- Home

- »

- Animal Health

- »

-

Veterinary Diagnostics Market Size, Industry Report, 2033GVR Report cover

![Veterinary Diagnostics Market Size, Share & Trends Report]()

Veterinary Diagnostics Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Consumables, Reagents & Kits, Equipment & Instruments), By Animal (Companion Animals, Production Animals), By Testing Category, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$8.4BMarket Estimate, 2026

$9.3BMarket Forecast, 2033

$19.2BCAGR, 2026–2033

11.0%Veterinary Diagnostics Market Summary

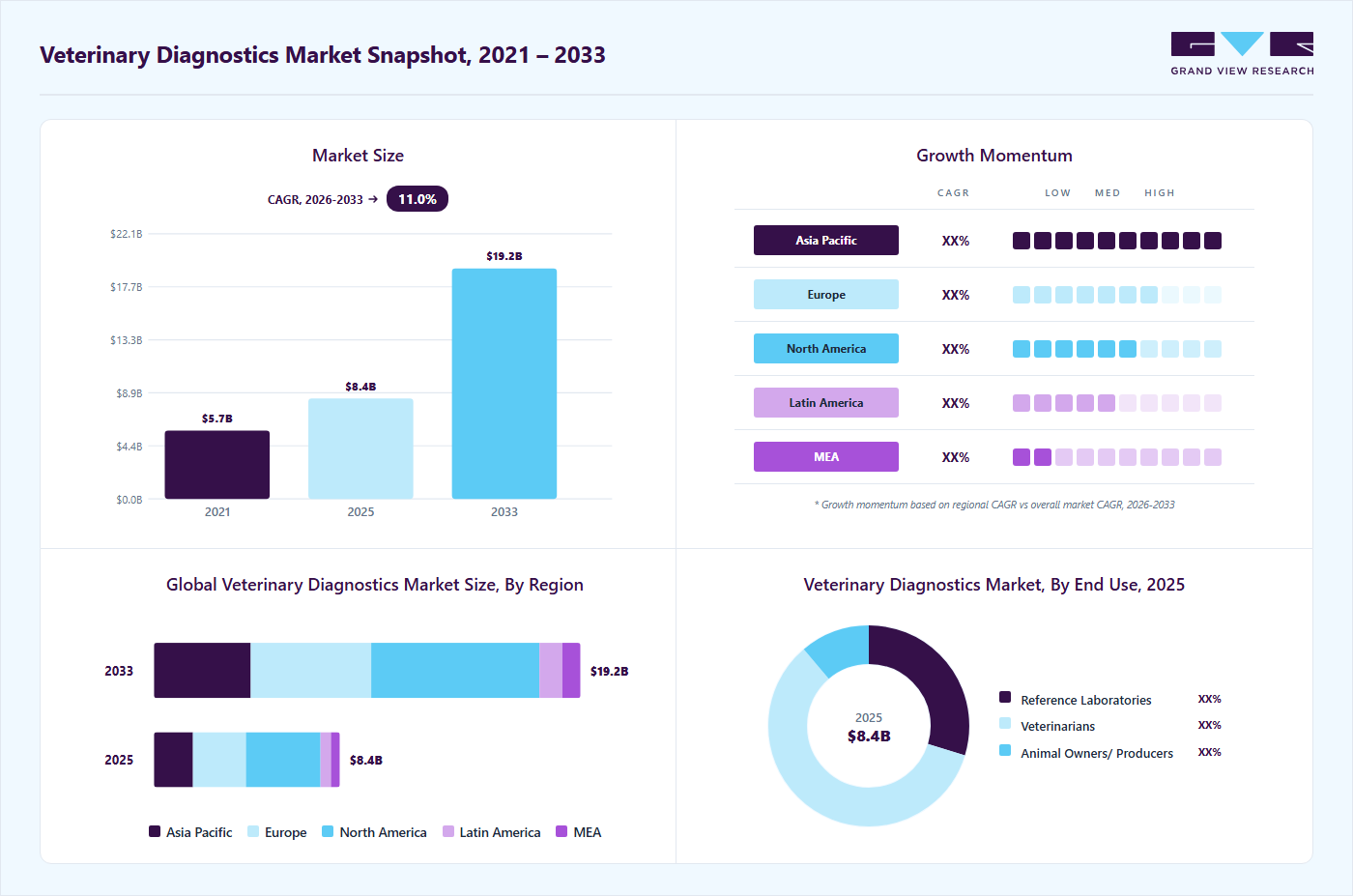

The global veterinary diagnostics market size was valued at USD 8.4 billion in 2025 and is projected to grow from USD 9.3 billion in 2026 to USD 19.2 billion by 2033, at a CAGR of 11.0% from 2026 to 2033. The North America veterinary diagnostics market held the largest share of 40.1% of the global market in 2025. The market is expanding steadily as pet adoption worldwide increases and owners allocate more spending toward routine veterinary examinations and preventive testing.

