- Home

- »

- Plastics, Polymers & Resins

- »

-

Barrier Packaging Market Size And Share Report, 2026-2033GVR Report cover

![Barrier Packaging Market (2026 - 2033)Report]()

Barrier Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Plastic Films, Aluminum Foil, Paper & Paperboard, Metallized Films, Coated Materials), By End Use (Food & Beverage, Pharmaceuticals, Personal Care, Industrial), By Region, And Segment Forecasts

Market Size, 2025

$19.6BMarket Estimate, 2026

$20.3BMarket Forecast, 2033

$27.3BCAGR, 2026–2033

4.3%Barrier Packaging Market Summary

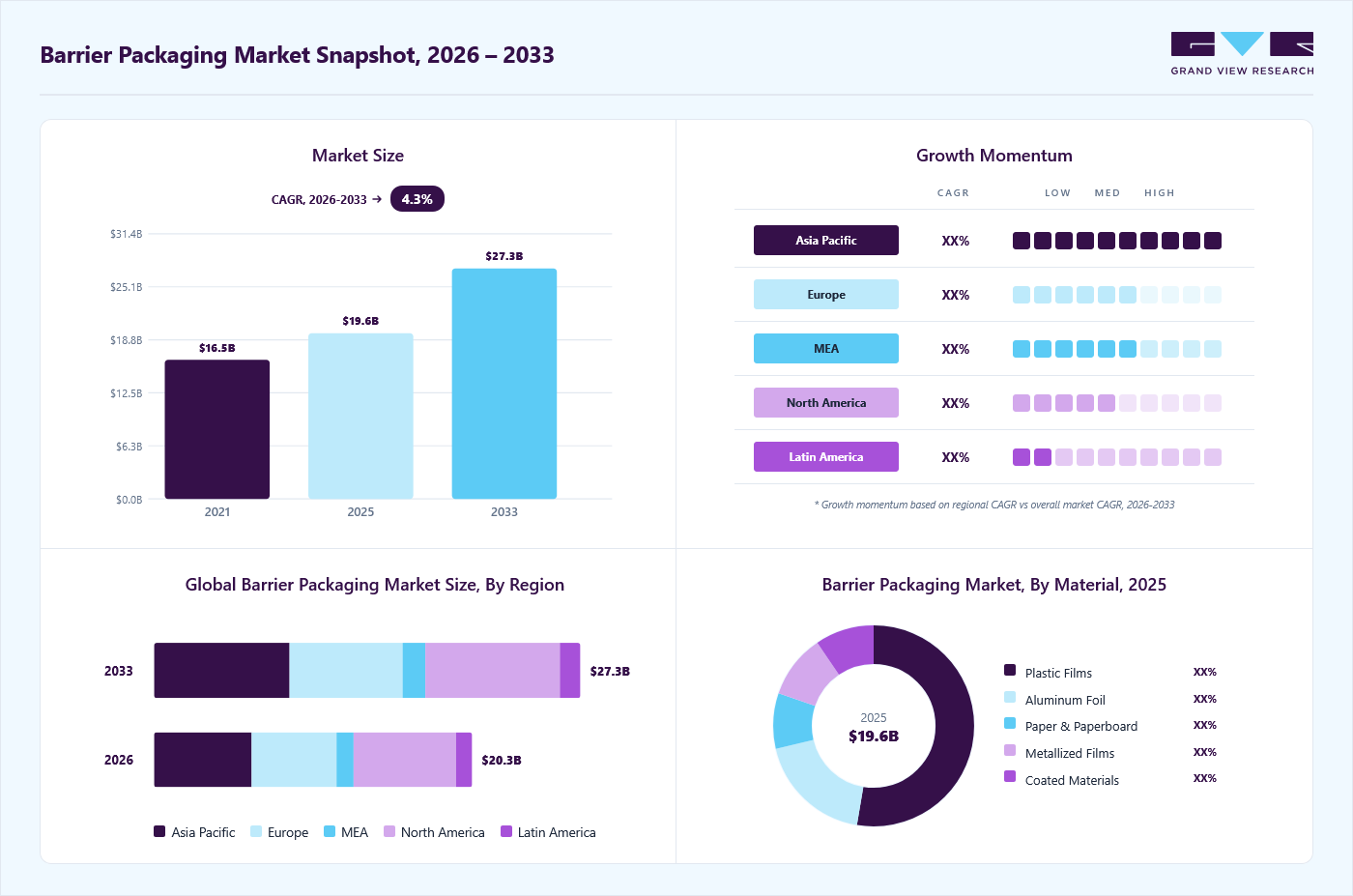

The global barrier packaging market size was valued at USD 19.6 billion in 2025 and is projected to grow from USD 20.3 billion in 2026 to USD 27.3 billion by 2033, at a CAGR of 4.3% from 2026 to 2033. North America dominated the market with the largest revenue share of 32.3% in 2025. One of the primary reasons for the rising demand for barrier packaging globally is the increasing need to extend the shelf life of products and preserve their quality across long supply chains.

Key Market Trends & Insights

- By material: Plastic films segment led the market with the largest revenue share of 52.6% in 2025.

- By end use: Food & beverages segment led the market with the largest revenue share of 56.3% in 2025.

Regional Highlights

- Largest regional market: North America (32.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 19.6 Billion

- Estimated market size in 2026: USD 20.3 Billion

- Projected market size by 2033: USD 27.3 Billion

- CAGR (2026-2033): 4.3%

Barrier packaging provides a protective shield against external elements such as oxygen, moisture, light, and contaminants, all of which can deteriorate the freshness, flavor, and safety of consumables, especially in food, beverage, and pharmaceutical products. As global trade expands and supply chains become more complex, products must travel longer distances and remain stable in varied climatic conditions. This has created a strong push for packaging materials that maintain product integrity, ensuring safety, hygiene, and extended usability. Consequently, both manufacturers and retailers are increasingly adopting barrier packaging to reduce spoilage, enhance shelf appeal, and minimize product returns or wastage.")

