- Home

- »

- IT Services & Applications

- »

-

PropTech Market Size, Share & Trends Report, 2026-2033GVR Report cover

![PropTech Market (2026 - 2033)Report]()

PropTech Market (2026 - 2033)

Size, Share & Trends Analysis Report By Property Type (Residential, Commercial & Industrial), By Deployment (Cloud, On-premise), By Solution, By End-use, By Region, And Segment Forecasts

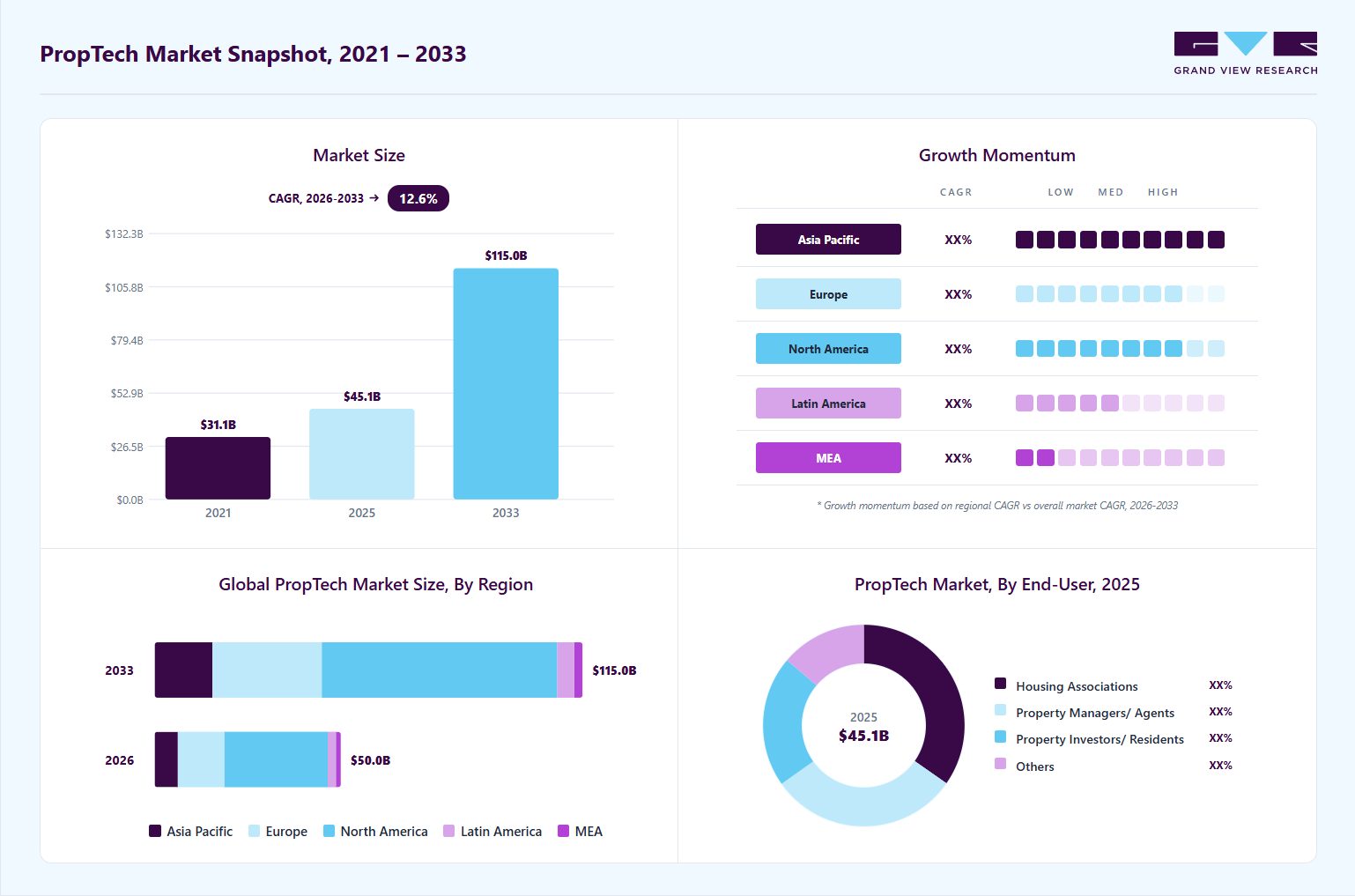

Market Size, 2025

$45.1BMarket Estimate, 2026

$50.1BMarket Forecast, 2033

$115.0BCAGR, 2026–2033

12.6%PropTech Market Summary

The global PropTech market size was valued at USD 45.1 billion in 2025 and is projected to grow from USD 50.1 billion in 2026 to USD 115.0 billion by 2033, at a CAGR of 12.6% from 2026 to 2033. The market in North America dominated with a revenue share of 55.5% in 2025. The growth is anticipated to be driven by the increasing adoption of several cutting-edge technologies, such as the Internet of Things (IoT), machine learning (ML), artificial intelligence (AI), and virtual reality (VR), across the real estate industry.

Key Market Trends & Insights

- By property type: Residential segment held the largest market share of 56.3% in 2025.

- By deployment: Cloud-based segment held the largest market share of 51.0% in 2025.

- By solution: Software segment held the largest market share of 62.0% in 2025.

- By end-use: Housing association segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (55.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 45.1 Billion

- Estimated market size in 2026: USD 50.1 Billion

- Projected market size by 2033: USD 115.0 Billion

- CAGR (2026-2033): 12.6%

Additionally, adopting such technologies helps streamline data management and simplifies massive property management operations. Furthermore, AI helps in understanding and recommending client preferences. AI in the real estate sector can help fine-tune advertising efforts by spotting trends and delivering actionable insights to clients and customers. The growth is expected to be driven by the increasing demand for property management software (PMS) and asset management software. Using the software provides efficiency in transactional costs and the development of consumer convenience, with the customer always being the priority. Furthermore, such software offers easy maintenance monitoring, smoother payments among tenants and contractors, data tracking, and quick inspection. A PMS shortens the time it takes to reply to tenant or owner concerns and grievances.")

