- Home

- »

- HVAC & Construction

- »

-

Reach Stacker Market Size And Share Report, 2026-2033GVR Report cover

![Reach Stacker Market (2026 - 2033)Report]()

Reach Stacker Market (2026 - 2033)

Size, Share & Trends Analysis Report By Tonnage (Less Than 30 Ton, 30 To 45 Ton), By Powertrain Type (Electric, Hybrid), By Application (Yards/Landside, Industrial), By Region, And Segment Forecasts

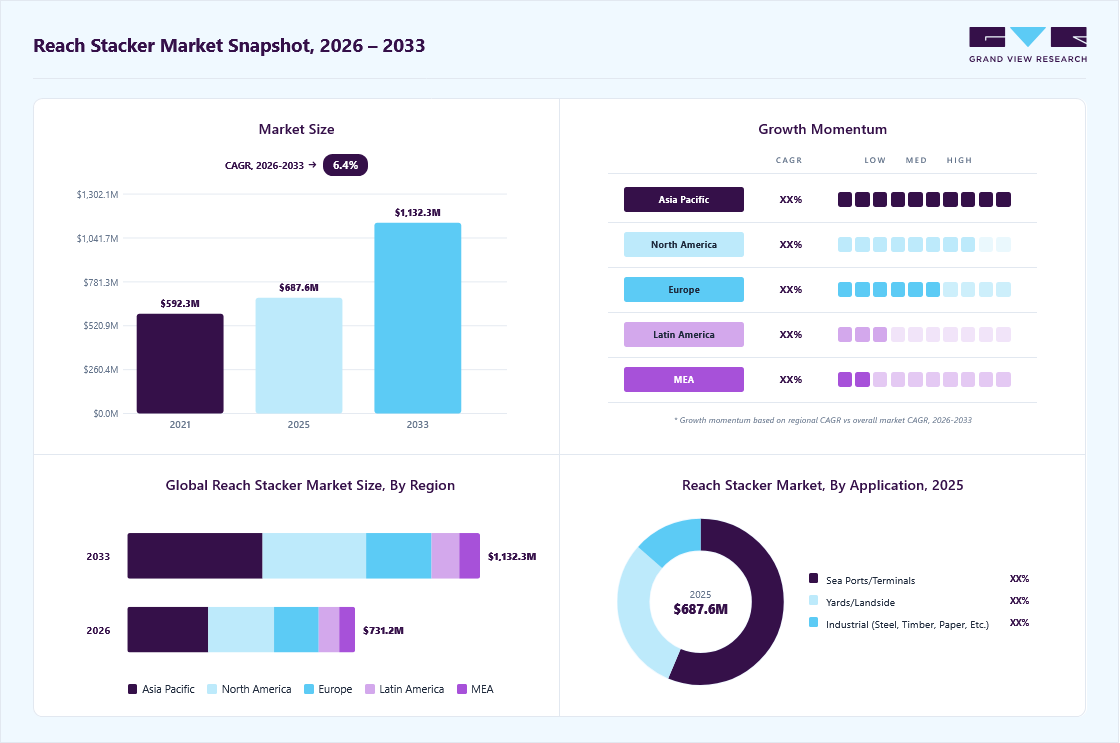

Market Size, 2025

$687.6MMarket Estimate, 2026

$731.2MMarket Forecast, 2033

$1,132.2MCAGR, 2026–2033

6.4%Reach Stacker Market Summary

The global reach stacker market size was valued at USD 687.6 million in 2025 and is projected to grow from USD 731.2 million in 2026 to USD 1132.2 million by 2033, at a CAGR of 6.4% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 35.1% in 2025. Expansion of global port and container-handling operations is significantly driving market growth.

Key Market Trends & Insights

- By tonnage: Less than 30 tons (low) segment held the largest market share of 47.6% in 2025.

- By powertrain type: Internal-combustion engine segment held the largest market share in 2025.

