- Home

- »

- Next Generation Technologies

- »

-

Remote Weapon Systems Market Size, Industry Report 2033GVR Report cover

![Remote Weapon Systems Market Size, Share & Trends Report]()

Remote Weapon Systems Market (2026 - 2033) Size, Share & Trends Analysis Report By Component (Sensors and EO/IR Suites), By Platform (Land-based, Naval-based, Airborne), By Weapon Type, By Technology, By Application, By Region, And Segment Forecasts

Market Size, 2025

$11.7BMarket Estimate, 2026

$12.7BMarket Forecast, 2033

$23.7BCAGR, 2026–2033

9.5%Remote Weapon Systems Market Summary

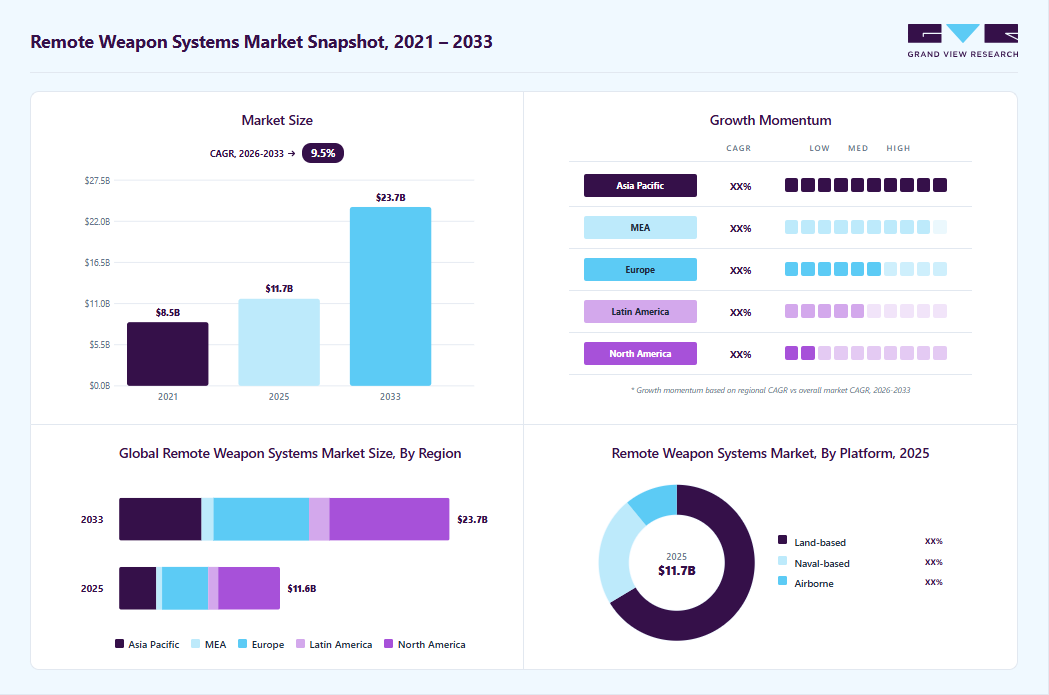

The global remote weapon systems market size was valued at USD 11.7 billion in 2025 and is projected to grow from USD 12.7 billion in 2026 to USD 23.7 billion by 2033, at a CAGR of 9.5% from 2026 to 2033. North America dominated the global remote weapon systems market with the largest revenue share of 38.4% in 2025.

Key Market Trends & Insights

- By component: the Sensors and EO/IR suites segment led the market with the largest revenue share of 27.2% in 2025.

- By platform: the Airborne segment is expected to grow at the fastest CAGR of 11.2% from 2026 to 2033.

- By application: Military & defense segment led the market with the largest revenue share of 92.3% in 2025.

Regional Highlights

- Largest regional market: North America (38.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 11.7 Billion

- Estimated market size in 2026: USD 12.7 Billion

- Projected market size by 2033: USD 23.7 Billion

- CAGR (2026-2033): 9.5%

Governments worldwide are prioritizing the modernization of armed forces, leading to increased procurement of advanced weapon systems that enhance operational effectiveness. This demand is particularly evident in regions facing security threats, where investment in remote and automated weapon platforms is seen as essential for maintaining tactical superiority and deterrence capabilities.

")

The shift toward modular, scalable systems that can support multiple weapon configurations and mission profiles is accelerating the market growth. Modern RWS are designed for flexibility, allowing integration of machine guns, cannons, missiles, and even non-lethal payloads. In addition, adoption is expanding beyond traditional military use to homeland security, border surveillance, and critical infrastructure protection. The rise of counter-drone warfare, software-driven upgrades, and service-based support models further highlights the evolution toward adaptable, future-ready weapon systems. These factors are expected to drive the remote weapon systems industry in the coming years.

