biologics.

Key Primary Pharmaceutical Packaging Companies:

The following key companies have been profiled for this study on the primary pharmaceutical packaging market.

- Amcor plc

- Gerresheimer AG

- SCHOTT AG

- West Pharmaceutical Services, Inc.

- AptarGroup, Inc.

- Becton, Dickinson and Company

- Berry Global

- CCL Industries

- SGD Pharma

- Nipro Corporation

Primary Pharmaceutical Packaging Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 120.3 billion

Revenue forecast in 2033

USD 183.3 billion

Growth rate

CAGR of 6.2% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, material, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; Australia; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

Amcor plc; Gerresheimer AG; Becton; Dickinson and Company; West Pharmaceutical Services, Inc.; Berry Global; ITC Packaging; Nipro Corporation; AptarGroup, Inc.; SGD Pharma; SCHOTT AG; CCL Industries

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Primary Pharmaceutical Packaging Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global primary pharmaceutical packaging market report based on product, material, and region:

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Bottles

-

Blister Packs

-

Vials & Ampoules

-

Prefilled Syringes & Cartridges

-

Caps & Closures

-

Others

-

-

Material Outlook (Revenue, USD Billion, 2021 - 2033)

-

Plastics & Polymers

-

Glass

-

Aluminum/Foils

-

Rubber/Elastomers

-

Others

-

-

Region Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The global primary pharmaceutical packaging market size was estimated at USD 113.9 billion in 2025 and is expected to reach USD 120.3 billion in 2026.

The global primary pharmaceutical packaging market is expected to grow at a compound annual growth rate of 6.2% from 2026 to 2033 to reach USD 183.3 billion by 2033.

Asia Pacific dominated the market and accounted for the largest revenue share of over 42.0% in 2025, due to its large pharmaceutical manufacturing base and cost advantages.

Some key players operating in the primary pharmaceutical packaging market include Amcor plc, Gerresheimer AG, Becton, Dickinson and Company, West Pharmaceutical Services, Inc., Berry Global, ITC Packaging, Nipro Corporation, AptarGroup, Inc., SGD Pharma, SCHOTT AG, and CCL Industries

The demand for primary pharmaceutical packaging is rising significantly due to the growth of the global pharmaceutical industry and rising medicine consumption across both developed and emerging economies. An aging population, coupled with the rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer, is driving the need for safe and reliable drug delivery systems.

Bottles segment accounted for the largest revenue share of 26.0% in 2025 and is forecasted to grow at a significant CAGR from 2026 to 2033

Plastics & polymers held the largest share (over 46.61%) in 2025, while glass segment is expected to grow at a CAGR of 6.6% over the forecast period

Asia Pacific dominated with a 42.0% revenue share in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.