- Home

- »

- Agrochemicals & Fertilizers

- »

-

Seed Coating Market Size And Share Report, 2026-2033GVR Report cover

![Seed Coating Market (2026 - 2033)Report]()

Seed Coating Market (2026 - 2033)

Size, Share & Trends Analysis Report By Form (Powder, Liquid), By Additive (Polymers, Colorants, Binders, Minerals), By Crop Type (Cereals & Grains, Oilseeds & Pulses), By Process (Encrusting, Pelleting), By Region, And Segment Forecasts

Market Size, 2025

$2.6BMarket Estimate, 2026

$2.7BMarket Forecast, 2033

$3.2BCAGR, 2026–2033

2.1%Seed Coating Market Summary

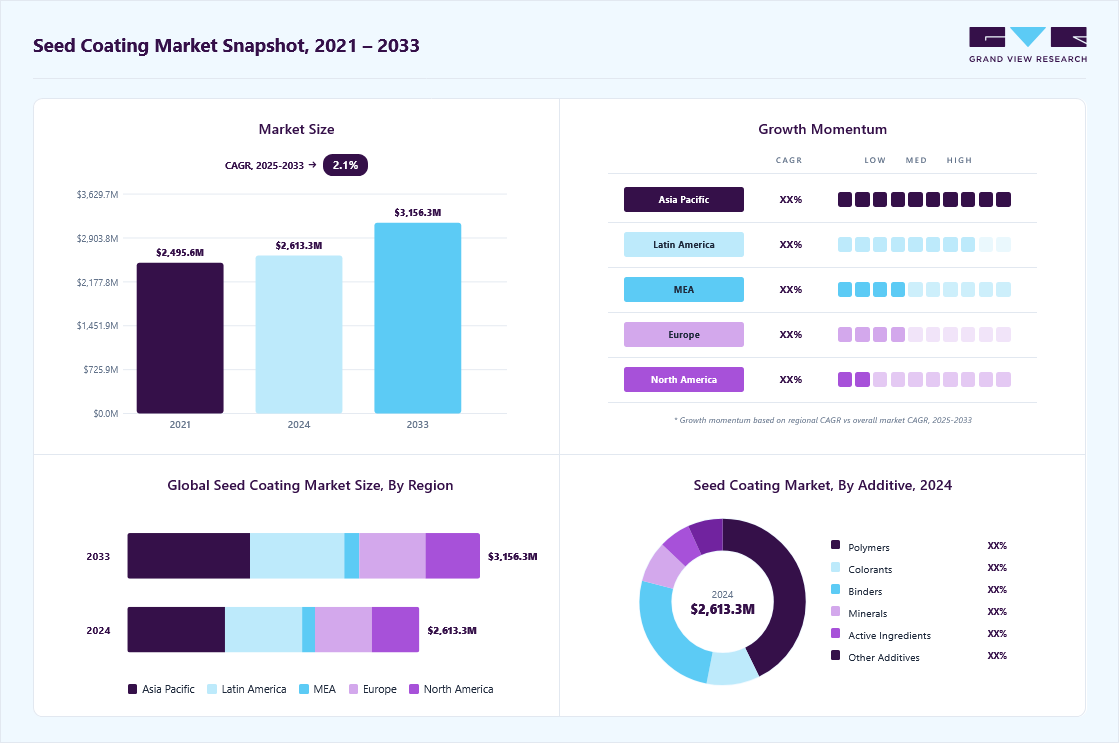

The global seed coating market size was valued at USD 2.6 billion in 2025 and is projected to grow from USD 2.7 billion in 2026 to USD 3.2 billion by 2033, growing at a CAGR of 2.1% from 2026 to 2033. Asia Pacific dominated the market with the highest revenue share of 33.4% in 2025. The market is primarily driven by the growing need to enhance seed performance and improve crop yield amidst shrinking arable land and increasing global food demand.

Key Market Trends & Insights

- By form: Liquid segment led the market with the largest revenue share of 63.5% in 2025.

- By additive: Polymers segment accounted for the dominant revenue share of 42.7%.

