- Home

- »

- Plastics, Polymers & Resins

- »

-

Returnable Packaging Market Size, Share Report, 2026-2033GVR Report cover

![Returnable Packaging Market (2026 - 2033)Report]()

Returnable Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastic, Metal, Wood), By Product (Pallets, IBCs, Crates, Drums & Barrels), By End Use (Food & Beverage, Automotive, Consumer Durables), By Region, And Segment Forecasts

Market Size, 2025

$128.9BMarket Estimate, 2026

$136.5BMarket Forecast, 2033

$206.2BCAGR, 2026–2033

6.1%Returnable Packaging Market Summary

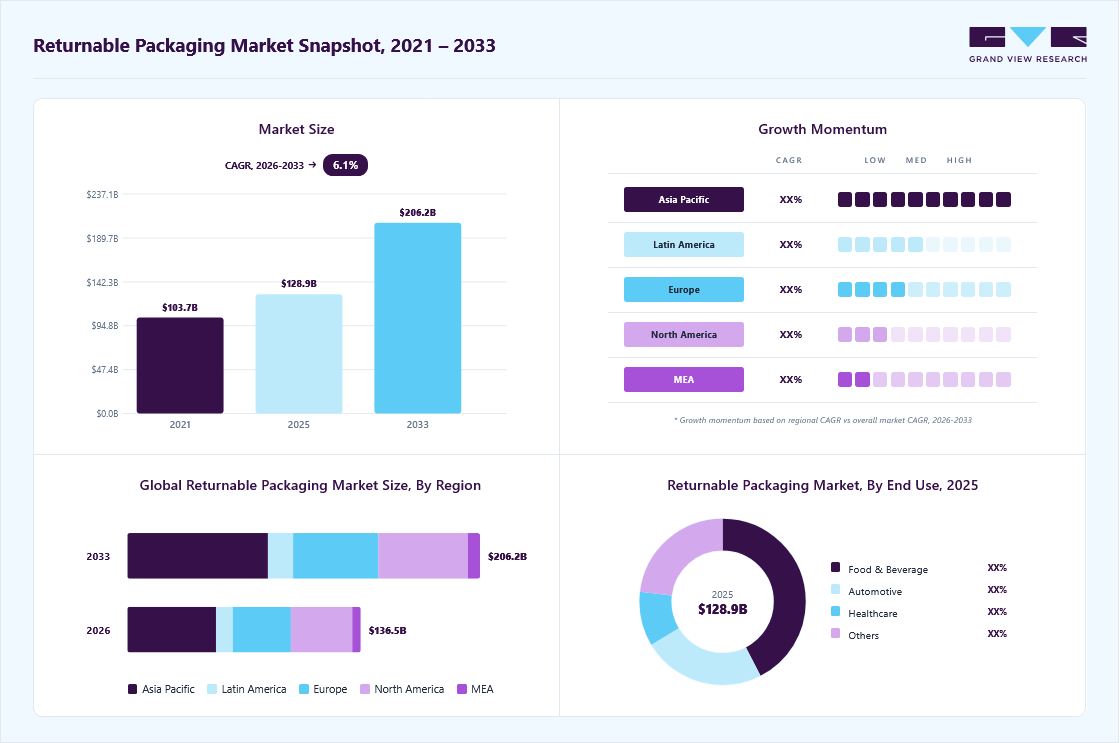

The global returnable packaging market size was valued at USD 128.9 billion in 2025 and is projected to grow from USD 136.5 billion in 2026 to USD 206.2 billion by 2033, at a CAGR of 6.1% from 2026 to 2033. The Asia Pacific held the largest share of 37.7% of the global market in 2025. The market is propelled by a rising emphasis on cost optimization and sustainability across logistics and supply chains.

Key Market Trends & Insights

- By material: The plastic segment recorded the largest market revenue share of 63.4% in 2025.

- By product: The pallets segment accounted for the largest market revenue share of 56.5% in 2025.

- By end use: The food & beverage segment recorded the largest market share of 34.4% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (37.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The market in India is expected to grow at a notable rate during the forecast period.