The explosive growth of the food and beverage industry, especially in emerging markets such as India, China, Brazil, and Indonesia, is a major factor driving the global demand for barrier packaging. Consumers today seek convenient, ready-to-eat, and on-the-go food formats that require longer storage times without refrigeration. Barrier packaging-through materials like multi-layer films, coated paper, and aluminum foils-prevents oxygen ingress and moisture loss, preserving the flavor, aroma, and texture of packaged foods and beverages. Moreover, in beverages such as juices, dairy, energy drinks, and alcoholic products, barrier packaging helps maintain carbonation and prevent oxidation, thus retaining freshness and quality. The growing consumption of processed foods and packaged beverages across urban and semi-urban regions continues to propel demand for advanced barrier solutions that balance performance, safety, and sustainability.

Modern consumers are increasingly drawn to on-the-go, portion-sized, and resealable packaging formats that fit their fast-paced lifestyles. Barrier packaging plays a crucial role in enabling such convenience-driven innovations by providing lightweight, flexible, and durable protection for food, pharmaceuticals, cosmetics, and personal care products. With the rise in dual-income households and increasing urbanization, consumers are demanding packaging that not only protects the product but also offers ease of handling, longer storage, and minimal mess or leakage. This consumer behavior shift has spurred innovation in flexible barrier films, pouches, and sachets, which are now replacing rigid packaging in many product categories. As a result, demand for barrier packaging continues to surge across both developed and developing economies.

