- Home

- »

- Next Generation Technologies

- »

-

Architecture, Engineering & Construction Software Market Report, 2026-2033GVR Report cover

![Architecture, Engineering, And Construction Software Market (2026 - 2033)Report]()

Architecture, Engineering, And Construction Software Market (2026 - 2033)

Size, Share, & Trends Analysis Report By Type, By Deployment (Cloud, On-premise), By Application (Architectural Design, Structural Engineering, Construction Management), By End Use, And Segment Forecasts

Market Size, 2025

$11.9BMarket Estimate, 2026

$14.2BMarket Forecast, 2033

$39.1BCAGR, 2026–2033

15.5%Architecture, Engineering, And Construction Software Market Summary

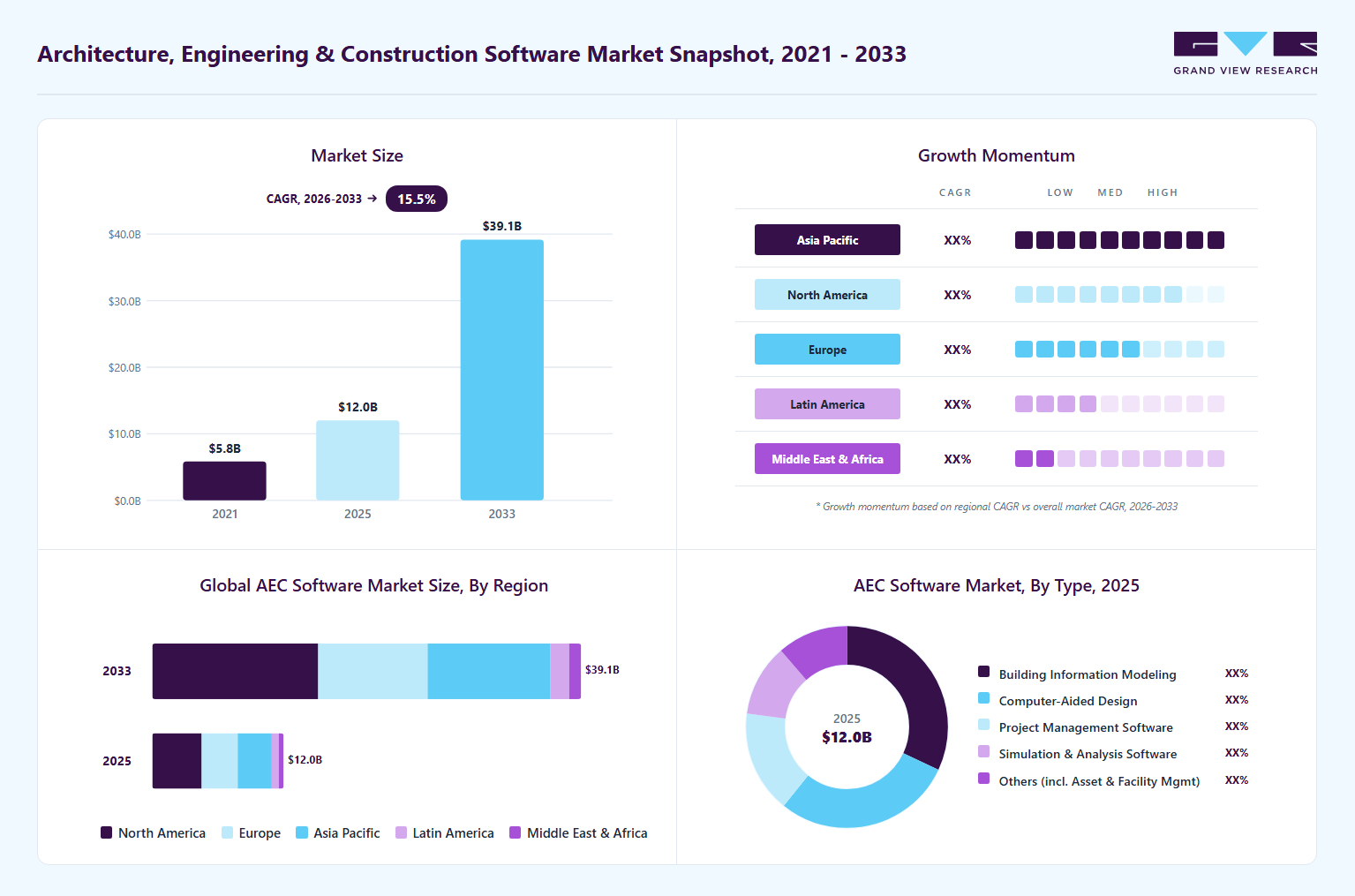

The global architecture, engineering, and construction software market size was valued at USD 11.9 billion in 2025 and is projected to grow from USD 14.2 billion in 2026 to USD 39.1 billion by 2033, at a CAGR of 15.5% from 2026 to 2033. The market in North America dominated with a revenue share of 37.6% in 2025. The increasing use of 3D modeling and simulation technologies is driving market growth.

Key Market Trends & Insights

- By type: Building information modeling segment held the largest market share of 31.9% in 2025.

- By application: Architectural design segment held the largest market share in 2025.

- By deployment: Cloud segment held the largest market share in 2025.

- By end use: Architects & designers segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (37.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 11.9 Billion

- Estimated market size in 2026: USD 14.2 Billion

- Projected market size by 2033: USD 39.1 Billion

- CAGR (2026-2033): 15.5%

The rapid adoption of building information modeling (BIM) and digital design technologies across the industry is driving market growth. BIM allows professionals to create detailed 3D models that integrate architectural, structural, and mechanical elements into a single platform. This improves coordination between different teams and reduces design conflicts. AEC software that supports BIM enables real-time collaboration and data sharing, enhancing productivity. It also allows for better cost estimation, scheduling, and lifecycle management of projects. Governments and large organizations are increasingly mandating the use of BIM for public infrastructure projects. This is accelerating the adoption of advanced AEC software solutions. The shift from 2D drawings to intelligent 3D modeling represents a major transformation in the industry.")

The rising demand for sustainable, energy-efficient building practices is also driving market growth. Governments and organizations are placing greater emphasis on reducing environmental impact and improving energy efficiency in construction. AEC software enables simulation and analysis of building performance, helping designers optimize energy use and material selection. This supports the development of sustainable building designs that meet regulatory requirements. Computer-Aided Design tools also help track environmental metrics and ensure compliance with green building standards. This reduces the risk of penalties and enhances project credibility. Sustainable construction practices are becoming a key differentiator in the market. As environmental concerns continue to grow, the adoption of AEC software is increasing.

