- Home

- »

- Plastics, Polymers & Resins

- »

-

Protective Packaging Market Size, Share Report, 2026-2033GVR Report cover

![Protective Packaging Market (2026 - 2033)Report]()

Protective Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Flexible, Foam, Rigid), By Material (Paper & Paperboard, Plastic, Plastic Foams), By Function (Void Fill, Wrapping, Insulation, Blocking & Bracing), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$40.4BMarket Estimate, 2026

$41.5BMarket Forecast, 2033

$57.0BCAGR, 2026–2033

4.6%Protective Packaging Market Summary

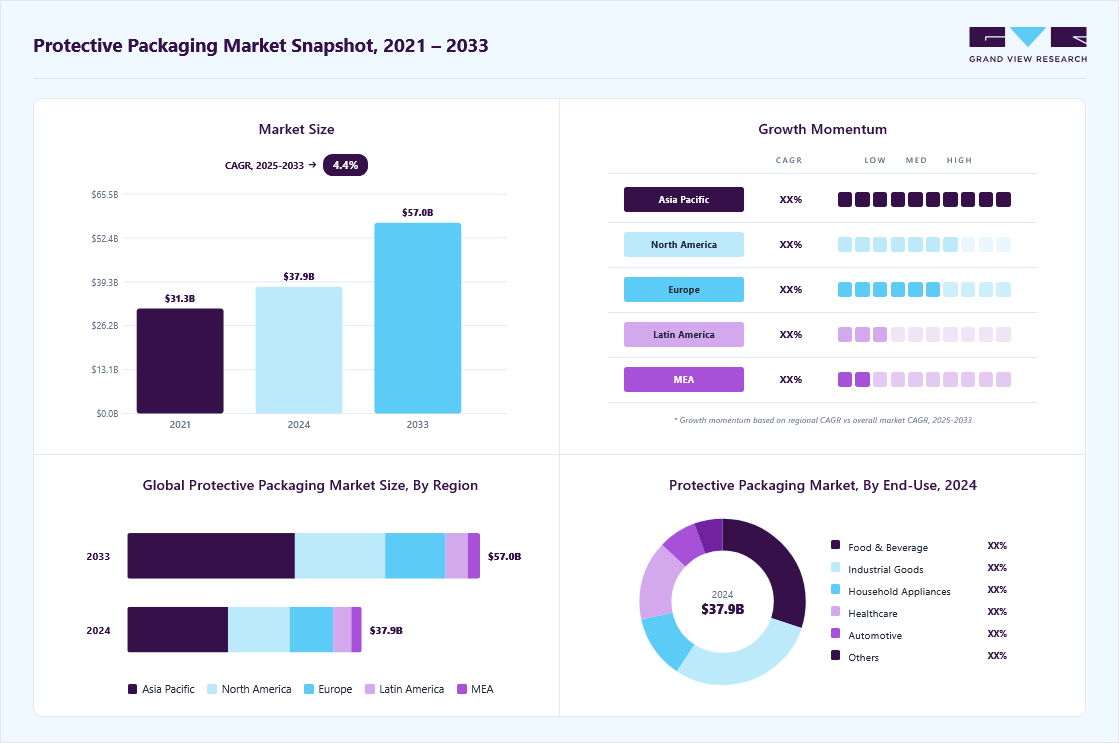

The global protective packaging market size was valued at USD 40.4 billion in 2025 and is projected to grow from USD 41.5 billion in 2026 to USD 57.0 billion by 2033, at a CAGR of 4.6% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 43.5% in 2025. The rapid growth of e-commerce and online retail has been the most significant driver of the market.

Key Market Trends & Insights

- By type: Flexible segment led the market with the largest revenue share of 66.4% in 2025.

- By material: Paper & Paperboard segment led the market with the largest revenue share of 45.7% in 2025.

- By function: Wrapping segment led the market with the largest revenue share of 29.3% in 2025.

