- Home

- »

- Healthcare IT

- »

-

Surgical Simulation Market Size & Share Report, 2026-2033GVR Report cover

![Surgical Simulation Market (2026 - 2033)Report]()

Surgical Simulation Market (2026 - 2033)

Size, Share & Trends Analysis Report By Specialty, By Material (Virtual Patient Simulation, 3D Printing), By End Use (Academic Institutes, Hospitals), By Region, And Segment Forecasts

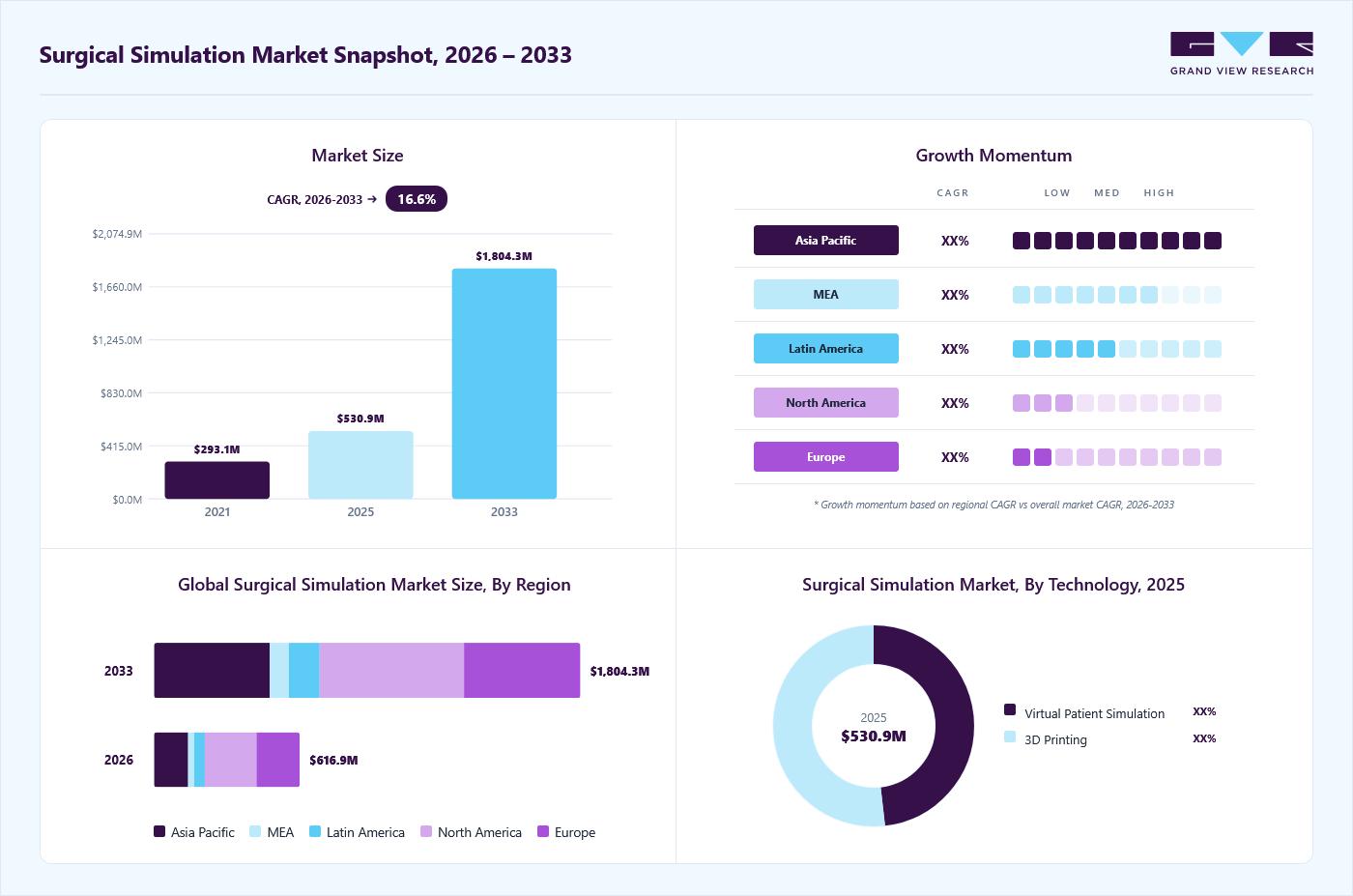

Market Size, 2025

$530.7MMarket Estimate, 2026

$616.9MMarket Forecast, 2033

$1,804.4MCAGR, 2026–2033

16.6%Surgical Simulation Market Summary

The global surgical simulation market size was valued at USD 530.7 million in 2025 and is projected to grow from USD 616.9 million in 2026 to USD 1,804.4 million by 2033, at a CAGR of 16.6% from 2026 to 2033. The market in North America dominated with a revenue share of 35.7% in 2025. Market growth is driven by advancements in medical technology, increasing demand for minimally invasive procedures, and a focus on enhancing surgical training and patient safety.

Key Market Trends & Insights

- By technology: 3D printing segment held the largest market share of 51.9% in 2025.

- By specialty: Orthopedic surgery segment held the largest market share of 31.8% in 2025.

- By end use: Academic institutes segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 530.7 Million

- Estimated market size in 2026: USD 616.9 Million

- Projected market size by 2033: USD 1,804.4 Million

- CAGR (2026-2033): 16.6%

Safe surgical care is a critical yet often overlooked component of health systems, with around 5 billion people lacking access. According to the Lancet Commission on Global Surgery 2030, only 6% of global surgeries are performed in the poorest nations, which account for one-third of the world’s population. A major issue is workforce training; low- and middle-income countries (LMICs) face severe shortages of certified surgeons, posing significant barriers to care. The global shortage of skilled surgeons, combined with the increasing complexity of surgeries, has intensified the need for advanced training tools that simulate real-life scenarios.")

The Lancet Commission recommends expanding the surgical, anesthetic, and obstetric workforce in LMICs to 40 per 100,000 people by 2030. However, traditional training in high-income countries can take over seven years, with up to 30% of trainees reporting a lack of readiness for independent practice post-residency. This gap in surgical education is driving the demand for surgical simulation solutions to improve workforce readiness and patient outcomes.