The growing adoption of prefabrication and modular construction techniques is also driving the AEC software market. These construction methods require precise planning, design, and coordination to ensure types fit together correctly on-site. AEC software enables detailed modeling and simulation, which are essential for prefabrication processes. It helps optimize design for manufacturing and assembly, reducing material waste and construction time. Digital tools also facilitate coordination between design teams and manufacturing units. This ensures that prefabricated types meet required specifications and quality standards. Modular construction is becoming increasingly popular due to its efficiency and cost advantages. As these methods gain traction, the need for advanced design and planning software is rising. This drives the adoption of AEC solutions.

The rising demand for customization and client-specific design solutions is also contributing to market growth. Clients are increasingly seeking unique and tailored designs that meet their specific requirements. AEC software enables architects and engineers to create flexible and customizable designs efficiently. Advanced modeling tools enable rapid modification and visualization of different design options. This improves client engagement and satisfaction by providing a clear understanding of the final outcome. Customization also adds value to projects and differentiates service providers in a competitive market. Computer-Aided Design tools help manage design changes without significantly impacting timelines or costs. This enhances overall project efficiency. As demand for personalized solutions grows, the adoption of AEC software is increasing.

Market Dynamics

The rising demand for digital twin technology is a key driver in the architecture, engineering, and construction software industry, as project stakeholders increasingly look beyond design and construction toward full asset lifecycle optimization. Traditional construction workflows often focused primarily on project completion, but modern infrastructure owners now want continuous visibility into how buildings, industrial facilities, transportation systems, and utilities perform over time. Digital twin technology allows software platforms to create living digital models that continuously reflect the real-world condition of physical assets through integrated operational data. This capability enables owners, operators, engineers, and maintenance teams to monitor asset behavior, detect inefficiencies, and make informed operational decisions throughout the asset’s lifespan. As organizations shift from project-based thinking toward lifecycle value creation, software solutions that support digital twins are experiencing stronger demand.