- By crop type: Cereals & grains segment dominated the market with a revenue share of 43.3% in 2025.

- By process: Pelleting segment by process dominated the global seed coating with a highest revenue share of 54.4% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (33.4% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 2.6 Billion

- Estimated market size in 2026: USD 2.7 Billion

- Projected market size by 2033: USD 3.2 Billion

- CAGR (2026-2033): 2.1%

The rising adoption of precision agriculture and advanced farming technologies has accelerated the use of coated seeds, especially in high-value and large-scale farming operations. In addition, the increasing focus on improving seed germination rates, uniform emergence, and early-stage pest protection is encouraging the integration of active ingredients, polymers, and micronutrients into seed coatings.The market offers significant opportunities with the rising demand for sustainable and organic seed coatings, driven by global shifts toward environmentally friendly farming practices. Advancements in biological additives, such as microbial inoculants and biostimulants, are opening new avenues for innovation and differentiation. In addition, expanding agricultural activities in emerging economies across Asia Pacific, Latin America, and Africa, supported by government initiatives and increased awareness about seed quality, are expected to create lucrative growth prospects for market participants.

")

Despite its advantages, the market faces challenges such as the high costs of seed coating technologies and raw materials, which can restrict adoption among small and medium-scale farmers. Moreover, variability in seed performance under different climatic and soil conditions may hinder consistent outcomes, reducing farmer confidence in certain regions. Regulatory restrictions on chemical-based additives and growing scrutiny over environmental impact also pose barriers to market expansion, particularly in Europe and North America.

Market Dynamics

Seed coating involves the application of protective and performance-enhancing materials onto seeds to improve handling, planting efficiency, germination rates, and crop establishment. Coatings may contain polymers, colorants, binders, nutrients, biological agents, and crop protection ingredients that support seed performance throughout the early stages of plant development. Increasing adoption of precision agriculture and demand for high-quality seeds continue to support market growth globally.

The increasing use of certified, hybrid, and genetically improved seeds is a major factor driving the seed coating market. Farmers are increasingly investing in high-value seeds that offer improved yield potential, disease resistance, and stress tolerance. Seed coatings help protect these investments by improving seed handling characteristics, enhancing germination performance, and supporting early crop establishment.

In addition, rising adoption of precision farming practices is encouraging the use of coated seeds that enable more accurate planting and uniform crop emergence. As agricultural producers focus on maximizing productivity and reducing input losses, demand for advanced seed treatment and coating technologies continues to increase across major crop-producing regions.

The seed coating market faces challenges from fluctuating crop prices, changing farm profitability, and volatility in agricultural input costs. During periods of lower farm income, growers often prioritize essential farm expenditures and may reduce spending on value-added seed technologies. Rising costs of fertilizers, crop protection products, fuel, and labor can further constrain farmers’ budgets, limiting investments in premium coated seeds. This price sensitivity is particularly evident in developing and cost-conscious agricultural markets, where adoption decisions are strongly influenced by short-term economic conditions. As a result, uncertain agricultural economics can slow the uptake of advanced seed coating solutions and hinder overall market growth.

Growing interest in sustainable agriculture is creating significant opportunities for seed coating manufacturers worldwide. The integration of biological agents, microbial inoculants, bio-stimulants, and environmentally friendly coating materials is gaining momentum as farmers seek solutions that enhance crop productivity while minimizing environmental impact. Increasing regulatory support for sustainable farming practices and the rising demand for residue-free agricultural products are further accelerating the adoption of biological seed treatments. These advanced coating technologies help improve seed vigor, nutrient uptake, and stress tolerance, contributing to higher crop yields. As the agriculture industry continues to shift toward eco-friendly and regenerative farming approaches, demand for sustainable seed coating solutions is expected to expand substantially, creating new growth avenues for market participants.

Market Concentration & Characteristics

The market is moderately fragmented, with a few global players, such as Solvay, BASF SE, Croda International Plc, Clariant, and DSM, dominating the competitive landscape. These companies benefit from their scale of operations, competitive pricing, and diversified product offerings. They are actively investing in research and development, expanding production capacities, and focusing on sustainable practices to strengthen their positions in the competitive market.