Market Size & Forecast

- Market size in 2025: USD 128.9 Billion

- Estimated market size in 2026: USD 136.5 Billion

- Projected market size by 2033: USD 206.2 Billion

- CAGR (2026-2033): 6.1%

Increasing adoption across automotive, food & beverages, and e-commerce sectors is further accelerating market expansion. A key driver of the returnable packaging market is its strong value proposition in reducing the total cost of ownership across the supply chain. While the initial investment is higher than single-use packaging, returnable systems typically support 50 to 150 reuse cycles, significantly lowering the cost per trip. This enables companies to reduce recurring procurement expenses, minimize waste management and disposal costs, and improve packaging utilization rates. Standardized returnable packaging also enhances load stability, reduces transit damage, and improves handling efficiency, generating additional operational cost savings and improving overall logistics economics.")

Rising regulatory pressure to reduce packaging waste, lower carbon emissions, and improve material recovery rates is accelerating the shift toward returnable packaging solutions. Governments are introducing stricter environmental compliance frameworks, while multinational corporations are strengthening their ESG strategies to meet sustainability targets and investor expectations. Returnable packaging directly supports circular economy objectives by enabling repeated use, lowering lifecycle environmental impact, and significantly reducing landfill waste. As sustainability performance increasingly influences corporate reputation and procurement decisions, returnable packaging is becoming a strategic priority rather than a discretionary investment.

The increasing adoption of closed-loop logistics models across automotive, food and beverage, pharmaceuticals, electronics, and industrial manufacturing is a major growth catalyst for the returnable packaging market. Predictable transport routes, high shipment frequency, and stable trade flows enhance the economic viability of returnable systems. At the same time, supply chain regionalization and nearshoring strategies are strengthening short-distance distribution networks, which further support the efficient circulation and recovery of returnable packaging. This structural shift improves system visibility, reduces reverse logistics complexity, and drives higher return rates.

Market Concentration & Characteristics

The returnable packaging market is characterized by high capital intensity and long asset life cycles, as products such as pallets, crates, containers, and intermediate bulk containers are designed for repeated use over extended periods. This results in higher upfront investment requirements for end users, balanced by lower operating costs over time. As a result, purchasing decisions are driven by total cost of ownership, durability, and lifecycle performance rather than unit price alone, making the market strongly value-oriented and performance-driven.

Technological integration is another defining characteristic, with increasing adoption of automation-compatible designs, RFID tracking, and digital asset management platforms. These technologies enhance traceability, improve asset utilization, reduce losses, and support real-time monitoring of packaging circulation. As logistics networks become more complex and data-driven, smart returnable packaging solutions are gaining traction, especially among large multinational manufacturers and third-party logistics providers.

Material Insights

The plastic segment recorded the largest market revenue share of 63.4% in 2025. Plastic is the most widely used material in returnable packaging due to its lightweight nature, design flexibility, and resistance to moisture and chemicals. It is commonly used for pallets, crates, totes, and intermediate bulk containers (IBCs). High-density polyethylene (HDPE) and polypropylene (PP) are the most widely used polymers due to their durability and recyclability. The growth of plastic-based returnable packaging is primarily driven by its cost efficiency over the long term, lightweight design, which reduces shipping costs, and its high durability for multiple reuse cycles.

The metal segment is projected to register the fastest CAGR over the forecast period. Metal-based returnable packaging, including steel containers, aluminum pallets, and wire mesh crates, is widely adopted in high-load and demanding environments such as automotive manufacturing, chemical processing, and heavy equipment handling. These solutions offer superior durability, high impact resistance, and excellent performance under extreme temperature conditions, enabling extended service life. Although metal packaging involves higher initial costs and greater weight, its exceptional strength and long operational lifespan deliver strong cost efficiency over time, making it a preferred choice for heavy-duty and repetitive logistics applications.