According to Hexagon’s Digital Twin Industry Report, digital twins are gaining strong recognition across the built environment, with 91% of architects and building managers acknowledging their value in improving asset performance and operational visibility. Their adoption can reduce building carbon emissions by up to 50%, making them a critical tool for sustainability and decarbonization initiatives, while also improving building operations and maintenance efficiency by nearly 35%. This is especially significant as the World Economic Forum highlights that buildings account for over 30% of total U.S. emissions, positioning digital twins, combined with AI-driven analytics, as an important solution for optimizing building management, enhancing energy efficiency, and strengthening ESG reporting capabilities.

High initial implementation and subscription costs represent a major restraint on the Architecture, Engineering, and Construction software industry, as many construction and engineering firms operate under tight, project-based budgets. Advanced AEC software platforms often require significant upfront investment in licenses, cloud infrastructure setup, system integration, and workforce training. For small and mid-sized construction firms, these costs can be difficult to justify, especially when project margins are already under pressure. Even subscription-based pricing models can become expensive over time as firms scale usage across multiple projects and teams. This creates hesitation among potential users who may continue to rely on traditional tools or partially digitized workflows rather than fully adopt software. As a result, cost barriers slow down the pace of digital transformation across a large portion of the industry.

The increasing adoption of modular and prefabricated construction workflows is creating a major opportunity for the architecture, engineering, and construction software industry, as these methods rely heavily on precise digital planning and coordination before physical assembly begins. Unlike traditional construction, where adjustments can be made on-site, modular construction requires that building components be designed, engineered, and manufactured with high accuracy in controlled factory environments. This shift increases the importance of advanced AEC software tools that can manage detailed design specifications, component standardization, and manufacturing-ready models. This creates a strong opportunity for software providers to expand their solutions into factory-based and off-site construction ecosystems. According to Mesocore, prefab homes are generally 10-20% less expensive than conventional construction methods and can generate overall cost savings of up to 30%. This cost advantage is primarily driven by significantly lower per-square-foot pricing: prefab housing averages around USD 87, compared to approximately USD 166 for traditional site-built homes. In addition to cost efficiency, modular construction is gaining traction due to its sustainability benefits. These buildings can deliver up to 15% higher energy efficiency than conventional structures.

Market Concentration & Characteristics

The AEC software industry is highly concentrated, with a strong presence of global enterprise software providers alongside several niche design, modeling, and construction technology vendors. Leading players such as Autodesk and Bentley Systems dominate significant portions of the market due to their deeply embedded design ecosystems, extensive product suites covering BIM, structural design, project management, and infrastructure lifecycle management, and long-standing relationships with architecture firms, engineering consultancies, and large construction contractors. These companies benefit from high switching barriers created by proprietary file formats, established design workflows, and widely adopted collaboration platforms that are entrenched across project stakeholders. In addition, the market is characterized by long project cycles, high customization requirements, and strong dependency on interoperability across multiple stakeholders and software ecosystems. From a competitive standpoint, the AEC software market exhibits strong vendor lock-in due to deep integration into design and construction workflows, extensive training investments, and long-term project dependencies.

Type Insights

The building information modeling segment accounted for the largest market share of 31.9% in 2025. The growing need for efficient project scheduling and time management is contributing to segment growth. BIM supports 4D modeling, which integrates time-related data with 3D design models. This allows project teams to visualize construction sequences and timelines more effectively. Improved scheduling helps identify potential delays and optimize workflows. It also enhances coordination between different construction activities. Real-time updates ensure that all stakeholders are aligned with project timelines. This reduces the risk of delays and improves overall project efficiency. Better time management leads to faster project completion and cost savings. As companies focus on delivering projects on time, BIM becomes an essential tool.

The computer-aided design segment is anticipated to grow at the fastest CAGR during the forecast period. The growing importance of customization and development services is driving the services segment growth. Architecture, Engineering, and Construction Software platforms provide flexibility, but this often requires custom development to fully realize their potential. Organizations need tailored solutions that align with their specific workflows, branding requirements, and customer engagement strategies. Development service providers build custom APIs, front-end applications, and integrations that extend the functionality of architecture, engineering, and construction software platforms. This enables businesses to create unique digital experiences that differentiate them in the market.