- By end use: Food & Beverage segment led the market with the largest revenue share of 24.3% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (43.5% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 40.4 Billion

- Estimated market size in 2026: USD 41.5 Billion

- Projected market size by 2033: USD 57.0 Billion

- CAGR (2026-2033): 4.6%

With consumers increasingly shopping online for everything from electronics to groceries, there is growing demand for packaging solutions that protect items during storage and transit. Companies such as Amazon and Alibaba have revolutionized retail logistics, creating massive demand for protective materials such as air pillows, bubble wrap, foam inserts, and corrugated packaging to ensure products reach customers safely. Rising consumer electronics sales and the increasing complexity of electronic devices have also fueled market growth. Smartphones, laptops, tablets, and other sensitive electronic equipment require sophisticated protective packaging solutions to prevent damage from shock, vibration, and static electricity. For instance, companies such as Apple and Samsung utilize custom-molded foam inserts, anti-static bags, and reinforced corners in their product packaging to protect high-value devices during shipping and handling.Environmental concerns and sustainability initiatives are reshaping the protective packaging landscape. There is growing pressure to reduce plastic waste and develop eco-friendly alternatives. This has led to innovations in biodegradable protective materials, recyclable packaging solutions, and the use of recycled content in traditional protective materials.

")

The healthcare and pharmaceutical sectors represent another major growth driver, particularly following the COVID-19 pandemic. The need to safely transport temperature-sensitive vaccines, biological materials, and medical devices has increased demand for specialized protective packaging solutions. This includes materials with thermal insulation properties, shock-absorbing capabilities, and sterility maintenance features. For example, the distribution of COVID-19 vaccines required sophisticated cold chain packaging solutions with multiple protective layers to maintain precise temperature control during shipping.

Market Dynamics

The protective packaging market is experiencing consistent growth, driven by the increasing need for product protection across industries such as e-commerce, electronics, pharmaceuticals, food & beverages, and industrial manufacturing. Protective packaging solutions play a vital role in minimizing product damage, maintaining product quality, and ensuring safe transportation throughout the supply chain. The rapid expansion of online retail, global trade activities, and temperature-sensitive product shipments is fueling demand for advanced cushioning, void-fill, and insulated packaging materials. Furthermore, growing emphasis on sustainable packaging practices and the development of recyclable and biodegradable protective packaging solutions are encouraging end users to adopt innovative packaging formats, supporting market growth worldwide.

The rapid growth of e-commerce and direct-to-consumer (DTC) distribution channels is one of the primary drivers of the protective packaging market. As online retailers handle increasing volumes of shipments, the need for reliable packaging solutions that protect products from damage during transit has become critical. Protective packaging materials such as air cushions, bubble wraps, paper-based void fillers, and foam inserts help reduce product returns, enhance customer satisfaction, and ensure products reach consumers in optimal condition.

The growing cross-border trade and rising consumer expectations for safe and timely deliveries are encouraging businesses to invest in advanced protective packaging solutions. Industries such as electronics, consumer goods, healthcare, and food & beverages are increasingly adopting customized protective packaging to safeguard fragile and high-value products. This trend is further accelerating innovation in lightweight, cost-efficient, and sustainable protective packaging materials, supporting overall market growth.

One of the significant restraints affecting the protective packaging market is the growing environmental concern associated with plastic-based packaging materials. Many widely used protective packaging products, including foam inserts, bubble wraps, and air cushions, are manufactured from plastics that contribute to packaging waste and recycling challenges. Increasing government regulations aimed at reducing single-use plastics, along with stricter sustainability requirements from businesses and consumers, are placing pressure on manufacturers to develop eco-friendly alternatives. While sustainable materials are gaining traction, they often involve higher production costs and may not always provide the same level of protection or cost efficiency as conventional materials, creating challenges for widespread adoption and market growth.

The increasing demand for sustainable packaging presents a significant opportunity for the market. As businesses across industries seek to reduce their environmental footprint, there is growing adoption of recyclable, biodegradable, compostable, and paper-based protective packaging materials. E-commerce companies, consumer goods manufacturers, and logistics providers are increasingly prioritizing eco-friendly packaging solutions to meet regulatory requirements and evolving consumer preferences. This shift is encouraging innovation in sustainable cushioning, void-fill, and protective wrapping materials that offer effective product protection while minimizing environmental impact. As sustainability becomes a key purchasing criterion, manufacturers that develop high-performance and environmentally responsible protective packaging solutions are expected to gain a competitive advantage and unlock new growth opportunities.