Key Market Trends & Insights

- By product: Consumables, reagents & kits segment held the largest share of 52.5% in 2025.

- By animal: Companion animal segment held the largest share in the market in 2025.

- By end use: Veterinarians segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (40.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. dominated the North America region with the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 8.4 Billion

- Estimated market size in 2026: USD 9.3 Billion

- Projected market size by 2033: USD 19.2 Billion

- CAGR (2026-2033): 11.0%

Routine blood work, screening panels, and early disease detection have become common components of companion animal care. In parallel, the continued occurrence of infectious and zoonotic diseases in livestock and pets is creating sustained demand for reliable diagnostic tools to support disease control, herd productivity, and food supply safety.")

Moreover, the need for faster, more streamlined diagnostic processes is driving growth in the veterinary diagnostics market. In many clinics, evaluating a pet’s health can take time, particularly where access to specialized clinical pathologists or parasitologists is limited. For instance, according to an article published by Zoetis in February 2026, veterinary practices in the United States collectively perform around 90 million fecal tests each year, reflecting the scale of routine diagnostic workload. Such high testing volumes are increasing interest in advanced in-clinic diagnostic systems that can shorten turnaround time, improve operational efficiency, and help veterinarians make timely treatment decisions, thereby contributing to greater adoption of modern diagnostic solutions.

Furthermore, broader adoption of structured clinical guidelines is increasing the use of detailed diagnostic workups in veterinary practice. For instance, according to an article published by AVMA, in February 2026, the American Veterinary Medical Association reported on a consensus statement from the American College of Veterinary Internal Medicine addressing chronic inflammatory enteropathy (CIE) in dogs. The document outlines a two-tier diagnostic pathway that recommends a stepwise evaluation, including detailed case history, use of standardized scoring indices such as CIBDAI and CCECAI, routine laboratory testing, imaging studies, and dietary trials before moving to invasive procedures. As clinics incorporate these recommendations into daily practice to improve case management and long-term monitoring, utilization of blood panels, fecal analysis, imaging, and related diagnostic services is likely to increase, contributing to the continued expansion of the veterinary diagnostics market.

In addition, ongoing advances in veterinary molecular testing the expanding the veterinary diagnostics market by improving the accuracy and timeliness of disease detection in both companion and production animals. Laboratory methods that analyze genetic material and protein markers are enabling veterinarians to identify infections and disorders earlier than with conventional techniques, supporting more targeted treatment decisions. For instance, in February 2026, BioVenic advanced this trend by expanding its veterinary molecular diagnostic development services, providing research teams with end-to-end technical support for new testing platforms. Efforts such as these are helping bring more precise and commercially viable molecular diagnostic tools to market, contributing to the continued growth of the sector.

")

Increased cross-border livestock trade and repeated transboundary disease incidents are influencing the global spread of Foot-and-Mouth Disease. For instance, according to an article published by Global Ag Media, in August 2025, data covering January 2024 to April 2025 show that serotype O accounted for the largest share of outbreaks at 67%, confirming its broad geographic presence. SAT 3 contributed 11% of cases, while SAT 1 and SAT 2 each represented 8%, indicating continued circulation of Southern African Territories strains beyond their historically endemic areas. Around 6% of cases remained untyped, reflecting pending or incomplete laboratory characterization. The overall pattern points to the dominance of serotype O alongside the persistent activity of SAT variants in the global FMD situation.

Market Dynamics

The global companion animal population continues to grow, driving demand for companion animal diagnostics for preventive care, disease detection, and routine health monitoring. Rising pet ownership, increasing pet humanization, and greater awareness regarding animal health are key growth drivers. Pets are also increasingly associated with mental and physical well-being benefits, including stress reduction and improved emotional health.

