- Home

- »

- Agrochemicals & Fertilizers

- »

-

Urea Market Size, Share, Trends, Global Report, 2026-2033GVR Report cover

![Urea Market (2026 - 2033)Report]()

Urea Market (2026 - 2033)

Size, Share & Trends Analysis Report By Form (Granular, Prilled, Liquid), By Application (Fertilizers, Industrial/Chemical), By End Use (Agriculture, Chemical, Automotive), By Region, And Segment Forecasts

Market Size, 2025

$73.5BMarket Estimate, 2026

$76.4BMarket Forecast, 2033

$97.1BCAGR, 2026–2033

3.5%Urea Market Summary

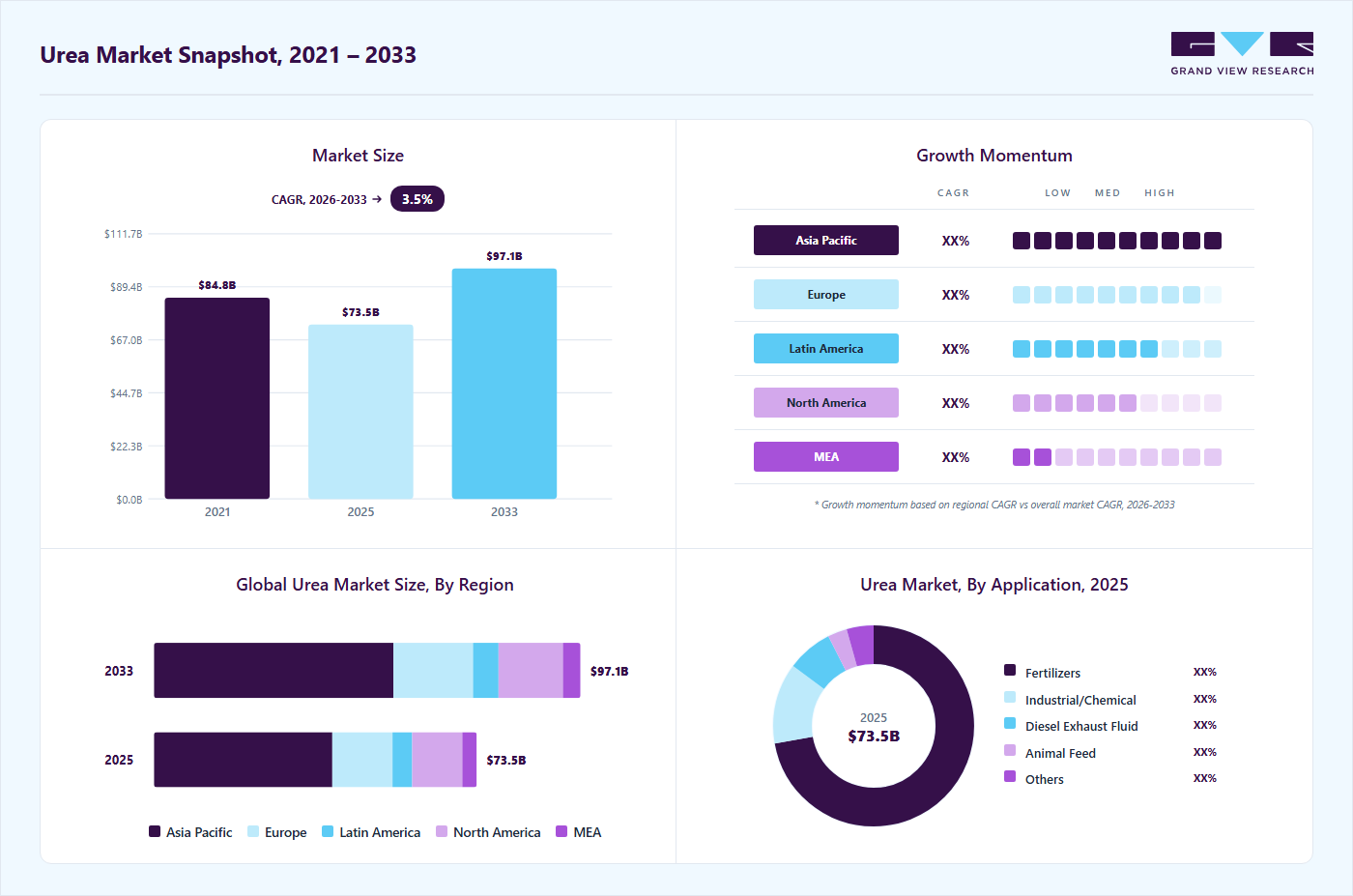

The global urea market size was valued at USD 73.5 billion in 2025 and is projected to grow from USD 76.4 billion in 2026 to USD 97.1 billion by 2033, at a CAGR of 3.5% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 55.1% in 2025. A major factor contributing to the growth of the urea market is the ongoing rise in global food demand. This demand is leading to a greater need for enhanced agricultural productivity and efficient nutrient management.

Key Market Trends & Insights

- By form: Granular segment held the largest market share of 66.0% in 2025.

- By application: Fertilizers segment held the largest market share of 72.1% in 2025.

- By end use: Agriculture segment held the largest market share of 75.1% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (55.1% revenue share, 2025)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 73.5 Billion

- Estimated market size in 2026: USD 76.4 Billion

- Projected market size by 2033: USD 97.1 Billion

- CAGR (2026-2033): 3.5%

As arable land remains to be limited, farmers are increasingly turning to cost-effective nitrogen fertilizers, such as urea, to maximize crop yields. This trend is expected to ensure a consistent demand for urea, supporting market expansion.

")

The market is presenting significant opportunities due to the ongoing shift towards sustainable and efficient enhanced fertilizers. This includes coated and slow-release urea variants that improve nutrient utilization and reduce environmental impact. Rapid industrialization and tightening global emission regulations are driving demand for Diesel Exhaust Fluid (DEF), creating a high-growth opportunity beyond traditional agricultural uses. Emerging markets in Africa and Southeast Asia are showing untapped potential, with increasing investments in agriculture and infrastructure. Advancements in green ammonia and low-carbon production technologies are opening new pathways for manufacturers to align with decarbonization goals while maintaining long-term competitiveness.