Technological advancements in the market, such as Virtual Reality (VR), have improved accessibility and reduced hardware costs, overcoming key adoption barriers. For instance, in November 2023, Simulare Medical announced the launch of its Alveolar Bone Graft (ABG) simulator, a novel addition to its expanding portfolio of high-fidelity surgical simulators designed for cleft surgery training.

"Alveolar bone graft surgery is technically challenging to perform and often underestimated. This is the first alveolar bone graft simulator developed and includes comprehensive anatomy that allows the user to perform all critical steps of the procedure. The alveolar bone graft simulator is a game changer with respect to training for this procedure."

-Dr. Dale Podolsky, MD, PhD, FRCSC, The Hospital for Sick Children.

Similarly, research by Vantari VR in June 2022 found that their medical VR training programs lowered medical errors by 40%. In addition, a University of Wollongong study conducted with Vantari VR reported a 32% improvement in student clinician performance and a 39% boost in adherence to safety and hygiene protocols. These results underscore VR technology’s significant potential to enhance surgical education and improve patient care outcomes.

Market Concentration & Characteristics

The degree of innovation in the surgical simulation industry is high. This is attributed to the advancements in VR, artificial intelligence, and haptic feedback. This technology offers realistic, risk-free training environments for medical professionals, enhancing skills and precision. For instance, in November 2023, Ethicon, a Johnson & Johnson MedTech company, introduced an AI-driven Surgical Simulation Platform designed to enhance skill development for current and future surgeons at the American Association of Gynecological Laparoscopists Global Congress. This technology utilizes artificial intelligence and augmented reality for training, offering real-time data and actionable feedback.

The level of partnerships and collaborations in the market remains moderate, with companies increasingly focusing on strategic alliances to technologically enhance and expand their existing product portfolios. For instance, in January 2025, InSimo, a Strasbourg-based company specializing in high-fidelity medical and surgical training simulation software, and VirtaMed AG, a global leader in highly realistic surgical simulation training, announced the renewal of their partnership. The collaboration aims to develop advanced simulation exercises designed to enhance robotic suturing training and elevate industry standards in surgical education.