According to the American Pet Products Association (APPA), nearly 94 million U.S. households owned pets in 2024, compared to approximately 85 million in 2019. Similarly, the Pet Food Manufacturers' Association (PFMA) reported that over 57% of UK households owned pets in 2024. In Canada, the Canadian Veterinary Medical Association also reported sustained growth in dog and cat ownership.

Increasing expenditure on pet healthcare, expanding pet insurance coverage, and growing adoption of advanced veterinary diagnostic technologies are expected to further support market growth during the forecast period.

The presence of region-specific and zoonotic infectious diseases poses a significant challenge to the veterinary diagnostics market due to the complexity of disease surveillance, evolving pathogen strains, and limitations in diagnostic accessibility across developing regions. Several transboundary animal diseases, including Avian Influenza, Newcastle Disease, Nipah Virus Infection, and swine influenza, require continuous monitoring and rapid detection capabilities to prevent large-scale outbreaks.

Frequent emergence of new viral strains and uneven veterinary infrastructure, particularly in emerging economies, can limit timely diagnosis and disease management. In addition, the need for advanced molecular diagnostics, skilled professionals, and stringent biosecurity measures increases operational costs for veterinary healthcare providers and diagnostic laboratories.

Furthermore, recurring outbreaks of highly pathogenic diseases across livestock and companion animals place pressure on existing diagnostic capacities, especially in rural and underpenetrated markets, thereby restraining consistent market expansion.

Market Concentration & Characteristics

The veterinary diagnostics industry is highly fragmented, characterized by the presence of numerous public and private participants competing across regions and product segments. Companies enhance their market standing through sustained investments in research and development, expansion of distribution capabilities, and strategic collaborations with regional partners to widen geographic penetration. By integrating technological innovation with robust supply chains and localized service support, these companies are able to accelerate product launches, improve accessibility for end users, and sustain a strong competitive position within the industry.

The industry is characterized by a high degree of innovation. Companies are investing in R&D to introduce novel diagnostic technologies and improve existing ones. Innovations such as portable diagnostic devices, integration with information technology, and the development of more accurate and rapid diagnostic assays contribute to the dynamic nature of the market. Moreover, integrating artificial intelligence and machine learning in veterinary diagnostics is becoming more prevalent. These technologies assist in data analysis, pattern recognition, and predictive modeling, improving diagnostic accuracy and efficiency.

The industry is also witnessing a notable level of merger and acquisition (M&A) activities. Established companies engage in strategic partnerships or acquire smaller firms to expand their product portfolios, access new technologies, and strengthen their market presence. This trend aims to create synergies, streamline operations, and capitalize on complementary strengths. For instance, in October 2025, OR Technology Group acquired VetEquip Ltd., an Irish veterinary equipment provider. The deal boosts OR's European reach and multimodality imaging services in Ireland.

The industry operates under country-specific regulatory structures that govern product approval, quality standards, and commercialization. In the United States, certain veterinary diagnostic kits fall under the oversight of the U.S. Department of Agriculture through the Animal and Plant Health Inspection Service, while some devices may be regulated by the U.S. Food and Drug Administration. In Europe, regulatory supervision is coordinated through the European Medicines Agency along with national authorities. These frameworks ensure product safety and performance standards but can extend approval timelines and increase compliance costs for manufacturers.

Product substitutes in the sector include traditional clinical examination, empirical treatment without laboratory confirmation, and basic in-clinic testing methods such as microscopy or simple rapid kits. In cost-sensitive and rural settings, veterinarians and livestock owners often rely on visual assessment and symptomatic diagnosis rather than advanced molecular or automated diagnostic systems. These lower-cost alternatives can reduce demand for high-end diagnostic platforms, particularly where awareness, infrastructure, or reimbursement support is limited.

Companies in the veterinary diagnostic products industry often engage in regional expansion strategies to broaden their market presence. This involves entering new geographic markets to tap into emerging opportunities, reach a larger customer base, and address the specific needs of diverse regions. Adapting products and strategies to suit regional preferences, regulatory environments, and specific healthcare needs is crucial for successful regional expansion. This may involve customizing diagnostic products to meet the unique requirements and characteristics of different markets.