In addition, modern military strategies focus on reducing human exposure in dangerous combat situations, making remote weapon systems an essential solution. These systems enable operators to control weapons remotely from protected locations, greatly decreasing casualties and enhancing survivability in urban combat and hostile environments. The growing need to counter threats such as improvised explosive devices (IEDs), ambushes, and close-quarters attacks has accelerated the adoption of remote weapon systems on land vehicles, naval ships, and fixed defense sites.

Furthermore, the proliferation of unmanned platforms, such as unmanned aerial vehicles (UAVs), ground vehicles (UGVs), and naval systems, is a major trend driving RWS integration. These platforms rely heavily on remote weapon stations for surveillance, target acquisition, and precision engagement. With defense forces shifting toward autonomous and network-centric warfare, RWS are becoming integral components of next-generation combat ecosystems, enabling remote operations with enhanced accuracy and efficiency.

Moreover, the growing advancements in artificial intelligence, sensor fusion, electro-optical/infrared (EO/IR) systems, and automated fire-control technologies are transforming RWS capabilities. AI-driven target recognition, real-time tracking, and ballistic computation significantly improve accuracy while reducing operator workload. Sensor systems, including thermal imaging and laser range finding, are emerging as key differentiators, enabling effective engagement across diverse operational conditions, such as low visibility and complex terrain, thereby fueling market innovation.

Component Insights

The sensors and EO/IR suites segment led the market with the largest revenue share of 27.2% in 2025 and is expected to grow at the fastest CAGR during the forecast period, driven by their central role in enabling real-time surveillance, target acquisition, and precision engagement across diverse combat environments. Advanced thermal imaging, laser range finding, and multispectral sensor fusion technologies significantly enhance situational awareness and operational accuracy, making them indispensable in modern network-centric warfare. In addition, increasing demand for day/night capabilities, border surveillance, and AI-enabled threat detection has further accelerated investments in high-performance sensor systems.

The fire-control and ballistic computers segment is expected to grow at a significant CAGR of 10% from 2026 to 2033, driven by rapid advancements in AI-powered targeting, automated tracking, and real-time ballistic computation. These systems are becoming critical for improving first-shot accuracy, reducing operator workload, and enabling semi-autonomous engagement in complex combat scenarios. Integration with advanced sensors and networked battlefield systems is further enhancing their importance in next-generation weapon platforms.

Platform Insights

The land-based segment accounted for the largest market revenue share in 2025, driven by widespread deployment across armored vehicles, infantry fighting systems, and stationary defense installations. Ongoing modernization programs, particularly the replacement of manually operated weapon mounts with stabilized remote systems, have significantly boosted adoption. These systems improve crew survivability, enable multi-role combat capabilities, and align with the broader shift toward digitized and network-enabled ground warfare. These factors are driving segmental growth.

The airborne segment is expected to grow at the fastest CAGR from 2026 to 2033, owing to the increasing integration of lightweight remote weapon systems into unmanned aerial vehicles (UAVs), helicopters, and advanced combat aircraft. Technological advancements in miniaturization, recoil management, and targeting systems are making airborne deployment more feasible and effective. The rising use of UAVs for surveillance and combat missions is further accelerating demand for compact, high-precision RWS solutions, thereby driving segmental growth.

Weapon Type Insights

The lethal segment accounted for the largest market revenue share in 2025, driven by strong demand for high-firepower weapon systems in active combat, counter-terrorism, and border defense operations. Military forces continue to prioritize systems capable of delivering precise and effective neutralization of threats, particularly in high-intensity conflict environments. The integration of medium- and large-caliber weapons with remote platforms has further strengthened the dominance of this segment.

The non-lethal segment is anticipated to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for applications in crowd control, peacekeeping, and critical infrastructure protection. Governments and security agencies are focusing on solutions that allow proportional response while minimizing collateral damage and complying with legal frameworks. The expansion of homeland security operations and the growing urban security challenges are also contributing to the adoption of non-lethal RWS solutions.

Application Insights

The military & defense segment accounted for the largest market revenue share in 2025, driven by rising global defense spending, ongoing modernization programs, and the need to enhance combat effectiveness and soldier safety. Armed forces worldwide are investing heavily in advanced weapon systems that integrate surveillance, targeting, and firepower capabilities into a single platform, reinforcing the dominance of this segment.

The homeland security segment is anticipated to grow at the fastest CAGR from 2026 to 2033, owing to increasing deployment of RWS in border security, surveillance, and critical infrastructure protection. Expanding threats such as illegal infiltration, terrorism, and smuggling are driving demand for remote and automated weapon systems among law enforcement and security agencies. In addition, the need for non-lethal, scalable solutions is further driving growth in this segment.