“Our ongoing collaboration between VirtaMed and InSimo has been focused on advancing surgical simulation, particularly in the development of tools to enhance suturing skills. By combining our expertise, we have created innovative training solutions that address the growing demands of modern surgical procedures. This partnership is driving significant progress in surgical education, making it more precise, efficient, and accessible. Our work not only equips surgeons with advanced skills but also contributes to improving patient outcomes, marking a pivotal step in the evolution of robotic surgical training.”

-Marcel Hohl, VirtaMed AG - Chief Product Officer

The impact of regulations is moderate in the market. Regulations significantly shape the market by setting safety, efficacy, and data privacy standards. Compliance with medical device regulations ensures product quality and patient safety, fostering trust in simulation technologies.

The geographical expansion is significant as market players engage in strategic initiatives to strengthen their positions in the global market. For example, in July 2024, Maximum Fidelity Surgical Simulations, which specializes in lifelike cadaveric models for realistic surgical training, raised USD 2.25 million in a seed funding round. This funding was primarily led by St. Louis Arch Angels, the Missouri Technology Corporation, and BioGenerator Ventures. The capital is expected to be used for entering new markets, hiring full-time staff, and advancing technology development.

Specialty Insights

Orthopedic surgery dominated the market with a revenue share of 31.77% in 2025. The market growth is attributed to the increasing number of cases of orthopedic conditions, including osteoporosis, osteoarthritis, rheumatoid arthritis, and ligamentous knee injuries globally. According to a study published by NCBI in 2023, the anterior cruciate ligament (ACL) is the most frequently injured ligament in the knee, accounting for nearly 50% of all knee injuries. In the U.S., the annual incidence of ACL injuries is roughly 1 in 3,500 individuals, with about 400,000 ACL reconstruction procedures performed yearly.

This rising prevalence fuels the demand for enhanced knee injury treatment, encouraging market players to develop advanced simulations to train surgeons. Swemac specializes in developing simulators for teaching orthopedic surgeons and manufacturing their products for fracture treatment. ArthroVision and TraumaVision are orthopedic simulator systems offered by Swemac.

However, the reconstructive surgery segment is anticipated to witness the fastest growth at a CAGR of 17.36% over the forecast period. The growth is attributed to the rising demand for enhanced training solutions in complex reconstructive procedures, including facial, craniofacial, and breast reconstruction. High-fidelity simulators help surgeons hone their skills with precision, improving patient outcomes. Moreover, advanced 3D modeling and VR technologies enable realistic practice environments, further contributing to market growth.

Technology Insights

3D printing dominated the market, with the largest share of over 51.86% in 2025. The increasing awareness regarding the benefits of 3D printing simulation, coupled with companies undertaking various strategic initiatives to sustain their position in the market, is driving market growth. In April 2023, 3D Systems partnered with Clarkson College to establish a 3D Printing and Training Center of Excellence focused on healthcare innovation, education, and patient care. This collaboration seeks enhanced access to 3D printing and visualization technologies for healthcare facilities in the Omaha area.

Virtual patient simulation is expected to grow at the fastest CAGR over the forecast period. The market growth is attributed to the technological advancements in immersive learning. This technology enables healthcare professionals to practice surgical procedures in a risk-free environment, enhancing skill acquisition and patient safety. Using AI and VR, virtual patient simulators offer realistic, interactive experiences, allowing for personalized, repetitive training. Rising demand for remote education and better training tools further fuels the growth.

End Use Insights

Academic institutes dominated the market, with the largest revenue share in 2025. This growth is attributed to the growing adoption of advanced training technologies in medical education and surgical skill development. Academic medical centers and universities are increasingly integrating simulation-based learning tools, including high-fidelity simulators, virtual reality (VR), and augmented reality (AR) platforms, to enhance clinical training and improve procedural proficiency among students and residents.