Product Insights

On the basis of product, consumables, reagents & kits segment held the largest revenue share of 52.51% in 2025 and is the fastest growing segment. Consumables, reagents, and diagnostic kits form the operational backbone of veterinary testing procedures, as they are required for the routine execution of laboratory and in-clinic analyses. These products are utilized across reference laboratories, veterinary hospitals, and point-of-care environments to perform a wide range of tests, including hematology, biochemistry profiling, urinalysis, serology, and immunoassay-based evaluations. The segment encompasses assay-specific reagents, control materials, calibrators, test strips, and single-use components that ensure accuracy and repeatability of results. Owing to their application across disease screening, infection detection, metabolic disorder assessment, and preventive health monitoring, these supplies generate recurring demand and represent a steady revenue stream within the veterinary diagnostics market.

The equipment & instruments segment is the second fastest growing segment over the forecast period. This is owing to technological advancements in diagnostic equipment, increasing adoption of point-of-care testing (POCT) devices, demand for imaging equipment, and investment in veterinary healthcare. For instance, in July 2024, EKF Diagnostics launched the Biosen C-Line, an advanced glucose and lactate analyzer designed for enhanced usability. It features a touch screen and advanced connectivity options to integrate seamlessly with hospital and lab IT systems via EKF Link. This benchtop analyzer provides highly precise glucose and lactate measurements, used in clinical settings for diabetes management and by elite sports teams for tracking lactate production in training.

Animal Insights

On the basis of animal, the companion animal segment dominated the market with the largest revenue share in 2025. The increasing reliance on clinical evidence in companion animal care is driving greater adoption of preventive and orthopedic diagnostics. For instance, according to an article published by BSAVA, in February 2026, A long-term study of over 20,000 dogs found a significant connection between cumulative gonadal hormone exposure and cranial cruciate ligament disease (CrCLD), with higher risk observed in dogs with lower hormone exposure, challenging earlier fixed gonadectomy timelines. Such findings are encouraging earlier orthopedic screening, expanded use of imaging, and biomarker-based risk assessment in dogs. As veterinarians and pet owners adopt structured preventive testing, diagnostic demand in the companion animal segment is expected to increase, supporting the segment's growth in the veterinary diagnostics market.

The production animals is the fastest growing segment over the forecast period. Strengthening technical expertise and laboratory capacity in livestock disease detection is supporting the market growth. Skill development initiatives improve the accuracy, speed, and adoption of advanced serological and molecular testing methods across poultry and livestock health management systems. For instance, the Joint Directorate of the Centre for Animal Disease Research and Diagnosis under the ICAR-Indian Veterinary Research Institute, India, organized a 10-day hands-on training program titled “Advances in Serological and Molecular Techniques for Diagnosis of Livestock and Poultry Diseases” from 13th to 22nd December 2025. Such programs enhance the capabilities of veterinarians and laboratory professionals in applying modern diagnostic tools, leading to wider testing adoption in cattle, poultry, and other farm animals, thereby increasing diagnostic volumes and supporting expansion of the production animal segment.

Testing Category Insights

On the basis of testing category, clinical chemistry segment dominated the market with largest revenue share in 2025, due to the growing use of routine blood and serum testing for evaluating organ function, metabolic balance, and chronic conditions in animals. These tests are widely used in preventive health checkups, pre-anesthetic screening, and ongoing disease management in companion animals. In livestock, biochemical profiling supports herd health monitoring and productivity assessment. Increased adoption of in-clinic analyzers and automated systems has improved testing efficiency and accessibility, leading to higher test volumes and steady segment growth.

The cytopathology is the fastest growing segment with highest CAGR over the forecast period, attributed to the increasing use of minimally invasive sampling techniques for evaluating tumors, infections, and inflammatory disorders. In companion animals, fine needle aspiration is routinely performed in dogs and cats to assess skin lumps such as mast cell tumors, lipomas, and mammary gland masses, while lymph node cytology is used to investigate lymphoma. Fluid cytology is also applied in cases of pleural or abdominal effusion to determine underlying causes. The growing incidence of cancer and age-related diseases in pets is contributing to higher demand for rapid cellular examination. In production animals, cytology supports reproductive assessment and disease investigation, further supporting segment growth.

