- Home

- »

- Next Generation Technologies

- »

-

AI Hardware Market Size, Share & Trends Report, 2026-2033GVR Report cover

![AI Hardware Market (2026 - 2033)Report]()

AI Hardware Market (2026 - 2033)

Size, Share & Trends Analysis Report By Hardware Component (Processors, Memory, Storage, Network, Specialized Embedded Hardware), By Application (Machine Learning/Deep Learning, Robotics), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$115.4BMarket Estimate, 2026

$151.3BMarket Forecast, 2033

$691.0BCAGR, 2026–2033

24.2%AI Hardware Market Summary

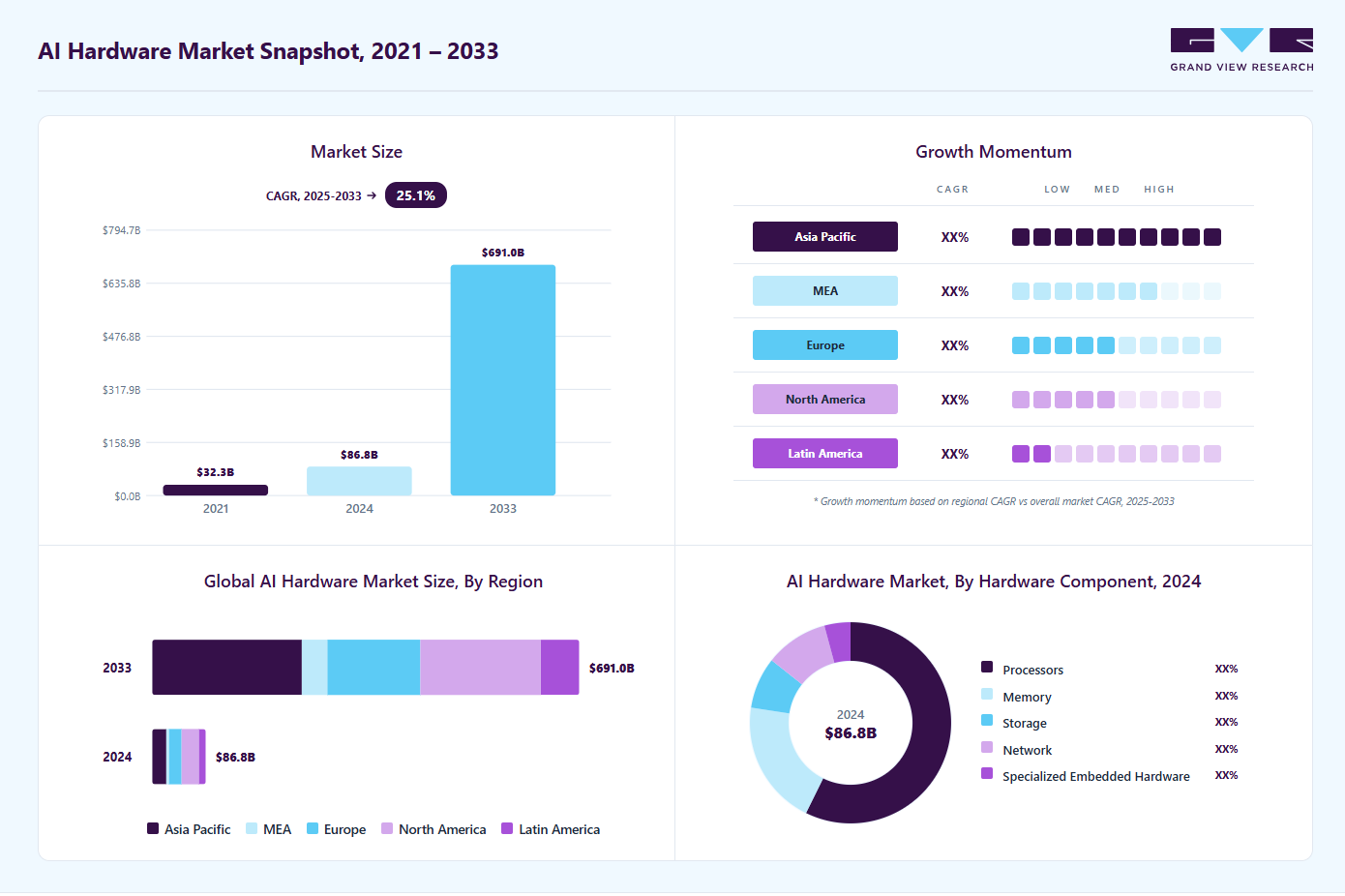

The global AI hardware market size was valued at USD 115.4 billion in 2025 and is projected to grow from USD 151.3 billion in 2026 to USD 691.0 billion by 2033, growing at a CAGR of 24.2% from 2026 to 2033. The market in North America dominated with a revenue share of 31.9% in 2025. The market is expanding rapidly, driven by the rising adoption of Artificial Intelligence (AI) across industries such as consumer electronics, automotive, healthcare, and defense.

Key Market Trends & Insights

- By hardware component: The processors segment led the market with the largest revenue share of 54.5% in 2025.

- By application: The machine learning/deep learning segment led the market with the largest revenue share of 44.2% in 2025.

Regional Highlights

- Largest regional market: North America (31.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 115.4 Billion

- Estimated market size in 2026: USD 151.3 Billion

- Projected market size by 2033: USD 691.0 Billion

- CAGR (2026-2033): 24.2%

Growth is fueled by increasing demand for high-performance processors, memory, and specialized chips to support training and inference of complex AI models. Chip designs are now being optimized to handle AI workloads directly on devices. This advancement enables smartphones, wearables, and PCs to process complex models with greater efficiency. The reduced reliance on cloud connectivity ensures faster performance for real-time applications. At the same time, keeping computations local enhances data privacy and security. Together, these developments are driving a stronger shift toward on-device AI processing.")

For instance, in September 2025, Arm Holdings plc, a UK-based semiconductor company, launched its Lumex chip designs, engineered for artificial intelligence on mobile devices, spanning from low-power wearables to advanced smartphones capable of running large AI models locally without relying on cloud access. The Lumex series, part of Arm’s Compute Subsystems business, is built on 3-nanometer manufacturing nodes.

