- Home

- »

- Healthcare IT

- »

-

ADHD Apps Market Size, Share & Trends Report, 2026-2033GVR Report cover

![ADHD Apps Market Size, Share & Trends Report]()

ADHD Apps Market (2026 - 2033) Size, Share & Trends Analysis Report By App Type (Behavioral Management Apps, Cognitive Training & Gamified Apps), By User Age Group, By Platform, By End Use (Parents & Caregivers, Healthcare Providers), By Region, And Segment Forecasts

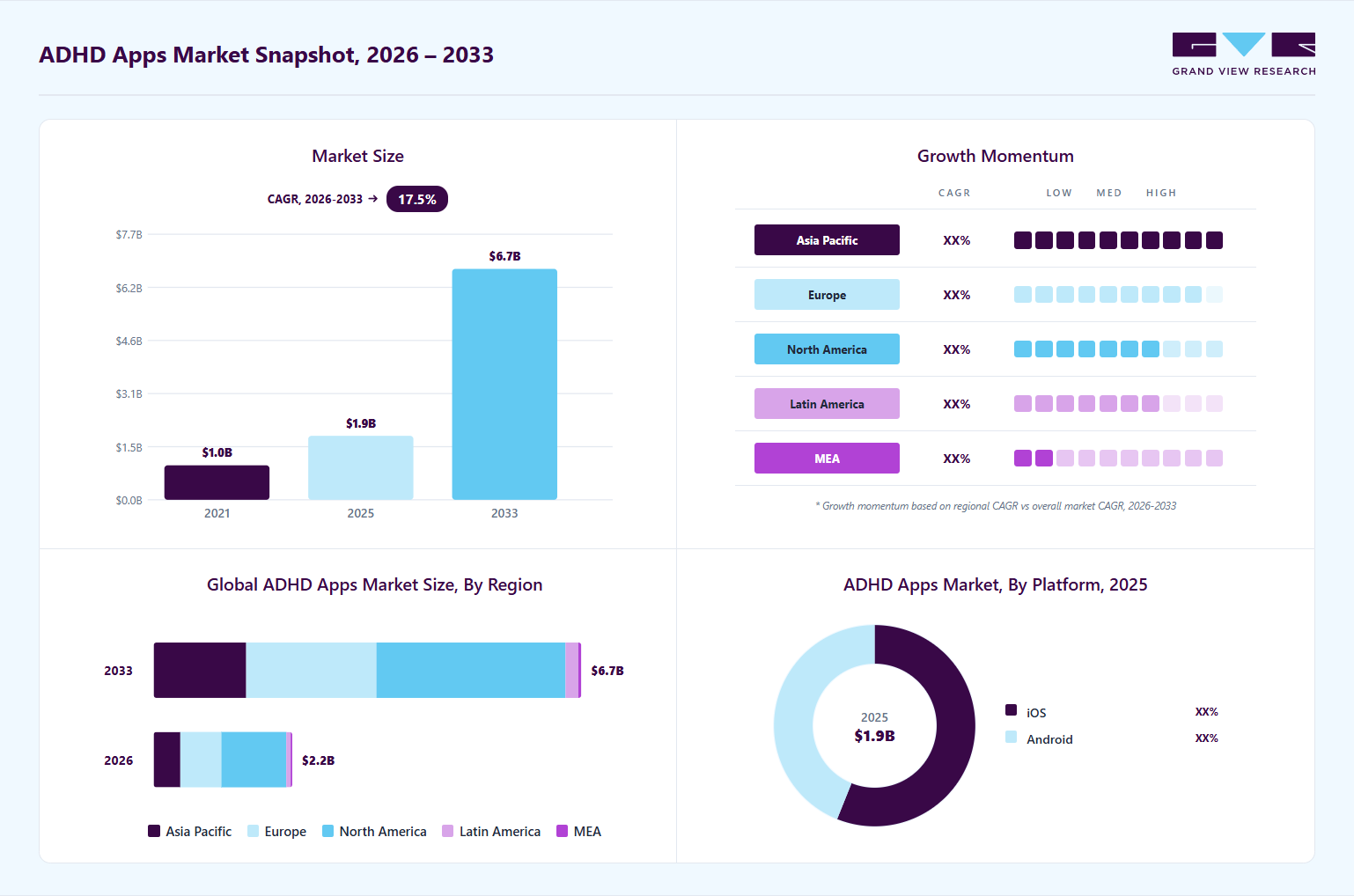

Market Size, 2025

$1.9BMarket Estimate, 2026

$2.2BMarket Forecast, 2033

$6.7BCAGR, 2026–2033

17.5%ADHD Apps Market Summary

The global ADHD apps market size was valued at USD 1.9 billion in 2025 and is projected to grow from USD 2.2 billion in 2026 to USD 6.7 billion by 2033, at a CAGR of 17.5% from 2026 to 2033. North America dominated the global market in 2025 and accounted for the largest revenue share of 47.2%. The increasing prevalence of ADHD among children, adolescents, and adults is significantly driving the demand for these applications.

Key Market Trends & Insights

- Asia Pacific ADHD apps market is anticipated to register the fastest growth rate during the forecast period.

- In terms of app type, the cognitive training & gamified apps segment held the largest revenue share in 2025.

- In terms of user age group, the adults (18+) segment held the largest revenue share in 2025.

- In terms of platform, the iOS segment held the largest revenue share in 2025.

- In terms of end use, the individuals / consumers segment held the largest revenue share in 2025.

Market Size & Forecast

- 2025 Market Size: USD 1.9 Billion

- 2026 Market Size: USD 2.2 Billion

- 2033 Projected Market Size: USD 6.7 Billion

- CAGR (2026-2033): 17.5%

- North America: Largest market in 2025

- Asia Pacific: Fastest growing market

")

Growing awareness regarding early diagnosis, mental health screening, and behavioral disorders has increased the adoption of digital tools for symptom monitoring, focus improvement, and behavioral management. For instance, in May 2026, Lumosity announced that the U.S. FDA granted 510(k) clearance to LumosityRx, a prescription digital therapeutic for adults with ADHD. The platform demonstrated statistically significant improvement in sustained and selective attention during a randomized, double-blind clinical trial involving over 500 participants.

Market Dynamics