The property technology (PropTech) industry is expected to be driven by the increasing adoption of big data analytics, owing to the benefits offered, such as helping in increasing overall productivity, making better decisions, improving customer service, and increasing overall revenue. Property investors are profiting from the insights provided by big data solutions, ranging from understanding the best investments to marketing and selling. Additionally, most companies are inclined to use big data techniques to differentiate themselves and stay competitive in the business.

For instance, Zillow Rental Manager is one of the "big data" programs that sets the trends in the real estate industry. By leveraging big data, agents can provide customers with the property details they have shown interest in. Additionally, financial risks are decreased when big data is used in commercial real estate. It examines all available information about a property and its previous owners to assess its value and recommend the next steps.

Moreover, the adoption of cloud computing is one of the key developments in the real estate industry. Cloud computing has substantially altered how software programs are managed and delivered to end users. Such advancements have enabled software developers to focus on cloud-based software technology. Multifamily residential property management businesses may readily incorporate Software as a Service (SaaS) platforms to integrate online payment solutions with their property management software, enabling easier transactions.

Market Dynamics

The increasing investment in smart city development is driving the industry. Governments and urban planners are investing heavily in intelligent transportation systems, digital public infrastructure, connected utilities, and sustainable urban development projects. Smart buildings are becoming a foundational element within these broader smart city ecosystems. PropTech solutions help integrate buildings with urban infrastructure networks through real-time data exchange, digital management systems, and automated operational coordination. This enables more efficient management of utilities, mobility, public safety, and environmental monitoring across urban spaces. As cities continue modernizing infrastructure through digital transformation, the role of PropTech platforms within connected urban ecosystems continues to expand.