Analyst Perspective

The protective packaging market is positioned for sustained growth, supported by the expansion of e-commerce, global trade, healthcare logistics, and high-value product shipments that require effective protection during storage and transportation. As businesses increasingly focus on minimizing product damage, reducing return rates, and improving supply chain efficiency, demand is rising for advanced cushioning, void-fill, insulation, and protective wrapping solutions. The market is also witnessing a strong shift toward sustainable packaging materials, driven by environmental regulations and growing consumer preference for eco-friendly alternatives. Going forward, manufacturers that can balance product protection, cost efficiency, and sustainability through innovative material development and customized packaging solutions will be well positioned to capitalize on emerging growth opportunities across diverse end-use industries.

Type Insights

Based on type, the fexible segment led the market with the largest revenue share of 66.4% in 2025 and is expected to grow at the fastest CAGR over the forecast period. Flexible protective packaging includes products such as bubble wrap, air pillows, and padded mailers that are adaptable in form and used to cushion and protect items during transit. This type is widely used across various industries, including e-commerce, food, and pharmaceuticals, due to its lightweight and easy-to-use nature.

Foam protective packaging includes materials such as polyurethane and expanded polystyrene (EPS) foam that provide superior cushioning and shock absorption. It is commonly used to secure delicate electronic equipment, appliances, and other fragile goods that require extra care during storage or transport. The main driver for foam packaging is the need for enhanced protection of sensitive products, especially in the electronics and automotive industries.

Rigid protective packaging encompasses products such as corrugated boxes, molded pulp packaging, and protective cases that provide a strong, stable structure for transporting goods. This type is popular for shipping heavy or bulky items and offers better stacking capability compared to flexible and foam options. The growing logistics and transportation industry is a primary driver for rigid protective packaging.

Material Insights

Based on material, the paper & paperboard segment led the market with the largest revenue share of 45.7% in 2025 and is expected to grow at the fastest CAGR over the forecast period. This positive outlook is due to its eco-friendliness and biodegradability. They are particularly favored in industries that prioritize sustainability and want to reduce their carbon footprint. Paper-based packaging is known for its shock absorption capabilities and ease of recyclability. The rise in environmental awareness and consumer preference for sustainable packaging options drive the demand for paper-based protective packaging.

Plastics play a significant role in the global protective packaging market due to their lightweight, versatile, and durable nature. They are widely used for various applications such as air pillows, bubble wraps, and foam sheets. Their resistance to moisture and impact makes them an ideal choice for transporting delicate electronics and perishable goods.

Plastic foams, such as expanded polystyrene (EPS) and polyurethane foam, are known for their exceptional shock absorption and insulation properties. They are used in protective packaging for delicate items such as electronics, appliances, and other high-value products. These foams can be easily molded to fit specific shapes, ensuring tailored protection for items.

Function Insights

Based on function, the wrapping segment led the market with the largest revenue share of 29.3% in 2025. Wrapping involves using materials that are wrapped directly around items to protect them from external elements such as dust, moisture, and physical damage. Popular wrapping materials include bubble wrap, plastic films, and foam sheets. This type of protective packaging is commonly used for fragile or irregularly shaped items that need extra care during handling.

Void fill packaging refers to materials used to fill empty spaces within a package to prevent the movement of the product during transit. This type of packaging ensures that items remain secure, avoiding potential damage caused by shifting. Void fill solutions include packing peanuts, air pillows, and crumpled paper. These materials are lightweight, which helps minimize shipping costs while providing effective protection for items.

End Use Insights

Based on end use, the food & beverage segment led the market with the largest revenue share of 24.3% in 2025. The primary drivers for protective packaging in food & beverage include increased consumer demand for packaged and processed foods, the growth of e-commerce for grocery delivery, and the need for strict food safety regulations.

Protective packaging for industrial goods is essential to safeguard products during transportation and handling, especially those that are bulky or delicate in nature. This includes machinery parts, tools, and components that require sturdy materials such as molded foam, rigid plastics, and corrugated containers. The expansion of global trade and the rise of manufacturing activities in emerging economies are significant drivers. Additionally, the need for cost-effective logistics solutions and damage prevention measures encourages the use of robust protective packaging in the industrial sector.