Application Insights

The architectural design segment dominated the market in 2025. The growing importance of 3D visualization and immersive design experiences in architectural workflows is driving segment growth. Clients increasingly want to see realistic representations of buildings before construction begins. AEC software provides powerful 3D modeling, rendering, and visualization tools that bring designs to life. Architects can create virtual walkthroughs and interactive models to showcase their concepts. This improves client engagement and decision-making by providing a clear understanding of the final outcome. Visualization also helps identify design issues early in the process. It enhances collaboration between architects, engineers, and clients by providing a shared visual reference. Realistic rendering improves marketing and presentation of projects. As visualization becomes a critical component of design, the demand for architectural software solutions is rising.

The construction management segment is expected to register the fastest CAGR from 2026 to 2033. The increasing adoption of mobile and cloud technologies in construction management is driving the adoption of these technologies. On-site teams require access to project data, drawings, and updates in real time. Construction management software with mobile capabilities allows field workers to access information directly from their devices. This improves communication between on-site and office teams. Cloud-based platforms enable real-time data synchronization across locations. This reduces delays caused by manual data transfer and outdated information. Mobile access enhances productivity and ensures that decisions are based on current data. It also supports remote project monitoring and management. As digital connectivity improves, the adoption of mobile-enabled construction management solutions is increasing.

Deployment Insights

The cloud segment dominated the market in 2025. The growing complexity of construction projects and the need for integrated workflows are driving the cloud segment. Modern projects require seamless integration of design, planning, and execution processes. Cloud-based AEC software supports integration with other tools such as BIM, CAD, and project management systems. This creates a unified platform for managing all aspects of a project. Integrated workflows reduce duplication of effort and improve efficiency. They also enhance data consistency across the project lifecycle. Real-time data synchronization ensures that changes are reflected across all systems. This improves decision-making and project outcomes. As projects become more complex, the need for integrated cloud solutions continues to grow.

The on-premise segment is expected to register a significant CAGR from 2026 to 2033. The requirement for customization and integration with existing enterprise systems is a key driver for the on-premises segment. Many organizations have legacy systems and workflows that are deeply integrated into their operations. On-premises AEC software can be customized to align with these specific requirements. This includes integration with internal databases, ERP systems, and proprietary tools. Customization ensures that software supports unique business processes without requiring major operational changes. It also allows companies to maintain consistency across different systems. Tailored solutions improve efficiency and user adoption. Organizations can implement updates and modifications at their own pace. As businesses prioritize flexibility in system design, on-premises solutions remain relevant.

End Use Insights

The architects & designers segment accounted for the largest market share in 2025. The growing demand for building information modeling (BIM) is propelling market growth throughout the architects & designers segment. BIM-based software enables architects to create intelligent digital building models containing detailed information about structural components, materials, mechanical systems, electrical layouts, and construction sequences within a unified environment. These comprehensive models improve coordination among architects, engineers, contractors, and project owners by allowing all stakeholders to work from a shared digital representation of the project. Early identification of design conflicts improves project accuracy while reducing construction delays and budget overruns. The expanding use of BIM methodologies continues to strengthen demand for advanced AEC software.

The construction segment is anticipated to register the fastest CAGR during the forecast period. The growing complexity of supply chain and material management in construction is driving the demand for AEC software. Projects require careful coordination of materials, equipment, and suppliers to ensure timely execution. AEC software helps streamline procurement processes and manage inventory efficiently. It provides real-time tracking of materials and ensures availability when needed. This reduces delays caused by supply shortages and improves project timelines. Efficient material management also minimizes waste and reduces costs. Integration with supplier systems enhances transparency and coordination. As supply chains become more complex, the need for integrated management solutions continues to grow.

Regional Insights

North America dominated the AEC software industry, accounting for 37.6% of revenue in 2025, driven by the region’s highly advanced construction and infrastructure ecosystem, which demands sophisticated digital tools for efficient project execution. Construction projects in this region are often large-scale, technically complex, and involve multiple stakeholders across different phases. Managing such projects using traditional methods creates inefficiencies, delays, and cost overruns. AEC software enables centralized coordination, real-time data sharing, and streamlined workflows, significantly improving project outcomes. Companies benefit from enhanced visibility into project progress, enabling better decision-making and risk management. The need to handle complex engineering designs and integrate multidisciplinary teams further strengthens the reliance on digital platforms. High expectations for quality and precision also push firms toward advanced software solutions. The region’s mature market environment encourages continuous improvement in construction practices. As project complexity continues to rise, the adoption of AEC software across North America is expanding steadily.