Heightened awareness around food safety, contamination prevention, and traceability has accelerated the adoption of barrier packaging worldwide. Governments and regulatory agencies such as the U.S. FDA, EFSA, and FSSAI are enforcing stricter regulations on packaging materials to ensure that they do not interact negatively with the product or cause contamination. Barrier packaging materials-especially multi-layer laminates and coated polymers-are designed to comply with these safety norms, offering high resistance to microbial ingress and chemical migration. For pharmaceutical and nutraceutical products, the ability of barrier packaging to provide moisture-proof, tamper-evident, and contamination-resistant protection is particularly valuable. These regulatory requirements, coupled with rising consumer expectations for hygiene and authenticity, are significantly boosting the global demand in the barrier packaging industry.

Market Dynamics

The barrier packaging market is witnessing strong growth driven by rising demand for extended shelf-life packaging solutions across the food & beverage, pharmaceutical, personal care, industrial, and healthcare sectors. Increasing consumption of packaged foods, growing pharmaceutical production, and expanding global trade are fueling the need for packaging materials that effectively protect products from moisture, oxygen, light, aroma loss, and microbial contamination. The market is also benefiting from advancements in multilayer structures, high-performance films, coatings, and sustainable barrier technologies that improve product preservation while reducing material usage. However, challenges such as recyclability concerns of multi-material packaging, stringent environmental regulations, and fluctuating raw material prices continue to impact market growth. Nevertheless, innovations in recyclable mono-material barrier packaging, bio-based materials, and circular economy initiatives are creating significant opportunities for future market expansion.

The increasing demand for packaged foods, pharmaceuticals, and sensitive consumer products is a major driver for the Barrier Packaging Market. Barrier packaging materials are designed to protect products from external factors such as oxygen, moisture, light, odors, and contaminants, helping maintain product quality, freshness, efficacy, and safety throughout storage and transportation. Growing consumer preference for convenience foods, ready-to-eat meals, frozen products, and premium packaged goods has significantly increased the need for high-performance barrier solutions. In the pharmaceutical sector, stringent requirements for drug stability and product integrity are driving the adoption of advanced barrier packaging formats such as blister packs, pouches, sachets, and high-barrier films. Additionally, globalization of supply chains and the growth of e-commerce have increased transportation durations, making effective barrier protection critical for reducing spoilage, product loss, and waste. As manufacturers continue to prioritize product preservation and shelf-life extension, demand for barrier packaging solutions is expected to remain strong across multiple industries.

A major restraint for the barrier packaging market is the growing concern regarding the environmental impact and recyclability of conventional barrier packaging materials. Many high-performance barrier solutions utilize multilayer structures composed of different polymers, aluminum foil, adhesives, and coatings that are difficult to separate and recycle using existing waste management infrastructure. Governments worldwide are introducing stricter regulations aimed at reducing packaging waste, increasing recyclability requirements, and promoting circular economy practices. At the same time, consumers and brand owners are increasingly demanding environmentally responsible packaging alternatives. These pressures are forcing manufacturers to redesign packaging structures, invest in sustainable material innovations, and comply with evolving regulatory standards, often resulting in increased production costs and technical challenges. The complexity of balancing high barrier performance with recyclability remains a key challenge for market participants.

The growing focus on sustainability presents a significant opportunity for the barrier packaging market. Packaging manufacturers, brand owners, and material suppliers are actively investing in recyclable mono-material structures, bio-based polymers, water-based barrier coatings, and compostable packaging technologies that deliver high barrier performance while improving environmental sustainability. Advancements in material science are enabling the development of next-generation barrier packaging solutions that maintain protection against moisture, oxygen, and contaminants while supporting recycling and circular economy objectives. Increasing commitments from food, beverage, pharmaceutical, and consumer goods companies to reduce packaging waste and carbon footprints are accelerating the adoption of sustainable barrier technologies. Furthermore, innovations in chemical recycling, advanced coating technologies, and renewable packaging materials are expected to create substantial growth opportunities for manufacturers seeking to address both performance and sustainability requirements in the global packaging industry.

