- Home

- »

- Next Generation Technologies

- »

-

Smart Meter Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Smart Meter Market (2026 - 2033)Report]()

Smart Meter Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Hardware, Software), By Type (Smart Electric Meter, Smart Water Meter), By Technology, By End Use (Residential, Commercial), By Region, And Segment Forecasts

Market Size, 2025

$30.9BMarket Estimate, 2026

$34.4BMarket Forecast, 2033

$58.7BCAGR, 2026–2033

7.9%Smart Meter Market Summary

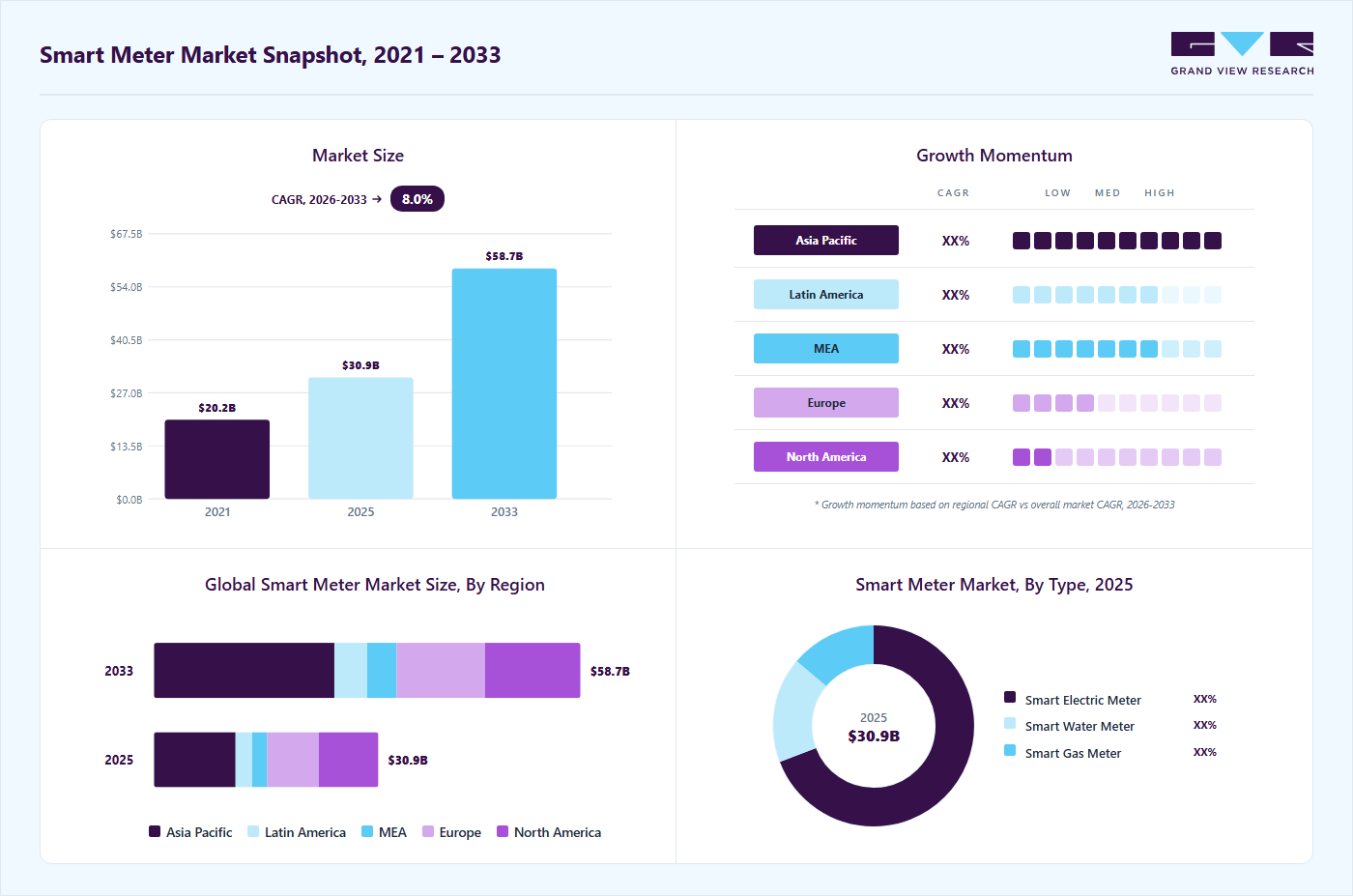

The global smart meter market size was valued at USD 30.9 billion in 2025 and is projected to grow from USD 34.4 billion in 2026 to USD 58.7 billion by 2033, at a CAGR of 7.9% from 2026 to 2033. The Asia Pacific market held the largest share of 36% of the global market in 2025. Governments worldwide are increasingly implementing policies and regulations that mandate advanced metering infrastructure (AMI) to replace traditional meters with smart energy market solutions, ensuring precise billing and minimizing revenue losses from theft or errors.

Key Market Trends & Insights

- By component: The hardware segment dominated the market with a share of over 78% in 2025.

- By type: The smart electric meter segment dominated the market in 2025.

- By technology: The AMR (Automated Meter Reading) segment accounted for the largest market share in 2025.

- By end use: The residential segment accounted for the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (36% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 30.9 Billion

- Estimated market size in 2026: USD 34.4 Billion

- Projected market size by 2033: USD 58.7 Billion

- CAGR (2026-2033): 7.9%

This regulatory push has standardized smart meter adoption across utilities, driving accelerated deployments as utilities comply with national mandates. The growing advancements in IoT sensors, edge AI, and 5G networks are revolutionizing the smart energy market by reducing deployment costs, enabling ultra-low latency data processing for millions of devices, and unlocking new revenue streams through predictive maintenance and value-added analytics services. This is further driving mass adoption as utilities scale smart grid operations with enhanced reliability and cyber-secure remote management, particularly in the smart electric meter industry and its market segments.")