Technology Insights

The remote-controlled segment accounted for the largest market revenue share in 2025, driven by its operational maturity, reliability, and widespread deployment across land and naval platforms. These systems provide enhanced force protection by allowing operators to engage targets from protected positions, reducing exposure to battlefield threats. Their compatibility with existing military infrastructure and ease of integration have further reinforced their dominance.

The autonomous segment is anticipated to grow at the fastest CAGR during the forecast period, owing to the increasing adoption of AI-driven technologies, automated target recognition, and the broader shift toward unmanned and network-centric warfare. Advances in sensor fusion and machine learning are enabling systems to operate with minimal human intervention, improving response times and operational efficiency. This trend is aligned with the growing deployment of autonomous ground and aerial combat platforms.

Regional Insights

North America dominated the global remote weapon systems market with the largest revenue share of 38.4% in 2025, owing to strong defense budgets, advanced technological infrastructure, and continuous military modernization programs. The region emphasizes integration of AI-enabled targeting, autonomous weapon platforms, and network-centric warfare systems. Increasing investments in border security, homeland defense, and unmanned combat systems further accelerate demand, while defense contractors drive innovation through next-generation RWS solutions.

U.S. Remote Weapon Systems Market Trends

The remote weapon systems market in the U.S. accounted for the largest market revenue share in North America in 2025, driven by extensive defense modernization initiatives and integration of RWS across armored vehicles, combat platforms, and security installations. The growing adoption of AI-integrated targeting systems, rising focus on force protection, and expansion of unmanned and autonomous weapon capabilities are the key trends driving the U.S. market.

Europe Remote Weapon Systems Market Trends

The remote weapon systems in Europe is growing at a rapid pace, driven by NATO defense commitments, rising geopolitical tensions, and collaborative defense funding such as the European Defense Fund. The cross-border procurement programs, modular RWS adoption, and increased deployment in border security and peacekeeping missions are the key factors driving the market growth. The region is also witnessing a push toward defense sovereignty and local manufacturing, alongside growing investments in counter-drone and advanced weapon technologies.

The UK remote weapon systems industry is expected to grow rapidly during the forecast period, driven by advanced defense technology development and the modernization of military capabilities, with a focus on integrating sophisticated RWS into land and naval platforms. The growing emphasis on precision targeting, interoperability with NATO systems, and innovation-led procurement are the key trends accelerating the market growth.

The remote weapon systems market in Germany is supported by strong defense industrial capabilities, NATO-aligned procurement, and participation in multinational military programs. The country focuses on high-performance, modular weapon systems and export-oriented defense manufacturing. Trends include increased investments in armored vehicle upgrades and collaborative European defense projects, although export controls and regulatory frameworks shape market dynamics.

Asia Pacific Remote Weapon Systems Market Trends

The remote weapon systems market in the Asia Pacific is anticipated to register at the fastest CAGR of 10.5% from 2026 to 2033, driven by rising defense expenditures, territorial disputes, and rapid military modernization. Countries are investing heavily in naval and land-based RWS to address maritime security challenges and drone threats. The localization of manufacturing, technology transfer agreements, and the increasing adoption of unmanned and AI-driven weapon systems are enhancing combat readiness, thereby driving the market growth.

The Japan remote weapon systems market is gaining momentum, driven by defense modernization focused on precision, reliability, and integration with existing military systems. The country emphasizes high-quality, technologically advanced systems with strong ethical and regulatory oversight. The steady adoption of automated and semi-autonomous weapon systems, supported by a mature defense ecosystem and a focus on national security amid regional tensions, is the key factor driving the market growth.

The remote weapon systems market in China is witnessing robust expansion, fueled by significant defense spending, indigenous technology development, and large-scale military modernization programs. The market is characterized by strong government support for domestic manufacturing, increasing deployment of AI-enabled and unmanned RWS platforms, and expansion of defense infrastructure. There is also a clear trend toward self-reliance and integration of advanced technologies into next-generation combat systems.

Key Remote Weapon Systems Company Insights

Some of the key players operating in the market are Elbit Systems Ltd. and Rheinmetall AG, Inc., among others.

-

Elbit Systems Ltd. develops and supplies advanced defense electronics, land systems, C4I solutions, electro-optics, unmanned aerial systems, and electronic warfare products for military, homeland security, and commercial aviation applications worldwide. Operating through segments such as Aerospace, ISTAR/EW, Land, and Elbit Systems of America, the Israel-based company, founded in 1966 and headquartered in Haifa, serves governments as a prime contractor or subcontractor, offering precision-guided munitions, command systems, armored vehicle protection, and signal intelligence technologies.

-

Rheinmetall AG operates as an integrated technology group focused on mobility and security solutions, spanning automotive components like engine parts and defense systems such as vehicle platforms, weapons, ammunition, electronic solutions, air defense, and sensor technologies. The company divides operations into Vehicle Systems, Weapon and Ammunition, and Power Systems segments, providing combat vehicles, turrets, artillery, radar, and protection systems to armed forces globally while pursuing CO2 neutrality.