According to Grand View Research, in 2024, the smart building startup ecosystem attracted USD 7.5 billion in investments. During the first half of 2025, a total of 126 funding rounds were recorded, amounting to USD 3.1 billion in investments. This represented a 13% decline compared to 145 funding rounds during the same period in the previous year, indicating comparatively weaker investor interest in the sector in 2025. At the same time, startup acquisition activity increased significantly, with 42 acquisitions completed in the first half of 2025, reflecting a 60% rise over the corresponding period last year.

High implementation and technology integration costs represent a significant restraint on the PropTech market, as adopting advanced digital real estate solutions often requires substantial upfront investment in software platforms, hardware infrastructure, and system customization. Many PropTech solutions involve integrating multiple technologies such as building management systems, IoT sensors, data analytics platforms, CRM systems, and cloud-based property management tools. This integration process can be technically complex and expensive, especially for legacy buildings and traditional real estate firms that lack modern digital infrastructure. As a result, organizations must spend heavily not only on software licensing but also on system upgrades and compatibility adjustments. Smaller property owners, developers, and facility managers often find these costs difficult to justify, which slows down widespread adoption. This financial barrier limits the pace at which PropTech solutions penetrate traditional real estate markets.

The growing adoption of virtual tours and digital property showcasing is creating a major opportunity for the industry because it is transforming how residential, commercial, and industrial properties are marketed and evaluated. Traditional property visits often require significant time, travel coordination, and physical site inspections, which can slow down the buying or leasing process. Virtual tour technologies allow potential buyers, tenants, and investors to explore properties remotely through immersive digital experiences. PropTech platforms integrate 3D visualization, interactive walkthroughs, augmented reality, and high-resolution property imagery to create realistic property presentations. This significantly improves customer engagement and expands market reach beyond local geographic boundaries. As digital-first property discovery becomes more common, demand for virtual showcasing solutions continues to rise rapidly.

According to recent Matterport data, properties with immersive digital tour experiences can sell up to 31% faster than traditional listings. The impact is also reflected in property values, with homes offering 3D virtual tours achieving sale prices up to 9% higher. Also, 3D tours receive nearly 2,000% more views than standard video tours, while video tours attract around 400% more attention than static images. Around 72% of buyers find that these interactive experiences help them feel more emotionally connected to a property. In addition, nearly half of prospective buyers prefer tools that help them better understand a home’s layout, making self-guided 3D virtual tours an increasingly valuable feature in modern real estate marketing.

Market Concentration & Characteristics

The industry is moderately fragmented, with a mix of global real estate technology platforms, SaaS providers, and specialized startups serving segments such as property management, digital listings, smart buildings, and real estate analytics. Established technology and platform players such as Zillow and CoStar Group hold strong positions due to their large property databases, data-driven platforms, and wide user networks. Entry barriers are moderate, as data access, network effects, and integration with real estate ecosystems are critical for scaling.

The industry is highly digitalization-driven, with strong adoption of AI-based property valuation, virtual tours, digital transactions, and cloud-based property management systems. Demand is primarily fueled by increasing urbanization, rising real estate investment activity, and the shift toward online property discovery and transactions. Smart building technologies and IoT-enabled infrastructure are also becoming important drivers of modernization in both residential and commercial real estate.

Competitive intensity is increasing, but customer switching costs remain moderate because multiple platforms often coexist in real estate workflows. However, data lock-in, user base concentration, and ecosystem integration can create strong retention for leading platforms. Innovation in AI-driven valuation, smart building automation, and immersive property experiences continues to be the key competitive differentiator in the market.

Property Type Insights

The residential segment accounted for the highest market share of 56.3% in 2025. This dominance is attributed to technological advancements in the residential sector across the real estate industry. The residential sector has drawn more attention from tech companies, which offer services such as digital closings and virtual open houses. Technological developments have made the first steps easier to reach for prospective house buyers. They can search for houses on various platforms, assess features and costs, and even take virtual tours. Thus, most tech start-ups are inclined to offer customized housing solutions that meet consumer requirements, which, in turn, is boosting the residential segment’s growth. The residential segment is further categorized into multifamily apartments/housing, single-family housing, and others. The multifamily segment is expected to register considerable growth over the forecast period.