Despite strong growth prospects, the market faces notable challenges stemming from its heavy reliance on natural gas as a primary feedstock, making production costs highly sensitive to energy price volatility. Environmental concerns related to nitrogen runoff, soil degradation, and greenhouse gas emissions have led to stricter regulatory frameworks, potentially constraining usage patterns. In addition, market imbalances caused by geopolitical tensions, export restrictions, and supply chain disruptions can lead to price instability and uneven global availability. The increasing push toward alternative fertilizers and organic farming practices also poses a long-term competitive threat to conventional urea demand.

Market Dynamics

Urea is one of the most widely used nitrogen-based fertilizers globally owing to its high nitrogen content, cost-effectiveness, and broad applicability across multiple crops. Rapid population growth, shrinking arable land, and rising food consumption are driving the need for higher agricultural productivity worldwide. Rising demand for cereals, grains, fruits, and vegetables across emerging economies such as India, China, Brazil, and Indonesia is significantly supporting the consumption of urea fertilizers to enhance crop yield and soil nutrient efficiency.

The global agriculture industry is witnessing continuous expansion, supported by favorable government subsidies, increased focus on food security, and the growing adoption of advanced farming practices. In addition, rising pressure on farmers to improve crop productivity and maintain consistent agricultural output under changing climatic conditions is accelerating the use of nitrogen fertilizers such as urea. Expansion of commercial farming activities and increasing fertilizer application rates across developing agricultural economies are further expected to strengthen the growth of the global urea market over the forecast period.