Some of the emerging players operating in the market include ASELSAN, and Saab AB, among others.

-

ASELSAN A.Ş. designs, develops, and manufactures defense electronics, including communication systems, radar, electronic warfare, electro-optics, avionics, unmanned systems, land and naval weapon platforms, air defense, missiles, and command-control solutions, alongside civilian applications in transportation, security, energy, and medical technologies.

-

Saab AB provides defense, aviation, and security solutions spanning military aircraft such as the Gripen fighter, missiles, radar systems, electronic warfare, command and control, unmanned aerial vehicles, naval combat systems, and civil security technologies across Aeronautics, Dynamics, Surveillance, Industrial Products and Services, and Support and Services segments. With a global presence, the company delivers integrated systems for air, land, sea, and space operations, emphasizing security through continuous technology adaptation for military and civilian customers.

Key Remote Weapon Systems Companies:

The following key companies have been profiled for this study on the remote weapon systems market.

- Elbit Systems Ltd.

- Rafael Advanced Defense Systems Ltd.

- Rheinmetall AG

- Leonardo S.p.A.

- BAE Systems plc

- Thales Group

- ASELSAN A.S.

- RTX Corporation / Raytheon Technologies

- General Dynamics Corporation

- Saab AB

Recent Developments

-

In February 2026, Rheinmetall AG showcased the RCWS320C-UAS, a latest-generation remote-controlled weapon station at Enforce Tac 2026 in Nuremberg, designed specifically for countering drones and fast-moving aerial threats.

-

In November 2025, Elbit Systems Ltd. signed a USD 2.3 billion international contract for an undisclosed strategic solution to be performed over eight years. The Haifa-based firm emphasized its investment in advanced systems providing competitive advantages, though details on the customer, location, or specific equipment remain confidential.

-

In March 2025, Rafael Advanced Defense Systems Ltd. and Elbit Systems Ltd. were awarded a contract to supply an integrated Maritime Electronic Warfare (EW) Self-Protection Solution for new frigates of NATO European countries.

Remote Weapon Systems Market Report Scope

Report Attribute

Details

Market size in 2025

USD 11.7 billion

Estimated market size in 2026

USD 12.7 billion

Projected market size by 2033

USD 23.7 billion

Growth rate

CAGR of 9.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, platform, weapon type, technology, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Elbit Systems Ltd.; Rafael Advanced Defense Systems Ltd.; Rheinmetall AG; Leonardo S.p.A.; BAE Systems plc; Thales Group; ASELSAN A.Ş.; RTX Corporation / Raytheon Technologies; General Dynamics Corporation; Saab AB.

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Remote Weapon Systems Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global remote weapon systems market report based on component, platform, weapon type, technology, application, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Sensors and EO/IR Suites

-

Weapons and Armaments

-

Human-Machine Interface (HMI)

-

Fire-Control and Ballistic Computers

-

Stabilization Units

-

-

Platform Outlook (Revenue, USD Million, 2021 - 2033)

-

Land-based

-

Naval-based

-

Airborne

-

-

Weapon Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Lethal

-

Non-lethal

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Remote Controlled

-

Autonomous

-

Semi-Autonomous

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Military & Défense

-

Homeland Security

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

MEA

-

UAE

-

South Africa

-

Kingdom of Saudi Arabia (KSA)

-

-

Frequently Asked Questions About This Report

The global remote weapon systems market size was valued at USD 11.7 billion in 2025 and is expected to reach 12.7 billion by 2026.

North America dominated with a 38.4% revenue share in 2025.

Land-based segment held the largest revenue share in 2025.

Lethal segment held the largest revenue share in 2025, while non-lethal is the fastest-growing area.

Military & defense held the largest share in 2025 and homeland security is the fastest-growing market.

Key players operating in the market include Elbit Systems Ltd., Rafael Advanced Defense Systems Ltd., Rheinmetall AG, Leonardo S.p.A., BAE Systems plc, Thales Group, ASELSAN A.Ş., RTX Corporation / Raytheon Technologies, General Dynamics Corporation, and Saab AB.

The steady rise in global defense spending amid escalating geopolitical tensions, border conflicts, and asymmetric warfare, growing shift toward modular, scalable systems, and the rising proliferation of unmanned platforms are the key factors driving the remote weapon systems market.

The global remote weapon systems market is expected to grow at a compound annual growth rate (CAGR) of 9.5% from 2026 to 2033 and is projected to reach 23.7 billion by 2033.

The sensors and EO/IR suites segment accounted for the largest share, over 27.2% in 2025, driven by their central role in enabling real-time surveillance, target acquisition, and precision engagement across diverse combat environments.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.