The increasing prevalence of Attention-Deficit/Hyperactivity Disorder among children, adolescents, and adults is significantly driving demand for ADHD management applications and digital therapeutics. Growing awareness regarding adult ADHD, improved screening practices, and expanding access to mental healthcare are increasing the adoption of mobile-based cognitive training, symptom tracking, and behavioral management solutions. According to the Centers for Disease Control and Prevention (CDC), in October 2024, approximately 15.5 million U.S. adults were reported to have ADHD, while nearly half received their diagnosis during adulthood, thereby accelerating demand for accessible and technology-enabled ADHD support solutions.

The rapid expansion of digital mental health platforms and telehealth services is accelerating the adoption of ADHD apps globally. Patients are increasingly utilizing mobile applications for focus improvement, medication reminders, cognitive behavioral therapy support, and remote consultations due to convenience, accessibility, and lower dependency on in-person psychiatric visits. In addition, increasing shortages of mental health professionals and long waiting periods for ADHD diagnosis are strengthening reliance on digital healthcare solutions. For instance, in April 2023, Talkspace launched its Mental Health Conditions Library, a free digital resource providing clinically reviewed information on mental health conditions, including ADHD. The initiative highlighted increasing consumer reliance on digital mental health platforms for ADHD awareness, self-assessment, virtual care access, and treatment guidance.

The adoption of ADHD apps remains constrained due to rising concerns associated with data privacy, cybersecurity risks, and limited clinical validation. A substantial number of ADHD and mental wellness applications lack strong clinical evidence, standardized treatment protocols, and regulatory approvals, reducing physician confidence and limiting healthcare integration. Privacy concerns are further restricting adoption as mobile health applications frequently collect sensitive personal and behavioral information. For instance, in February 2026, security researchers from Oversecured identified more than 1,500 vulnerabilities across 10 Android mental health applications with approximately 14.7 million downloads, exposing sensitive data, including therapy records, mood logs, medication schedules, and cognitive behavioral therapy notes, highlighting major cybersecurity concerns within digital mental health platforms.