End Use Insights

On the basis of end use, veterinarians dominated the market with the largest revenue share in 2025. This segment traditionally holds the largest market share because veterinarians play a central role in animal diagnosis, treatment, and overall healthcare. Veterinary professionals utilize various diagnostic tools and services, including imaging equipment, laboratory tests, and point-of-care diagnostic devices. The segment's dominance is driven by the reliance of animal owners on veterinarians for expert guidance and the comprehensive nature of the diagnostic services they offer.

Animal owners/ producers segment is the fastest-growing segment over the forecast period. This is due to the rising popularity of point-of-care testing (POCT) devices that allow on-site diagnostic testing. These devices enable quick and convenient testing at home or on the farm without the need to visit a veterinary clinic, making them attractive to animal owners and producers. For livestock owners and producers, diagnostic tools are crucial for managing herd health, optimizing production, and ensuring the safety of food products. The integration of diagnostics into on-farm practices enhances decision-making and contributes to overall farm management.

Regional Insights

North America dominated the market with largest revenue share of 40.08% in 2025. This is owing to established veterinary healthcare infrastructure, advanced technology adoption, high disposable income, and the presence of key players. Strategic initiatives undertaken by these companies are expected to continue fueling regional market growth. For instance, in September 2025, IMV Imaging has entered into a partnership with Asto CT to integrate IMV’s ultrasound, X-ray, CT, and MRI portfolio with Asto’s Equina standing CT scanner designed for horses. The collaboration is aimed at supporting equine and mixed veterinary practices globally by expanding access to advanced imaging solutions.

U.S. Veterinary Diagnostics Market Trends

The veterinary diagnostics market in the U.S. accounted for the highest market share in the North America market. Expanding access to advanced imaging technologies is expected to support growth of the veterinary diagnostics market in the United States. For instance, in January 2026, Adaptix Ltd has entered into a distribution partnership with Centura Imaging to introduce the Adaptix VetSA3D system into the U.S. market, improving availability of low-dose 3D X-ray imaging for veterinary applications. Wider distribution of such systems can enhance diagnostic precision in orthopedic and complex cases, encourage adoption of advanced imaging in veterinary practices, and contribute to higher imaging procedure volumes across the country.

The Canada Veterinary Diagnostics market is expected to grow at a significant CAGR during the forecast period. Growth of AI-enabled imaging solutions is expected to increase diagnostic efficiency and test volumes in Canada’s veterinary sector. For instance, in July 2024, SK Telecom introduced its AI-based veterinary diagnosis platform, X Caliber, in Canada, with plans to roll it out across more than 100 pet hospitals nationwide. The tool assists veterinarians in interpreting X-ray images of dogs and cats more quickly and accurately, supporting faster clinical decisions. With Canada’s large companion animal population, estimated at 28 million pets, wider deployment of such technology is likely to enhance imaging adoption, improve workflow in clinics, and contribute to growth of the veterinary diagnostics market in the country.

Europe Veterinary Diagnostics Market Trends

The Veterinary Diagnostics market in Europe is growing steadily, driven by the expanding animal welfare regulations and structured disease control programs across the region The European Union’s coordinated surveillance measures for transboundary and zoonotic diseases in livestock are increasing routine herd-level testing and laboratory monitoring. At the same time, high companion animal ownership, widespread preventive care practices, and strong penetration of pet insurance in Western European countries are contributing to greater use of blood screening, molecular diagnostics, and imaging services. Well-developed veterinary networks and access to advanced laboratory infrastructure further sustain diagnostic demand across the region.

The Veterinary Diagnostics market in UK is expected to grow significantly over the forecast period. Adoption of advanced imaging systems is strengthening the growth of the veterinary diagnostics market in the UK by improving diagnostic precision and clinical efficiency. For instance, in April 2025, Lumbry Park Veterinary Specialists, part of CVS Group, became the first practice in the country to install the MAGNETOM Flow.Ace MRI system from Siemens Healthineers, enhancing image quality while significantly reducing helium consumption. The system enables faster scans, smoother workflow, and shorter anesthesia time for pets, which can increase case throughput and encourage wider use of advanced imaging. Such investments support higher diagnostic volumes and contribute to expansion of the UK veterinary diagnostics market.

A veterinary diagnostics market in Germany grow at a steady rate over the forecast period. Strong regulatory focus on animal health monitoring and well-established veterinary infrastructure are supporting growth of the veterinary diagnostics market in Germany. Strict disease surveillance programs in livestock, particularly for dairy and swine herds, are increasing routine screening and laboratory testing volumes. In addition, high pet ownership rates and structured preventive care practices across small animal clinics are contributing to steady demand for blood testing, imaging, and specialized diagnostics, driving market expansion in the country.