The commercial and industrial segment is anticipated to register the fastest CAGR over the forecast period. The growth of the segment is attributed to the increasing demand for office spaces and growing urbanization across the globe. The use of cutting-edge technology for property management in the commercial and industrial real estate sector has observed significant growth in the past few years. In the commercial and industrial sectors, property technology is completely revamping office buildings. PropTech solutions that integrate with IoT and smart devices are changing workspaces into smart offices. Thus, PropTech has become an essential tool in the commercial and industrial sectors. Moreover, the commercial and industrial segment comprises various sub-segments, including retail, office, hotel, and warehouse spaces, among others.

Solution Insights

The software segment accounted for the highest revenue share in 2025 and is projected to continue its dominance in the coming years. The segment's growth is attributed to the benefits of proptech software, such as its assistance in helping real estate managers and agents market properties more quickly, efficiently, and with higher-quality results. The software segment is further divided into property management, asset management, sales and advertisements, work order management, customer relationship management, and others. Property management dominated the market in 2025 and is expected to maintain its dominance, owing to the benefits it offers, including quick access to information, cost efficiency, and improved communication.

The services segment is expected to register the highest CAGR over the forecast period. The segment's growth is attributed to the increasing demand for property search tools, new renting practices, selling alternatives, and new concept agents & landlord services, among others. The services segment is further divided into professional and managed services. The professional services segment dominated the market in 2025 and is expected to continue its dominance during the forecast period. The segment's growth is owing to the increasing demand for professional services across the real estate sector, such as consulting, advisory, and portfolio analysis.

Deployment Insights

The cloud-based segment accounted for the largest revenue share in 2025. The segment's growth is driven by the growing adoption of cloud deployment across various end users, including housing associations, property managers, property investors, and others. Additionally, features such as ease of use, scalability, affordability, and reduced tenant conflicts are motivating small, medium, and large businesses to switch to cloud-based proptech solutions. In addition, cloud-based deployment provides businesses with backup and seamless data integration, helping prevent data loss. Additionally, it saves property managers direct and indirect expenses by automating a labor-intensive process.

The on-premises segment is anticipated to register significant growth over the forecast period. The growth is driven by the benefits of on-premises deployments, such as control and ownership of hardware and a higher level of data security than cloud-based proptech software. In addition, on-premises deployment offers businesses or firms the ability to customize their systems to their requirements. The benefits of on-premises deployment mentioned contribute to the segment's growth during the forecast period.

End Use Insights

The housing association segment accounted for the highest market share in 2025. This growth is attributed to the challenges faced by townships and apartments, including collecting payments, performing maintenance, and tracking tenants. All such challenges have forced key players in the market to provide solutions for payment tracking, inspections, and transparent and comprehensive reporting. Affordable housing using property technology software helps assign correct rent payments based on the amount contributed by the rent payer relative to the government payment.

The property managers/agents segment is anticipated to register the fastest CAGR during the forecast period. This expansion of the segment is driven by the rising number of commercial buildings and real estate developments across the globe. PropTech adoption by property managers has the potential to significantly impact and improve their business models. For instance, agents can improve the availability of their property information by using PropTech's machine learning and AI tools. Tenants can find it easier to get the answers they need if the search engine includes a chatbot AI that responds to client questions and requests without human intervention. Furthermore, proptech software helps property managers and agents maintain track of all properties, including essential maintenance work, automation, better communication, and easier accessibility.