Urea production is highly dependent on natural gas as a primary feedstock, making the market significantly vulnerable to fluctuations in natural gas prices and energy costs. Rising volatility in global energy markets, supply disruptions, and geopolitical uncertainties continue to impact urea production economics and profit margins for manufacturers. In addition, stringent environmental regulations on greenhouse gas emissions, nitrogen runoff, and excessive fertilizer use are increasing compliance pressure on fertilizer producers globally. Growing concerns regarding soil degradation, water contamination, and environmental sustainability are further encouraging the adoption of alternative nutrient management practices and organic farming solutions, which may restrain the long-term growth of the global urea market.

Market Concentration & Characteristics

The market exhibits a highly competitive and capacity-intensive structure, with participation from international corporations, regional manufacturers, and government-supported entities. While many producers operate globally, the market is not heavily consolidated, resulting in strong competition based on production scale, cost efficiency, and supply reliability. Key players such as Yara International ASA, CF Industries Holdings, Inc., Nutrien Inc., EuroChem Group AG, and Qatar Fertilizer Company benefit from integrated operations and large-scale production capabilities, which optimize costs and strengthen market positioning. Producers in regions with abundant natural gas resources, particularly the Middle East, maintain a significant competitive edge due to lower input costs, allowing them to serve global export markets efficiently.

Innovation, sustainability initiatives, and strategic expansion efforts increasingly influence competitive dynamics. Market participants are focusing on developing environmentally sustainable production processes, including low-emission and energy-efficient technologies, to comply with evolving regulatory standards and address environmental concerns. Companies are pursuing expansion strategies such as capacity enhancements, partnerships, and entry into emerging markets to secure long-term growth. The presence of state-owned and cooperative organizations, especially in developing economies, further impacts pricing structures and supply stability by prioritizing domestic agricultural needs. The competitive landscape is gradually shifting beyond price-based competition toward a more balanced approach that incorporates technological advancement, environmental responsibility, and global market reach.

Form Insights

Granular segment dominated the market, accounting for 66.0% of the total revenue share in 2025, primarily due to its superior physical properties and ease of application. Its larger particle size enhances handling, storage, and uniform field distribution, making it the preferred choice in large-scale agricultural operations. Granular urea is well-suited for blending and controlled release formulations, further supporting its widespread adoption. Strong demand from both developed and emerging agricultural economies continues to reinforce its leading position.

Prilled urea is expected to grow at the fastest CAGR of 3.8% from 2026 to 2033, driven by its cost-effectiveness and widespread availability. Although it is gradually being replaced by granular variants in some regions, prilled urea remains popular in price-sensitive markets due to its lower production cost and simpler manufacturing process. It is also widely used in industrial applications and smaller-scale farming, where handling requirements are less stringent. Continued demand from developing regions is expected to sustain its moderate growth trajectory.

Application Insights

Fertilizers segment represented the largest revenue share of 72.1% in 2025. This dominance is driven by the critical role of urea as a primary nitrogen source essential for crop productivity and soil fertility. Increasing global food demand, coupled with the adoption of intensive farming practices and supportive government policies, continues to drive consumption. The segment’s strong reliance on agriculture ensures consistent demand, making it the cornerstone of the urea market.

The diesel exhaust fluid (DEF) segment is expected to grow at the fastest CAGR of 3.9% from 2026 to 2033, supported by stringent emission regulations across major automotive markets. Urea-based DEF plays a crucial role in reducing nitrogen oxide emissions in diesel engines, making it indispensable for compliance with environmental standards such as Euro VI and equivalent norms. Rising vehicle production and increasing regulatory enforcement are key factors driving demand in this segment, positioning it as a significant growth avenue beyond agriculture.

End Use Insights

Agriculture dominated the end-use segment, accounting for 75.1% of the global urea market in 2025. The segment’s prominence is attributed to the extensive use of urea as a cost-efficient nitrogen fertilizer to enhance crop yields and support large-scale food production. Population growth, shrinking arable land, and the need for higher agricultural productivity continue to drive demand. Government subsidies and rural development initiatives further strengthen urea consumption in this sector.

The automotive segment is expected to grow at a CAGR of 3.9% during the forecast period, due to the increasing adoption of urea-based DEF in diesel vehicles. As emission standards become more stringent globally, the use of selective catalytic reduction (SCR) systems is becoming standard, thereby driving urea demand in the automotive sector. Growth in commercial vehicle fleets and regulatory compliance requirements is expected to sustain this upward trend, making automotive a key emerging end-use segment.