- By application: Sea ports/terminals segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (35.1% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 687.6 Million

- Estimated market size in 2026: USD 731.2 Million

- Projected market size by 2033: USD 1132.2 Million

- CAGR (2026-2033): 6.4%

Rising international trade and containerized cargo movement are increasing demand for efficient reach stackers across ports, terminals, and logistics hubs to improve cargo handling speed, operational flexibility, and productivity. The market growth can be attributed to the rapid expansion of intermodal transportation and rail freight networks worldwide. The growing movement of containerized cargo between ports, rail terminals, inland depots, and logistics hubs is driving significant demand for efficient reach stackers that improve cargo transfer speed, handling efficiency, and operational flexibility. As global supply chains become more interconnected, reach stackers are increasingly being adopted to support seamless cargo movement across multiple transportation modes.")

Technological advancements in reach stackers are improving efficiency and sustainability in port and logistics operations. Manufacturers are adopting automation, telematics, GPS tracking, real-time monitoring, and intelligent fleet management to improve performance and reduce downtime. In addition, the introduction of electric reach stackers is also lowering fuel consumption and emissions, thereby supporting global sustainability goals. Various companies have launched technologically advanced electric reach stackers to improve operational efficiency and energy efficiency in container-handling applications. For instance, in August 2025, SANY Group launched the 50-tonne energy storage reach stacker for container handling. This model features advanced electric control pump technology, high-pressure hydraulic systems, and energy recovery systems with over 65% recovery efficiency. It is equipped with a 512kWh swappable battery system that supports fast charging and battery swapping, allowing more than seven hours of continuous operation and minimizing downtime.

The market is expanding significantly as companies introduce advanced equipment to meet the demand for efficient and sustainable cargo handling. Manufacturers are expanding their portfolios with electric reach stackers equipped with intelligent control systems and energy-efficient powertrains to improve operational productivity and reduce emissions. For instance, in November 2025, Konecranes expanded its lift truck portfolio by launching a new electric reach stacker for high-intensity operations. This model delivers up to 16 hours of performance on a single charge and features advanced electric powertrain technology and intelligent controls. It also uses Konecranes’ TRUCONNECT technology to collect real-time operational data. Such expansions are strengthening the development of technologically advanced and sustainable reach stacker solutions.

The regulatory landscape plays a crucial role in shaping the market by establishing strict safety and operational standards used across ports, terminals, and logistics facilities. Various regions have implemented regulations and workplace safety standards to protect operators, reduce operational risks, and ensure safe cargo handling. For instance, the Occupational Safety and Health Administration’s (OSHA) Material Handling Equipment Regulations require proper operator training, regular equipment inspections, safe load-handling practices, and maintenance procedures to minimize workplace accidents and improve operational safety. These regulations are encouraging the adoption of advanced reach stackers equipped with enhanced safety and operational control systems.

The market faces challenges. One of the major challenges is high maintenance and repair costs, as these machines rely on complex hydraulic systems, lifting mechanisms, and high-capacity tires that require regular maintenance and replacement. Insufficient maintenance can lead to increased downtime and costly repairs. In addition, reach stackers require stable, level ground for safe, efficient operation; poor surface conditions can compromise stability and performance. Their large size also makes maneuvering difficult in congested ports and container yards, potentially causing delays, reduced productivity, and increased safety risks during cargo handling.

Market Dynamics

The rapid growth of global e-commerce is increasing demand for reach stackers, as more containerized goods move through logistics networks. Higher online retail penetration has raised import and export volumes, putting additional pressure on ports, container yards, and inland logistics hubs to process cargo efficiently. Furthermore, reach stackers are essential for fast stacking, unloading, and container movement, thereby improving operational speed and reducing turnaround times in high-volume environments.