Leading players in the seed coating market are adopting a mix of strategic initiatives to strengthen their market position and address evolving agricultural demands. Key strategies include product innovation focused on sustainable and biodegradable coatings, integration of biological additives such as biopesticides and microbial inoculants, and developing customized formulations for specific crops and regional climates. Companies are also engaging in strategic partnerships and collaborations with seed producers, agrochemical firms, and research institutions to expand their technological capabilities and global footprint.

Analyst Perspective

The seed coating market is evolving beyond conventional crop protection applications toward integrated seed enhancement solutions that support precision farming and sustainable agriculture objectives. While protective coatings continue to account for a substantial share of demand, future growth opportunities are emerging in biological seed treatments, micronutrient delivery systems, and environmentally friendly coating technologies. Increasing adoption of high-value hybrid seeds and growing emphasis on improving planting efficiency are expected to accelerate innovation across the industry.

Form Insights

Based on form, the liquid segment led the market with the largest revenue share of 63.5% in 2025. Liquid coatings offer enhanced adhesion, uniform seed coverage, and better compatibility with a broad range of additives such as polymers, colorants, and active ingredients. These coatings facilitate precise and efficient application, improving seed handling, flowability, and germination consistency. The growing emphasis on precision farming and the need for high-quality, pre-treated seeds, especially in crops like cereals, oilseeds, and vegetables, have further contributed to the segment’s market leadership.

In contrast, while powder-based coatings remain cost-effective and are used in traditional or small-scale farming setups, they lack the consistency and binding strength of liquid formulations. The increasing demand for high-performance seed treatments and the integration of biologically active compounds, requiring liquid dispersal systems, continue to shift market preference toward liquid forms. Additionally, advancements in seed coating equipment and automation technologies are better aligned with liquid formulations, making them the preferred choice for large seed processors and agribusinesses seeking scalability and operational efficiency.

Additive Insights

In 2025, the polymers segment by additive accounted for the dominant revenue share of 42.7% share of total market revenue, driven by their critical role in enhancing seed protection, durability, and controlled-release functionality. Polymers act as binding agents that ensure uniform coating, improve adhesion of other additives, and form a protective barrier around the seed, preventing moisture loss and mechanical damage. Their versatility in both liquid and film coating processes, along with compatibility with a wide range of chemical and biological inputs, makes them indispensable in modern seed treatment solutions. Additionally, the growing adoption of polymer-based biodegradable and water-soluble formulations aligns with sustainability trends, further fueling demand.

Other additive categories such as colorants, binders, minerals, and active ingredients serve specialized roles, colorants aid in seed differentiation and safety compliance, binders enhance coating adhesion, minerals provide micronutrient support, and active ingredients deliver protection against pests and diseases. While these additives are essential, their effectiveness is often dependent on the structural base provided by polymers. As seed companies increasingly pursue integrated formulations for high-value crops, the demand for advanced polymer systems, capable of encapsulating active ingredients while maintaining seed vigor, continues to position this segment at the forefront of additive innovation and revenue generation.

Crop Type Insights

By crop type, the cereals & grains segment dominated the market with a revenue share of 43.3% in 2025, driven by the vast global acreage dedicated to staple crops such as wheat, corn, rice, and barley. These crops form the cornerstone of food security across developed and developing nations, driving consistent demand for high-quality, treated seeds. Seed coating is widely adopted in cereals and grains to enhance uniform germination, improve seed flow during mechanical sowing, and provide early-stage protection against pathogens and pests. Additionally, large-scale commercial farming operations in key agricultural economies, such as the United States, China, Brazil, and India, have accelerated the uptake of coated cereal seeds to ensure higher yields and operational efficiency.

While other crop types such as oilseeds & pulses, fruits & vegetables, and flowers & ornamentals are gaining traction, particularly with the expansion of high-value and export-oriented farming, their total cultivated area remains significantly lower than that of cereals and grains. Moreover, seed coating in cereals is cost-effective and scalable, making it particularly attractive for both seed manufacturers and farmers operating in high-volume markets. As global food demand continues to rise, coupled with the need for sustainable agricultural inputs, the cereals & grains segment is expected to maintain its dominant position in the crop-type outlook of the seed coating market.