The development of specialized chips for complex AI tasks is driving the growth of the AI hardware industry. These chips enhance efficiency and speed for real-world AI applications, prompting organizations to invest in advanced hardware capable of handling large-scale computations. This emphasis on practical AI workloads is fostering innovation in chip design, memory architecture, and system integration. It also encourages manufacturers to provide scalable solutions that support diverse AI applications. Companies are increasingly developing high-performance, task-focused chips that enable practical AI solutions efficiently. For instance, in September 2025, NVIDIA Corporation, a U.S.-based technology company specializing in GPUs and AI hardware, announced its Rubin CPX GPU, designed for disaggregated AI inference, where compute-focused chips handle context processing and memory-bandwidth-optimized chips manage generation tasks. The Rubin CPX, paired with standard Rubin GPUs in the upcoming Vera Rubin NVL144 CPX rack, will deliver up to 8 exaFLOPs of performance, targeting large AI workloads such as multi-step reasoning and AI video generation.

Edge computing is increasingly influencing chip design, focusing on processing data near its source. This approach reduces latency for real-time AI applications. Chips must operate independently to support decentralized workloads, while power efficiency remains crucial for devices at the edge. Compact design allows integration into small form factors, and low thermal output ensures stable operation in confined spaces. Reliability is essential to handle varied and remote environments. Edge-focused designs often integrate multiple functions on a single chip. These innovations improve performance and responsiveness for AI tasks. Chip developers are prioritizing versatility and efficiency. Manufacturers are also exploring new materials and architectures to further optimize edge performance.

Market Dynamics

The AI hardware market is being driven by the rapid expansion of generative AI, machine learning, and large language model deployments across enterprises, requiring high-performance computing infrastructure. Growing demand for faster data processing, real-time analytics, and edge AI applications is accelerating the adoption of advanced processors, GPUs, AI accelerators, and specialized chips. Cloud service providers and hyperscale data centers are making substantial investments in AI computing capacity to support increasingly complex workloads.