The market presents significant growth opportunities through expanding adoption of AI-enabled digital therapeutics, gamified cognitive training platforms, and personalized behavioral management solutions. Advancements in artificial intelligence, neurofeedback, adaptive learning technologies, and real-time analytics are improving patient engagement, cognitive assessment, and treatment adherence. Growing regulatory support for prescription digital therapeutics is further supporting market expansion. For instance, in June 2024, Akili Interactive announced expanded commercialization initiatives for EndeavorRx, its FDA-authorized digital therapeutic for pediatric ADHD, strengthening the integration of game-based cognitive treatment solutions into mainstream ADHD care management.

Market Concentration & Characteristics

The market is experiencing strong innovation through the integration of AI, gamified cognitive training, neurofeedback technologies, and personalized behavioral analytics. These technologies are improving focus enhancement, symptom monitoring, treatment adherence, and patient engagement while enabling scalable digital mental healthcare delivery. For instance, in September 2025, Shelpful, a digital health startup, launched its iOS application on the Apple App Store. Designed for individuals with ADHD and those experiencing challenges with organization and productivity, the app simplifies habit formation and task management through an intuitive chat-based interface.

The market is witnessing increasing merger, acquisition, and partnership activity as digital health companies expand mental health capabilities, strengthen user engagement platforms, and broaden virtual behavioral healthcare offerings. Strategic acquisitions are enabling companies to enhance AI capabilities, expand subscription-based mental wellness ecosystems, and strengthen digital therapeutic portfolios. For instance, in March 2026, Cerebral acquired Inflow, an ADHD-focused behavioral health application offering cognitive behavioral therapy-based modules, community engagement features, and daily skill-building programs, strengthening Cerebral’s continuous care and ADHD management capabilities.

Regulatory frameworks significantly influence product development, clinical validation standards, patient data protection, and commercialization strategies within the ADHD apps industry. Regulatory agencies are increasingly emphasizing cybersecurity compliance, clinical evidence generation, digital therapeutic approvals, and patient privacy standards to improve safety and treatment reliability across mental health applications. Growing regulatory support for prescription digital therapeutics is supporting wider healthcare adoption.

The market is expanding into diversified service offerings, including cognitive behavioral therapy support, ADHD coaching, medication adherence tracking, neurofeedback training, virtual psychiatric consultations, productivity management tools, and personalized cognitive training programs. Companies are increasingly integrating AI-powered analytics, wearable connectivity, telehealth capabilities, and real-time behavioral monitoring features to improve accessibility, treatment personalization, and long-term patient engagement across digital ADHD management platforms. For instance, in March 2026, Cerebral acquired Inflow to expand its ADHD care capabilities through self-guided support tools, behavioral management programs, and continuous care solutions between therapy sessions.

App Type Insights

By app type, the cognitive training & gamified apps segment dominated the market and accounted for the largest share of 27.0% in 2025. Growth of the segment is driven by increasing demand for interactive, evidence-based digital interventions designed to improve attention, executive function, and behavioral self-regulation through structured cognitive exercises and game-based learning models. Rising smartphone penetration, growing acceptance of digital therapeutics, and increasing preference for self-managed ADHD support tools further strengthened segment expansion. Market participants were enhancing offerings through AI-enabled adaptive learning systems, neurofeedback integration, and personalized cognitive training modules to improve user engagement and clinical outcomes. For instance, in April 2026, Excellent Brain Ltd. launched an Android-based neurofeedback platform for ADHD cognitive training, expanding access to mobile-enabled brain training solutions designed to improve attention and cognitive performance through EEG-driven interactive exercises.

The prescription digital therapeutics (PDTs) segment is anticipated to witness the fastest growth during the forecast period in the market. Growth of the segment is driven by increasing clinical validation of app-based interventions, rising regulatory approvals for software-as-medical-device solutions, and growing physician acceptance of digitally delivered behavioral therapies for attention regulation and executive function improvement. Expanding integration of prescription-based mobile therapeutics into standard ADHD treatment pathways is further accelerating adoption, supported by improved reimbursement frameworks and stronger evidence from randomized clinical studies demonstrating measurable symptom reduction and improved patient adherence outcomes.