Advanced metering infrastructure (AMI) is rapidly advancing within the smart meter market, facilitating bidirectional communication between utilities and end users, with strong growth in the smart gas meter market and smart water meter market. This technology supports real-time data gathering, dynamic load balancing, and sophisticated analytics, allowing utilities to streamline grid performance while enabling consumers to better control their energy consumption. The expansion of AMI is closely linked with IoT and AI integration, which enhances data processing, predictive maintenance, and demand response capabilities across smart electric meter market applications.

In addition, the demand for smart meters is rapidly increasing, driven by their critical applications in energy management, grid modernization, billing accuracy, and real-time consumption monitoring, especially in the three-phase smart electric meter industry for industrial and commercial use. Smart meters enable utilities and consumers to access high-resolution usage data, optimizing energy distribution and supporting advanced decision-making for load forecasting and demand response programs. Their role in enhancing transparency, reducing non-technical losses, and enabling precise billing is fueling adoption across residential, commercial, and industrial sectors, strengthening deployment initiatives by governments and utility providers worldwide.

Furthermore, consumer-focused software platforms and analytics tools are revolutionizing the smart meter industry through real-time monitoring, granular consumption insights, and customized energy management features, with notable traction in the residential smart gas meter market. These advancements foster stronger customer engagement, enable effective demand-response programs, and empower utilities to enhance grid performance in the broader smart energy market.

Moreover, key companies are pursuing innovative strategies centered on integrating cutting-edge technologies like IoT, artificial intelligence, and edge computing to improve data precision, grid-edge functionality, and real-time analytics across smart gas meter market, smart water meter market, smart electric meter market, and smart electricity meter market solutions. They are broadening their advanced metering infrastructure (AMI) portfolios to support predictive maintenance, facilitate electric vehicle integration, and provide holistic energy monitoring and optimization, including specialized three phase smart electric meter market and residential smart gas meter market offerings. Such strategies by key companies are expected to drive the market growth in the coming years.