Consumer electronics such as smartphones, laptops, and household gadgets are highly susceptible to damage from shocks, vibrations, and static electricity. Protective packaging for this end use segment typically involves anti-static materials, air cushions, molded pulp, and foam inserts that offer high protection levels.

Region Insights

Asia Pacific dominated the protective packaging market with the largest revenue share of 43.5% in 2025. The Asia Pacific region dominated the market space due to its robust manufacturing sector and explosive growth in e-commerce. Countries such as China, India, Japan, and South Korea have become major manufacturing hubs for electronics, automotive components, and consumer goods. For instance, companies such as Foxconn in China, which manufactures for Apple and other tech giants, require extensive protective packaging solutions to ensure safe transportation of sensitive electronic components both within their supply chain and to end consumers.

China Protective Packaging Market Trends

The protective packaging market in the China held the largest share in the Asia Pacific region in 2025. Protective packaging market in China is growing due to exponential growth of country’s e-commerce market, led by giants such as Alibaba and JD.com. With over 800 million digital consumers, Chinese e-commerce platforms handle billions of packages annually, necessitating reliable protective packaging to ensure products reach consumers safely. Besides, the country's strict quality control requirements, especially for export products, have led to increased demand for high-performance protective materials such as bubble wrap, foam packaging, and molded pulp solutions.

Europe Protective Packaging Market Trends

The presence of high-value manufacturing industries, such as automotive, electronics, and pharmaceuticals, particularly in countries like Germany, Switzerland, and Sweden, further drives the protective packaging market in the region. These sectors require sophisticated packaging solutions to protect sensitive components during transport and storage.

The protective packaging market in the Germany is primarily driven by its robust manufacturing and industrial base, particularly in sectors such as automotive, machinery, electronics, and precision instrument, drives significant demand for protective packaging. Companies such as BMW, Siemens, and Bosch require specialized packaging solutions to safely transport sensitive components and finished products. For example, German automotive manufacturers often use custom-designed foam inserts, anti-static bags, and shock-absorbing materials to protect electronic components and delicate car parts during shipping.

North America Protective Packaging Market Trends

The North American protective packaging market dominance can be primarily attributed to the explosive growth of e-commerce. Major players such as Amazon, Walmart, and Target have significantly expanded their online presence, necessitating robust protective packaging solutions to ensure products reach consumers safely. The region's advanced logistics infrastructure and high consumer expectations for damage-free deliveries have pushed companies to invest in innovative protective packaging, thus positively benefiting the market in the region.

Protective packaging market in the U.S. is primarily driven by its robust manufacturing sector, particularly in sensitive industries such as electronics, medical devices, and automotive parts. For example, companies such as Apple, Medtronic, and Ford require specialized protective packaging for shipping delicate components between facilities and to end users. The aerospace industry, with players such as Boeing and Lockheed Martin, also drives demand for high-performance protective packaging solutions that can safeguard costly and sensitive equipment during transport and storage.

Key Protective Packaging Company Insights

The protective packaging market is characterized by a highly competitive environment driven by key players and numerous regional and global manufacturers. Companies are competing based on product innovation, quality, sustainability, and cost-effectiveness to cater to various industries such as e-commerce, food and beverage, electronics, and healthcare. Technological advancements, including the use of eco-friendly and recyclable materials, are becoming essential differentiators as consumer and regulatory emphasis on sustainability increases. The market also sees strategic mergers, acquisitions, and collaborations to strengthen market positions and expand geographic reach.

-

In May 2025, Pregis LLC expanded its EasyPack on-demand paper packaging portfolio by introducing the white version of GeoTerra paper, a curbside-recyclable, paper-based wrapping solution that provides light cushioning and interleaving protection for products. The new white GeoTerra offers a sleek, premium alternative to the original kraft option, aligning with minimalist design trends favored by high-end beauty, wellness, and lifestyle brands. This addition allows brands to elevate their packaging presentation while maintaining eco-friendly and protective qualities.

