- Home

- »

- Next Generation Technologies

- »

-

Unmanned Systems Market Size, Growth Report, 2026-2033GVR Report cover

![Unmanned Systems Market (2026 - 2033)Report]()

Unmanned Systems Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type, By Technology (Semi-Autonomous, Remotely Operated, Fully Autonomous), By Application, By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa), And Segment Forecasts

Market Size, 2025

$29.3BMarket Estimate, 2026

$32.4BMarket Forecast, 2033

$67.6BCAGR, 2026–2033

11.1%Unmanned Systems Market Summary

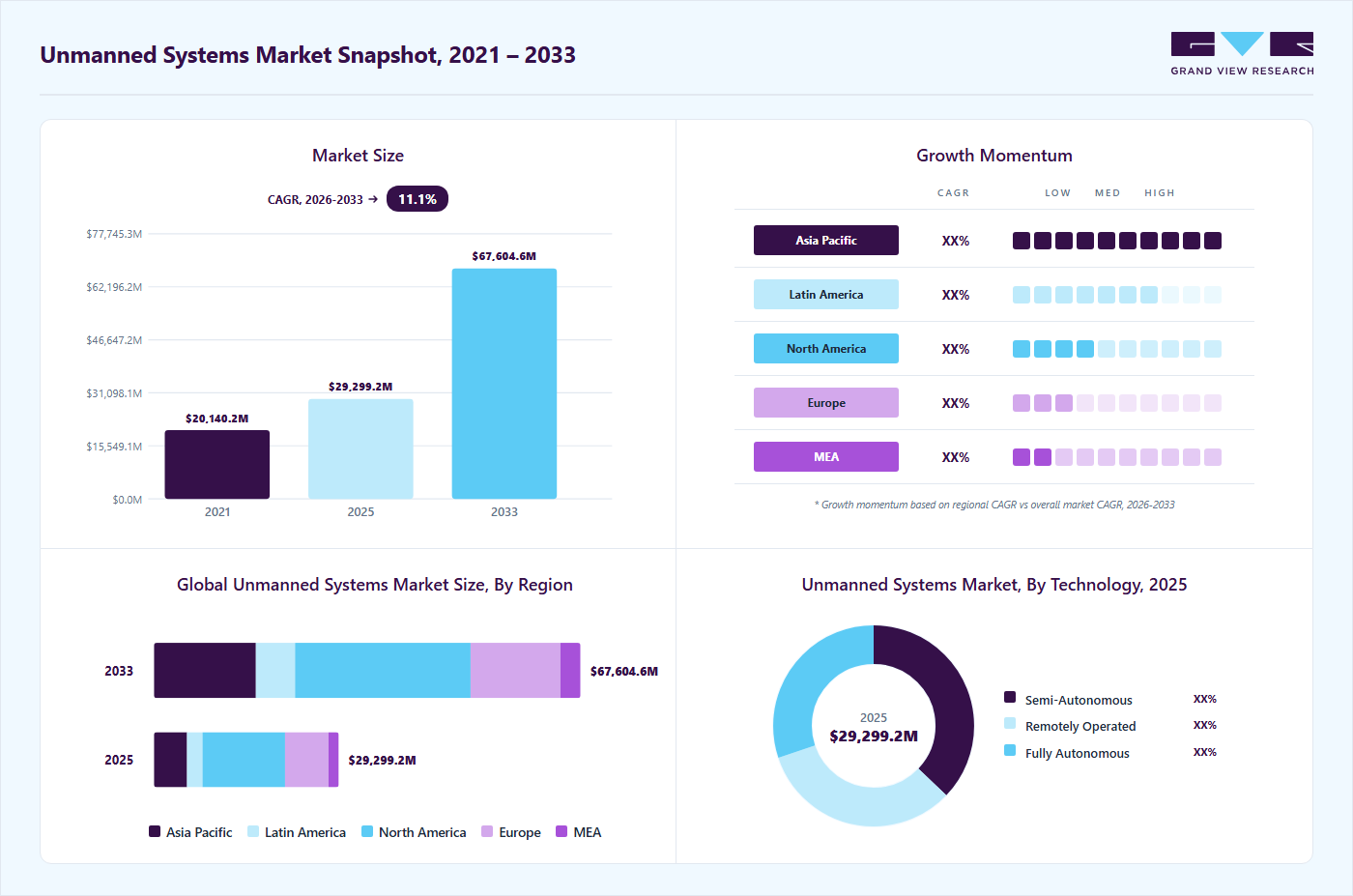

The global unmanned systems market size was valued at USD 29.3 billion in 2025 and is projected to grow from USD 32.4 billion in 2026 to USD 67.6 billion by 2033, at a CAGR of 11.1% from 2026 to 2033. The market in North America dominated with a revenue share of 44% in 2025. The market growth is driven by the surging demand for autonomous and semi-autonomous platforms spanning defense, surveillance, logistics, and industrial applications.