The rapid adoption of generative AI and large language models (LLMs) is significantly increasing demand for advanced AI hardware across industries. Training and deploying complex AI models require massive computational power, driving the need for high-performance GPUs, AI accelerators, and specialized processors. As organizations integrate AI into applications such as content generation, virtual assistants, software development, and customer support, the scale of computing infrastructure required continues to expand.

In addition, the growing complexity and size of AI models are increasing requirements for memory bandwidth, processing speed, and energy-efficient architectures. Technology companies, research institutions, and enterprises are investing heavily in AI hardware to reduce model training times and improve inference performance. This sustained growth in generative AI workloads is creating strong demand for next-generation AI chips and supporting long-term expansion of the AI hardware market.

The AI hardware market faces a significant restraint in the form of high development and deployment costs associated with advanced computing infrastructure. AI processors, GPUs, accelerators, high-bandwidth memory systems, and specialized networking equipment require substantial capital investment, making adoption challenging for small and medium-sized enterprises. The complexity of designing and manufacturing cutting-edge AI chips also drives up research, development, and fabrication expenses. Additionally, organizations must invest in supporting infrastructure such as high-performance servers, storage systems, and cooling technologies to effectively deploy AI workloads.

The total cost of ownership extends beyond initial hardware purchasing and includes software integration, maintenance, upgrades, and energy consumption. Rapid technological advancements can shorten hardware refresh cycles, forcing companies to make frequent investments to remain competitive. Many organizations struggle to justify these expenditures without clear and immediate returns on investment, particularly in emerging AI applications. As a result, the high financial barriers associated with AI hardware infrastructure can slow adoption rates and limit market expansion in cost-sensitive regions and industries.

The increasing deployment of AI capabilities directly on devices such as smartphones, autonomous vehicles, industrial equipment, surveillance systems, and IoT endpoints is creating significant growth opportunities for the AI hardware market. Organizations are increasingly adopting edge AI solutions to process data locally, reducing dependence on cloud infrastructure and minimizing latency. This enables faster decision-making, improved operational efficiency, and enhanced user experiences in real-time applications. As industries demand immediate insights from connected devices, the need for high-performance and energy-efficient AI processors at the edge continues to rise. The growing concerns regarding data privacy, security, and bandwidth limitations are accelerating the shift toward on-device intelligence. Processing sensitive information locally helps organizations comply with regulatory requirements while reducing the costs associated with data transmission and cloud computing. Advances in semiconductor design, low-power AI accelerators, and integrated neural processing units are making edge AI deployments more practical and scalable. The emergence of smart factories, connected healthcare devices, and intelligent transportation systems is further expanding the addressable market for edge AI hardware.

Market Concentration & Characteristics

The AI hardware market demonstrates a high degree of innovation, driven by continuous advancements in AI accelerators, GPUs, custom silicon, high-bandwidth memory, and chiplet architectures. Market participants are investing heavily in performance optimization, energy efficiency, and specialized hardware designed for generative AI and large-scale model training. Rapid technological evolution has shortened product cycles and increased competitive differentiation through architectural innovation. As AI workloads become more complex, innovation remains a primary factor influencing market leadership and adoption.

End-user concentration is relatively high, with a significant share of AI hardware spending originating from hyperscale cloud providers, large enterprises, government agencies, and research institutions. These organizations account for substantial investments in AI data centers, high-performance computing systems, and advanced AI infrastructure. Their large procurement volumes influence product roadmaps, pricing strategies, and technology adoption trends across the industry. As a result, market growth remains closely linked to capital expenditure patterns among a concentrated group of high-value customers.

Analyst Perspective

The AI hardware market occupies a foundational position in the AI value chain, supported by accelerating investments. Unlike software markets where differentiation can shift rapidly, competitive advantage in AI hardware is increasingly defined by access to advanced semiconductor manufacturing, high-performance architectures, memory bandwidth, and software ecosystem integration. The most durable market leaders are likely to be those that combine compute, networking, memory, and developer platforms into a unified AI infrastructure stack, creating high switching costs and long deployment cycles. As AI workloads continue to expand from training-centric environments to inference at scale, revenue growth is expected to increasingly depend on delivering performance-per-watt, system-level optimization, and full-stack infrastructure solutions rather than standalone chip innovation alone.