-

In January 2024, Reedbut Group, a UK-based designer and manufacturer of bespoke cardboard packaging, launched a new range of universal protective packaging solutions to enhance the safety of refurbished tech items during transit. The new packaging eliminates the need for single-use materials such as plastic foam or polystyrene inserts, opting instead for entirely recyclable cardboard solutions.

Key Protective Packaging Companies

The following key companies have been profiled for this study on the protective packaging market.

-

Sealed Air

-

Sonoco Products Company

-

Smurfit Kappa

-

WestRock Company

-

Huhtamaki

-

DS Smith

-

Pregis LLC

-

Pro-Pac Packaging Limited

-

Dow

-

Intertape Polymer Group (IPG)

-

Storopack Hans Reichenecker Gmbh

-

International Paper Company

-

EcoEnclose

-

Point Five Packaging

-

Universal Protective Packaging, Inc.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Sealed Air; Sonoco Products Company; Smurfit Kappa; WestRock Company; Huhtamaki; DS Smith; Pregis LLC; Dow; Intertape Polymer Group (IPG); Storopack Hans Reichenecker GmbH; International Paper Company)

- Focus on large-scale manufacturing, integrated supply chains, and long-term contracts with e-commerce, electronics, healthcare, food & beverage, and industrial customers.

- Invest in automation, sustainable packaging innovations, and global distribution networks to improve operational efficiency and strengthen market presence.

- Extensive product portfolios covering foam, paper-based, air-cushion, corrugated, and customized protective packaging solutions across multiple end-use industries.

- Strong financial resources, global manufacturing footprints, and established customer relationships enable economies of scale and continuous product innovation.

- Large organizational structures can reduce operational flexibility and slow response to rapidly changing customer requirements.

- High dependence on raw material prices, regulatory compliance costs, and global supply chain stability can affect profitability.

Emerging Players (Pro-Pac Packaging Limited; EcoEnclose; Point Five Packaging; Universal Protective Packaging, Inc.)

- Focus on niche applications, customized packaging solutions, and sustainable product offerings to address specific customer requirements.

- Expand through regional market penetration, direct customer engagement, and flexible manufacturing capabilities.

- Greater agility in responding to changing market trends and customer demands, particularly in eco-friendly and specialized protective packaging segments.

- Ability to offer personalized service, shorter decision-making processes, and tailored packaging designs for small and medium-sized customers.

- Limited financial resources and production capacities compared to established global competitors.

- Lower brand recognition, narrower distribution networks, and reduced bargaining power with suppliers may restrict market expansion opportunities.

Protective Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 40.4 billion

Estimated market size in 2026

USD 41.5 billion

Projected market size by 2033

USD 57.0 billion

Growth rate

CAGR of 4.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, material, function, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Sealed Air; Sonoco Products Company; Smurfit Kappa; WestRock Company; Huhtamaki; DS Smith; Pregis LLC; Pro-Pac Packaging Limited; Dow; Intertape Polymer Group (IPG); Storopack Hans Reichenecker GmbH; International Paper Company; EcoEnclose; Point Five Packaging; Universal Protective Packaging, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Protective Packaging Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global protective packaging market report based on type, material, function, end use, and region:

-

Type Outlook (Revenue, USD Billion; Volume, Million Tons, 2021 - 2033)

-

Flexible

-

Foam

-

Rigid

-

-

Material Outlook (Revenue, USD Billion; Volume, Million Tons, 2021 - 2033)

-

Paper & Paperboard

-

Plastic

-

Plastic Foams

-

Others

-

-

Function Outlook (Revenue, USD Billion; Volume, Million Tons, 2021 - 2033)

-

Void Fill

-

Wrapping

-

Insulation

-

Blocking & Bracing

-

Cushioning

-

-

End Use Outlook (Revenue, USD Billion; Volume, Million Tons, 2021 - 2033)

-

Food & Beverage

-

Industrial Goods

-

Consumer Electronics

-

Household Appliances

-

Healthcare

-

Automotive

-

Others

-

-

Region Outlook (Revenue, USD Billion; Volume, Million Tons, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

Southeast Asia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Type

Revenue capture definition

Flexible

Revenue generated from the sale of flexible protective packaging solutions designed to provide lightweight product protection, shock absorption, and space-efficient transportation. This segment includes bubble wraps, air pillows, protective mailers, and flexible cushioning materials used across e-commerce, consumer goods, electronics, and healthcare applications.