User Age Group Insights

The adults (18+) segment dominated the market and accounted for the largest share of 55.9% in 2025. Rising diagnosis rates among adults, increasing awareness of persistent Attention-Deficit/Hyperactivity Disorder symptoms beyond childhood, and growing adoption of digital self-management tools to support attention regulation, productivity, and emotional control in daily life are fueling the market. Expanding telehealth access and increased willingness among adults to seek non-stigmatizing, app-based behavioral support further strengthened segment dominance. Market participants are introducing clinically supported digital therapeutics and mobile-based cognitive training solutions tailored specifically for adult users. For instance, in January 2026, ArkBio received marketing authorization in China for Aizhida, an ADHD treatment indicated for individuals aged 6 years and older, reflecting the growing clinical focus on ADHD management across adolescent and adult populations and reinforcing demand for structured, long-term digital support ecosystems for adults living with ADHD symptoms.

The children & adolescents (ages 5-17) segment is expected to witness significant growth over the forecast period in the market, owing to the rising early diagnosis rates, increasing awareness of neurodevelopmental disorders among parents and educators, and growing integration of digital behavioral interventions into pediatric care and school-based support systems. Expanding use of gamified cognitive training, attention-building exercises, and behavior modification applications is further strengthening adoption among younger users. For instance, in August 2024, Cog ADHD launched a digital ADHD management application integrating clinician-guided treatment frameworks, self-help modules, and symptom tracking tools, supporting children and adolescents in building structured routines and improving attention and behavioral control outcomes.

Platform Insights

The iOS platform held a significant user base in the market with the largest revenue share of 56.1%, driven by high smartphone penetration, strong presence of premium subscription users, and greater adoption of digital health applications among urban and high-income populations. iOS users are typically more engaged with paid productivity, cognitive training, and digital therapeutic applications, contributing disproportionately to in-app purchase revenue despite representing a smaller share of total global smartphone users. According to a comparative analysis published by Adapty, iOS users demonstrate significantly higher monetization potential compared to Android users, driven by stronger purchasing power, higher subscription conversion rates, and greater in-app spending behavior. The study highlights that iOS users contribute nearly 68-69% of global app revenue despite representing a smaller share of total smartphone users, reflecting a premium user base with a higher willingness to pay for digital products and subscription-based applications.

The Android segment is expected to grow significantly over the forecast period. Growth of the segment is driven by widespread smartphone penetration across emerging economies, affordability of Android devices, and increasing access to digital mental health applications among price-sensitive user groups. The open ecosystem of Android enables broader app distribution, contributing to higher downloads and improved accessibility of ADHD-focused behavioral management, cognitive training, and productivity applications. This expanding user base is expected to support strong volume-led growth across ADHD apps over the forecast period.

End Use Insights

The individuals/consumers segment accounted for a significant share of 44.3% in 2025. Growth of the segment was driven by rising self-management of attention-deficit/hyperactivity disorder symptoms, increasing preference for discreet and on-demand digital mental health support, and growing adoption of mobile-based cognitive training, productivity tracking, and behavioral therapy applications. Expanding awareness of ADHD among adults and adolescents, coupled with improved accessibility of subscription-based and freemium app models, further supported segment dominance.

The enterprises/corporate wellness segment is expected to grow significantly over the forecast period. Rising productivity concerns are linked to attention-related disorders, and growing adoption of digital wellness programs within workplace environments. Organizations are increasingly integrating ADHD-focused applications into employee assistance programs (EAPs) to improve focus, task management, stress regulation, and overall workplace efficiency. Expanding hybrid and remote work models further strengthen demand for scalable, app-based behavioral and cognitive support tools. Market participants are developing workplace-oriented ADHD solutions that combine coaching, productivity tracking, and cognitive training modules tailored for professional users. For instance, in January 2025, Headspace expanded its employer wellness offerings by enhancing digital mental health programs designed to support focus, stress management, and behavioral well-being in corporate settings, reflecting increasing integration of ADHD-aligned digital tools within enterprise wellness ecosystems.

Regional Insights

North America ADHD apps market led with a revenue share of 47.2% in 2025, supported by high digital health adoption, increasing ADHD diagnosis rates, strong telehealth infrastructure, and growing acceptance of prescription digital therapeutics. The region is witnessing the rapid expansion of AI-enabled mental health platforms, virtual psychiatry services, and cognitive training applications due to rising awareness regarding adult ADHD and increasing demand for accessible behavioral healthcare solutions. Strong smartphone penetration and favorable reimbursement support for digital mental health services are further accelerating market growth.