Component Insights

The hardware segment dominated the market with a share of over 78% in 2025, owing to surging demand for reliable physical infrastructure in AMI rollouts, government mandates, and utility upgrades, which drive hardware growth by requiring durable, scalable installations that support real-time data capture and grid connectivity, reducing deployment risks while enabling seamless integration with existing networks. The growing advancements, such as integration with IoT devices, support for multiple utilities (electricity, gas, water), and enhanced display features, are key drivers of the segment.

The software segment is expected to witness the fastest CAGR of over 11% from 2026 to 2033. The segmental growth is driven by the increasing demand for data analytics, real-time monitoring, predictive maintenance, cloud-AI integration, and user-friendly platforms that enable utilities to analyze consumption patterns, detect anomalies, optimize grid performance, and boost customer engagement for superior energy management. Integration with cloud computing and AI enhances decision-making, while user-friendly interfaces improve customer engagement and energy management. These factors are expected to drive segmental growth in the coming years.

Type Insights

The smart electric meter segment dominated the market in 2025, driven by global initiatives for energy efficiency, grid upgrades, and decarbonization. These meters facilitate bidirectional communication, precise billing, and remote oversight, aiding the incorporation of renewable energy while curbing non-technical losses. Government regulations alongside IoT and edge computing innovations accelerate their widespread deployment.

The smart water meter segment is expected to witness the fastest CAGR from 2026 to 2033, driven by urgent water conservation needs and advanced leakage detection requirements. Offering real-time usage visibility to utilities and consumers, these meters enhance billing precision and resource management. IoT integration and data analytics enable anomaly detection and optimized distribution, supporting broader sustainability objectives.

Technology Insights

The AMR (Automated Meter Reading) segment accounted for the largest market share in 2025, owing to its ability to automate data collection, reducing manual meter reading costs and errors. The segmental growth is driven by utilities seeking cost-effective automation to replace manual meter readings, improving billing accuracy and operational efficiency through one-way data transmission, while meeting regulatory demands for reduced labor costs and faster data turnaround in electricity, gas, and water sectors.

The AMI (Advanced Metering Infrastructure) segment is expected to witness the fastest CAGR from 2026 to 2033. AMI segment expansion is propelled by the need for advanced grid intelligence via two-way communication, enabling real-time demand response, remote management, outage detection, and renewable integration, as governments and utilities prioritize smart grid modernization for enhanced reliability and consumer engagement. These factors are expected to drive segmental growth in the coming years.

End Use Insights

The residential segment accounted for the largest market share in 2025, driven by widespread government incentives for household energy efficiency, rising consumer adoption of smart home technologies, and utilities targeting mass deployments to enable real-time usage monitoring, demand response programs, and personalized billing that reduce peak loads and promote conservation. Regulatory mandates and government incentives promote widespread adoption, while technological advancements such as IoT integration and advanced communication technologies enhance functionality.

The industrial segment is expected to witness the fastest CAGR from 2026 to 2033, owing to escalating demand for large-scale energy optimization, integration with automation systems like SCADA, and advanced analytics for predictive maintenance, as manufacturers prioritize cost savings, regulatory compliance, and resilience against power disruptions in high-consumption facilities.

Regional Insights

North America smart meter industry accounted for a significant global market share of over 26% in 2025, driven by federal funding such as the Infrastructure Investment and Jobs Act allocating billions for AMI upgrades, widespread utility replacements of aging meters, and state mandates in California and Texas for energy efficiency plus outage management, with trends toward second-wave deployments integrating EVs and renewables amid high penetration rates. Utilities and consumers are increasingly adopting smart meters to enhance energy efficiency and integrate renewable energy sources such as solar and wind into the grid.

U.S. Smart Meter Market Trends

The U.S. smart meter industry dominated the market with a share of over 79% in 2025, fueled by regulatory commissions mandating digital metering for peak load forecasting, cybersecurity compliance, and clean energy goals in states such as New York and Illinois, trending toward IoT-enhanced systems for real-time analytics and consumer demand-response programs.