Regional Insights

Asia Pacific urea market dominated the global market, with a revenue share of 55.1% in 2025. This dominance is driven by a large agricultural base and high population density. Countries such as India and China heavily rely on urea to support intensive farming practices and ensure food security. Strong government subsidies, expanding irrigation infrastructure, and increasing fertilizer consumption continue to bolster regional demand. The rise in industrial applications and enhanced domestic production capacity further solidified the Asia Pacific’s leadership position in the global market.

Urea market in China represented one of the largest producers and consumers of urea globally, supported by its extensive agricultural activities and well-established chemical industry. The country benefits from significant domestic production capacity, enabling it to meet internal demand while also participating in export markets during surplus periods. Regulatory measures focused on environmental protection and energy efficiency have led to periodic production controls influencing global supply dynamics. China’s strategic focus remains on balancing food security needs with sustainable manufacturing practices.

North America Urea Market Trends

North America accounted for 15.5% of the global urea market in 2025. This growth is supported by extensive commercial agriculture and advanced farming technologies. The region benefits from relatively stable natural gas supplies, which allow for competitive domestic production. Besides agricultural demand, the increasing use of urea in industrial applications and diesel exhaust fluid (DEF) is also contributing to market expansion. The presence of major fertilizer producers and a well-developed supply chain enhance the stability of the regional market.

U.S. Urea Market Trends

The U.S. plays a key role in the North American urea market, primarily due to its substantial agricultural production and widespread use of modern farming techniques. Domestic production benefits from access to shale gas, which offers a cost advantage for manufacturing nitrogen fertilizers. There is a strong demand for Diesel Exhaust Fluid (DEF) because of strict emission standards in the transportation sector. However, fluctuations in supply and demand can lead to a reliance on imports to fulfill peak agricultural needs.

Europe Urea Market Trends

Europe accounted for 18.7% of the global urea market in 2025, benefiting from established agricultural practices and strong regulatory oversight. Demand in the region remains relatively stable, bolstered by advanced farming techniques and consistent use of fertilizers. However, strict environmental regulations and carbon reduction targets are prompting a gradual shift toward sustainable fertilizers and alternative nutrient solutions. The region is experiencing cost pressures from higher energy prices, which affect the competitiveness of domestic production.

Urea market in Germany plays a key role in the European urea market, driven by its advanced agricultural sector and strong chemical manufacturing base. The country emphasizes high-efficiency fertilizer usage and precision farming techniques, which influence demand patterns. Environmental regulations and sustainability targets are particularly stringent, encouraging the adoption of eco-friendly alternatives and optimized nutrient management practices. Germany’s market is also shaped by its reliance on imports due to limited domestic production capacity.

Middle East & Africa Urea Market Trends

The Middle East & Africa region plays a dual role in the global urea market as both a major production hub and an emerging consumption market. Middle Eastern countries benefit from abundant natural gas resources, enabling cost-efficient production and strong export competitiveness. In contrast, Africa represents a high-growth demand center due to increasing agricultural development and efforts to improve food security. The region’s strategic importance is expected to rise as investments in production capacity and agricultural modernization continue to expand.

Latin America Urea Market Trends

The Latin America is a growing market, supported by agricultural activities in countries such as Brazil and Argentina. The region’s increasing focus on export-oriented crops, including soybeans and corn, is driving fertilizer consumption. Limited domestic production capacity results in a high dependence on imports, making the market sensitive to global price fluctuations. Ongoing investments in agriculture and infrastructure are expected to sustain long-term demand growth.

Key Urea Company Insights

Companies in the global urea market are enhancing their competitive edge by increasing production capacities and securing long-term access to low-cost feedstock, particularly natural gas. This strategy aims to improve cost competitiveness. Many companies are also investing in sustainable technologies, such as low-carbon ammonia and efficiency-enhanced fertilizers, to comply with stricter environmental regulations and meet changing customer preferences. They are pursuing strategic partnerships, expanding into emerging markets, and integrating downstream operations to diversify revenue streams and ensure stable demand.