Foam

Revenue generated from the sale of foam-based protective packaging solutions used to safeguard products against impact, vibration, and handling damage. This segment includes polyethylene foam, polyurethane foam, expanded polystyrene (EPS), and custom foam inserts utilized in electronics, automotive, industrial, and medical product packaging.

Rigid

Revenue generated from the sale of rigid protective packaging products designed to provide structural strength and enhanced product security during storage and transit. This segment includes molded pulp packaging, protective trays, clamshells, corrugated structures, and rigid containers used for fragile and high-value products.

Segment - Material

Revenue capture definition

Paper & Paperboard

Revenue generated from the sale of paper-based protective packaging materials developed to provide cushioning, wrapping, and void-fill functions while supporting sustainability objectives. This segment includes corrugated paper, kraft paper, molded pulp, and paper cushioning solutions used across various end-use industries.

Plastic

Revenue generated from the sale of plastic protective packaging materials designed to deliver durability, moisture resistance, and effective product protection. This segment includes polyethylene films, air cushions, bubble wraps, and protective mailers used in logistics, retail, and industrial packaging applications.

Plastic Foams

Revenue generated from the sale of plastic foam materials used for impact protection, thermal insulation, and vibration control. This segment includes expanded polystyrene (EPS), expanded polyethylene (EPE), and polyurethane foams utilized in electronics, healthcare, automotive, and industrial packaging applications.

Paper & Paperboard

Revenue generated from the sale of paper-based protective packaging materials developed to provide cushioning, wrapping, and void-fill functions while supporting sustainability objectives. This segment includes corrugated paper, kraft paper, molded pulp, and paper cushioning solutions used across various end-use industries.

Others

Revenue generated from the sale of protective packaging materials not classified under paper, plastic, or plastic foams. This segment includes textile-based protective materials, biodegradable polymers, wood wool, natural fiber packaging, and other specialty materials used in niche applications.

Segment - Function

Revenue capture definition

Void Fill

Revenue generated from the sale of protective packaging solutions used to fill empty spaces within shipping containers and prevent product movement during transit. This segment includes paper fillers, air pillows, foam peanuts, and inflatable packaging products.

Wrapping

Revenue generated from the sale of protective packaging materials designed to wrap and shield products from scratches, dust, moisture, and minor impacts. This segment includes bubble wraps, protective films, foam sheets, and paper wrapping solutions.

Insulation

Revenue generated from the sale of insulated protective packaging solutions used to maintain temperature stability and protect temperature-sensitive products. This segment includes thermal liners, insulated containers, and cold-chain packaging materials used in food, beverage, and healthcare applications.

Blocking & Bracing

Revenue generated from the sale of packaging solutions designed to secure products within shipping containers and prevent shifting during transportation. This segment includes corrugated inserts, foam supports, edge protectors, and customized bracing systems.

Cushioning

Revenue generated from the sale of protective packaging solutions designed to absorb shocks and vibrations during handling and transit. This segment includes foam inserts, air cushions, molded pulp packaging, and other impact-resistant materials used across various industries.

Segment - End Use

Revenue capture definition

Food & Beverage

Revenue generated from the sale of protective packaging solutions used to protect food and beverage products from damage, contamination, and temperature fluctuations during storage and distribution.

Industrial Goods

Revenue generated from the sale of protective packaging products used for transporting and storing machinery, equipment, components, tools, and other industrial products requiring impact and vibration protection.

Consumer Electronics

Revenue generated from the sale of protective packaging solutions designed for electronic devices and components. This segment includes cushioning, anti-static packaging, foam inserts, and protective trays used for smartphones, computers, and consumer electronic products.

Household Appliances

Revenue generated from the sale of protective packaging materials used to safeguard household appliances during shipping, warehousing, and retail distribution. This segment includes foam packaging, corrugated inserts, and protective wraps for large and small appliances.