Hardware Component Insights

Based on hardware component, the processors segment led the market with the largest revenue share of 54.5% in 2025 and is expected to grow at the fastest CAGR over the forecast period. These processors are central to AI workloads, enabling faster data processing and efficient model execution. Advances in GPU, CPU, and AI accelerator technologies have enhanced their capabilities, supporting complex AI applications across industries. The adoption of specialized processors for both training and inference further strengthened their market position. Increasing investments in data centers and edge computing fueled the need for powerful processors. Consequently, this segment maintained a dominant share in the AI hardware market throughout 2024.

Specialized embedded hardware is expected to experience significant growth over the forecast period. These devices are designed to perform dedicated AI tasks efficiently, offering low power consumption and compact form factors. Their adoption is rising across industries such as automotive, healthcare, and industrial automation. As AI workloads become more diverse and decentralized, the demand for embedded solutions continues to increase. This trend shows the market’s shift toward more application-specific and energy-efficient AI hardware. Manufacturers are investing in research and development to enhance processing capabilities and reduce latency.

Application Insights

Based on application, the machine learning/deep learning segment led the market with the largest revenue share of 44.2% in 2025. The hardware, primarily high-performance GPUs, supports a broad range of tasks, including computer vision, natural language processing, and general data analysis. The established use of these technologies across industries such as healthcare, finance, and manufacturing makes this segment the largest by market share. This dominance is due to the maturity and widespread implementation of these foundational AI models. This continued dominance is further solidified by the constant need for more powerful and efficient hardware to train increasingly complex models.

Generative AI is a rapidly growing force in the AI hardware market, though it is still a smaller segment. The demand for specialized and powerful hardware is accelerating as the complexity of large language models and image-generation tools increases. This sector's explosive growth is fueled by massive investments in creating next-generation models that require unprecedented computational resources for both training and inference. The future market share of generative AI is projected to significantly expand, challenging the dominance of traditional machine learning hardware.

End Use Insights

Based on End Use, Consumer electronics segment led the AI hardware maket with revenue share of 27.5% in 2025. The ubiquity of smart devices such as smartphones, smart speakers, and smart TVs has driven immense demand for on-device AI chips and processors. This market is further boosted by the integration of AI-powered features such as voice assistants, personalized recommendations, and advanced image processing directly into consumer products. This widespread adoption, combined with the sheer volume of devices sold annually, solidifies consumer electronics' dominant position in the market. The constant innovation in smart devices, with each new generation offering more advanced AI capabilities, ensures this dominance will continue for the foreseeable future.

The automotive sector is an increasingly important and rapidly growing market for AI hardware. The rise of Advanced Driver-Assistance Systems (ADAS) and the push for fully autonomous vehicles are creating a massive demand for powerful and specialized AI chips. Hardware is crucial for processing real-time sensor data from cameras, LiDAR, and radar to enable features such as lane-keeping assist and automatic emergency braking. As regulations tighten and consumer demand for smarter, safer cars increases, the automotive industry's investment in AI hardware is growing exponentially. This explosive growth is further fueled by the transition to electric vehicles, which heavily rely on AI for optimizing battery management and improving energy efficiency.

Regional Insights

North America dominated the AI hardware market with the largest revenue share of 31.9% in 2025, a position driven by its thriving technology ecosystem. The region hosts a number of leading hardware developers who are at the forefront of creating powerful processors. These organizations make substantial investments in research and development, which solidifies the region's technological leadership. Furthermore, North America benefits from significant venture capital funding and a strong concentration of top research institutions and skilled talent. The early and widespread adoption of AI across various industries, from IT to healthcare, further drives the demand for advanced hardware.

U.S. AI Hardware Market Trends

The AI hardware market in the U.S. held the largest share in the North America region in 2025. This position is a result of a highly developed technology ecosystem and a strong presence of numerous leading AI hardware innovators. The U.S. benefits from substantial private and public sector investment in AI research and development, a robust venture capital environment, and a deep pool of skilled talent.

Europe AI Hardware Market Trends

Europe represents a major and steadily growing market for AI hardware, fueled by increasing adoption in manufacturing, automotive, and healthcare. The region is actively strengthening its own semiconductor and AI capabilities through government initiatives and a focus on building a robust technological foundation. While Europe's market share is smaller than the U.S.'s, its emphasis on ethical AI frameworks and the development of specialized industrial applications positions it for consistent and deliberate expansion.

