- Home

- »

- Advanced Interior Materials

- »

-

Lignin Market Size, Share & Growth, Industry Report, 2033GVR Report cover

![Lignin Market Size, Share & Trends Report]()

Lignin Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Ligno-sulphonates, Kraft, Soda, Organosolv, Hydrolyzed), By Application (Construction Material, Transportation Fuel, Biopolymer), By Region, And Segment Forecasts

Market Size, 2025

$1.3BMarket Estimate, 2026

$1.4BMarket Forecast, 2033

$2.0BCAGR, 2026–2033

5.2%Lignin Market Summary

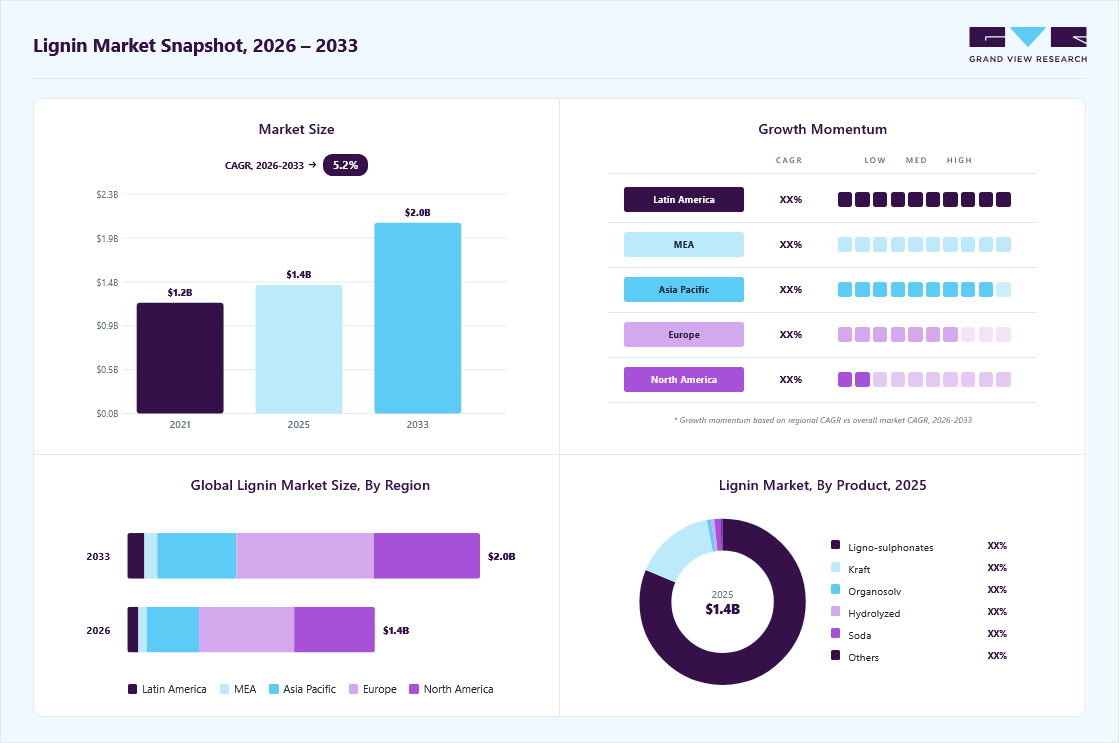

The global lignin market size was estimated at USD 1.37 billion in 2025 and is projected to reach USD 2.04 billion by 2033, growing at a CAGR of 5.2% from 2026 to 2033. The increasing demand for bio-based and sustainable materials in industries such as chemicals, packaging, and construction is driving the use of lignin as a renewable alternative to petroleum-based products.

Key Market Trends & Insights

- Europe dominated the global lignin market with the largest revenue share of 38.5% in 2025.

- The lignin industry in the Latin America is expected to grow at the fastest CAGR of 6.4% during the forecast period.

- By product, the kraft segment is projected to register at the fastest CAGR of 5.3% from 2026 to 2033.