Product Insights

The pallets segment recorded the largest market revenue share of 56.5% in 2025. Pallets are flat transport structures used to support goods during storage and transportation. Returnable pallets are especially popular in closed-loop systems due to their durability and reusability, making them ideal for sectors such as automotive, food & beverage, and pharmaceuticals. The increasing focus on supply chain efficiency and the growing demand for cost-effective and sustainable logistics solutions are driving the adoption of returnable pallets.

The IBCs segment is projected to witness the highest growth rate over the forecast period. This growth is driven by rising demand for efficient bulk handling of liquids and semi-liquids across chemical, food and beverage, and pharmaceutical industries. Increasing focus on safe transportation, space optimization, and reduced logistics costs is accelerating IBC adoption. Moreover, the shift toward reusable and sustainable bulk packaging solutions further supports rapid market expansion.

End Use Insights

The food & beverage segment recorded the largest market share of 34.4% in 2025. This dominance is driven by high-volume, repetitive distribution cycles in beverages, dairy, and processed foods, which favor closed-loop and returnable packaging systems. Strict hygiene, food safety, and regulatory compliance requirements further encourage the use of durable and standardized packaging formats. Additionally, strong sustainability commitments by food and beverage companies are accelerating the shift toward reusable packaging solutions.

The healthcare segment is anticipated to register the fastest CAGR during the forecast period. In the healthcare sector, returnable packaging is used for medical instruments, pharmaceutical containers, laboratory equipment, and diagnostic devices. Packaging must meet strict sterilization and hygiene standards. Stringent regulatory standards in medical logistics and rising global pharmaceutical demand are key drivers.

Region Insights

Asia Pacific returnable packaging market dominated the global market and accounted for the largest revenue share of 37.7% in 2025 and is expected to grow at the fastest CAGR during the forecast period. This positive outlook is due to rapid industrialization, booming e-commerce, and increasing environmental regulations. Countries such as China, India, and Japan are adopting returnable packaging to reduce waste and logistics costs, particularly in automotive, food & beverage, and electronics sectors.

Automotive manufacturers such as Toyota and Hyundai use returnable plastic containers (RPCs) for transportation, improving supply chain efficiency. Additionally, government initiatives promoting sustainability, such as China’s circular economy policies, are accelerating demand. The rise of quick-commerce and online grocery platforms, such as Alibaba and JD.com, further fuels the need for reusable crates and pallets to optimize last-mile deliveries.

North America Returnable Packaging Market Trends

The region’s growth in returnable packaging market is due to stringent environmental laws, advanced logistics infrastructure, and high consumer awareness of sustainability. The U.S. andCanada have well-established reverse logistics systems, enabling efficient reuse of packaging in retail, pharmaceuticals, and automotive industries. Walmart and Amazon, use returnable transit packaging (RTP) to minimize waste in their supply chains. The automotive sector, with companies such as Ford and GM, relies heavily on returnable dunnage and containers for just-in-time manufacturing. Furthermore, the push for zero-waste initiatives and corporate sustainability goals (e.g., Coca-Cola’s reusable bottle programs) is boosting market growth.

U.S. Returnable Packaging Market Trends

The U.S. returnable packaging market thrives on corporate sustainability commitments and cost-saving supply chain strategies. Major retailers such as Walmart and Target use reusable plastic containers (RPCs) for fresh produce, reducing packaging waste by up to 40%. The automotive industry employs returnable dunnage to cut costs and improve logistics.

Europe Returnable Packaging Market Trends

The European returnable packaging market is growing due to strict EU regulations on single-use plastics and a strong circular economy framework. Germany, France, and the Netherlands are pioneers in reusable packaging systems, particularly in food retail and automotive sectors. For instance, supermarkets such as Tesco and Carrefour use returnable crates for fresh produce, while automotive giants like Volkswagen employ reusable containers for parts logistics. The EU’s Single-Use Plastics Directive (SUPD) and Extended Producer Responsibility (EPR) laws further drive adoption. Additionally, the rise of reusable packaging start-ups highlights Europe’s innovation in closed-loop systems.