Europe Smart Meter Market Trends

Europe smart meter industry is expected to grow at a CAGR of over 6% from 2026 to 2033, driven by strong regulatory mandates requiring widespread deployment to enhance energy efficiency and support the region’s carbon neutrality goals. The European Green Deal further accelerates investments in smart grid modernization and advanced energy management technologies. The market growth is also fueled by expanding infrastructure upgrades across Central and Eastern Europe, with increasing adoption of IoT and real-time data analytics playing a key role.

The UK smart meter industry is expected to grow at a significant rate in the coming years, owing to a government-led initiative to equip all households with smart meters. Utility companies and consumer awareness programs actively support this rollout, emphasizing dynamic pricing and energy consumption management. The focus on empowering consumers and regulatory backing continues to drive strong growth in smart meter adoption across the country.

The Germany smart meter industry is driven by its comprehensive regulatory framework and a national commitment to achieving carbon neutrality. The country’s advanced smart grid infrastructure and high integration of renewable energy sources create strong demand for smart metering solutions. Local technology providers contribute significantly by integrating smart meters with real-time monitoring and load balancing systems, supporting both residential and industrial energy management.

Asia Pacific Smart Meter Market Trends

The Asia Pacific smart meter industry accounted for the largest global market share of 36% in 2025, driven by rapid urbanization, industrialization, and government mandates promoting energy efficiency and grid modernization. Initiatives such as India’s Revamped Distribution Sector Scheme and growing investments in IoT and advanced metering infrastructure (AMI) support large-scale deployments. Rising energy demand and environmental concerns further propel adoption across residential, commercial, and industrial sectors are, thereby fueling market growth in the region.

The Japan smart meter industry is gaining traction, fueled by efforts to enhance energy supply safety and reduce costs following vulnerabilities. Japan’s emphasis on energy efficiency and grid resilience, combined with government and utility investments, supports steady market expansion in the country.

The China smart meter industry is rapidly expanding, driven by comprehensive government mandates and a completed nationwide rollout of smart electricity meters. In addition, advanced communication technologies such as PLC are widely used, and ongoing replacements of first-generation meters sustain continuous growth.

Key Smart Meter Company Insights

Some of the key players operating in the market are Siemens AG and Honeywell International, Inc., among others.

-

Siemens AG is a key player in the smart meter industry, driving growth through its advanced metering infrastructure and integration of IoT and AI technologies. The company focuses on providing smart meters equipped with grid-edge capabilities that support renewable energy integration, electric vehicle charging management, and predictive maintenance. Siemens’ smart meter solutions contribute to energy efficiency, grid modernization, and enhanced consumer energy management.

-

Honeywell International Inc. is a prominent player in the smart meter industry, offering comprehensive solutions that enable two-way communication between utilities and consumers for real-time data collection, accurate billing, and remote monitoring. Honeywell integrates IoT and AI technologies into its smart metering systems to enhance grid resilience, energy optimization, and customer engagement. The company’s smart meters support the transition to renewable energy sources and the digitalization of energy infrastructure.

Landis+Gyr Limited and Wasion Holdings Limited are some of the emerging market participants in the smart meter industry.

-

Landis+Gyr Limited specializes in integrated energy management solutions, with a strong presence in Europe and worldwide. The company has a large installed base of smart meters and is recognized for its advanced metering infrastructure, grid edge intelligence, and smart infrastructure technologies. Landis+Gyr continues to expand its market share in key European countries and benefits from supportive regulatory environments, energy transition trends, and strong investments in R&D and software services.

-

Wasion Holdings Limited is a global provider of advanced metering infrastructure, energy efficiency management, and smart energy solutions and specializes in the research, development, manufacturing, and sales of smart meters for electricity, water, gas, and heat, as well as comprehensive energy management systems. The company operates in over 20 countries with localized production facilities in Mexico, Brazil, Tanzania, Hungary, and other regions, enabling it to serve a broad international customer base.