Market Concentration & Characteristics

The rapid growth of e-commerce has redefined packaging requirements globally. Products now need to be shipped over long distances, often passing through multiple handling stages and varying climatic conditions. Barrier packaging ensures that products remain intact, uncontaminated, and appealing upon delivery, making it a preferred choice for online retailers and logistics providers. The surge in cross-border trade and the globalization of supply chains have intensified the need for robust packaging that protects against temperature fluctuations, humidity, and rough handling. For perishable goods, pharmaceuticals, and personal care items, barrier packaging provides both functional protection and aesthetic value, helping brands maintain consistency in product quality and customer experience across regions.

Continuous innovation in material science has significantly improved the performance and cost-efficiency of barrier packaging. The development of multi-layer coextruded films, metallized foils, nanocoatings, and bio-based barrier polymers has expanded the applicability of barrier packaging across diverse industries. These innovations allow manufacturers to achieve superior gas and moisture resistance while reducing material thickness and improving recyclability. Moreover, advancements in active and intelligent packaging-which can monitor freshness, release preservatives, or absorb oxygen-are adding further value to barrier solutions. These technological upgrades not only enhance product protection but also align with sustainability goals, thus fueling demand from environmentally conscious brands and consumers alike.

Analyst Perspective

The barrier packaging market is expected to witness robust growth over the coming years, driven by increasing demand for product protection, shelf-life extension, and preservation of product quality across the food & beverage, pharmaceutical, personal care, and industrial sectors. As global supply chains become more complex and consumers increasingly favor packaged, convenient, and premium products, manufacturers are placing greater emphasis on high-performance packaging solutions that provide effective barriers against moisture, oxygen, light, aroma loss, and contamination. The market is further supported by the expansion of pharmaceutical production, growing demand for processed foods, and rising international trade activities that require reliable packaging to maintain product integrity throughout distribution.

Material Insights

Based on material, the plastic films segment led the market with the largest revenue share of 52.6% in 2025. It is expected to grow at a CAGR of 4.3% during the forecast period. Plastic films dominate the barrier packaging material segment because they offer an optimal balance between performance, flexibility, and cost-effectiveness. Materials such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), ethylene vinyl alcohol (EVOH), and polyamide (PA) provide exceptional barrier protection against oxygen, moisture, and aroma migration - critical for maintaining product quality. Unlike metal or glass, plastic films can achieve the same preservation benefits at a fraction of the cost and weight. This makes them the preferred choice for mass-market applications such as snacks, dairy, frozen foods, and ready-to-eat meals. Furthermore, the ability to fine-tune barrier properties by using multi-layer film structures allows packaging engineers to design solutions customized to specific product requirements, creating an unparalleled advantage for plastics over other materials.

Moreover, plastic films are inherently lightweight and flexible, offering substantial logistical and operational benefits. They reduce transportation costs, require less storage space, and are easier to handle during filling and sealing processes. The versatility of plastic films enables them to be used in a wide range of packaging formats, from pouches and wraps to blister packs and vacuum-sealed containers. These films also support high-quality printing, lamination, and embossing, which are essential for branding and visual appeal. This adaptability across industries, from food to pharmaceuticals and cosmetics, has made plastic films indispensable in the modern packaging landscape.

End Use Insights

Based on end use, the food & beverages segment led the market with the largest revenue share of 56.3% in 2025. The food and beverage industry accounts for the largest share of the barrier packaging market primarily because it relies heavily on protection, preservation, and presentation. Perishable food items such as meats, dairy, bakery products, snacks, and beverages require packaging that can prevent oxidation, moisture loss, and microbial contamination.

Barrier packaging materials, particularly plastic films and laminates, create an airtight environment that ensures freshness and maintains flavor integrity for extended periods. This functionality is essential for both shelf-stable and chilled food products, as it enables global distribution without compromising safety or quality. The growing consumer preference for packaged and processed foods has further accelerated demand in this segment.