Key Returnable Packaging Company Insights

The competitive environment of the returnable packaging market is moderately fragmented, with a mix of established global players and regional manufacturers vying for market share. Key players such as Brambles, Schoeller Allibert, DS Smith, CHEP, Nefab Group, ORBIS Corporation, and Rehrig Pacific dominate through extensive distribution networks, strong customer relationships, and innovations in material durability and tracking technologies. These players focus on sustainable packaging solutions, product customization, and strategic partnerships with end-use industries such as automotive, food & beverage, and healthcare. Meanwhile, new entrants and smaller firms are leveraging niche applications and cost-effective solutions to gain traction, intensifying competition in specific regional and application segments.

Key Returnable Packaging Companies:

The following key companies have been profiled for this study on the returnable packaging market.

- Brambles

- Schoeller Allibert

- Orbis Corporation

- DS Smith

- Myers Industries

- Nefab Group

- Rehrig Pacific Company

- Schutz GmbH & Co. KGaA

- Vetropack Holding

- Amatech Inc.

- CHEP

Recent Developments

-

In July 2025, IPL, inc., a North American rigid plastic packaging company, merged with Europe’s Schoeller Allibert, a reusable transport packaging specialist, forming a global sustainable packaging powerhouse with over USD 1.4 billion in annual revenue. This merger is expected to combine strengths across food, automotive, and industrial sectors to drive innovation and sustainability.

-

In February 2025, ORBIS Corporation opened a 660,000-square-foot manufacturing plant in Greenville, Texas, to produce reusable totes and pallets. This expansion boosts ORBIS’s production capacity and supports its commitment to sustainability and the circular economy.

-

In November 2024, GWP Correx launched a new returnable packaging system called Rapitainer, designed to replace single-use corrugated cardboard boxes with durable, reusable plastic containers made from Correx material. The Rapitainer offers significant cost savings of up to 75% over single-use cardboard by providing a reusable container that can be used for more than 200 trips.

-

In October 2024, Tri-Wall Circular launched the YOYOBin Adjustable, a modular, foldable, and returnable plastic packaging solution specifically designed for the automotive industry to support sustainability and efficiency goals. Made of lightweight polypropylene with a capacity of up to 900 kg, this container significantly reduces weight compared to traditional metal and plastic options, aiding automotive OEMs and Tier suppliers in achieving lightweighting targets across their supply chains.

Returnable Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 128.9 billion

Estimated Market size in 2026

USD 136.5 billion

Projected Market size by 2033

USD 206.2 billion

Growth rate

CAGR of 6.1% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Material, product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; the Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; Australia; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE

Key companies profiled

Brambles; Schoeller Allibert; Orbis Corporation; DS Smith; Myers Industries; Nefab Group; Rehrig Pacific Company; Schutz GmbH & Co. KGaA; Vetropack Holding; Amatech Inc.; CHEP

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Returnable Packaging Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global returnable packaging market report based on material, product, end use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic

-

Metal

-

Wood

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Pallets

-

Crates

-

IBCs

-

Drums & Barrels

-

Dunnage

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Food & Beverage

-

Automotive

-

Consumer Durables

-

Healthcare

-

Others

-

-

Region Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The returnable packaging market is driven by increasing focus on cost efficiency and sustainability in logistics and supply chains.

The global returnable packaging market size was valued at USD 128.9 billion in 2025 and is expected to reach USD 136.5 billion in 2026.

The plastic segment recorded the largest market revenue share of 63.4% in 2025.

The pallets segment recorded the largest market revenue share of 56.5% in 2025.

The food & beverage segment recorded the largest market share of 34.4% in 2025.

The key players in the returnable packaging market include Brambles; Schoeller Allibert; Orbis Corporation; DS Smith; Myers Industries; Nefab Group; Rehrig Pacific Company; Schutz GmbH & Co. KGaA; Vetropack Holding; Amatech Inc.; and CHEP.

Asia Pacific dominated the returnable packaging market with the largest revenue share of 37.7% in 2025.

Asia Pacific is the fastest growing regional market.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.