Regional Insights

North America PropTech market accounted for the largest revenue share of 55.5% in 2025. The regional growth is attributed to the presence of prominent players in the region, such as Ascendix Technologies, Zumper Inc., Opendoor, and Altus Group, among others. The real estate sector in North America is growing and is one of the most stable and promising industries. The region is considered an early adopter of technology. The millennial generation in the region, which is well-versed in technology, accounts for around 43% of the housing market, driving up demand for smart homes with IoT-enabled devices. This, in turn, is boosting the market growth in North America.

U.S. PropTech Market Trends

The PropTech industry in the U.S. is projected to grow significantly during the forecast period. The increasing demand for improved tenant experience and digital-first property services is a major driver in the U.S. PropTech market. Tenants in residential and commercial spaces now expect seamless digital interactions, including online leasing, virtual property tours, mobile maintenance requests, and smart access control systems. PropTech platforms enable property managers to meet these expectations by offering integrated digital ecosystems that enhance convenience and communication. This improves tenant retention rates and strengthens competitiveness in highly saturated urban real estate markets. Enhanced user experience has become a key differentiator for property owners in attracting and retaining tenants. As consumer expectations continue to evolve, digital property services are becoming standard across the U.S. real estate sector.

Asia Pacific PropTech Trends

The PropTech industry in Asia Pacific is expected to grow at the fastest CAGR from 2026 to 2033. The increasing penetration of mobile internet and digital ecosystems across the Asia Pacific is another major driver supporting PropTech adoption. A large proportion of real estate transactions, tenant interactions, and property searches is now shifting to mobile platforms due to widespread smartphone use and improved internet connectivity. PropTech companies are leveraging this trend by offering mobile-first applications that enable property listings, virtual tours, rental payments, and maintenance requests through digital interfaces. This has significantly improved accessibility to real estate services, especially in developing economies where digital adoption is rapidly increasing. The convenience of mobile-based property management is encouraging both consumers and businesses to transition away from traditional offline processes. As digital connectivity continues to expand, PropTech platforms are becoming deeply integrated into everyday real estate activities.

The China PropTech industry is projected to grow significantly during the forecast period. The rapid digitalization of real estate transactions and property services is significantly driving PropTech growth in China. Online platforms for property listing, virtual tours, digital leasing, and mobile payment integration have become widely accepted among consumers and real estate professionals. This shift is improving transparency and efficiency in property transactions while reducing dependence on traditional brokerage channels. PropTech solutions are enabling faster decision-making by providing users with real-time data on pricing, availability, and market trends. The widespread use of mobile applications and digital ecosystems is making real estate services more accessible to a large urban population. As digital transaction systems continue to mature, PropTech platforms are becoming the standard mode of property engagement.

Europe PropTech Market Trends

The PropTech industry in Europe is anticipated to grow steadily from 2026 to 2033. The expansion of urban regeneration and infrastructure redevelopment projects is supporting PropTech adoption across Europe. Many cities are investing in upgrading aging buildings, redeveloping industrial zones, and modernizing public infrastructure to improve urban living standards. These projects require advanced planning, monitoring, and management tools capable of handling complex redevelopment workflows. PropTech solutions help optimize construction planning, asset tracking, and long-term property performance management during redevelopment cycles. This improves efficiency and reduces risks associated with large-scale urban transformation projects. As urban redevelopment initiatives continue across Europe, PropTech platforms are becoming increasingly important in managing modern real estate ecosystems.

The UK PropTech industry is driven by the rapid digital transformation of the real estate sector, as property developers, landlords, and facility managers increasingly adopt technology-enabled platforms to improve efficiency and transparency. Traditional property processes such as leasing, tenant communication, maintenance coordination, and asset tracking are being replaced by digital systems that streamline operations across residential and commercial portfolios. This shift is reducing administrative workload while improving decision-making speed and accuracy in property management. As a result, adoption of PropTech solutions is expanding steadily across the UK real estate ecosystem. The country’s mature financial and real estate markets further support early adoption of advanced digital solutions. This ongoing transformation of property operations is a key structural driver of market growth.