Moreover, rapid urbanization, changing lifestyles, and an increase in dual-income households have transformed global eating habits. Consumers now prefer on-the-go, single-serve, and ready-to-eat meals, which require durable, lightweight, and protective packaging solutions. Barrier packaging fulfills these needs by offering flexible options like stand-up pouches, sachets, and resealable wraps that keep food fresh and portable. The demand for convenience-driven food formats, such as frozen meals, snack bars, and beverage pods, has surged, especially in North America, Europe, and Asia Pacific. This evolving consumer lifestyle is a primary reason why the food and beverage sector continues to dominate as the key end use market for barrier packaging.

Region Insights

North America dominated the barrier packaging market with the largest revenue share of 32.3% in 2025. The barrier packaging industry in North America is witnessing robust growth due to the strong presence of mature packaged food, beverage, and pharmaceutical industries, which demand advanced packaging materials to meet strict regulatory and safety standards. Consumers in the region prioritize convenience, freshness, and sustainability, driving innovation in high-performance multilayer films and recyclable materials. Moreover, the rapid expansion of e-commerce grocery delivery and meal kit services has increased the need for packaging that offers superior product protection during transit. Companies are also investing in smart and intelligent packaging technologies, integrating QR codes and freshness indicators to enhance consumer engagement. The strong emphasis on sustainable production practices and circular economy initiatives, particularly in the U.S. and Canada, further accelerates the adoption of recyclable and bio-based barrier materials.

U.S. Barrier Packaging Market Trends

The barrier packaging market in the U.S. held the largest share in the North America region in 2025. In the U.S., the market growth is primarily fueled by technological advancements in flexible packaging and increasing demand from the frozen and ready-to-eat food sectors. The country’s dynamic consumer lifestyle, coupled with a high preference for portion-controlled and on-the-go food formats, has significantly increased reliance on advanced barrier films that ensure product freshness. The pharmaceutical industry’s expansion, driven by the aging population and increased healthcare spending, has also created strong demand for moisture- and oxygen-resistant packaging. Moreover, investments in recycling infrastructure and government-backed initiatives, such as the U.S. Plastics Pact, are fostering innovation in sustainable materials. Local manufacturers are also focusing on lightweight, monomaterial solutions to align with extended producer responsibility (EPR) frameworks, making the U.S. one of the most progressive markets for barrier packaging development.

Asia Pacific Barrier Packaging Market Trends

Asia Pacific has emerged as the fastest-growing region in the global barrier packaging market, driven by rapid urbanization, expanding middle-class populations, and rising consumption of packaged food and beverages. Countries like India, China, Japan, and South Korea are experiencing a surge in demand for convenient, long-lasting, and visually appealing packaging formats due to evolving dietary habits and busy lifestyles. The booming pharmaceutical, personal care, and nutraceutical sectors are further accelerating demand for high-barrier materials to ensure product stability and hygiene. Additionally, Asia-Pacific’s cost-efficient manufacturing ecosystem and increasing foreign investments in packaging innovation hubs have strengthened regional competitiveness. The ongoing shift toward eco-friendly and recyclable packaging alternatives, supported by stricter environmental regulations and consumer awareness, continues to fuel market expansion across the region.

China’s barrier packaging marketgrowth is driven by massive domestic consumption, rapid retail modernization, and advancements in packaging technology. The country’s large-scale food processing and beverage industries rely heavily on barrier materials to meet shelf-life and safety requirements amid rising demand for convenience foods. Additionally, China’s dual focus on innovation and sustainability has resulted in significant research into bio-based films and recyclable laminates.

Europe Barrier Packaging Market Trends

Europe represents one of the most technologically advanced and sustainability-driven markets for barrier packaging. The region’s growth is largely fueled by strict environmental regulations, including the EU Packaging and Packaging Waste Directive and the Circular Economy Action Plan, which mandate recyclable and reusable packaging solutions. European consumers have a strong preference for eco-friendly and ethically produced goods, prompting manufacturers to adopt bio-based polymers, solvent-free laminates, and mono-material structures.