Key Market Trends & Insights

- By type: Unmanned aerial vehicles (UAVs) segment held the largest market share of 63% in 2025.

- By technology: Semi-autonomous segment held the largest market share in 2025.

- By application: Commercial segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (44% revenue share, 2025)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 29.3 Billion

- Estimated market size in 2026: USD 32.4 Billion

- Projected market size by 2033: USD 67.6 Billion

- CAGR (2026-2033): 11.1%

Additionally, heightened geopolitical tensions, along with ongoing defense modernization initiatives, are compelling military and law enforcement entities to integrate solutions from the tactical UAV market and the broader unmanned aerial systems market for reconnaissance, surveillance, and tactical operations. The growing relevance of the tactical UAV market is particularly evident in modern battlefield scenarios, where real-time intelligence and rapid deployment capabilities are critical, thereby accelerating overall unmanned systems industry growth.")

Rising global defense spending and heightened geopolitical tensions are accelerating demand for ISR capabilities and high‑risk mission support, helping reduce personnel exposure while improving precision‑strike effectiveness. The growing advancements in AI, sensor fusion, edge computing, and communication technologies are enabling real‑time data processing and seamless multi‑domain operations across aerial, ground, and maritime platforms. These innovations are significantly contributing to the expansion of the autonomous systems market while also strengthening capabilities within the counter-unmanned aerial systems market.

Additionally, military and law enforcement agencies are increasingly adopting unmanned systems to enhance mission efficiency and reduce personnel risks. These organizations are prioritizing semi‑autonomous platforms that provide a balanced mix of autonomous functionality and human oversight. Growing competition among industry players is also broadening the range of applications and driving continuous innovation, particularly across the military counter-unmanned aerial systems market and unmanned target systems market.

Furthermore, an increasing number of strategic partnerships and high-value contracts across the defense and commercial sectors is significantly driving the market expansion. These alliances focus on integrating advanced autonomy, interoperability, and mission-critical technologies to address rising demands for surveillance, logistics, and hazardous operations. Such collaborations are also supporting growth in commercial unmanned maritime systems market and the mining unmanned driving systems market, enabling seamless operations in complex and high-risk environments.

Moreover, governments worldwide are significantly increasing their investments in UAS technologies and forming strategic alliances with private contractors. These public-private partnerships promote innovation, boost local manufacturing capabilities, and accelerate fleet expansion, ensuring swift deployment across defense, law enforcement, and civil applications such as agriculture and urban planning. Such collaborations are critical enablers, providing market players with the resources and scale to innovate rapidly and capture emerging opportunities. These factors are expected to collectively drive the expansion of the unmanned systems industry in the coming years.

Type Insights

The unmanned aerial vehicles (UAVs) segment accounted for the largest share of over 63% in 2025, driven by surging demand in media and entertainment for aerial cinematography, live event coverage, and immersive FPV (first-person view) drones that deliver dynamic, hyper-realistic content unattainable by traditional cameras. UAVs enable high-demand applications such as 4K/8K drone light shows at concerts and stadiums, AI-integrated autonomous filming for esports broadcasts, and real-time streaming with low-latency 5G, capturing over half of commercial drone growth amid theme park expansions and virtual production trends.

The unmanned ground vehicles segment is expected to grow at a significant CAGR of 8.9% from 2026 to 2033, driven by increasing adoption in autonomous theme park rides, robotic interactive exhibits, and mobile AR-enhanced performances that deliver safe, dynamic crowd engagement without human operators. This growth underscores UGVs' rising role in scalable, cost-effective entertainment automation, particularly as AI navigation and modular designs enable seamless integration into live events and venues.

Technology Insights

The semi-autonomous segment accounted for the largest market share in 2025, driven by the widespread adoption of human-in-the-loop operations that combine operator oversight with robotic precision, enabling safer deployment in crowded entertainment venues such as drone light shows and robotic performances, where remote control ensures regulatory compliance and enables real-time adjustments. These systems lower entry barriers for producers through affordable hardware and intuitive interfaces, while hybrid autonomy supports scalable swarm coordination for immersive aerial or ground spectacles at festivals and stadium events.

The fully autonomous segment is expected to grow rapidly from 2026 to 2033, driven by advancements in AI-driven navigation, machine learning for obstacle avoidance, and edge computing that enable seamless, human-free operation, powering next-gen attractions such as self-navigating theme park robots and adaptive AR environments. Regulatory easing for BVLOS flights and standardized safety protocols accelerates commercialization, as these systems cut operational costs and enable 24/7 immersive experiences in location-based entertainment.