Key PropTech Company Insights

Some prominent players in the PropTech market include Autodesk, Inc. and Nemetschek Group, among others.

-

Autodesk, Inc. is a global software company specializing in design, engineering, and digital content creation technologies. Autodesk provides a comprehensive and integrated portfolio of solutions that facilitate design, modeling, simulation, and project management. Its offerings include advanced tools for building information modeling (BIM), 3D design, drafting, and structural analysis, enabling professionals to create highly detailed digital representations of buildings and infrastructure projects. These solutions allow architects, engineers, and contractors to collaborate in real time, improve design accuracy, detect potential issues early, and optimize project execution.

-

Nemetschek Group is a Germany-based global software provider specializing in solutions for the architecture, engineering, construction, and media industries. Nemetschek Group offers a broad, diversified portfolio spanning design, modeling, planning, construction execution, and facility management. Its solutions include tools for building information modeling (BIM), 3D design, structural engineering, project planning, cost estimation, and asset lifecycle management. By enabling the creation of detailed digital building models and facilitating collaboration across stakeholders, Nemetschek’s software helps improve design accuracy, reduce errors, and enhance project efficiency.

Key PropTech Companies

The following key companies have been profiled for this study on the propTech market.

-

Altus Group

-

Ascendix Technologies

-

Coadjute

-

Enertiv

-

Guesty Inc.

-

HoloBuilder, Inc.

-

Homelight

-

ManageCasa

-

Opendoor

-

Proptech group

-

Qualia

-

Reggora

-

Vergesense

-

Zillow, Inc.

-

Zumper Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Zillow, Inc.; CBRE Group; Altus Group; Ascendix Technologies

- Mature players in the PropTech market focus on integrating real estate data, brokerage services, and digital property platforms.

- Many expand through enterprise real estate management and commercial leasing solutions. Their strategy centers on end-to-end digital transformation of property lifecycle management.

- Mature players benefit from massive real estate data assets and strong global client bases. Their platforms are widely used for property listing, valuation, and asset management.

- Advanced analytics improves pricing accuracy and market forecasting. Strong brand trust supports high institutional adoption.

- These players often depend on traditional real estate revenue models alongside digital platforms. Innovation can be slower due to legacy business structures.

- High operational complexity affects agility in product development. Smaller tech-focused competitors can outperform them in niche digital features.

Emerging Players: Guesty Inc.; Coadjute; Enertiv; Reggora

- Emerging players focus on fully digital real estate transactions and property management platforms. They use AI, automation, and blockchain to buy, sell, and lease properties.

- Many target residential markets with simplified online experiences. Their strategy emphasizes reducing friction in real estate transactions.

- Emerging players offer faster, more transparent property transactions. Their platforms reduce dependence on traditional brokers and paperwork.

- Strong UX design improves customer adoption in residential segments. They also innovate quickly in digital and fintech-driven real estate models.

- Emerging players face regulatory challenges in different real estate markets. They often lack access to large-scale commercial property portfolios.

- Limited brand trust compared to established firms affects enterprise adoption. Financial instability can restrict long-term expansion and scaling.

Recent Developments

-

In April 2026, Coadjute launched the deployment of Clara, the UK’s first digital human created to assist estate agents, buyers, and sellers with critical anti-money laundering (AML) checks. The company offers a fully managed solution that integrates an advanced technology platform with a UK-based compliance team to simplify and streamline regulatory compliance processes. Clara marks the next evolution of the company’s technology capabilities by delivering digital-human support for AML verification and compliance activities.

-

In April 2026, HomeLight launched EVA, an AI-powered escrow agent designed to automate a significant share of the tasks involved in closing real estate transactions. Marketed as the real estate industry’s first agentic escrow officer, EVA can operate across more than 80 integrated tools to communicate with external systems and improve workflow efficiency. The platform uses advanced AI capabilities to manage a large portion of transaction file activities, such as opening orders, requesting HOA documents and title reports, coordinating with lenders, processing wire transfers, and supporting other essential escrow functions.