U.S. ADHD Apps Market Trends

The ADHD apps market in the U.S. is expected to grow at a significant rate, driven by increasing adoption of digital therapeutics, rising mental health awareness, and expanding telepsychiatry services. Growing demand for productivity management tools, behavioral therapy support, and medication adherence applications among adults and students is further strengthening market expansion. In September 2025, Shelpful launched an ADHD-focused iOS application featuring AI-powered habit coaching, chat-based task management, personalized reminders, and behavioral support tools. The platform is developed to improve task adherence, reduce overwhelm, and strengthen personalized productivity management for individuals with ADHD.

Canada ADHD apps market is anticipated to register notable growth during the forecast period, supported by increasing investment in digital mental healthcare, rising awareness regarding neurodevelopmental disorders, and expanding virtual healthcare accessibility. Governments' focus on improving mental healthcare delivery and increasing utilization of mobile health applications is supporting market expansion across the country. In May 2026, Flint ADHD Daily Planner launched an ADHD-focused productivity application featuring task scheduling, mood tracking, voice-based note creation, and adaptive daily planning tools. The platform is developed to simplify task management and improve daily organization for individuals with ADHD.

Asia Pacific ADHD Apps Market Trends

The ADHD apps market in Asia Pacific is expected to register the fastest CAGR during the forecast period from 2026 to 2033, driven by increasing awareness regarding ADHD, rising smartphone penetration, expanding telehealth accessibility, and growing demand for affordable digital mental healthcare solutions. ADHD prevalence in India remains significant, with studies indicating prevalence rates ranging from 1.3% to 28.9%, supported by regional and socioeconomic variations. Underdiagnosis and limited access to specialized mental healthcare services continue to create substantial unmet needs, particularly among females and underserved populations.

China ADHD apps market led the Asia Pacific region in 2025, supported by rapid digital healthcare expansion, increasing mental health awareness, and strong adoption of mobile health platforms. Government initiatives promoting digital healthcare infrastructure and telemedicine services are further supporting market growth. Expansion of AI-powered mental wellness applications and online psychiatric consultation platforms is improving accessibility to ADHD-related behavioral healthcare services across urban populations.

The ADHD apps market in India held a notable share in the Asia Pacific region, driven by increasing awareness regarding ADHD, growing utilization of telehealth platforms, and rising demand for affordable digital mental healthcare solutions among students and working professionals. Expansion of app-based mental wellness platforms, rising smartphone penetration, and increasing acceptance of online counseling services are accelerating the adoption of ADHD management applications across urban regions.

Europe ADHD Apps Market Trends

The ADHD apps market in Europe is supported by growing mental health awareness, increasing demand for digital therapeutics, and strong healthcare digitization initiatives. Rising prevalence of adult ADHD, increasing utilization of telepsychiatry services, and favorable regulatory focus on digital healthcare innovation are strengthening market growth across the region. In 2025, MEDICE Health Family advanced the commercialization of MEDIGITAL, an ADHD-focused digital health application developed for families of children with ADHD across Scandinavian markets. The initiative focused on improving patient support, healthcare accessibility, and digital treatment integration despite limited reimbursement frameworks for digital health solutions.

Germany ADHD apps market is anticipated to register a considerable growth rate during the forecast period. The country is witnessing increasing adoption of digital mental healthcare solutions due to strong healthcare infrastructure, rising demand for remote behavioral therapy services, and growing focus on digital therapeutics. Expansion of app-based cognitive training platforms and telepsychiatry services is further improving ADHD care accessibility. In 2022, Psyon Games and Takeda launched FULL ADHD in Germany, a mobile awareness game developed to improve understanding of adult ADHD through experiential learning and interactive storytelling. The platform aimed to increase public awareness, reduce stigma, and support empathy toward individuals living with ADHD.