The growth of large-scale warehousing and distribution centers for e-commerce fulfillment is also driving market expansion. Companies such as Amazon Inc., DHL Group, and FedEx Corporation continue to expand their logistics network to manage higher order volumes and speed up deliveries. For instance, in May 2026, Amazon launched its Amazon Supply Chain Services (ASCS) initiative, expanding its logistics and warehousing network to support external businesses across retail, manufacturing, and healthcare sectors. This has increased demand for efficient reach stackers that can move containerized goods between ports, warehouses, and distribution hubs. Thus, reach stackers are being adopted to emphasize productivity, optimize space, and cargo handling across global supply chains.

Limited visibility during reach stacker operations represents a significant challenge in the market, primarily impacting operational safety and efficiency. Due to their large structural design and height, reach stackers often restrict the operator’s field of vision, which makes it difficult to clearly observe surrounding equipment and containers. In busy environments such as ports and logistics terminals, this visibility constraint increases the likelihood of collisions, operational errors, and damage to both cargo and machinery.

Although technological advancements such as integrated camera systems and sensor-based monitoring solutions have improved situational awareness, the risk of human error still persists. Operators with insufficient training or experience may struggle to manage restricted visibility conditions effectively, further increasing safety risks. Thus, continuous operator training, along with the adoption of advanced visibility-enhancement technologies, is essential to reduce accidents and ensure safe reach stacker operations.

The increasing modernization and expansion of ports and cargo terminals worldwide present a significant opportunity for the market. Governments and port authorities are investing heavily in upgrading port infrastructure to accommodate rising international trade volumes and increased cargo-handling requirements. For instance, the Port of Long Beach in the U.S. is investing USD 1.8 billion in the Pier B On-Dock Rail Support Facility to expand rail capacity and improve cargo movement efficiency across port operations. Such projects are increasing the deployment of advanced reach stackers to support faster container handling, improved operational efficiency, and reduced cargo turnaround time across modern port terminals.

In addition, the integration of smart technologies is further creating growth opportunities for advanced reach stackers. Upgraded terminals increasingly require equipment with higher lifting capacities, improved maneuverability, and enhanced operational precision to support faster and more efficient cargo movement. As global ports continue to focus on infrastructure modernization and operational optimization, the adoption of technologically advanced reach stackers is expected to increase steadily across major logistics and trade hubs.

Market Concentration & Characteristics

The reach stacker industry is moderately concentrated, with established European and American manufacturers competing against rapidly growing Chinese companies that leverage cost advantages and robust domestic manufacturing. Competition remains balanced among major regional players. Companies such as Kalmar Corporation, Konecranes, and Hyster-Yale hold strong positions in advanced and premium port equipment, while Chinese manufacturers such as SANY Group and Shanghai Zhenhua Heavy Industries Company Limited (ZPMC) are expanding globally through competitive pricing and diverse product offerings.

The market is further characterized by technological advancements in automation, electrification, fuel efficiency, and smart fleet management to improve productivity at ports, terminals, rail yards, and logistics hubs. Increased investment in port modernization and expansion of intermodal networks, along with rising global containerized cargo volumes, are supporting steady growth. Thus, manufacturers are developing electric and hybrid reach stackers, advanced safety systems, and automation-ready equipment to remain competitive and meet evolving customer needs in global cargo handling.

Tonnage Insights

The less than 30 ton (low) segment accounted for the largest share of 47.64% in 2025. The segment growth is driven by high demand for compact maneuverability, as these machines are widely used in narrow container yards, urban logistics hubs, and small-scale construction sites where operational space is limited and flexible handling is essential. In addition, cost efficiency further supports growth, as low-tonnage reach stackers require lower initial investment, reduced fuel or energy consumption, and lower maintenance costs, thereby making them highly suitable for rental fleets and small- to mid-sized logistics operators.

The 30 to 45 ton (medium) segment is expected to grow at the fastest CAGR during the forecast period. The demand for high-capacity handling is driving the segment growth, as rising container volumes require equipment capable of efficiently managing heavier loads and improving turnaround times at ports and intermodal terminals. In addition, infrastructure modernization is further accelerating adoption, as logistics operators are increasingly upgrading to advanced, versatile reach stackers that balance lifting strength with operational efficiency, thus making them suitable for high-intensity cargo-handling environments.