Asia Pacific AI Hardware Market Trends

The Asia Pacific region is the fastest-growing AI hardware industry and is poised to significantly increase its global share. This rapid growth is driven by massive digitalization efforts, government support, and a booming consumer electronics sector. Countries such as China, Japan, and South Korea are making large-scale investments in AI and 5G infrastructure, creating a vast and expanding market for AI-enabled devices. The region is a critical hub for both innovation and manufacturing, making it a key player in the global AI hardware supply chain.

Key AI Hardware Company Insights

Some of the key companies in the AI hardware industry include Amazon.com, Inc.; Apple Inc.; Cerebras Systems Inc.; Graphcore; and Intel Corporation. Organizations are focusing on increasing their customer base to gain a competitive edge. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Microsoft has been actively expanding its AI hardware and cloud infrastructure capabilities to support AI workloads. Its Azure cloud platform provides specialized AI instances optimized for machine learning and deep learning tasks. The company is investing in high-performance computing clusters to accelerate AI research and enterprise adoption. Microsoft collaborates with hardware vendors to integrate cutting-edge GPUs and FPGAs into its offerings. These efforts enable Microsoft to provide scalable, efficient, and secure AI solutions for a wide range of industries.

-

NVIDIA Corporation is a major player in AI hardware, particularly known for its GPUs used in machine learning and deep learning applications. Its GPU architectures are designed to deliver high performance for both training and inference workloads. NVIDIA also develops AI software frameworks, enabling seamless integration with its hardware for accelerated computation. The company’s innovations have positioned it as a preferred choice for cloud providers, research institutions, and enterprises. NVIDIA continues to advance AI hardware with new products targeting next-generation AI models and high-efficiency computing.

Key AI Hardware Companies:

The following key companies have been profiled for this study on the AI hardware market.

-

Advanced Micro Devices, Inc. (AMD)

-

Amazon.com, Inc.

-

Apple Inc.

-

Cerebras Systems Inc.

-

Graphcore

-

Intel Corporation

-

Microsoft

-

NVIDIA Corporation

-

Qualcomm Incorporated

-

Robert Bosch GmbH

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Apple Inc., Amazon.com, Inc., Advanced Micro Devices, Inc., Microsoft)

- Focus on vertically integrated AI ecosystems combining hardware, software, cloud, and developer platforms.

- Invest heavily in advanced semiconductor design, strategic partnerships, and large-scale manufacturing capacity to maintain market leadership.

- Strong financial resources, established customer relationships, and global networks support large-scale deployment.

- Broad product portfolios and mature software ecosystems enable end-to-end AI infrastructure offerings across multiple industries.

- Large organizational structures can result in longer product development and commercialization cycles.

- Dependence on advanced foundries and complex supply chains may expose operations to capacity constraints and geopolitical risks.

Emerging Players (Graphcore, Cerebras Systems Inc.)

- Focus on specialized AI architectures to address limitations of conventional processors.

- Target niche AI training and inference workloads for product development and strategic technology collaborations.

- Faster architectural innovation and rapid adaptation to evolving AI workload requirements.

- Differentiated chip designs deliver higher efficiency for specific AI applications and model architectures.

- Limited ecosystem support compared with established industry leaders.

- Dependence on external funding and slower enterprise adoption regarding long-term platform support and interoperability.

Recent Developments

-

In June 2025, Hewlett Packard Enterprise, a U.S.-based Information technology company, and NVIDIA Corporation expanded their partnership at HPE Discover in Las Vegas, launching new modular AI infrastructure and turnkey AI platforms, including HPE’s AI-enabled RTX PRO Servers and the HPE Private Cloud AI platform. The aim is to help enterprises build and scale generative, agentic, and industrial AI applications by providing full-stack AI factory solutions that combine computing hardware, software, and services.

-

In September 2024, Intel Corporation launched Xeon 6 processors and Gaudi 3 AI accelerators to enhance enterprise AI performance and efficiency. These AI hardware solutions aim to optimize the total cost of ownership and support large-scale AI workloads.