Germany’s barrier packaging market is expected to grow over the forecast period. Germany stands out as a leader in sustainable packaging innovation and technological integration, making it a key growth hub for the barrier packaging industry in Europe. The country’s strong industrial base and emphasis on engineering excellence have led to the development of sophisticated multi-layer films and recyclable laminates tailored for food, pharmaceutical, and industrial applications. Moreover, Germany’s consumers are highly sustainability-conscious, encouraging packaging producers to transition toward compostable, paper-based, and recyclable plastic alternatives.

Key Barrier Packaging Company Insights

The global barrier packaging market is characterized by intense competition, driven by continuous innovation, sustainability mandates, and growing consumer expectations for high-performance yet eco-friendly materials. The market is moderately consolidated, with leading players such as Amcor plc, Sealed Air Corporation, Mondi Group, Berry Global, Huhtamaki Oyj, and Constantia Flexibles dominating global production capacities. These companies compete on parameters such as material innovation, barrier efficiency, recyclability, and cost optimization, while regional manufacturers focus on price competitiveness and local customization.

-

In March 2024, Berry Global Group, Inc., and Mitsubishi Gas Chemical Company, Inc. (MGC) announced a partnership to launch a recyclable barrier solution for thermoformed articles, plastic jars, tubes, and bottles using MXD6, a superior barrier resin manufactured by MGC.

-

In July 2023, Mondi, a global leader in packaging and paper, invested USD 16.81 million in new and advanced technologies to develop a new packaging range called FunctionalBarrier Paper Ultimate. The ultra-high barrier paper-based food solution fulfills the growing customer demand for sustainable packaging that contributes to a circular economy.

Key Barrier Packaging Companies

The following are the leading companies in the barrier packaging market.

-

Amcor plc

-

Huhtamaki

-

Sealed Air

-

Graphic Packaging International, LLC

-

ProAmpac

-

Mondi

-

DS Smith

-

Coveris

-

TOPPAN Inc.

-

CarePac

-

ISOFlex Packaging

-

C-P Flexible Packaging

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Amcor plc, Huhtamaki, Sealed Air, Graphic Packaging International, LLC, ProAmpac, Mondi, DS Smith, Coveris, and TOPPAN Inc.)

- Invest heavily in advanced barrier packaging technologies, sustainable material development, and global manufacturing expansion to strengthen market leadership.

- Focus on acquisitions, strategic collaborations, product innovation, and integrated packaging solutions to serve multinational food, beverage, pharmaceutical, and consumer goods companies.

- Extensive global production footprints, diversified product portfolios, and established customer relationships enable broad market penetration across multiple end-use industries.

- Strong R&D capabilities support the development of high-performance barrier materials, recyclable packaging solutions, and regulatory-compliant products, enhancing competitive positioning.

- High capital expenditure requirements for manufacturing facilities, sustainability initiatives, and technology upgrades can pressure margins.

- Greater exposure to raw material price volatility, environmental regulations, and operational complexities associated with managing large global supply chains.

Emerging Players (CarePac, ISOFlex Packaging, and C-P Flexible Packaging)

- Focus on specialized barrier packaging solutions, customer-centric product customization, and niche market applications to establish market presence.

- Emphasize flexible manufacturing capabilities, shorter lead times, and tailored packaging designs to meet specific customer requirements across food, healthcare, and industrial sectors.

- Operational flexibility and customer responsiveness enable rapid adaptation to changing packaging requirements and emerging market trends.

- Ability to offer customized solutions and personalized service helps secure contracts in specialized applications where large manufacturers may be less agile.

- Limited production scale, geographic reach, and financial resources may restrict expansion opportunities and investment in advanced technologies.

- Lower brand recognition and smaller distribution networks can create challenges when competing for large-volume contracts against established global packaging companies.