Powertrain Type Insights

The internal-combustion engine segment held the largest market share in 2025. The ICE’s high durability is driving demand, as these reach stackers can sustain continuous, high-intensity cargo-handling operations in ports, terminals, and industrial facilities with minimal operational interruptions, which makes them suitable for demanding working environments. In addition, the lower upfront cost and strong availability of fuel-based servicing networks are further supporting adoption, as they make internal-combustion models more economical and easier to maintain, especially in regions where diesel infrastructure and maintenance support are already widely established.

The electric segment is expected to grow at a significant CAGR during the forecast period. The segment growth is supported by advancements in battery and charging technology and by rising operational efficiency, with lower energy consumption. The advancement in battery and charging systems is driving adoption as modern lithium-ion batteries and energy recovery systems are improving uptime and enabling longer operational cycles, thus making electric reach stackers more suitable for intensive cargo-handling applications. In addition, improved energy efficiency is further accelerating demand, as electric models reduce fuel dependency and lower operating costs, thus making them increasingly preferred across modern ports and logistics facilities.

Application Insights

The sea ports/terminals segment dominated the market in 2025. The segment growth is attributed to high container throughput and centralized operations, as major ports handle large volumes of international trade, requiring efficient, high-capacity reach stackers to ensure smooth loading, unloading, and stacking of containers. In addition, ongoing modernization of port infrastructure and adoption of advanced cargo-handling systems are further strengthening demand, as terminals increasingly deploy technologically advanced reach stackers to improve turnaround time, operational efficiency, and overall port productivity.

The yards/landside segment is projected to grow at a substantial CAGR over the forecast period. The expansion of inland logistics and warehousing is driving this segment as growing distribution networks require efficient material-handling equipment for container movement outside traditional port environments. In addition, the growing need for flexible, cost-efficient container handling in rail yards, freight stations, and inland depots is further driving adoption, as operators seek versatile reach stackers to efficiently manage storage and short-distance container transportation.

Regional Insights

The Asia Pacific reach stacker market dominated the global market and accounted for a share of 35.12% in 2025. The region’s growth is attributed to rising port modernization and expansion in major economies such as Japan, Australia, China, and India. Governments and port authorities are prioritizing improved cargo-handling efficiency and logistics operations, which is increasing demand for advanced reach stackers for container and material handling. In addition, rising containerized trade volumes in developing economies are creating a greater need for high-productivity cargo-handling equipment to support efficient container movement at ports, freight terminals, and logistics hubs.

China Reach Stacker Market Trends

The reach stacker market in China held a dominant position in 2025. The country’s growth is supported by rising investments in infrastructure development and logistics expansion activities. For instance, according to the China Belt and Road Initiative (BRI) Investment Report 2025, China continues to invest heavily in transportation and logistics infrastructure, including roads, rail, shipping, and aviation networks, to strengthen global trade connectivity. Such large-scale infrastructure and logistics developments are significantly increasing container trade and freight movement activities, thereby driving demand for advanced reach stackers across ports and logistics terminals.

India reach stacker market is expected to grow rapidly in the forecast years. The adoption of reach stackers in the country is closely tied to government infrastructure and logistics initiatives. For instance, the Ministry of Ports, Shipping and Waterways (MoPSW) launched the Sagarmala Program, now Sagarmala 2.0 (2012-2035), to advance India’s long-term economic growth and its goal of becoming a multi-trillion-dollar economy by 2047. With over 845 projects valued at approximately USD 73 billion underway or planned as of April 2026, the program is expanding port capacity, improving logistics connectivity, and increasing cargo-handling efficiency. These developments are driving demand for advanced reach stackers in port and terminal operations.