-

In June 2024, NVIDIA Corporation launched new AI hardware and products at Computex 2024 in Taipei, including the general availability of Nvidia ACE generative AI, plans for an ultra version of the Blackwell platform in 2025, and a next-generation GPU architecture codenamed Rubin. It aims to accelerate AI adoption by transforming traditional data centers into AI-focused factories, supporting generative AI applications, and enabling AI-powered autonomous systems.

AI Hardware Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 115.4 billion

Market size value in 2026

USD 151.3 billion

Revenue forecast in 2033

USD 691.0 billion

Growth rate

CAGR of 24.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Hardware component, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; Russia; Iceland; Finland; China; Japan; India; South Korea; Australia; Thailand; Singapore; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait; Israel

Key companies profiled

Advanced Micro Devices, Inc. (AMD), Amazon.com, Inc., Apple Inc., Cerebras Systems Inc., Graphcore, Intel Corporation, Microsoft, NVDIA Corporation, Qualcomm Incorporated, Robert Bosch GmbH

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AI Hardware Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global AI Hardware market report based on hardware component, application, end use, and region:

-

Hardware Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Processors

-

Memory

-

Storage

-

Network

-

Specialized Embedded Hardware

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Machine Learning/Deep Learning

-

Computer Vision

-

Natural Language Processing

-

Robotics

-

Generative AI

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Consumer Electronics

-

Automotive

-

Healthcare

-

Aerospace and Defense

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Hardware Component

Revenue capture definition

Processors

As the largest hardware component segment, processors capture revenue generated from AI-focused computing processors, and application-specific integrated circuits (ASICs) used for AI training and inference workloads. Revenue includes sales of standalone processors and integrated compute chips deployed across data centers, edge devices, enterprise systems, and high-performance computing environments.

Memory

This segment captures revenue derived from memory components that support AI workloads, including high-bandwidth memory (HBM), DRAM, SRAM, and other advanced memory technologies. Revenue includes memory solutions integrated into AI servers, accelerators, and computing platforms to enable high-speed data access and efficient model processing.

Storage

This segment captures revenue generated from storage hardware used for AI data management, including solid-state drives (SSDs), hard disk drives (HDDs), and high-performance storage arrays. Revenue includes storage systems deployed for handling large-scale datasets, model training data, inference outputs, and enterprise AI workloads.

Network

Captures revenue from networking hardware that enables data transfer and communication within AI infrastructure, including switches, routers, network interface cards (NICs), interconnects, and optical networking equipment. Revenue includes products supporting high-speed connectivity across AI clusters, cloud environments, and distributed computing architectures.

Specialized Embedded Hardware

Revenue generated from embedded AI hardware integrated into end devices, including AI-enabled microcontrollers, system-on-chips (SoCs), field-programmable gate arrays (FPGAs), and edge AI modules. Revenue includes hardware deployed in automotive systems, industrial automation equipment, consumer electronics, robotics, healthcare devices, and IoT applications for localized AI processing.

Segment - Application

Revenue capture definition

Machine Learning/Deep Learning

This segment captures revenue generated from AI hardware deployed for machine learning and deep learning model training, optimization, and inference across enterprise, cloud, and research environments. Revenue includes processors, accelerators, memory, and supporting infrastructure used to execute predictive analytics, pattern recognition, recommendation systems, and advanced neural network workloads.

Computer Vision

This segment captures revenue derived from AI hardware supporting image recognition, video analytics, object detection, and visual inspection applications. Revenue includes hardware integrated into surveillance systems, industrial automation equipment, healthcare imaging solutions, and smart devices requiring visual data processing.

Natural Language Processing

Revenue generated from language understanding, speech recognition, language translation, and conversational AI applications in AI hardware. Revenue includes computing infrastructure supporting the training and deployment of NLP models.

Robotics

AI hardware deployed in autonomous and semi-autonomous robotic systems used across various industries generates revenue, which includes processors, embedded AI modules, sensors, and edge computing components for decision-making, and task execution capabilities.

Generative AI

This segment supports the training and inference of generative AI models used for content creation, code generation, and multimodal applications. Revenue includes high-performance processors, accelerators, memory solutions, and networking infrastructure deployed in data centers, cloud platforms, and enterprise AI environments.