Healthcare

Revenue generated from the sale of protective packaging solutions used for pharmaceuticals, medical devices, diagnostic equipment, and healthcare products requiring secure handling and protection from physical damage or environmental factors.

Automotive

Revenue generated from the sale of protective packaging products used to transport automotive parts, components, and assemblies. This segment includes custom foam inserts, protective trays, dunnage solutions, and impact-resistant packaging materials.

Others

retail generated from the sale of protective packaging solutions used in additional end-use industries such as aerospace, personal care, chemicals, retail, and logistics applications that require product protection during storage and transportation.

Estimation Model

Layer Name

Key Question

Description

Product Shipment Layer

Which products require protective packaging?

Analyze shipment volumes of products requiring protection during storage and transportation.

Protective Packaging Adoption Layer

Which shipments use protective packaging?

Apply adoption rates of cushioning, void-fill, wrapping, insulation, and blocking & bracing solutions across end-use industries.

Packaging Consumption Layer

How much protective packaging is consumed?

Estimate packaging demand based on shipment volumes, product fragility, packaging requirements, and material usage per shipment.

Revenue Generation Layer

How much revenue is generated?

Multiply packaging volumes by average selling prices (ASP) across packaging types, materials, functions, end-use industries, and regions to calculate market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Description

Regional Segmentation Analysis

Provided detailed market size, growth forecasts, demand patterns, healthcare expenditure trends, diagnostic testing volumes, and regulatory landscape analysis across North America, Europe, Asia Pacific, Central & South America, and Middle East & Africa, including key country-level insights for In Vitro Diagnostic (IVD) Packaging demand and adoption.

Enabled identification of high-growth healthcare markets, emerging diagnostic testing hubs, regulatory opportunities, and region-specific expansion strategies to support investment and market entry decisions.

Analyze shipment volumes of products requiring protection during storage and transportation.

Cross-Segmentation Assessment

Delivered customized market analysis across Product Type (Bottles & Vials, Tubes, Petri Dishes, Labels & Stickers, Other Products), Application (Hospitals, Laboratories, Academic Institutes, Other Applications), and Region to highlight demand dynamics, adoption trends, and growth opportunities across the IVD packaging value chain.

Supported targeted product positioning, customer-focused strategy development, identification of high-growth application segments, and portfolio optimization initiatives.

Apply adoption rates of cushioning, void-fill, wrapping, insulation, and blocking & bracing solutions across end-use industries.

Competitive Benchmarking

Conducted benchmarking of key IVD packaging manufacturers based on product portfolios, packaging innovation, regulatory compliance capabilities, healthcare packaging expertise, manufacturing footprint, customer base, and strategic developments.

Helped clients assess competitive positioning, identify differentiation opportunities, understand industry best practices, and evaluate strategic partnerships and acquisition opportunities within the IVD packaging ecosystem.

Estimate packaging demand based on shipment volumes, product fragility, packaging requirements, and material usage per shipment.

Frequently Asked Questions About This Report

Asia Pacific dominated the protective packaging market with a share of over 43.5% in 2024. This is attributable to increasing consumer spending, continuous technological advancements, and improvements in manufacturing activities in the region.

Some key players operating in the protective packaging market include Sealed Air, Sonoco Products Company, Smurfit WestRock, Huhtamaki, DS Smith, Pregis LLC, Pro-Pac Packaging Limited, Dow Chemical Company, and Intertape Polymer Group (IPG)

The protective packaging market is driven by the booming e-commerce industry and increasing demand for damage-free product transportation. Additionally, rising consumer awareness toward sustainable and eco-friendly packaging solutions is propelling market growth.

The global protective packaging market is expected to grow at a CAGR of 4.6% from 2026 to 2033, reaching USD 57.0 billion by 2033.

Based on end use, the food & beverage segment led the market with the largest revenue share of 24.3% in 2025.

The flexible segment led the market with a 66.4% revenue share in 2025 and is the fastest-growing segment.

Paper & Paperboard segment held the largest revenue share in 2025 and is the fastest-growing segment.

Wrapping segment held the largest share in 2025, while void fill is the fastest-growing segment.

The global protective packaging market size was valued at USD 40.4 billion in 2025 and is estimated at USD 41.5 billion for 2026.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.