Application Insights

The commercial segment accounted for the largest market share in 2025, driven by booming demand for entertainment applications such as drone light shows at concerts, UAV cinematography for films, and UGV-powered autonomous rides in theme parks, where cost efficiencies from reusable fleets and real-time audience engagement tools boost profitability. Additionally, regulatory advancements enabling beyond-visual-line-of-sight (BVLOS) operations and partnerships with streaming platforms have accelerated adoption, allowing operators to deliver synchronized, multi-site immersive experiences that captivate global audiences at reduced logistical costs.

The military & law enforcement segment is anticipated to grow at a CAGR in the coming years, driven by escalating investments in drone swarms for tactical training simulations, unmanned surveillance at public events, and AI-enhanced robotic patrols that simulate real-world threat scenarios in VR/AR environments. Heightened focus on counter-terrorism readiness and border security integration further propels demand, as these systems offer cost-effective alternatives to manned operations while spilling over into entertainment, including hyper-realistic combat games and crowd management demos. This trajectory highlights the segment's pivotal role in bridging defense tech with immersive experiential applications.

Regional Insights

North America unmanned systems industry accounted for the largest market share of over 44% in 2025, driven by increased defense modernization budgets, cross-border surveillance needs, rapid technological innovation, and expanding commercial applications in agriculture and logistics. Additionally, the region's mature regulatory framework for BVLOS drone operations and a robust ecosystem of startups, tech giants, and venture capital have fueled widespread adoption in entertainment sectors such as large-scale drone light shows and autonomous film production.

U.S. Unmanned Systems Market Trends

The U.S. unmanned systems industry accounted for the largest market share of over 80% in 2025. The market is propelled by aggressive defense spending focused on next-generation Intelligence, Surveillance, and Reconnaissance (ISR) unmanned aerial vehicles, tactical autonomy programs, and the large-volume production of attractive drones. The Federal Aviation Administration's evolving BVLOS regulations support commercial applications such as precision agriculture and parcel delivery, as seen by Walmart's drone delivery network.

Europe Unmanned Systems Market Trends

Europe unmanned systems industry accounted for a significant share of over 23% from 2026 to 2033. In Europe, the market is heavily influenced by rising defense budgets and modernization programs, particularly driven by geopolitical tensions in Eastern Europe. Advancements in AI, sensor technology, and data communication are enabling increased autonomy and operational efficiency. Regulatory frameworks are evolving to integrate drones safely into urban airspaces while addressing cybersecurity and privacy concerns.

The UK unmanned systems industry is expected to grow rapidly in the coming years, driven by the strong defense spending combined with vibrant aerospace and technology sectors. The government’s push for digital transformation in defense includes accelerated development of tactical UAVs and autonomous ground systems.

The Germany unmanned systems industry is propelled by the country's robust industrial foundation and steadfast dedication to research and development. The country prioritizes autonomous systems for military, industrial automation, and smart infrastructure applications. Federal funding boosts innovation in hybrid UAVs, unmanned ground vehicles, and collaborative robotics.

Asia Pacific Unmanned Systems Market Trends

The Asia Pacific unmanned systems industry is anticipated to register the highest CAGR of over 15% from 2026 to 2033, driven by escalating defense investments, increasing adoption of commercial drone technology in agriculture, logistics, and infrastructure monitoring, and government initiatives promoting indigenous manufacturing and technology innovation. The integration of AI and IoT enhances system capabilities, enabling sophisticated mission execution in surveillance, disaster management, and precision farming.

The Japan unmanned systems industry is gaining momentum, driven by Japan's strong industrial robotics base, precision agriculture applications for rice paddy monitoring and yield optimization, and advanced disaster response capabilities in earthquake-prone regions.

The China unmanned systems industry is witnessing robust expansion. China dominates the regional market with a robust manufacturing ecosystem led by major companies such as DJI. The government’s subsidies and investments accelerate R&D, fueling growth in commercial drones for agriculture and logistics as well as military unmanned platforms.

Key Unmanned Systems Company Insights

Some of the key players operating in the market are Lockheed Martin Corporation and Northrop Grumman Corporation among others.

-

Northrop Grumman Corporation is an aerospace and defense technology company that provides unmanned ground vehicles (UGVs) tailored for explosive ordnance disposal (EOD), route clearance, and tactical reconnaissance, ensuring troop safety in hazardous environments. Northrop Grumman’s unmanned solutions serve military, government, and commercial customers worldwide, supporting intelligence, surveillance, reconnaissance (ISR), logistics, combat, and multi-domain operations.

-

Lockheed Martin Corporation operates through four major business segments: Aeronautics, Rotary and Mission Systems, Missiles and Fire Control, and Space. Lockheed Martin has developed notable platforms such as the Stalker XE and the Indago quadrotor family. The company has contributed significantly to unmanned maritime solutions. Its Marlin autonomous underwater vehicle (AUV) has been developed for missions such as mine countermeasures, port and harbor security, and infrastructure inspection.