-

Yara International ASA is a leading global player in the urea market, known for its integrated production capabilities and extensive international distribution network. The company utilizes its strong presence in Europe, the Americas, Asia, and Africa to ensure a consistent supply and access to markets, especially in high-demand agricultural regions. Yara’s competitive advantage comes from its focus on operational efficiency, premium product offerings, and agronomic expertise, which allow it to provide value-added fertilizer solutions beyond basic commodity urea. In recent years, the company has also prioritized sustainability by investing in low-carbon ammonia and environmentally responsible production technologies, positioning itself as a leader in the transition to greener fertilizers.

-

OCI Global is a leading producer of nitrogen fertilizers, with a significant presence in the global urea market. The company operates strategically located production facilities in Europe, the Middle East, and North America, which provide access to cost-advantaged feedstock. OCI's vertically integrated business model enhances its operational resilience and cost competitiveness. OCI's portfolio includes ammonia and methanol, allowing the company to diversify its revenue streams while maintaining a strong position in nitrogen-based fertilizers. OCI is actively pursuing growth through capacity optimization and investments in clean energy solutions, such as low-carbon and blue ammonia projects. This approach aligns its long-term strategy with evolving environmental standards and global sustainability goals.

Key Urea Companies:

The following key companies have been profiled for this study on the urea market.

- EMR Claight

- Yara International ASA

- Indian Farmers Fertilisers Cooperative Limited

- PT Pupuk Kalimantan Timur

- Qatar Fertilizer Company

- National Fertilizers Limited

- EuroChem Group AG

- Saudi Arabian Fertilizer Company

- CF Industries Holdings, Inc.

- Nutrien Inc.

- Fazaz Global Concepts LLC

- Takasugi Pharmaceutical Co., Ltd.

- IBI Scientific

- OCI Global

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Yara International ASA; Indian Farmers Fertiliser Cooperative Limited; Qatar Fertilizer Company; EuroChem Group AG; Saudi Arabian Fertilizer Company; CF Industries Holdings, Inc.; Nutrien Inc.; OCI Global; PT Pupuk Kalimantan Timur; National Fertilizers Limited

- Focus on large-scale production expansion, backward integration, and long-term natural gas sourcing agreements to strengthen operational efficiency.

- Invest in sustainable fertilizer technologies, export network expansion, and strategic partnerships to enhance global market penetration.

- Possess strong global distribution networks, integrated manufacturing infrastructure, and large-scale production capacities across key agricultural regions.

- Benefit from established brand recognition, strong financial capabilities, and diversified fertilizer product portfolios supporting long-term market leadership.

- Face significant exposure to natural gas price volatility and stringent environmental regulations impacting production economics and profitability.

- High capital-intensive operations and dependency on agricultural subsidy structures may affect operational flexibility during market fluctuations.

Emerging Players: EMR Claight; Faraz Global Concepts LLC; Takasugi Pharmaceutical Co., Ltd.; IBI Scientific

- Focus on niche product offerings, regional distribution expansion, and customized fertilizer solutions targeting specific agricultural requirements.

- Emphasize partnerships with local distributors and cost-effective sourcing strategies to improve regional market visibility and competitiveness.

- Benefit from operational flexibility and faster responsiveness toward changing regional agricultural and customer requirements.

- Offer specialized products and localized business strategies tailored to regional farming practices and application needs.

- Operate with limited production capacities, lower global brand recognition, and comparatively smaller distribution networks than established players.

- Face challenges in securing large-scale investments and competing with multinational companies on pricing, technology, and supply chain capabilities.

Recent Developments

-

CF Industries Holdings, Inc. invested USD 2.3 billion in a new urea facility in the U.S., which focuses on enhancing domestic production and ensuring supply security

-

PT Pupuk Kalimantan Timur undertook a large-scale investment of USD 2 billion to develop an integrated urea, ammonia, and methanol plant in Indonesia, strengthening its production capabilities and regional supply position.