In addition, the rising emphasis on patient safety and competency-based medical education has encouraged academic institutions to invest in simulation systems that allow trainees to practice complex procedures in a controlled and risk-free environment. Many universities and teaching hospitals have also established dedicated simulation laboratories and training centers, further driving the procurement of advanced simulation solutions.

The hospitals segment is expected to witness the fastest growth over the forecast period. An increased focus on advanced learning primarily drives the growth. Moreover, introducing advanced simulation technologies, the extensive application of simulation models in surgeries, and an increased need to reduce errors contribute to market growth. For instance, in March 2026, the Department of Ophthalmology at Kasturba Medical College and Hospital, Manipal, inaugurated an Ophthalmology Microsurgical Skills and Simulation Lab at Kasturba Hospital. The facility represents a significant advancement in simulation-based surgical education and training. Similarly, in January 2023, Attikon University General Hospital inaugurated a Surgical Simulation Lab designed to facilitate the training of general and orthopedic surgeons.

Regional Insights

North America dominated the surgical simulation market with the largest revenue share of 35.66% in 2025. The market growth is attributed to the region's availability of technologically advanced healthcare infrastructure. Furthermore, increasing investment in the healthcare sector, coupled with prominent players in the market, is fueling the market growth. For instance, in September 2024, the Health Resources and Services Administration, part of the U.S. Department of Health and Human Services, allocated approximately USD 75 million to enhance healthcare services in rural areas. The Biden-Harris Administration has implemented various initiatives to improve health in rural communities, including investments in medical training for physicians in these regions.

U.S. Surgical Simulation Market Trends

The surgical simulation market in the U.S. dominated North America. The market growth is attributed to the emergence of advanced technologies, favorable government policies, a rise in chronic conditions, and the presence of key players in the market. In November 2023, at the Global Congress meeting of the American Association of Gynecological Laparoscopists (AAGL), Medical Devices Business Services, Inc., the MedTech subsidiary of J&J known as Ethicon, introduced an AI-powered surgical simulation platform. This innovative platform aims to improve skill development for both existing and aspiring surgeons.

“We understand the challenges faced by today’s surgeons and surgical residents in their professional education journey, including issues related to accessibility and the vital tactile feedback needed for the development of cognitive and psychomotor skills.”

-Ethicon U.S. president Vishnu Kalra

Canada surgical simulation market is driven by the increased demand for minimally invasive procedures. Moreover, Canada’s investment in simulation-based education prioritizes patient safety and practical training, especially for high-risk surgeries. In addition, initiatives from organizations like Simulation Canada promote standardized simulation training, further driving its adoption across medical institutions.

Asia Pacific Surgical Simulation Market Trends

The surgical simulation market in the Asia Pacific is anticipated to grow at the fastest 2026 to 2033. Market growth is driven by rising demand for innovative technologies, minimally invasive treatments, and solutions focused on patient safety. Moreover, an increasing number of studies proving the surgical simulation efficiency significantly contributed to the market growth. For instance, a February 2022 study published by Hokkaido University’s Graduate School of Medicine in Japan highlighted that.

“Simulation-based training led to higher overall proficiency scores than conventional training, and fewer procedures were required to achieve proficiency in the complex form of the index procedure, with fewer serious complications overall. It is expected that the results of the trial will have a positive impact for advanced procedural training beyond the fields of surgery and urology in order to promote patients’ safety as well as better surgical outcomes.”

-Associate Professor of Urology at Hokkaido University’s Graduate School of Medicine

Japan surgical simulation marketis expected to grow rapidly in the coming years. The developments in healthcare education, an increased focus on patient safety, rising awareness, and adoption of simulation technology for surgeries are anticipated to drive market growth in Japan during the forecast period. For instance, in October 2023, Clinician-scientists from National University Health (NUH) and National University of Singapore (NUS) Medicine in Singapore utilized Japan's first surgical robot to perform a simulated gastrectomy, transmitting their movements in real-time from Singapore to a robotic unit in Japan over a dedicated international fiber-optic network. Leveraging the robotic surgery expertise of FHU, this initiative seeks to assess and address potential challenges in remote surgical procedures.