Asia Pacific Veterinary Diagnostics Market Trends

Asia Pacific is expected to grow at the fastest CAGR over the forecast period, driven by rising pet ownership, increased awareness of pet health, and a growing demand for breed identification and genetic insights. In countries like Japan and Australia, pet owners are increasingly investing in DNA tests to monitor health risks and hereditary conditions. In addition, the expansion of e-commerce platforms in the region has made veterinary diagnostics testing kits more accessible. Market growth in the region can be attributed to a significantly large cattle population. For instance, China & India constitute more than 30% of the global cattle population.

The Veterinary Diagnostics market in Japan is witnessing a lucrative growth over the forecast period. An aging pet population and rising demand for advanced companion animal care are driving veterinary diagnostics growth in Japan. With a significant proportion of dogs and cats entering senior age groups, there is increasing need for regular health screening, chronic disease monitoring, and oncology diagnostics. The presence of technologically advanced veterinary hospitals and growing adoption of in-clinic analyzers and imaging systems are further supporting higher diagnostic utilization across urban centers.

The market for veterinary diagnostics in India is expected to grow significantly over the forecast period. Rising adoption of pet insurance in India is expected to increase demand for veterinary diagnostics by improving affordability and encouraging timely medical intervention. As urban pet ownership grows and animals are increasingly regarded as family members, spending on advanced veterinary care, including laboratory testing and imaging, is rising. For instance, according to an article published by CNBC TV 18, in February 2026, Industry leaders such as Pratik Sheth of Barker and Meowsky have noted a clear shift toward structured financial protection for pets. With insurance coverage reducing out-of-pocket burden, pet owners are more likely to opt for routine screenings, preventive diagnostics, and early disease detection, thereby supporting expansion of the veterinary diagnostics market in India.

Latin America Veterinary Diagnostics Market Trends

The Latin American Veterinary Diagnostics market is experiencing significant growth, driven by rising pet ownership and increased awareness of animal health and genetics. The demand for animal protein is increasing in Latin America, expanding the livestock industry. This has resulted in a greater need for accurate and rapid disease diagnosis to ensure animal health and prevent disease outbreaks. In addition, Latin America has experienced outbreaks of various animal diseases, such as Foot-and-Mouth Disease, Avian Influenza, and Porcine Reproductive and Respiratory Syndrome (PRRS). The need for accurate and rapid diagnosis of these diseases drives market growth.

Brazil Veterinary Diagnostics market is projected to grow at a significant CAGR during the forecast period, as there is an increase in pet ownership, advancements in diagnostic technologies, and rising awareness of animal health. Growth in livestock farming and government initiatives to combat zoonotic diseases further support market expansion. In Brazil, high mortality rates among beef cattle due to infectious diseases underscore the urgent demand for skilled veterinary professionals proficient in molecular diagnostics. This necessity addresses significant financial losses and supports market growth in one of the world's leading beef-producing nations.

Middle East & Africa Veterinary Diagnostics Market Trends

The Veterinary Diagnostics market in MEA is witnessing significant growth, driven by rising pet adoption rates and increasing awareness about animal health. Growing investment in veterinary healthcare infrastructure and the adoption of advanced diagnostic technologies are also expected to boost market growth. For instance, countries like South Africa and the UAE are leading the adoption with increased spending on veterinary services and diagnostic tools, reflecting the region's evolving healthcare landscape.

South Africa Veterinary Diagnostics market is observing significant growth driven by increased product launches from domestic players. Companies are introducing innovative testing solutions tailored to local pet owners' needs. For instance, the launch of breed identification and health screening tests by local firms like EasyDNA South Africa and International Biosciences South Africa has expanded consumer access to affordable genetic testing options. These products help identify breed composition and screen for potential genetic health risks, empowering pet owners to make informed care decisions. This surge in domestic offerings fosters competition and enhances market awareness, ultimately driving growth in the veterinary diagnostics sector across South Africa.