Process Insights

In 2025, the pelleting segment by process dominated the global seed coating with a highest revenue share of 54.4% in 2025, driven by its advanced functionality and high precision in sowing applications. Pelleting involves transforming irregular-shaped seeds, such as lettuce, carrots, or flower seeds, into uniformly round units by adding inert materials, significantly enhancing planting accuracy and flowability in automated equipment. This method is particularly favored in high-value crops and horticultural sectors where uniform plant spacing and efficient seedling emergence are critical for maximizing yield and resource efficiency. Moreover, pelleting enables the incorporation of multiple active ingredients, including micronutrients, biostimulants, and protective agents, making it a preferred solution for value-added, multi-functional seed treatment.

Although film coating and encrusting remain widely used, especially for field crops and cost-sensitive applications, they typically involve thinner layers and less structural modification compared to pelleting. Film coating is popular for cereals and oilseeds due to its simplicity and minimal impact on seed size, while encrusting serves as a middle ground, offering slight increases in weight and improved handling. However, the versatility, mechanical precision, and compatibility with sophisticated sowing machinery have positioned pelleting as the most commercially viable and revenue-generating process, particularly in regions with advanced agricultural practices and intensive farming systems.

Regional Insights

Asia Pacific dominated the seed coating market with the highest revenue share of 33.4% in 2025, driven by rapid agricultural expansion, rising demand for high-yield crops, and government initiatives promoting seed quality enhancement. Countries such as India, China, Australia, and Southeast Asian nations are increasingly adopting coated seeds in cereals, rice, pulses, and vegetables to meet growing food security demands and export opportunities. Additionally, the region benefits from a large agricultural workforce, expanding mechanization, and rising awareness of precision farming techniques, further accelerating the adoption of advanced seed coating technologies.

China accounted for a dominating revenue share of 34.7% of the Asia Pacific seed coating market in 2025, supported by its vast agricultural base and strong government emphasis on improving seed performance and food self-sufficiency. With a focus on increasing crop productivity and reducing agrochemical inputs, Chinese seed producers are integrating coatings with biological and micronutrient additives. Rapid industrialization of agriculture, large-scale commercial farming in northern provinces, and the growth of protected cultivation for vegetables and ornamentals have positioned China as a key market for both film coating and pelleting technologies.

Latin America Seed Coating Market Trends

Latin America held a substantial 26.4% market share in 2024, fueled by large-scale cultivation of soybean, corn, and other cash crops, particularly in Brazil and Argentina. The region benefits from a strong export-oriented agricultural model and increasing mechanization, driving demand for coated seeds that support uniform sowing and yield consistency. Favorable climate conditions, growing awareness of seed technology benefits, and partnerships between global agribusinesses and regional players are contributing to the rapid expansion of both polymer-based coatings and pelleted seed formats.

Brazil seed coating marketstands as a key growth engine in the global seed coating market, driven by its dominant position in global soybean, corn, and cotton production. The country’s highly developed agribusiness sector and expansive commercial farming operations have accelerated the adoption of advanced seed coating technologies, particularly in the pelleting and film coating segments. Brazilian farmers are increasingly utilizing coated seeds to enhance plantability, protect against soil-borne pests, and optimize yield performance across large-scale plantations.

Europe Seed Coating Market Trends

European market captured 19.5% of the global seed coating market revenue in 2024, underpinned by strict seed quality standards, growing demand for organic and low-input farming, and government support for sustainable agriculture. The region exhibits strong adoption of eco-friendly seed coating formulations, with emphasis on biodegradable polymers and biological additives that comply with EU regulatory frameworks. High-value crops such as vegetables, fruits, and ornamentals, often cultivated under controlled conditions, drive the demand for pelleting and encrusting technologies, especially in countries such as Germany, France, and the Netherlands.