- By application, the vanillin segment is forecast to witness at the fastest CAGR of 6.3% during the forecast period.

Market Size & Forecast

- 2025 Market Size: USD 1.37 Billion

- 2033 Projected Market Size: USD 2.04 Billion

- CAGR (2026-2033): 5.2%

- Europe: Largest market share in 2025

- Latin America: Fastest growing market

In addition, the growing pulp and paper industry is increasing the availability of lignin as a by-product during the processing of Cellulose, supporting its use in applications such as adhesives, dispersants, and biofuels.Industries are increasingly seeking renewable alternatives to petroleum-derived chemicals due to environmental concerns and regulatory pressures to reduce carbon emissions. Lignin, which is abundantly available as a by-product of the pulp and paper industry, has emerged as a promising raw material for producing bio-based chemicals, resins, adhesives, and carbon materials. As companies move toward circular economy models and sustainable sourcing, lignin is gaining attention as a valuable resource that can replace fossil-based ingredients in multiple industrial applications.

The lignin industry is also benefiting from the expansion of the pulp and paper industry, which generates significant quantities of lignin during the processing of wood into pulp. Traditionally, most lignin has been used as a low-value fuel within paper mills, but advancements in biorefinery technologies are enabling its conversion into high-value products such as dispersants, binders, and phenol substitutes. This shift toward lignin valorization is encouraging pulp producers to commercialize lignin extraction and processing technologies, thereby increasing its availability in the market and supporting the growth of lignin-based product applications across various industries.

")

The increasing demand for bio-based chemicals and advanced materials is also contributing to market growth. Lignin’s complex aromatic structure makes it a suitable feedstock for producing renewable chemicals, polymers, and carbon fibers used in automotive, construction, and energy storage applications. Researchers and manufacturers are exploring lignin-based alternatives to petrochemical compounds in coatings, polyurethane foams, and thermoplastics. As innovation in materials science continues to advance, lignin is expected to play an important role in developing sustainable performance materials with a lower environmental impact.

Furthermore, government policies promoting renewable resources and waste valorization are strengthening the lignin industry. Many countries are supporting the development of bio-based industries through funding programs, carbon-reduction targets, and regulations that encourage the use of renewable raw materials. For example, initiatives under the European Commission and programs such as the U.S. Department of Energy Bioenergy Technologies Office are encouraging research into lignin-derived products and integrated biorefineries. These policy frameworks are accelerating commercialization efforts and encouraging investment in lignin-processing technologies, thereby driving long-term market expansion.

Market Concentration & Characteristics

The lignin industry is closely linked to the pulp and paper sector, as lignin is primarily produced as a by-product of wood pulping processes, such as the Kraft process. This means the supply of lignin largely depends on global pulp production rather than dedicated lignin manufacturing. Large pulp mills generate significant volumes of lignin during the separation of cellulose from wood, making the industry highly resource-efficient and closely integrated with existing forestry and paper value chains.

The lignin industry is also technology-driven, as lignin has a complex chemical structure that varies depending on biomass sources and processing methods. Converting it into high-performance materials requires advanced processing and modification technologies. Continuous research in polymer science, green chemistry, and biorefinery technologies is enabling the development of lignin-based materials for applications in plastics, coatings, adhesives, and carbon materials, expanding the commercial potential of lignin across multiple industries.

Recent innovations highlight how the lignin industry is evolving toward bio-based plastic alternatives. For example, in May 2025, the Swedish greentech company Lignin Industries raised around USD 4.5 billion to scale up production of its lignin-derived thermoplastic, Renol, designed to replace fossil-fuel-based plastics. The company has also collaborated with Hellyar Plastics to develop applications in consumer electronics, home accessories, appliances, and construction. Such developments demonstrate that lignin-based materials can deliver performance comparable to conventional plastics while reducing carbon emissions, reinforcing the industry’s role in advancing sustainable materials.