UAE Veterinary Diagnostics market is strengthened by rising investment in advanced veterinary infrastructure and increasing pet ownership among expatriate and high-income populations The expansion of modern veterinary hospitals in cities such as Dubai and Abu Dhabi has improved access to in-clinic laboratory testing, diagnostic imaging, and preventive health screening. In addition, strong government focus on livestock disease monitoring and biosecurity, particularly in poultry and camel farming, is increasing routine surveillance testing. Growing awareness of preventive pet healthcare and demand for high-quality veterinary services are further supporting diagnostic adoption across the country.

Key Veterinary Diagnostics Company Insights

The market is characterized by the presence of several large, medium, to small companies. Some of the key players operating in the market include IDEXX Laboratories, Inc.; Zoetis; Antech Diagnostics, Inc. (Mars Inc.); and Agrolabo S.p.A. Market players often engage in collaborations and partnerships with veterinary clinics, research institutions, and academic organizations. These collaborations aim to enhance research and development efforts, share knowledge, and expand the reach of diagnostic products in the veterinary healthcare ecosystem. Market players are also increasingly expanding their geographical presence to tap into emerging markets and capitalize on the growing awareness of veterinary diagnostics.

Key Veterinary Diagnostics Companies:

The following key companies have been profiled for this study on the veterinary diagnostics market.

- IDEXX Laboratories, Inc.

- Zoetis

- Antech Diagnostics, Inc. (Mars Inc.)

- Agrolabo S.p.A.

- Embark Veterinary, Inc.

- Esaote SPA

- Thermo Fisher Scientific, Inc.

- Innovative Diagnostics SAS

- Virbac

- FUJIFILM Corporation

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Zoetis Inc.

- Focus on R&D to launch novel diagnostic platforms with advanced technologies.

- Prioritize long-term relationships through excellent service, technical support, and responsive after-sales engagement.

- Enhanced positioning via product diversification and AI integration.

- Extensive distribution networks, regulatory expertise, and strong brand recognition in both companion and food animal segments.

- Price erosion due to intensifying competition.

- Regulatory complexity regarding AI-driven diagnostics.

- Vulnerability to lower-cost competitive alternatives in the point-of-care segment.

Emerging Players: Thermo Fisher Scientific, Inc.

- Actively expanding veterinary diagnostics and imaging portfolios.

- Pursuing strategic agreements for shared ownership of innovative technologies.

- Robust internal R&D programs and an expanding global footprint.

- Capturing "white-space" opportunities in livestock, specifically affordable, field-deployable PCR solutions.

- Modest R&D capabilities compared to incumbents, slowing the pace of new assay development.

- Underdeveloped regulatory infrastructure, creating barriers to entry in the US and EU markets.

Recent Developments

-

In September 2025, IMV Imaging and Asto CT formed a partnership to combine IMV's ultrasound, X-ray, CT, and MRI tools with Asto's Equina standing CT scanner for horses. The deal targets equine and mixed practices worldwide.

-

In April 2025, The Equine Analytical Chemistry Laboratory at the University of Kentucky has been acquired by Eagle Diagnostics. The facility will now operate under the new name Equine Integrity and Anti-Doping Sciences (EQIAS) Labs. Under its new ownership, the lab will maintain its prominent role in anti-doping testing for the equine and competitive animal sectors, while also broadening its scope for research advancements and innovation initiatives.

-

In November 2025, Zoetis Inc. acquired Veterinary Pathology Group (VPG), a prominent veterinary diagnostics laboratory network operating across the UK and Ireland. This strategic move strengthens Zoetis’ diagnostics portfolio and highlights its continued focus on enhancing animal health through advanced, high-quality diagnostic services and solutions.

-

In September 2024, Zoetis Inc. introduced Vetscan OptiCell, a new cartridge-based hematology analyzer that employs AI-powered technology to deliver precise Complete Blood Count (CBC) analysis at the point of care, offering lab-quality results with time, cost, and space efficiencies for veterinary clinics.