U.S. Architecture, Engineering, and Construction Software Market Trends

The U.S. AEC software industry is projected to grow significantly during the forecast period. The growing investment in infrastructure development and renovation in the U.S. is driving market growth. Aging infrastructure across the country requires modernization and expansion. This creates demand for efficient planning, design, and execution tools. AEC software supports these projects by improving coordination, resource management, and scheduling. It enables better planning and reduces the risk of delays and cost overruns. Government and private sector investments further stimulate market growth. Infrastructure projects often involve complex requirements that necessitate advanced digital solutions. Efficient execution is critical for meeting deadlines and budgets. As infrastructure spending continues, the adoption of AEC software is expanding.

Asia Pacific Architecture, Engineering, and Construction Software Market Trends

The AEC software industry in Asia Pacific is expected to grow at the fastest CAGR from 2026 to 2033. The rising demand for sustainable and energy-efficient construction practices is contributing to the growth of the market in the Asia Pacific. Environmental concerns and regulatory requirements are encouraging the adoption of green building practices. AEC software enables analysis of energy performance, material usage, and environmental impact during the design phase. This helps architects and engineers optimize buildings for sustainability. Sustainable designs reduce long-term operational costs and improve environmental performance. Governments and organizations are promoting eco-friendly construction to address climate challenges. Software tools support compliance with sustainability standards and certifications. This enhances the value and attractiveness of projects. As sustainability becomes a priority, the demand for AEC software is increasing.

The AEC software industry in China is projected to grow significantly during the forecast period. The rapid development of smart cities and digital infrastructure in China is driving market growth. The country is investing heavily in technology-driven urban development projects that require advanced planning and execution tools. AEC software supports these initiatives by enabling integrated design and management of complex systems. It helps coordinate various components such as transportation, utilities, and buildings. Digital tools improve efficiency and reduce the risk of errors in large-scale projects. Smart city development requires seamless integration of multiple technologies, and AEC software facilitates this integration. This enhances overall project performance and sustainability. As smart city initiatives expand, the demand for AEC software continues to grow.

Europe Architecture, Engineering, and Construction Software Market Trends

The AEC software industry in Europe is anticipated to grow steadily from 2026 to 2033. The growing need to renovate and modernize aging infrastructure in Europe is contributing to market adoption. Many countries in the region have well-established infrastructure that requires upgrades to meet modern standards. Renovation projects are often more complex than new construction because the require integrating new systems with existing structures. AEC software provides tools for accurate modeling, analysis, and planning of such projects. It enables better visualization of existing conditions and supports efficient redesign. Digital tools help reduce errors and improve coordination during renovation activities. This ensures minimal disruption and better resource utilization. Governments and private organizations are investing heavily in infrastructure modernization. Efficient project execution is critical to meet timelines and budgets. As renovation activities increase, the adoption of AEC software is expanding.

The AEC software industry in the UK is expected to grow significantly during the forecast period. The increasing investment in infrastructure development and urban planning in the UK is driving market growth. The government and private sector are focusing on expanding transportation networks, housing, and urban infrastructure. These projects require efficient planning, design, and execution tools. AEC software supports these initiatives by improving coordination and resource management. It enables better scheduling and reduces the risk of delays. Infrastructure projects often involve large budgets and strict timelines. Efficient execution is critical for success. Software tools help ensure that projects are completed within scope and budget. As infrastructure investment continues, the adoption of AEC software is expanding.

Key Architecture, Engineering, And Construction Software Company Insights

Some prominent players in the architecture, engineering, and construction software market include Autodesk, Inc. and Nemetschek Group, among others.

-

Autodesk, Inc. is a global software company specializing in design, engineering, and digital content creation technologies. Autodesk provides a comprehensive and integrated portfolio of solutions that facilitate design, modeling, simulation, and project management. Its offerings include advanced tools for building information modeling (BIM), 3D design, drafting, and structural analysis, enabling professionals to create highly detailed digital representations of buildings and infrastructure projects. These solutions allow architects, engineers, and contractors to collaborate in real time, improve design accuracy, detect potential issues early, and optimize project execution.