The ADHD apps industry in the UK is anticipated to grow considerably during the forecast period. The UK ADHD apps market is anticipated to grow significantly during the forecast period, driven by increasing mental health awareness, growing telehealth utilization, and rising diagnosis rates among adults and adolescents. Demand for digital behavioral management tools, virtual therapy platforms, and medication adherence applications is increasing due to pressure on traditional mental healthcare systems and long waiting periods for ADHD assessments. For instance, in January 2026, NHS England reported rising pressure on ADHD assessment services due to increasing diagnosis demand and extended waiting periods across Integrated Care Boards, strengthening reliance on digital behavioral management platforms, telepsychiatry services, and virtual ADHD support solutions.

Latin America ADHD Apps Market Trends

The ADHD apps market in Latin Americais expected to register strong growth during the forecast period, supported by increasing digital healthcare adoption, rising awareness regarding mental health disorders, and expanding smartphone accessibility. Countries including Brazil and Mexico are witnessing growing utilization of mobile mental wellness applications, online counseling platforms, and AI-enabled behavioral health tools due to increasing internet penetration and improving healthcare accessibility.

Brazil ADHD apps market accounted for a significant share, driven by increasing awareness regarding behavioral health disorders, rising utilization of digital mental healthcare platforms, and growing demand for affordable remote psychological support services. Expansion of app-based therapy platforms and telepsychiatry services is further supporting market development across urban populations.

MEA ADHD Apps Market Trends

The ADHD apps market in the Middle East & Africa held a significant share, supported by improving healthcare digitization, increasing mental health awareness, and rising adoption of telehealth services. Growing smartphone penetration and expansion of digital healthcare infrastructure are strengthening accessibility to behavioral health applications and virtual psychiatric support services across the region. For instance, in October 2025, PureHealth launched nationwide virtual mental health services through its AI-enabled Pura application in collaboration with SAKINA, strengthening accessibility to digital psychiatric consultations and behavioral healthcare services across the UAE and broader Gulf region.

The UAE ADHD apps market holds a significant market share due to increasing investment in digital healthcare infrastructure, rising utilization of telemedicine platforms, and growing awareness regarding mental health management solutions. Government initiatives supporting healthcare innovation and digital transformation are further strengthening the adoption of ADHD management applications across the country.

Key ADHD Companies Insights

Key participants in the ADHD apps market are focusing on devising innovative business growth strategies in the form of service portfolio expansions, partnerships & collaborations, mergers & acquisitions, and business footprint expansions.

Key ADHD Companies

The following key companies have been profiled for this study on the ADHD apps market.

-

Inflow

-

Akili Interactive (EndeavorRx)

-

Shelpful

-

Focus@Will Labs, Inc.

-

Lumosity

-

CogniFit

-

SimpleMind

-

Skitch

-

MEDICE Health Family (MEDIGITAL)

-

ADHD Angel

-

Numo ADHD

-

Tiimo

-

Habitica

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Player: Lumosity

- Focus on large-scale cognitive training, attention enhancement programs, and brain performance optimization tools across the global consumer base.

- Strong global brand recognition and large existing user base (e.g., Lumosity, CogniFit, Focus@Will)

- Limited clinical positioning as prescription-grade ADHD digital therapeutics.

Emerging Player: Inflow

- Focus on ADHD-specific digital therapeutics, behavioral coaching, and executive function support tools.

- Higher personalization through AI coaching, adaptive reminders, and behavioral nudging systems.

- Limited global scale and lower brand recognition compared to mature cognitive apps

Recent Developments

-

In April 2026, Excellent Brain Ltd. launched an Android version of its Neurofeedback for ADHD platform, expanding mobile accessibility for cognitive training and neurofeedback therapy. The platform utilized EEG-based neurofeedback technologies to support attention improvement and cognitive function management among individuals with ADHD.

-

In August 2024, Cog ADHD launched a digital ADHD management application integrating specialist access, symptom analytics, self-help strategies, and educational resources. The platform utilized a treatment framework developed by researchers from Harvard Medical School and Massachusetts General Hospital to support behavioral management and attention regulation.

-

In January 2024, Pery, an AI-powered application developed to support parents of children with ADHD, was launched in the U.S. and Israel. The platform leverages advanced AI technology to deliver personalized, real-time guidance, providing parents with evidence-based answers and recommendations derived from the latest research and expert guidelines, tailored to the unique needs and circumstances of their children.