Some of the emerging players operating in the market include Elbit Systems Ltd., and Teledyne Technologies Incorporated, among others.

-

Elbit Systems Ltd. is a global defense electronics company that offers a comprehensive portfolio of unmanned aerial vehicles (UAVs) designed for intelligence, surveillance, reconnaissance (ISR), target acquisition, and tactical missions. Its UAVs range from small, portable tactical drones for rapid deployment to medium- and high-altitude long-endurance (MALE and HALE) platforms capable of persistent surveillance.

-

Teledyne Technologies Incorporated is a U.S.-based company that produces autonomous underwater vehicles (AUVs) and remotely operated vehicles (ROVs) that support a wide range of missions, from military applications such as mine countermeasures and anti-submarine warfare to commercial uses such as offshore energy inspection, environmental monitoring, and oceanographic research. The company also provides unmanned surface vehicle (USV) solutions and supports integration of its sensor technologies into broader autonomous maritime systems.

Key Unmanned Systems Companies:

The following key companies have been profiled for this study on the unmanned systems market.

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Teledyne Technologies Incorporated

- BAE Systems plc

- DJI

- Thales Group

- Israel Aerospace Industries

- Boeing

- General Dynamics Corporation

- Textron Inc.

- L3Harris Technologies Inc.

- Elbit Systems Ltd.

Recent Developments

-

In January 2026, Teledyne Technologies Incorporated delivered the first four GAVIA autonomous underwater vehicle (AUV) systems to Sweden's Defence Materiel Administration (FMV) as part of a multi-year framework agreement to modernize the Swedish Armed Forces' fleet with enhanced underwater surveillance capabilities.

-

In December 2025, Lockheed Martin Skunk Works announced the integration of XTEND's XOS operating system into its MDCX autonomy platform, enabling single-operator control of multiple unmanned aircraft system (UAS) classes for joint all-domain command and control (JADC2) missions.

-

In September 2025, the UK’s BAE Systems signed a 10-year agreement with Canadian firm Cellula Robotics to advance Herne, an autonomous submarine for military applications, with plans to deliver by the end of 2026. Herne features BAE Systems’ platform-agnostic autonomous control system and has been configured to provide militaries with a cost-effective solution for a range of missions.

Unmanned Systems Market Report Scope

Report Attribute

Details

Market size in 2025

USD 29.3 billion

Estimated market size in 2026

USD 32.4 billion

Projected market size by 2033

USD 67.6 billion

Growth rate

CAGR of 11.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million and CAGR from 2026 to 2033

Report Product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, Technology, Application and Region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Northrop Grumman Corporation; Lockheed Martin Corporation; Teledyne Technologies Incorporated; BAE Systems plc; DJI; Thales Group; Israel Aerospace Industries; Boeing; General Dynamics Corporation; Textron Inc.; L3Harris Technologies Inc.; Elbit Systems Ltd.

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Unmanned Systems Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global unmanned systems market based on type, technology, application, and region.

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Unmanned Aerial Vehicles

-

Small UAVs

-

Medium UAVs

-

Large UAVs

-

-

Unmanned Ground Vehicles

-

Wheeled

-

Tracked

-

Legged

-

Hybrid

-

-

Unmanned Sea Vehicles

-

Unmanned Underwater Vehicles (UUVs)

-

Unmanned Surface Vehicles (USVs)

-

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Semi-Autonomous

-

Remotely Operated

-

Fully Autonomous

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Military and Law Enforcement

-

Commercial

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

MEA

-

UAE

-

South Africa

-

Kingdom of Saudi Arabia (KSA)

-

-

Frequently Asked Questions About This Report

The unmanned aerial vehicles (UAVs) segment led with a 63% revenue share in 2025.

The semi-autonomous segment held the largest revenue share in 2025, while the fully autonomous segment is the fastest-growing.

The commercial segment held the largest revenue share in 2025.

The global unmanned systems market size was valued at USD 29.3 billion in 2025 and is estimated at USD 32.4 billion for 2026.

The global unmanned systems market is expected to grow at a CAGR of 11.1% from 2026 to 2033, reaching USD 67.6 billion by 2033.

North America dominated with a 44% revenue share in 2025.

Key players include Northrop Grumman Corporation; Lockheed Martin Corporation; Teledyne Technologies Incorporated; BAE Systems plc; DJI; Thales Group; Israel Aerospace Industries; Boeing; General Dynamics Corporation; Textron Inc.; L3Harris Technologies Inc.; Elbit Systems Ltd.

Key factors that are driving the market growth include integration of advanced AI and edge computing, diverse multi-domain applications, and advancements in AI, sensor fusion, & communication technologies.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.