Product Insights

The ligno-sulphonates segment led the market with the largest revenue share of 81.1% in 2025 and is projected to grow at the fastest CAGR during the forecast period. This dominance is due to its large-scale production from the sulfite pulping process and its wide use as dispersants, binders, and additives in industries such as construction, agriculture, and animal feed. Their cost-effectiveness, high water solubility, and strong dispersing properties make them widely preferred for applications such as concrete admixtures and dust suppressants, leading to significantly higher commercial adoption than other lignin types.

The Kraft lignin segment is anticipated to grow at a significant CAGR during the forecast period, due to its high purity, strong aromatic structure, and suitability for high-value applications such as bio-based resins, carbon fibers, and advanced materials. Increasing investments in lignin valorization and biorefinery technologies are enabling pulp producers to extract and commercialize kraft lignin for use as a sustainable alternative to petroleum-based chemicals, driving its market growth.

Application Insights

The dispersants segment led the market with the largest revenue share of 20.5% in 2025, due to the extensive use of lignin-based dispersants, particularly lignosulfonates, in industries such as concrete admixtures, ceramics, dyes, and agrochemicals. These dispersants improve particle dispersion, reduce water consumption, and enhance processing efficiency, making them cost-effective additives in large-volume industrial applications. Their strong demand in the construction and chemical sectors significantly contributes to the segment’s leading market share.

The vanillin segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the use of lignin as a renewable raw material for producing bio-based vanillin. Lignin-derived vanillin is widely utilized in the food & beverage, fragrance, and pharmaceutical industries as a flavoring and aromatic compound. Growing demand for sustainable and natural alternatives to petrochemical-based vanillin is further supporting the growth of this segment.

Regional Insights

Europe dominated the global lignin market with the largest revenue share of 38.5% in 2025, driven by its well-established pulp and paper industry and strong emphasis on bio-based and sustainable chemicals. Countries such as Finland, Sweden, and Germany host major pulp mills that generate large volumes of lignin as a by-product, supporting its commercialization across applications such as dispersants, binders, and bio-based chemicals. In addition, strict environmental regulations and the region’s push toward a circular bioeconomy are encouraging the utilization of lignin as a renewable alternative to petroleum-based materials, thereby strengthening market growth in Europe.

North America Lignin Market Trends

The lignin market in the North America is anticipated to grow at a significant CAGR during the forecast period, due to the presence of a large pulp and paper industry and increasing investments in bio-based chemicals and sustainable materials. The U.S. and Canada generate substantial quantities of lignin as a by-product of kraft pulping, which supports its use as a dispersant, binder, and bio-based chemical. In addition, strong research initiatives and government support for renewable materials and bio-refinery technologies are accelerating the commercialization of lignin-based products across various industries.

Asia Pacific Lignin Market Trends

The lignin marketin theAsia Pacific is emerging as a key region in the global market, driven by rapid industrialization, expanding construction activities, and growing demand for cost-effective additives across sectors such as concrete, ceramics, and agrochemicals. Countries such as China, India, and Japan are witnessing increasing consumption of lignin-based dispersants and binders driven by infrastructure development and a growing chemical manufacturing base. In addition, the expansion of the pulp and paper industry and rising interest in bio-based materials are supporting the regional growth of the lignin industry.

Latin America Lignin Market Trends

The lignin market in Latin America is anticipated to grow at the fastest CAGR during the forecast period, supported by the strong pulp and paper industries in countries such as Brazil, Chile, and Argentina. These countries generate significant quantities of lignin as a by-product from wood processing, enabling its use in applications such as concrete additives, animal feed binders, and agrochemical dispersants. In addition, increasing infrastructure development and the region’s expanding agricultural sector are contributing to the steady demand for lignin-based products.

Key Lignin Company Insights

The competitive environment of the lignin industry is moderately consolidated, with major players focusing on expanding production capacity, developing high-value lignin derivatives, and strengthening partnerships with end-use industries such as construction, chemicals, and agriculture. Leading companies such as Borregaard AS, UPM, Stora Enso, and Domtar Corporation leverage their strong pulp and paper manufacturing base to ensure a consistent supply of lignin and invest in R&D to develop bio-based alternatives to petroleum-derived chemicals. At the same time, emerging players and technology firms are focusing on lignin valorization technologies, specialty chemicals, and sustainable materials to gain a competitive edge in the evolving bioeconomy market.