PropTech Market Report Scope

Report Attribute

Details

Market size in 2025

USD 45.1 billion

Estimated market size in 2026

USD 50.1 billion

Projected market size by 2033

USD 115.0 billion

Growth rate

CAGR of 12.6% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Property type, solution, deployment, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Altus Group; Ascendix Technologies; Coadjute; Enertiv; Guesty Inc.; HoloBuilder, Inc.; Homelight; ManageCasa; Opendoor; Proptech group; Qualia; Reggora; Vergesense; Zillow, Inc.; Zumper Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global PropTech Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global PropTech market report based on property type, solution, deployment, end use, and region:

-

Property Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Residential

-

Multi-Family Housing

-

Single Family Housing

-

Others

-

-

Commercial & Industrial

-

Retail Spaces

-

Office Spaces

-

Hotels

-

Warehouses

-

Others

-

-

-

Solution Outlook (Revenue, USD Million, 2021 - 2033)

-

Software

-

Property Management

-

Rental Listings Management

-

Applicant Management

-

Reporting & Analytics

-

Maintenance Activities Management

-

Others

-

-

Asset Management

-

On/Offline Rent Payments

-

Portfolio Management

-

Evaluation and Financial Management

-

Others

-

-

Sales and Advertisements

-

Workorder Management

-

Customer Relationship Management

-

Customer Service

-

Customer Experience Management

-

CRM Analytics

-

Marketing Automation

-

Social Media Monitoring

-

-

Others

-

-

Services

-

Professional Services

-

Managed Services

-

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud-based

-

On-Premises

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Housing Associations

-

Property Managers/ Agents

-

Property Investors

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

PropTech Market Opportunity Assessment for Real Estate Technology Provider

Analysis of digital property management, online leasing, smart building operations, and virtual property showcasing trends across residential and commercial real estate

Evaluation of industry challenges, including fragmented tenant communication, manual documentation, delayed property transactions, and inefficient facility management workflows

Identified high-growth customer segments adopting digital real estate solutions

Improved positioning around operational efficiency, tenant experience, and property visibility

Smart Property Management Platform Strategy for SaaS Provider

Identification of operational pain points, including delayed maintenance response, disconnected property data, and inefficient facility coordination

Evaluation of demand for mobile-first property management platforms integrated with IoT-enabled smart building technologies

Improved differentiation through automation, centralized operations, and better tenant experience

Increased customer retention through efficient maintenance and communication workflows

Real Estate Transaction Digitization Strategy for Property Technology Company

Analysis of digital transaction workflows, including virtual tours, e-signatures, AI-based property recommendations, and online documentation processes

Evaluation of adoption barriers such as legacy broker dependency, data privacy concerns, and integration complexity with existing real estate systems

Assessment of customer demand for faster transaction processing, transparent communication, and digital mortgage or financing support

Accelerated digital transaction adoption through streamlined workflows

Reduced operational delays using automated documentation and communication tools

Improved customer experience with faster, transparent, and digitally enabled property transactions

Frequently Asked Questions About This Report

The global PropTech market is expected to grow at a compound annual growth rate of 12.6% from 2026 to 2033 to reach USD 115.0 billion by 2033.

Key factors include the increasing adoption of several cutting-edge technologies, such as the Internet of Things (IOT), machine learning (ML), artificial intelligence (AI), and virtual reality (VR), across the real estate industry. Additionally, adopting such technologies helps streamline data management and simplifies massive property management operations.

The global PropTech market size was estimated at USD 45.1 billion in 2025 and is expected to reach USD 50.1 billion in 2026.

Some prominent players in the proptech market include Ascendix Technologies, Zumper Inc., Opendoor, Altus Group, Guesty Inc., HoloBuilder, Inc., Zillow, Inc., ManageCasa, Reggora, Qualia, Vergesense, and Coadjute among others.

North America dominated with a 55.5% revenue share in 2025.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.