Segment - End Use

Revenue capture definition

Consumer Electronics

This segment includes smartphones, laptops, tablets, smart speakers, wearables, smart TVs, and home automation products. Revenue includes processors, AI accelerators, embedded chips, and related components that enable voice recognition, personalization, image processing, and intelligent device functionality.

Automotive

Revenue derived from AI hardware deployed in vehicles for ADAS, predictive maintenance, and in-vehicle intelligence. Revenue includes AI processors, sensors, embedded computing platforms, and edge hardware supporting vehicle perception, navigation, and decision-making functions.

Healthcare

Segment captures revenue generated from medical imaging, diagnostics, drug discovery, robotic surgery, and clinical decision-support applications. Revenue includes high-performance computing systems, AI accelerators, and embedded hardware integrated into healthcare devices and medical infrastructure.

Aerospace and Defense

This segment captures revenue from AI hardware utilized in defense systems and aerospace operations. In which, revenue includes specialized processors, edge computing systems, ruggedized AI hardware, and mission-critical computing infrastructure designed for high-reliability environments.

Others

The others segment captures revenue generated from industries such as manufacturing, retail, telecommunications, energy, agriculture, financial services, and logistics. Revenue includes computing, storage, networking, and embedded AI hardware supporting industry-specific automation, analytics, and operational intelligence applications.

Estimation Model

AI Workload Layer

Infrastructure Layer

Deployment Layer

Monetisation Layer

Who Needs AI Computing?

Who Buys AI Hardware?

What Components Get Deployed?

How much revenue is generated?

Identify organizations and applications-cloud, enterprise, government, and research environments-that establish the demand for AI training, inference, automation, and generative AI workloads.

Apply AI infrastructure adoption rates across data centers, cloud, enterprise IT, edge networks, and embedded devices to identify organizations actively investing in AI hardware.

Apply hardware penetration rates across AI processors, accelerators, memory, storage, networking, and embedded modules to estimate deployed hardware and installed computing capacity.

Multiply hardware units by average selling prices (ASPs) and add revenue generated from AI servers, accelerators, networking, and edge devices to derive the total AI hardware market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Entry & Expansion Assessment

Regional demand sizing and forecasting

Customer segmentation and buying behavior analysis

Competitive landscape benchmarking

Regulatory and distribution channel assessment

Identified high-growth market opportunities

Supported go-to-market strategy development

Highlighted investment priorities and risks

Enabled data-driven expansion planning

Technology & Innovation Assessment

Emerging technology trend analysis

Innovation pipeline

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Product Positioning & Competitive Intelligence

Product benchmarking and feature comparison

Pricing and value proposition analysis

Brand perception and customer preference study

Competitor strategy evaluation

Improved product differentiation strategy

Supported pricing optimization

Identified unmet customer needs

Enhanced competitive positioning

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The global AI hardware market size was estimated at USD 115.4 billion in 2025 and is expected to reach USD 151.3 billion in 2026.

The global AI hardware market is expected to grow at a compound annual growth rate of 24.2% from 2026 to 2033 to reach USD 691.0 billion by 2033.

Key factors that are driving the market growth include the rising demand for high-performance computing, rapid expansion of data centers, increasing adoption of AI in edge devices, continuous advancements in semiconductor design, and growing investments in AI-driven applications across industries.

The Processors segment led with a 54.5% revenue share in 2025, while Specialized Embedded Hardware is the fastest growing segment.

Machine Learning/Deep Learning held the largest revenue share in 2025, while Generative AI is the fastest growing segment.

The Consumer Electronics segment led with a 27.5% revenue share in 2025, while Automotive is the fastest growing segment.

North America dominated the AI hardware market with a share of 31.9% in 2025. This is attributable to strong semiconductor manufacturing capabilities, significant investments in AI infrastructure, and early adoption of advanced computing technologies across industries.

Some key players operating in the AI hardware market include Advanced Micro Devices, Inc. (AMD), Amazon.com, Inc., Apple Inc., Cerebras Systems Inc., Graphcore, Intel Corporation, Microsoft, NVDIA Corporation, Qualcomm Incorporated, Robert Bosch GmbH

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.