Seed coating market in Germany plays a pivotal role in the European seed coating market, driven by its highly mechanized agricultural sector and advanced seed treatment infrastructure. German seed companies prioritize quality, traceability, and regulatory compliance, leading to the widespread use of environmentally sustainable coatings. The country shows high demand for pelleted seeds in vegetable farming and controlled-environment agriculture, with a focus on reducing chemical usage through precision seed treatments. Germany also serves as a hub for R&D in novel coating materials and seed enhancement technologies.

North America Seed Coating Market Trends

North America accounted for 16.3% of the market in 2024, supported by the widespread adoption of precision agriculture, advanced seed technologies, and strong R&D investments by leading agri-input companies. The region is characterized by high usage of coated seeds in genetically modified (GM) and hybrid crops, particularly corn, soybean, and canola. Technological innovations in biologically active seed coatings and sustainability-driven formulations are gaining momentum, especially as environmental regulations and climate-resilient farming practices influence product development and adoption.

U.S. Seed Coating Market Trends

The United States remains the core market within North America, with robust adoption of coated seeds in large-scale monoculture farming and contract seed production. U.S. agribusinesses are leveraging pelleting and film coating techniques to improve seed flowability, optimize planting rates, and ensure early-stage crop protection. Regulatory support for advanced agri-tech and partnerships between seed companies and research institutions continue to drive innovation in polymer coatings and bio-based additives. Demand is particularly strong in crops such as maize, soybean, and vegetables cultivated in the Midwest and California regions.

Middle East & Africa Seed Coating Market Trends

The Middle East & Africa region is an emerging market in the seed coating industry, with growth supported by efforts to enhance agricultural productivity, food security, and water-use efficiency. While adoption is still in early stages, countries such as South Africa, Kenya, Saudi Arabia, and the UAE are increasingly exploring coated seeds to improve crop resilience under arid and semi-arid conditions. International development programs, government subsidies, and private sector investments in agricultural modernization are gradually driving uptake, particularly in staple crops and horticultural segments.

Key Seed Coating Company Insights

Key players, such as Solvay, BASF SE, Croda International Plc, Clariant, DSM, Precision Laboratories LLC, are dominating the market.

-

Solvay is a leading global chemical company that plays a significant role in the seed coating market through its portfolio of high-performance polymers, binders, and specialty additives. Leveraging its deep expertise in advanced materials and sustainable chemistry, Solvay provides innovative solutions that enhance seed protection, improve adhesion, and support the controlled release of active ingredients. The company is actively focused on developing bio-based and eco-friendly coating materials aligned with evolving regulatory standards and sustainable agriculture trends. Through strategic R&D investments, partnerships with agricultural technology firms, and a commitment to green innovation, Solvay continues to strengthen its position as a trusted supplier to seed treatment and crop protection companies worldwide.

Key Seed Coating Companies:

The following are the leading companies in the seed coating market.

-

Solvay

-

BASF SE

-

Croda International Plc

-

Clariant

-

DSM

-

Precision Laboratories LLC

-

Chromatech Incorporated

-

Germains Seed Technology

-

Universal Coating Systems

-

Michelman Inc.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Solvay, BASF SE, Croda International Plc, Clariant, DSM, Michelman Inc.)

- Expanding advanced seed enhancement technologies through continuous investment in sustainable coating innovations.

- Strengthening collaborations with seed companies to develop customized crop-specific coating solutions.

- Strong global presence enables extensive penetration across major agricultural production regions.

- Broad specialty chemical expertise supports development of high-performance and multifunctional coating formulations.

- Lengthy regulatory approval processes may delay commercialization of new coating technologies.

- Dependence on agricultural input demand exposes growth to seasonal and climatic fluctuations.

Emerging Players (Precision Laboratories LLC, Chromatech Incorporated, Germains Seed Technology, Universal Coating Systems)

- Focusing on specialized seed treatment technologies and tailored coating solutions for niche applications.

- Expanding regional distribution capabilities to strengthen market penetration and customer engagement.

- Strong application-specific expertise supports development of customized products for targeted crop segments.

- Agile organizational structures enable faster response to evolving agricultural market requirements.

- Limited global footprint may restrict access to large multinational seed producers.