Veterinary Diagnostics Market Report Scope

Report Attribute

Details

Market size in 2025

USD 8.4 billion

Estimated market size in 2026

USD 9.3 billion

Projected market size by 2033

USD 19.2 billion

Growth rate

CAGR of 11.0% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Billion/Million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, Testing Category, Animal, End Use, and Regional

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Thailand; South Korea; Australia; Brazil; Argentina; South Africa; UAE; Saudi Arabia; Kuwait; Qatar; Oman

Key companies profiled

IDEXX Laboratories, Inc.; Zoetis; Antech Diagnostics, Inc. (Mars Inc.); Agrolabo S.p.A.; Embark Veterinary, Inc.; Esaote SPA; Thermo Fisher Scientific, Inc.; Innovative Diagnostics SAS; Virbac; FUJIFILM Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Veterinary Diagnostics Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the veterinary diagnostics market report based on product, testing category, animal, end use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumables, Reagents & Kits

-

Equipment & Instruments

-

-

Animal Outlook (Revenue, USD Million, 2021 - 2033)

-

Companion Animals

-

Dogs

-

Cats

-

Horses

-

Other Companion Animals

-

-

Production Animals

-

Cattle

-

Poultry

-

Swine

-

Other Production Animals

-

-

-

Testing Category Outlook (Revenue, USD Million, 2021 - 2033)

-

Clinical Chemistry

-

Microbiology

-

Parasitology

-

Histopathology

-

Cytopathology

-

Hematology

-

Immunology & Serology

-

Imaging

-

Molecular Diagnostics

-

Other Categories

-

-

Veterinary Diagnostics Market by End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Reference Laboratories

-

Veterinarians

-

Animal Owners/ Producers

-

-

Veterinary Diagnostics Market by Region Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

UAE

-

Saudi Arabia

-

Kuwait

-

Qatar

-

Oman

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Investor & Go-to-Market Intelligence

Customized market sizing, competitive landscape mapping, and demand analysis tailored to support startup pitch decks, investor due diligence, and commercial entry planning across selected veterinary diagnostics segments.

Equips startups and their backers with credible, data-backed market narratives; strengthens fundraising positioning; and provides a clear view of addressable opportunity, competitive white spaces, and optimal go-to-market pathways.

Diagnostic Kits - Scope-Defined Segmentation

Customized report scoped exclusively to veterinary diagnostic kits, defined to include reagent kits, rapid test kits, ELISA kits, PCR kits, and other packaged assay formats - excluding standalone instruments, analyzers, and software platforms. Scope boundaries clearly documented and aligned with client expectations prior to delivery.

Ensures full alignment between client intent and research coverage; eliminates ambiguity around product classification; and delivers a focused, actionable view of the kits market across relevant segments, species, and geographies.

Regional Segmentation - Species & Disease Specific

Dedicated market analysis for infectious disease diagnostics in pigs and bovines across Brazil and broader LATAM, covering market size and forecast, disease prevalence and testing demand, regulatory environment, distribution landscape, key competitors, and country-level breakdown across priority geographies.

Enables precise regional entry or expansion planning; supports product and portfolio prioritization by species and disease area; and helps clients benchmark Brazil against the wider LATAM opportunity to allocate commercial resources effectively.

Frequently Asked Questions About This Report

The global veterinary diagnostics market is expected to grow at a CAGR of 11.0% from 2026 to 2033, reaching USD 19.2 billion by 2033.

North America dominated with a 40.1% revenue share in 2025. This is owing to established veterinary healthcare infrastructure, advanced technology adoption, presence of key companies, and high disposable income.

Key players include IDEXX Laboratories, Inc.; Zoetis; Antech Diagnostics, Inc. (Mars Inc.); Agrolabo S.p.A.; Embark Veterinary, Inc.; Esaote SPA; Thermo Fisher Scientific, Inc.; Innovative Diagnostics SAS; Virbac; FUJIFILM Corporation.

Key factors that are driving the veterinary diagnostics market growth include increased expenditure on animal health, rising incidence of diseases in animals, advancements in diagnostics, and increasing medicalization rate.

The global veterinary diagnostics market size was valued at USD 8.4 billion in 2025 and is estimated at USD 9.3 billion for 2026.

Asia Pacific is the fastest-growing region over the forecast period.

The consumables, reagents & kits led with a 52.5% revenue share in 2025, while equipment & instruments is the fastest-growing product.

The companion animal segment held the largest revenue share in 2025, while production animals is the fastest-growing segment.

The clinical chemistry segment held the largest revenue share in 2025, while cytopathology is the fastest-growing category.

Veterinarians segment held the largest share in 2025, while animal owners/producers is the fastest-growing segment.

About the Author(s)

Animal Health Research Team

Healthcare · Animal HealthThis report was authored by the animal health research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the animal health segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.