The increasing adoption of ADHD productivity applications reflects growing demand for digital tools that address executive functioning challenges such as time management, task prioritization, organization, focus enhancement, and habit formation. These applications are increasingly leveraging AI, gamification, visual planning, and behavioral support features to help individuals with ADHD improve productivity and daily functioning.

Some of the key apps in the ADHD market (as of 2026) are as follows:

Application

Key Focus Area

Key Features

Blabby AI

AI-Powered Productivity Assistance

Voice-to-task conversion, AI planning, task organization

Goblin Tools

Task Management & Planning

Task breakdown, estimation tools, ADHD-friendly planning

Tiimo

Visual Scheduling & Routine Building

Visual planners, reminders, routine management

Llama Life

Time Management

Time blocking, focus timers, task sequencing

Focusmate

Accountability & Focus Support

Virtual body doubling, productivity sessions

Sunsama

Workflow & Productivity Management

Daily planning, task prioritization, calendar integration

Todoist

Task Management

Project organization, reminders, productivity tracking

TickTick

Productivity & Habit Tracking

To-do lists, Pomodoro timer, habit monitoring

Motion

AI-Based Scheduling

Automated calendar management and task scheduling

Notion

Personal Knowledge & Task Management

Custom workflows, note-taking, project management

Forest

Focus Improvement

Gamified focus sessions and distraction reduction

ADHD Apps Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 1.9 billion

Market size value in 2026

USD 2.2 billion

Revenue forecast in 2033

USD 6.7 billion

Growth rate

CAGR of 17.5 % from 2026 to 2033

Actual data

2021 - 2025

Forecast data

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

App type, user age group, platform, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; Spain; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Inflow; Akili Interactive (EndeavorRx); Shelpful; Focus@Will Labs Inc.; Lumosity; CogniFit; SimpleMind; Skitch; MEDICE Health Family (MEDIGITAL); ADHD Angel; Numo ADHD; Tiimo; Habitica

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global ADHD Apps Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research, Inc. has segmented the global ADHD apps market report based on app type, user age group, platform, end use, and region:

-

App Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Behavioral Management Apps

-

Cognitive Training & Gamified Apps

-

Task Management & Productivity Tools

-

Prescription Digital Therapeutics (PDTs)

-

Others

-

-

User Age Group Outlook (Revenue, USD Billion, 2021 - 2033)

-

Children & Adolescents (Ages 5-17)

-

Adults (18+)

-

-

Platform Outlook (Revenue, USD Billion, 2021 - 2033)

-

iOS

-

Android

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Individuals / Consumers

-

Parents & Caregivers

-

Schools & Educational Institutions

-

Enterprises / Corporate Wellness

-

Healthcare Providers

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

Spain

-

France

-

Sweden

-

Denmark

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Thailand

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

App-level value and user volume analysis at the country level

Detailed subscription pricing, in-app purchase analysis, active user base trends, and download volume assessment for key ADHD app providers across cognitive training apps, digital therapeutics, behavioral management apps, productivity tools, and telehealth-based ADHD platforms across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Enables pricing benchmark assessment, evaluation of premium vs. freemium app models, identification of regional adoption trends, user engagement analysis, and assessment of market penetration across digital ADHD management platforms.

ADHD Apps Competitive Landscape & Digital Platform Analysis

Comprehensive competitive landscape assessment including feature benchmarking, AI capability analysis, therapeutic model comparison, regulatory approval tracking, partnership evaluation, user engagement analysis, and regional market share assessment across leading ADHD-focused app providers.

Supports strategic competitor evaluation, product differentiation assessment, acquisition and partnership analysis, platform positioning evaluation, regional expansion planning, and identification of high-growth digital therapeutic and behavioral management segments.

User Engagement, Retention & Subscription Analysis

Detailed analysis of monthly active users, subscription conversion rates, app retention trends, user engagement metrics, therapy adherence rates, and customer acquisition strategies across major ADHD app providers and regional markets.

Enables assessment of platform scalability, recurring revenue potential, user retention challenges, monetization efficiency, behavioral engagement performance, and long-term sustainability of ADHD-focused digital health platforms.

About the Author(s)

Healthcare IT Research Team

Healthcare · Healthcare ITThis report was authored by the healthcare it research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the healthcare it segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.