- Smaller operational scale can constrain investments in advanced research and international expansion.

Global Seed Coating Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.6 billion

Estimated market size in 2026

USD 2.7 billion

Projected market size by 2033

USD 3.2 billion

Growth rate

CAGR of 4.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Form, Additive, Crop Type, Process, Region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

Solvay; BASF SE; Croda International Plc; Clariant; DSM; Precision Laboratories LLC; Chromatech Incorporated; Germains Seed Technology; Universal Coating Systems; Michelman Inc.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Seed Coating Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global seed coating market report based on form, additive, crop type, process, and region.

-

Form Outlook (Revenue, USD Million, 2021 - 2033)

-

Powder

-

Liquid

-

-

Additive Outlook (Revenue, USD Million, 2021 - 2033)

-

Polymers

-

Colorants

-

Binders

-

Minerals

-

Active Ingredients

-

Other Additives

-

-

Crop Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Cereals & Grains

-

Oilseeds & Pulses

-

Fruits & Vegetables

-

Flowers & Ornamentals

-

Other Crop Types

-

-

Process Outlook (Revenue, USD Million, 2021 - 2033)

-

Film Coating

-

Encrusting

-

Pelleting

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Latin America

-

Brazil

-

Argentina

-

-

Research Methodology

The seed coating market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each seed coating segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Form

Revenue capture definition

Liquid

As the dominant form segment, revenue is generated through liquid coating formulations applied during commercial seed treatment processes. Broad compatibility with polymers, active ingredients, and biological additives supports widespread adoption across large-scale agricultural seed production operations.

Powder

Revenue is supported by dry coating materials utilized to improve seed handling, protection, and planting performance. Demand is influenced by crop-specific treatment requirements, processing preferences, and applications where dry formulations provide operational advantages.

Segment - Additive

Revenue capture definition

Polymers

As the leading additive segment, revenue capture is driven by their extensive use in improving coating adhesion, durability, and active ingredient retention. Their critical role in maintaining coating performance supports strong demand across commercial seed treatment facilities.

Colorants

Revenue is generated through products used to enhance seed identification, brand differentiation, and regulatory compliance. Demand is supported by increasing adoption of treated seeds requiring clear visual distinction from untreated seed varieties.

Binders

Market value is supported by additives that improve coating attachment and formulation stability during processing, storage, and planting. Their contribution to coating integrity makes them an important component within seed treatment systems.

Minerals

Revenue is derived from mineral-based additives incorporated into coatings to improve seed performance and support early plant development. Demand is influenced by crop nutrition strategies and value-added seed enhancement programs.

Active Ingredients

Revenue capture is driven by crop protection compounds, biological agents, and performance enhancers integrated into coating systems. Increasing emphasis on seed protection and improved establishment continues to support growth within this segment.

Other Additives

This segment captures revenue from specialty materials including nutrients, microbial inoculants, bio-stimulants, and formulation aids designed to enhance seed quality and crop performance under varying agricultural conditions.

Segment - Crop Type

Revenue capture definition

Cereals & Grains

As the largest crop segment, revenue is generated through extensive treatment of corn, wheat, rice, barley, and other grain seeds. Large planting volumes and growing adoption of premium seed technologies contribute significantly to market value.

Oilseeds & Pulses

Revenue is supported by seed coating applications for crops such as soybean, canola, sunflower, and pulses. Demand is influenced by increasing cultivation acreage and the need to improve germination and crop establishment rates.

Fruits & Vegetables

Market value is driven by high-value crop seeds requiring enhanced planting precision, protection, and performance. Intensive cultivation practices and premium seed investments support adoption across commercial horticulture operations.

Flowers & Ornamentals

Revenue is generated through specialized seed coating technologies designed for ornamental and floriculture applications. Improved handling characteristics and planting efficiency continue to support commercial demand in this segment.

Other Crops

This segment derives revenue from coating applications across forage crops, turfgrass, industrial crops, and niche agricultural species requiring seed enhancement and protection solutions.