North America Reach Stacker Market Trends

The reach stacker market in North America is anticipated to grow at a substantial CAGR during the forecast period. The region’s growth is driven by the presence of well-established port infrastructure and the increasing adoption of technologically advanced reach stackers across cargo-handling operations. Major ports across the U.S. and Canada, such as the Port of Los Angeles, the Port of Long Beach, and the Port of Vancouver, are increasingly modernizing cargo-handling operations with advanced and high-capacity material-handling equipment to improve operational efficiency and reduce turnaround time. In addition, the growing adoption of technologically advanced and electric reach stackers across logistics facilities is further supporting market growth in the region.

The U.S. reach stacker market held a substantial market share in 2025. The Rapid growth in e-commerce and rail freight is driving demand for efficient container-handling equipment, including reach stackers at logistics hubs and distribution centers. Increased investment in port expansion and smart cargo-handling infrastructure is prompting operators to adopt advanced reach stackers to enhance productivity and cargo movement. For instance, in April 2026, the U.S. Department of Transportation announced an investment of approximately USD 774 million through the Maritime Administration (MARAD) to upgrade 37 port infrastructure projects nationwide, further supporting advanced cargo-handling equipment and port modernization.

Europe Reach Stacker Market Trends

The reach stacker market in Europe was identified as a lucrative region in 2025. The strong presence of advanced logistics networks and high container throughput at major ports is significantly supporting the demand for efficient reach stackers in the region. In addition, the growing emphasis on automation and digitalization in cargo-handling operations is further enhancing the adoption of technologically advanced equipment to improve productivity and operational efficiency.

The UK reach stacker market is expected to grow rapidly in the coming years. The rising focus on improving supply chain efficiency and reducing cargo handling time is encouraging the adoption of advanced reach stackers across terminals and freight facilities in the country. In addition, the growing shift toward high-performance material-handling equipment is further supporting market expansion.

The reach stacker market in Germany held a substantial market share in 2025. The increasing demand for efficient cargo movement across rail yards and warehouses, as well as in export- and import-oriented industries, is driving the adoption of high-capacity reach stackers. In addition, the emphasis on operational efficiency and advanced engineering standards in material-handling equipment is further strengthening the growth of reach stackers in the country.

Key Reach Stacker Company Insights

Some of the key companies in the market include Kalmar Corporation, Konecranes, Hyster-Yale Group, and others. Organizations are focusing on increasing their customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Kalmar Corporation is a Finland-based company specializing in cargo and material-handling solutions for ports, terminals, distribution centers, and the heavy logistics industry. The company offers a broad portfolio of equipment, including reach stackers, terminal tractors, forklift trucks, empty container handlers, and automation solutions designed to improve operational efficiency and sustainability in container handling operations. Kalmar has a strong global operational presence across Europe, Asia Pacific, North America, and the Middle East, supported by extensive manufacturing facilities and service networks.

-

Konecranes is a manufacturer of material-handling equipment and offers lifting and cargo-handling solutions for ports, terminals, manufacturing facilities, and the global logistics industry. Its portfolio includes reach stackers, lift trucks, container handling equipment, industrial cranes, and automated port solutions that improve productivity and safety. Konecranes operates in over 50 countries and serves a diverse customer base across container handling, automotive, mining, energy, and industrial sectors. The company prioritizes innovation and sustainability by developing intelligent, automated, and electric equipment, including advanced reach stacker solutions for modern logistics and intermodal operations.

Key Reach Stacker Companies:

The following key companies have been profiled for this study on the reach stackers market.

- Kalmar Corporation

- Konecranes

- Hyster-Yale Group

- Liebherr Group

- SANY Group

- CVS Ferrari S.p.A.

- Terex Corporation

- Taylor Machine Works, Inc.

- Hoist Material Handling, Inc.

- Toyota Material Handling

Recent Developments

-

In March 2026, DP World introduced Chile’s first fully electric reach stacker at its multipurpose terminal at Lirquén Port. The company deployed the electric SANY SRSC45E3 reach stacker to support sustainable, low-emission cargo-handling operations. The introduction of the electric reach stacker was expected to eliminate approximately 60,000 liters of diesel consumption annually, equivalent to reducing nearly 160,000 kilograms of CO₂ emissions.