-

Nemetschek Group is a Germany-based global software provider specializing in solutions for the architecture, engineering, construction, and media industries. Nemetschek Group offers a broad, diversified portfolio spanning design, modeling, planning, construction execution, and facility management. Its solutions include tools for building information modeling (BIM), 3D design, structural engineering, project planning, cost estimation, and asset lifecycle management. By enabling the creation of detailed digital building models and facilitating collaboration across stakeholders, Nemetschek’s software helps improve design accuracy, reduce errors, and enhance project efficiency.

Key Architecture, Engineering, And Construction Software Companies:

The following key companies have been profiled for this study on the architecture, engineering, and construction software market.

- AEC Group, LLC

- AEC Software, Inc.

- Autodesk Inc.

- DiRoots, LDA

- Egnyte, Inc.

- e-verse

- Monograph Inc.

- Nemetschek Group

- Oracle Corporation

- Pinnacle Infotech

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Autodesk Inc.; Nemetschek Group; Oracle Corporation; Pinnacle Infotech

- Mature players in the AEC software market focus on integrated BIM-based ecosystems that connect design, engineering, and construction workflows. They invest heavily in cloud platforms, digital twins, and lifecycle management solutions.

- Their strategy emphasizes end-to-end project integration across infrastructure and building assets. They also expand through enterprise contracts and cross-industry applications.

- Mature players benefit from strong global adoption and deeply embedded industry standards. Their BIM and design platforms are widely used in large-scale infrastructure and construction projects.

- High R&D investment enables advanced simulation, AI-based design, and real-time collaboration tools. Strong ecosystem lock-in creates high switching costs for users.

- Mature players often face high implementation costs and complex deployment requirements. Their platforms require skilled users and strong IT infrastructure.

- Integration across multiple tools can be time-consuming and technically challenging. Slower innovation cycles reduce agility compared to emerging SaaS competitors.

Emerging Players: AEC Group, LLC; DiRoots; LDA; Egnyte, Inc.; e-verse; Monograph Inc.

- Emerging players focus on cloud-native, mobile-first, and SaaS-based construction management platforms. They prioritize real-time collaboration, field data capture, and simplified project tracking tools.

- Many integrate AI, computer vision, and drone-based monitoring for construction progress. Their solutions are designed for fast deployment and ease of use..

- Emerging players compete through simplicity, agility, and faster deployment compared to legacy systems. They provide cost-effective tools tailored to mid-sized contractors and developers.

- Their platforms focus on solving specific pain points like site tracking and project coordination. Strong UX design and cloud accessibility improve adoption speed.

- Emerging players lack full lifecycle integration across design, construction, and operations. Their dependence on third-party BIM and design ecosystems limits independence.

- Weak global brand recognition restricts access to large enterprise projects. Limited capital also constrains long-term innovation and global scaling.

Recent Developments

-

In April 2026, Nemetschek Group acquired Heavy Construction Systems Specialists, LLC, which will now be integrated into its Build & Construct segment. By combining these solutions, the Build & Construct segment aims to improve collaboration and enhance the overall quality of construction workflows across both office and field environments. The inclusion of HCSS is expected to further strengthen this portfolio, enabling more seamless collaboration and improved process optimization across various project phases and types. This acquisition also supports Nemetschek Group’s broader strategy of expanding and reinforcing its business model, while solidifying its position as a key player in the global AEC software market.

-

In April 2026, Graphisoft, the developer of BIM software for the architecture and design industry, has strengthened its presence in the Pacific region through acquiring its distributor partners in Australia and New Zealand. The company acquired the Graphisoft Australia and Central Innovation New Zealand from Central Innovation, strengthening its customer engagement and improving service capabilities across two of the region’s key BIM markets. By bringing these operations under direct control, Graphisoft is better positioned to deliver services and support to its customers with the infrastructure and resources required.

-

In February 2026, Nemetschek Group signed a strategic partnership agreement with Ingram Micro to accelerate digital transformation and unlock new business opportunities across the Middle East and North Africa. As part of this agreement, Nemetschek’s software portfolio will be integrated with Ingram Micro’s extensive regional presence, partner network, and market expertise to drive wider adoption of digital solutions within the AEC software industry. The collaboration will emphasize joint market development initiatives, including coordinated marketing campaigns, participation in industry events, and enhanced customer engagement activities, alongside comprehensive sales enablement and training programs for Ingram Micro’s regional teams.