Segment - Process

Revenue capture definition

Film Coating

Revenue is supported by projects requiring basic fire protection compliance across smaller commercial, residential, and institutional structures. Lower material consumption requirements and broad applicability contribute to steady market demand.

Encrusting

Market value is supported by processes that modify seed size and shape while maintaining seed identity. Demand is driven by crops requiring improved handling and planting performance within commercial farming systems.

Pelleting

As the dominant process segment, revenue capture is driven by extensive use in creating uniform seed size and shape for precision planting applications. Growing mechanization and adoption of advanced sowing equipment continue to support strong demand.

Estimation Model

Layer Name

Key Question

Description

Seed Production Layer

What forms the addressable base?

Identify global production volumes of commercial seeds across cereals, grains, oilseeds, pulses, fruits, vegetables, and specialty crops requiring treatment and performance enhancement.

Coating Adoption Layer

Where are intumescent coatings adopted?

Estimate the proportion of commercial seed volumes utilizing coating technologies based on crop type, farming practices, seed value, and regional adoption of seed enhancement solutions.

Consumption Intensity Layer

How much coating is applied?

Analyze application rates, coating formulations, additive inclusion levels, and treatment processes to determine annual consumption of coating materials across crop categories.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the sale of liquid and powder coating formulations, polymers, binders, colorants, active ingredients, and related technologies supplied to seed companies and commercial seed treatment providers.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

The study delivers detailed country-level analysis across major agricultural markets, including Turkiye, Russia, Colombia, Chile, etc., covering coated seed adoption rates, crop production trends, regulatory landscape, and growth outlooks.

Enables stakeholders to identify high-potential agricultural markets, assess regional demand patterns, and develop expansion strategies aligned with crop cultivation trends and seed technology adoption levels.

Pricing Analysis

The report delivers comprehensive pricing assessment covering coating material costs, formulation economics, regional pricing trends, and cost structures influencing seed coating product competitiveness across major agricultural markets.

Supports procurement optimization, pricing strategy development, and profitability analysis by providing deeper visibility into key cost drivers and pricing dynamics throughout the seed coating value chain.

Opportunity Assessment

The study delivers detailed evaluation of growth opportunities across biological seed treatments, polymer-based coatings, micronutrient delivery systems, precision agriculture applications, and sustainable seed enhancement technologies.

Helps companies identify emerging revenue streams, prioritize innovation investments, and align product development strategies with evolving agricultural productivity and sustainability requirements globally.

Frequently Asked Questions About This Report

Some of the key players operating in the seed coating market include Solvay, BASF SE, Croda International Plc, Clariant, DSM, Precision Laboratories LLC, Chromatech Incorporated, Germains Seed Technology, Universal Coating Systems, Michelman Inc.

The seed coating market is driven by the growing demand for high-yield, high-quality seeds amid shrinking arable land and increasing global food needs. Advancements in precision agriculture and rising adoption of biologically active seed treatments are fueling market growth.

The global seed coating market is expected to grow at a CAGR of 2.1% from 2025 to 2033 to reach USD 3.2 billion by 2033.

Asia Pacific dominated the market with the highest revenue share of 33.4% in 2025.

The global seed coating market size was valued at USD 2.6 billion in 2025 and is estimated at USD 2.7 billion for 2026.

The liquid segment held the largest revenue share of 63.5% in 2025 due to its superior adhesion, uniform seed coverage, and compatibility with a wide range of additives, enhancing overall seed performance. Its ease of application and suitability for large-scale, precision farming further accelerated its adoption across key crop segments.

The liquid segment dominated the seed coating market in 2025, accounting for 63.5% of market revenue

The polymers segment dominated the seed coating market in 2025, capturing 42.7% of market revenue, due to its ability to enhance seed handling, improve coating adhesion, and support the effective delivery of active ingredients.

The encrusting segment is projected to witness the fastest growth during the forecast period, registering a CAGR of 2.2% from 2026 to 2033

About the Author(s)

Agrochemicals & Fertilizers Research Team

Bulk Chemicals · Agrochemicals & FertilizersThis report was authored by the agrochemicals & fertilizers research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the agrochemicals & fertilizers segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.