The surgical simulation market in China held a substantial market share in 2025. The growth is attributed to an increasing number of surgeries, along with the shortage of skilled doctors and surgeons. In addition, the rising number of local startups and the launch of technologically advanced simulations significantly drive the market growth.

India surgical simulation market is growing significantly in the coming years. The growth is attributed to an increasing number of simulation laboratories by hospitals and the adoption of advanced surgical simulators in academic institutes. In addition, the notable healthcare organizations are also taking initiatives to drive the adoption of these tools in the Indian market. For instance, in December 2025, Medtronic launched a new Mobile Surgi-Skill Lab across India’s tier-2 and tier-3 cities, intended for expanding access to advanced surgical training for healthcare professionals and young surgeons. The initiative is designed to strengthen clinical skill development by bringing hands-on training and simulation-based learning opportunities closer to healthcare professionals in underserved regions.

Latin America Surgical Simulation Market Trends

The surgical simulation market in Latin America is expected to witness steady growth over the forecast period, driven by increasing investments in medical education and the growing adoption of advanced training technologies. Medical institutions across countries such as Brazil, Mexico, and Argentina are increasingly incorporating simulation-based training platforms to improve surgical proficiency and patient safety. The rising focus on reducing surgical errors and enhancing the clinical readiness of medical graduates is encouraging hospitals and academic institutions to invest in virtual reality (VR), augmented reality (AR), and high-fidelity simulators.

Middle East & Africa Surgical Simulation Market Trends

The surgical simulation market in the MEA is projected to experience notable growth, supported by the rapid expansion of healthcare infrastructure and rising investments in medical training programs. Countries such as the UAE, Saudi Arabia, and South Africa are increasingly integrating simulation-based learning into their medical education frameworks to enhance the clinical skills of surgeons and healthcare professionals. The growing emphasis on improving surgical outcomes and minimizing procedural risks is encouraging hospitals and training centers to adopt advanced simulation technologies.

Key Surgical Simulation Company Insights

The market is moderately fragmented and highly competitive, characterized by the presence of several global and specialized simulation technology providers. Key market participants include Materialise, Stratasys, CAE Inc., Surgical Science, Mentice, Gaumard Scientific, and Simulab Corporation, among others. These companies focus on developing high-fidelity simulation platforms, VR- and AR-based training solutions, and procedure-specific simulators to address the growing demand for advanced surgical training tools. Market leaders are increasingly investing in technological advancements such as AI, VR, AR, and 3D printing technologies to enhance the realism and effectiveness of simulation-based surgical education. In addition, companies are expanding their product portfolios and strengthening their market presence through strategic collaborations with medical universities, hospitals, and training institutes.

Key Surgical Simulation Companies:

The following key companies have been profiled for this study on the surgical simulation market.

- Materialise

- Stratasys

- CAEInc.

- SurgicalScience

- Mentice

- GaumardScientific

- SimulabCorporation

- VirtaMedAG

- 3-DmedLearningThroughSimulation

- LaerdalMedical

- 3DSystems,Inc.

- Osteo3d

- AXIAL3D

- Formlabs

- KyotoKagakuCo.,Ltd.

Recent Developments

-

In July 2024, Materialise acquired FEops to enhance efficiency and clinical outcomes in structural heart interventions. This acquisition enabled Materialise to broaden its cardiovascular solutions by integrating predictive simulation capabilities, thereby advancing personalized treatment options for patients with heart conditions.

"At Materialise, we are pioneering the advent of mass personalization in healthcare, using advanced visualization and 3D printing technologies to deliver precise, patient-specific solutions. By integrating FEops’ advanced predictive simulation technology with our Mimics Planner, we are expanding our cardiovascular solutions to provide clinicians with comprehensive insights into patient anatomy. This integration will not only enhance the accuracy and efficiency of structural heart interventions but also improve clinical outcomes and patient safety.”-Brigitte de Vet, CEO, Materialise

-

In June 2024, Stratasys Ltd. launched the J5 Digital Anatomy 3D printer to meet the increasing need for affordable, high-accuracy anatomical models. This development supports hospitals, medical device manufacturers, and research institutions in improving patient outcomes, optimizing operations, and accelerating product development timelines.