-

In November 2025, Konecranes expanded its lift truck portfolio with the launch of a new electric reach stacker designed for high-intensity material-handling operations. The electric reach stacker delivers up to 16 hours of performance on a single charge, addressing the growing demand for eco-efficient cargo-handling solutions. The product was introduced in Shanghai, China, and was made available across Asia-Pacific, the Middle East & Africa, and South America, with further expansion into Europe and North America planned for the following year.

Reach Stacker Market Report Scope

Report Attribute

Details

Market size in 2025

USD 687.6 million

Estimated market size in 2026

USD 731.2 million

Projected market size by 2033

USD 1,132.2 million

Growth rate

CAGR of 6.4% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Tonnage, powertrain type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Kalmar Corporation; Konecranes; Hyster-Yale Group; Liebherr Group; SANY Group; CVS Ferrari S.p.A.; Terex Corporation; Taylor Machine Works, Inc.; Hoist Material Handling, Inc.; Toyota Material Handling.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Reach Stacker Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global reach stacker market report based on tonnage, powertrain type, application, and region:

-

Tonnage Outlook (Revenue, USD Million, 2021 - 2033)

-

Less Than 30 Ton (Low)

-

30 to 45 Ton (Medium)

-

45 to 100 Ton (High)

-

More Than 100 Ton (Super-Heavy)

-

-

Powertrain Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Internal-Combustion Engine

-

Electric

-

Hybrid

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Sea Ports/Terminals

-

Yards/Landside

-

Industrial

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Reach Stacker Industry Opportunity Assessment

Country/region-wise market sizing and forecasts

Analysis of demand, adoption trends, and regulatory landscape

Identification of high-growth regions and investment hotspots

Identified region-specific growth opportunities

Supported expansion and go-to-market strategy

Enabled informed regional investment decisions

Cross-Segmentation Analysis for the Reach Stacker Industry

Criss-cross market analysis by tonnage, by powertrain type, by application

Demand and adoption assessment across key segments

Segment attractiveness and growth potential benchmarking

Identified high-potential market segments

Supported targeted product positioning and marketing strategy

Improved customer and segment prioritization

Competitive Benchmarking and Strategic Positioning in the Reach Stacker Industry

Benchmarking of key competitors across products, pricing, partnerships, and innovation

Comparative assessment of market share, capabilities, and strategies

Analysis of competitive strengths, gaps, and differentiation areas

Identified competitive white spaces and growth gaps

Supported strategic positioning and differentiation

Enabled data-driven competitive strategy development

Frequently Asked Questions About This Report

The global reach stacker market size was valued at USD 687.6 million in 2025 and is estimated at USD 731.2 million for 2026.

The less than 30 ton (low) segment accounted for the largest share of 47.6% in 2025. The segment growth is driven by high demand for compact maneuverability, as these machines are widely used in narrow container yards, urban logistics hubs, and small-scale construction sites where operational space is limited and flexible handling is essential.

Expansion of global port and container-handling operations is significantly driving the growth of the reach stacker market. Rising international trade and containerized cargo movement are increasing demand for efficient reach stackers across ports, terminals, and logistics hubs to improve cargo handling speed, operational flexibility, and productivity.

The global reach stacker market is expected to grow at a CAGR of 6.4% from 2026 to 2033, reaching USD 1,132.2 million by 2033.

Asia Pacific dominated with a 35.1% revenue share in 2025.

The internal-combustion engine segment held the largest revenue share in 2025.

The sea ports/terminals segment dominated the market and accounted for the largest share in 2025.

Key players include Kalmar Corporation; Konecranes; Hyster-Yale Group; Liebherr Group; SANY Group; CVS Ferrari S.p.A.; Terex Corporation; Taylor Machine Works, Inc.; Hoist Material Handling, Inc.; Toyota Material Handling.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.