Key Lignin Companies:

The following key companies have been profiled for this study on the lignin market.

- Stora Enso

- West Fraser Timber Co.

- UPM

- Sweetwater Energy

- Borregaard LignoTech

- Rayonier Advanced Material

- Domsjo Fabriker

- Changzhou Shanfeng Chemical Industry Co Ltd

- Domtar Corporation

- Nippon Paper Industries Co., Ltd

- Metsa Group

- The Dallas Group of America, Inc.

- Liquid Lignin Company

- Burgo Group S.p.A

- Valmet Corporation

Recent Developments

-

In February 2026, Metsä Group launched a demo plant in Äänekoski, Finland, to produce Metsä LigO, a lignin-based product derived from bioproduct mill side streams, with a capacity of two tons per day. Developed with ANDRITZ and in partnership with Dow, the project aims to validate lignin applications, including bio-based additives for construction and packaging. If successful, the company plans to scale up to a full commercial plant to support the circular economy and sustainable material development.

-

In January 2026, Lignin Industries launched Renol TPV, a bio-based thermoplastic elastomer made with 70% lignin-derived Renol and 30% elastomer additives. The material can reduce CO₂ emissions by up to 50% compared to fossil-based TPVs while offering strong oil resistance, full recyclability, and compatibility with existing manufacturing processes. It is suitable for applications such as seals, bellows, grips, and protective covers.

Lignin Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 1.43 billion

Revenue forecast in 2033

USD 2.04 billion

Growth rate

CAGR of 5.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Spain; Italy; China; India; Japan; Indonesia; Malaysia; Brazil; South Africa

Key companies profiled

Stora Enso; West Fraser Timber Co.; UPM; Sweetwater Energy; Borregaard LignoTech; Rayonier Advanced Materials; Domsjö Fabriker; Changzhou Shanfeng Chemical Industry Co., Ltd.; Domtar Corporation; Nippon Paper Industries Co., Ltd.; Metsä Group; The Dallas Group of America, Inc.; Liquid Lignin Company; Burgo Group S.p.A; Valmet Corporation

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Lignin Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global lignin market report based on the product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Lingosulfonates

-

Kraft Lignin

-

Organosolv Lignin

-

Hydrolyzed Lignin

-

SODA Lignin

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

Construction Material

-

Transportation Fuel

-

Biopolymer

-

Polyurethane Foam

-

Others

-

-

Bio-asphalt

-

Resins & Glues

-

Dispersants

-

Carbon Fiber & Bio-based Carbons

-

Vanillin

-

Animal Feed

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Indonesia

-

Malaysia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

-

Frequently Asked Questions About This Report

The global lignin market size was estimated at USD 1.37 billion in 2025 and is expected to reach USD 1.43 billion in 2026.

The global lignin market is expected to grow at a compound annual growth rate a CAGR of 5.2% from 2026 to 2033 to reach USD 2.04 billion by 2033.

Key factors driving the lignin market growth include the increasing demand for lignin in dust control applications and construction activities.

Europe dominated the lignin market with a share of over 38.5% in 2025. This is attributable to the presence of a favorable regulatory framework for the use of lignin in a wide array of commercial applications.

Some of the key players operating in the Lignin market include Stora Enso; West Fraser Timber Co.; UPM; Sweetwater Energy; Borregaard LignoTech; Rayonier Advanced Materials; Domsjö Fabriker; Changzhou Shanfeng Chemical Industry Co., Ltd.; Domtar Corporation; Nippon Paper Industries Co., Ltd.; Metsä Group; The Dallas Group of America, Inc.; Liquid Lignin Company; Burgo Group S.p.A; Valmet Corporation

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.