Architecture, Engineering, And Construction Software Market Report Scope

Report Attribute

Details

Market size in 2025

USD 11.9 billion

Estimated market size in 2026

USD 14.2 billion

Projected market size by 2033

USD 39.1 billion

Growth rate

CAGR of 15.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Type, deployment, application, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

AEC Group, LLC; AEC Software, Inc.; Autodesk Inc.; DiRoots; LDA; Egnyte, Inc.; e-verse; Monograph Inc.; Nemetschek Group; Oracle Corporation; Pinnacle Infotech

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Architecture, Engineering, And Construction Software Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global architecture, engineering, and construction software market report based on type, deployment, application, end use, and region.

-

Architecture, Engineering, and Construction Software Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Computer-Aided Design

-

Building Information Modeling

-

Project Management Software

-

Simulation & Analysis Software

-

Asset & Facility Management Software

-

Others

-

-

Architecture, Engineering, and Construction Software Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-premise

-

-

Architecture, Engineering, and Construction Software Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Architectural Design

-

Structural Engineering

-

Mechanical, Electrical & Plumbing Design

-

Construction Management

-

Project Planning & Scheduling

-

Others

-

-

Architecture, Engineering, and Construction Software End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Architects & Designers

-

Engineering Firms

-

Construction

-

Government

-

Others

-

-

Architecture, Engineering, and Construction Software Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

AEC Software Market Opportunity Assessment for a Construction Technology Provider

Assessment of digital transformation trends across architecture firms, engineering consultancies, and construction contractors

Analysis of operational challenges including fragmented project communication, design revision delays, documentation errors, and limited real-time collaboration

Evaluation of enterprise readiness for cloud-based design, project collaboration, document management, and integrated construction planning solutions

Identified high-potential customer segments seeking workflow digitization and project efficiency improvements

Supported solution positioning around collaboration, project transparency, and lifecycle visibility

Enabled prioritization of customer groups with stronger software adoption readiness and long-term digital investment potential

BIM and Project Lifecycle Software Strategy for an Engineering Software Developer

Analysis of customer requirements related to 3D modeling, design coordination, clash detection, project simulation, and lifecycle asset information management

Identification of pain points across design teams, consultants, and contractors including coordination gaps, rework costs, approval delays, and disconnected project data

Evaluation of demand for integrated workflows connecting design, procurement, construction execution, and facility management processes

Identified product capabilities with strongest demand across multidisciplinary project teams

Supported product roadmap development aligned with end-to-end project lifecycle management needs

Enabled differentiation through improved project coordination, design accuracy, and reduced execution risks

Construction Management Software Commercialization Strategy for a SaaS Platform Provider

Assessment of contractor and developer requirements related to cost estimation, scheduling, workforce coordination, compliance tracking, and field reporting

Analysis of adoption barriers including resistance to legacy workflow migration, integration complexity, training requirements, and budget constraints among small and mid-sized firms

Evaluation of customer expectations around mobile accessibility, real-time reporting, and centralized project visibility across distributed construction sites

Identified commercialization opportunities through subscription-based deployment and modular software adoption

Supported go-to-market strategy focused on solving field productivity and project control challenges

Enabled expansion into under-digitized construction segments looking for scalable and user-friendly software platforms

Frequently Asked Questions About This Report

Factors such as increasing use of 3D modeling and simulation technologies and expansion of smart city and urban development projects are the key factors driving the market growth.

The building information modeling segment led with a 31.9% revenue share in 2025, while the computer-aided design segment is the fastest-growing.

Which application segment dominated the architecture, engineering, and construction software market?The architectural design segment held the largest revenue share in 2025, while the construction management segment is the fastest-growing.

The cloud segment held the largest revenue share in 2025, while the on-premise segment is the fastest-growing.

The architects & designers segment held the largest revenue share in 2025, while the construction segment is the fastest-growing.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include AEC Group, LLC; AEC Software, Inc.; Autodesk Inc.; DiRoots; LDA; Egnyte, Inc.; e-verse; Monograph Inc.; Nemetschek Group; Oracle Corporation; Pinnacle Infotech

The global architecture, engineering, and construction software market size was valued at USD 12.0 billion in 2025 and is estimated at USD 14.2 billion for 2026.

The global architecture, engineering, and construction software market is expected to grow at a CAGR of 15.5% from 2026 to 2033, reaching USD 39.1 billion by 2033.

North America dominated with a 37.6% revenue share in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.