Urea Market Report Scope

Report Attribute

Details

Market size in 2025

USD 73.5 billion

Estimated market size in 2026

USD 76.4 billion

Projected market size by 2033

USD 97.1 billion

Growth rate

CAGR of 3.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Form, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; South Africa; Saudi Arabia.

Key companies profiled

EMR Claight; Yara International ASA; Indian Farmers Fertilisers Cooperative Limited; PT Pupuk Kalimantan Timur; Qatar Fertilizer Company; National Fertilizers Limited; EuroChem Group AG; Saudi Arabian Fertilizer Company; CF Industries Holdings, Inc.; Nutrien Inc.; Fazaz Global Concepts LLC; Takasugi Pharmaceutical Co. Ltd.; IBI Scientific; OCI Global

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Urea Market Report Segmentation

This report forecasts volume & revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global urea market report based on form, application, end use, and region:

-

Form Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Granular

-

Prilled

-

Liquid

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Fertilizers

-

Industrial/Chemical

-

Resins

-

Adhesives & laminates

-

Other Industrial/Chemical Applications

-

-

Diesel Exhaust Fluid

-

Animal Feed

-

Other Applications

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Agriculture

-

Chemical

-

Automotive

-

Construction

-

Other End Uses

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed regional analysis of urea demand and consumption patterns across specific to any region such as Asia Pacific, North America, Europe, Latin America, and Middle East & Africa, along with key country-level production and usage trends.

Identify high-growth and high-consumption regions to support expansion strategies, distribution planning, and market prioritization.

Pricing Analysis

Assessment of global urea pricing trends influenced by natural gas costs, seasonal agricultural demand, government subsidies, and import-export parity pricing across key producing and consuming regions.

Enable better pricing strategy development, margin optimization, and procurement planning by understanding cost drivers and price volatility.

Opportunity Assessment

Evaluation of emerging opportunities across precision farming, controlled-release fertilizers, and high-efficiency nitrogen solutions driven by productivity pressures and sustainability trends in agriculture.

Identify new revenue streams and innovation-driven segments to support long-term growth and product diversification strategies.

Frequently Asked Questions About This Report

The global urea market size was estimated at USD 73.5 billion in 2025 and is expected to reach USD 76.4 billion in 2026.

The global urea market is expected to grow at a compound annual growth rate of 3.5% from 2026 to 2033 to reach USD 97.1 billion by 2033.

Asia Pacific held the largest share of the global urea market in 2025, accounting for 55.1% of revenue, primarily due to its extensive agricultural base, high population-driven food demand, and strong government support for fertilizer usage. Large-scale domestic production and widespread adoption of intensive farming practices further reinforce the region’s market dominance.

Some of the key players operating in the urea market include EMR Claight, Yara International ASA, Indian Farmers Fertilisers Cooperative Limited, PT Pupuk Kalimantan Timur, Qatar Fertilizer Company, National Fertilizers Limited, EuroChem Group AG, Saudi Arabian Fertilizer Company, CF Industries Holdings, Inc., Nutrien Inc., Fazaz Global Concepts LLC, Takasugi Pharmaceutical Co., Ltd., IBI Scientific, OCI Global.

The urea market is primarily driven by rising global food demand, which is increasing the need for high-efficiency nitrogen fertilizers to enhance agricultural productivity. Expanding industrial applications and stricter emission regulations supporting diesel exhaust fluid usage are further contributing to market growth.

The granular segment led with a 66.0% revenue share in 2025, while the prilled urea segment is the fastest-growing.

The fertilizers segment led with a 72.1% revenue share in 2025, while the diesel exhaust fluid segment is the fastest-growing.

The agriculture segment led with a 75.1% revenue share in 2025, while the automotive segment is the fastest-growing.

About the Author(s)

Agrochemicals & Fertilizers Research Team

Bulk Chemicals · Agrochemicals & FertilizersThis report was authored by the agrochemicals & fertilizers research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the agrochemicals & fertilizers segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.