Key Smart Meter Companies:

The following key companies have been profiled for this study on the smart meter market.

- ABB Group

- CIRCUTOR

- Hexing Electrical Co. Ltd.

- Honeywell International Inc.

- Iskraemeco

- Itron Inc.

- Kamstrup A/S

- Landis+Gyr Limited

- Larsen & Toubro

- Ningbo Sanxing Medical Electric Co., Ltd.

- Sagemcom SAS

- Sensus Technologies Private Limited

- Shenzhen Kaifa Technology Co., Ltd.

- Siemens AG

- Wasion Holdings Limited

Recent Developments

-

In February 2026, Honeywell launched its Hybrid Heating Solution to enable industrial manufacturers to integrate natural gas and electric energy sources for process heating, optimizing costs and emissions.

-

In January 2026, Ningbo Sanxing Medical Electric Co., Ltd. was certified by Frost & Sullivan as the world's No.1 smart meter vendor for 2020-2024, recognizing its leadership in global AMI deployments and innovation.

-

In March 2025, Itron and CHINT Global introduced the first residential electric smart meter based on the DLMS User Association’s AC Electricity Smart Meter (ACESM) Generic Companion Profile (GCP) standard. This collaboration advances interoperability and streamlines multi-vendor solution integration for the global utility market, enabling utilities to adopt smart meters more quickly and reduce integration and deployment costs.

Smart Meter Market Report Scope

Report Attribute

Details

Market size in 2025

USD 30.9 billion

Estimated market size in 2026

USD 34.4 billion

Projected market size by 2033

USD 58.7 billion

Growth rate

CAGR of 7.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report Product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, technology, type, end use, region

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Australia; Japan; India; South Korea; Brazil; South Africa; Saudi Arabia; UAE

Key companies profiled

ABB Group; CIRCUTOR; Hexing Electrical Co. Ltd.; Honeywell International Inc.; Iskraemeco; Itron Inc.; Kamstrup A/S; Landis+Gyr Limited; Larsen & Toubro; Ningbo Sanxing Medical Electric Co. Ltd.; Sagemcom SAS; Sensus Technologies Private Limited; Shenzhen Kaifa Technology Co. Ltd.; Siemens AG; Wasion Holdings Limited

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Smart Meter Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the smart meter market report based on component, technology, type, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Smart Electric Meter

-

Smart Water Meter

-

Smart Gas Meter

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Automatic Meter Reading (AMR)

-

Advanced Meter Infrastructure (AMI)

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Residential

-

Commercial

-

Industrial

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Frequently Asked Questions About This Report

Asia Pacific dominated with a 36.0% revenue share in 2025.

The smart electric meter segment led the market with the largest revenue share in 2025, while smart water meter is the fastest-growing type.

The AMR (automated meter reading) segment held the largest revenue share in 2025, while AMI (advanced metering infrastructure) is the fastest-growing technology.

The residential segment accounted for the largest revenue share in 2025, while the industrial segment is the fastest-growing.

The hardware segment dominated the market with a share of over 78.0% in 2025, owing to the growing innovations and focus on improved accuracy, durability, and communication capabilities.

Key players include ABB Group; CIRCUTOR; Hexing Electrical Co. Ltd.; Honeywell International Inc.; Iskraemeco; Itron Inc.; Kamstrup A/S; Landis+Gyr Limited; Larsen & Toubro; Ningbo Sanxing Medical Electric Co. Ltd.; Sagemcom SAS; Sensus Technologies Private Limited; Shenzhen Kaifa Technology Co. Ltd.; Siemens AG; Wasion Holdings Limited.

The global smart meter market size was valued at USD 30.9 billion in 2025 and is estimated at USD 34.4 billion for 2026.

The global smart meter market is expected to grow at a CAGR of 7.9% from 2026 to 2033, reaching USD 58.7 billion by 2033.

Key factors that are driving the smart meter market include the increasing adoption of renewable energy sources and the global push for energy efficiency and decarbonization.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.