-

In October 2023, Hologic, Inc. partnered with the American Association of Gynecologic Laparoscopists and Inovus Medical. As part of this collaboration, Hologic will be the primary supplier of hysteroscopes for the AAGL's Essentials in Minimally Invasive Gynecologic Surgery training program aimed at OB-GYN residents.

“This collaboration will strengthen our ability to offer hysteroscopy simulation for our residents, and to integrate advanced tools to aid our trainees in pursuing excellence in surgical training.” -Nash S. Moawad, M.D., EMIGS Chair.

-

In April 2022, Alcon launched the Alcon Fidelis Virtual Reality Ophthalmic Surgical Simulator. This VR tool is portable and is designed for cataract surgery trainees. Integrated within the Alcon Experience Academy, the simulator provides a realistic virtual operating room setting with haptic feedback to accurately replicate the experience of performing cataract surgery.

-

In September 2021, CAE Healthcare partnered with RCSI University of Medicine and Health Sciences to enhance healthcare technology, education, and research through simulation methodologies. The RCSI SIM Centre for Simulation Education and Research has been recognized as a certified Centre of Excellence, marking the first such designation in Europe.

Surgical Simulation Market Report Scope

Report Attribute

Details

Market size in 2025

USD 530.7 million

Estimated market size in 2026

USD 616.9 million

Projected market size by 2033

USD 1,804.4 million

Growth rate

CAGR of 16.6% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Specialty, technology, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country Scope

U.S.; Canada; Mexico; UK; Germany; France; Spain; Italy; Sweden; Denmark; Norway; Japan; China; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Materialise; Stratasys; CAE Inc.; Surgical Science; Mentice; Gaumard Scientific; Simulab Corporation; VirtaMed AG; 3-Dmed Learning Through Simulation; Laerdal Medical; 3D Systems, Inc.; Osteo3d; AXIAL3D; Formlabs; Kyoto Kagaku Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Surgical Simulation Market Report Segmentation

This report forecasts revenue growth and provides, at the regional and country level, an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global surgical simulation market based on specialty, technology, end use, and region:

-

Specialty Outlook (Revenue, USD Million, 2021 - 2033)

-

Cardiac Surgery

-

Gastroenterology

-

Neurosurgery

-

Orthopedic Surgery

-

Reconstructive Surgery

-

Oncology Surgery

-

Transplant

-

Others

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Virtual Patient Simulation

-

3D Printing

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Academic Institutes

-

Hospitals

-

Military Organizations

-

Research Organizations

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

Orthopedic surgery segment led with a 31.8% revenue share in 2025, while reconstructive surgery is the fastest-growing specialty.

The academic institutes segment held the largest revenue share in 2025, while hospitals is the fastest-growing segment.

3D printing segment led with a 51.9% revenue share in 2025, while virtual patient simulation is the fastest-growing technology.

Key players include Materialise; Stratasys; CAE Inc.; Surgical Science; Mentice; Gaumard Scientific; Simulab Corporation; VirtaMed AG; 3-Dmed Learning Through Simulation; Laerdal Medical; 3D Systems, Inc.; Osteo3d; AXIAL3D; Formlabs; Kyoto Kagaku Co., Ltd.

The global surgical simulation market size was valued at USD 530.7 million in 2025 and is estimated at USD 616.9 million for 2026.

The global surgical simulation market is expected to grow at a CAGR of 16.6% from 2026 to 2033, reaching USD 1,804.4 million by 2033.

North America dominated the surgical simulation market with a share of 35.7% in 2025. This growth is attributed to advancements in technology, increasing demand for minimally invasive surgeries, and increasing adoption of virtual reality (VR) and augmented reality (AR) technologies in surgical training.

Key factors that are driving the surgical simulation market growth include advancements in medical technology, increasing demand for minimally invasive procedures, and a focus on enhancing surgical training and patient safety.

About the Author(s)

Healthcare IT Research Team

Healthcare · Healthcare ITThis report was authored by the healthcare it research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the healthcare it segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.