Barrier Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 19.6 billion

Estimated market size in 2026

USD 20.3 billion

Projected market size by 2033

USD 27.3 billion

Growth rate

CAGR of 4.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Amcor plc; Huhtamaki; Sealed Air; Graphic Packaging International, LLC; ProAmpac; Mondi; DS Smith; Coveris; TOPPAN Inc.; CarePac; ISOFlex Packaging; C-P Flexible Packaging.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Barrier Packaging Market Report Segmentation

This report forecasts revenue growth at the global, regional & country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global barrier packaging market report based on material, end use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic Films

-

Aluminum Foil

-

Paper & Paperboard

-

Metallized Films

-

Coated Materials

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Food & Beverage

-

Pharmaceuticals

-

Personal Care

-

Industrial

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Material

Revenue capture definition

Plastic Films

Revenue generated from the sale of barrier packaging products manufactured using plastic-based films such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), polyamide (PA), ethylene vinyl alcohol (EVOH), and other high-barrier polymer films. Includes mono-layer and multilayer film structures used in pouches, sachets, wraps, lidding films, and flexible packaging applications.

Aluminum Foil

Revenue generated from barrier packaging solutions incorporating aluminum foil as the primary barrier material. Includes foil laminates, foil-based pouches, blister packaging, sachets, and pharmaceutical and food packaging applications requiring superior protection against moisture, oxygen, light, and contaminants.

Paper & Paperboard

Revenue generated from barrier packaging products utilizing paper and paperboard substrates with inherent or added barrier properties. Includes coated paper packaging, cartons, wraps, cups, trays, and sustainable packaging formats used across food, beverage, healthcare, and consumer goods industries.

Metallized Films

Revenue generated from packaging materials consisting of plastic films coated with a thin metallic layer, typically aluminum, to enhance barrier performance. Includes metallized PET, metallized BOPP, and related structures used in snack food packaging, confectionery packaging, coffee packaging, and industrial applications.

Coated Materials

Revenue generated from barrier packaging products utilizing specialized coatings such as water-based coatings, acrylic coatings, PVDC coatings, silicon oxide (SiOx), aluminum oxide (AlOx), and other functional barrier technologies applied to films, paper, or paperboard substrates to improve moisture, oxygen, grease, and aroma resistance.

Segment - Product

Revenue capture definition

Food & Beverage

Revenue generated from barrier packaging solutions used for food and beverage products, including dairy products, meat and seafood, frozen foods, ready-to-eat meals, snacks, confectionery, bakery products, beverages, coffee, tea, and pet food. Includes both flexible and rigid barrier packaging formats designed to extend shelf life and preserve product quality.

Pharmaceuticals

Revenue generated from barrier packaging products used in pharmaceutical and healthcare applications, including blister packs, sachets, pouches, strip packs, medical device packaging, diagnostic packaging, and drug delivery systems requiring protection from moisture, oxygen, light, and contamination.

Personal Care

Revenue generated from barrier packaging solutions used for cosmetics, skincare products, haircare products, fragrances, oral care products, and hygiene products. Includes packaging formats designed to protect formulations from degradation while maintaining product stability and consumer appeal.

Industrial

Revenue generated from barrier packaging products used in industrial and chemical applications, including packaging for lubricants, adhesives, agrochemicals, specialty chemicals, electronic components, and other industrial products requiring protection from environmental exposure during storage and transportation.

Others

Revenue generated from barrier packaging applications not covered under the above categories, including household products, home care products, consumer goods, tobacco products, and specialty packaging applications across various end-use industries.

Estimation Model

Layer Name

Key Question

Description

End-Use Consumption Layer

What forms the demand base?

Identify global consumption volumes of products requiring barrier packaging across major end-use industries, including food & beverage, pharmaceuticals, personal care, industrial products, household goods, and other consumer applications. This layer establishes the total addressable demand for barrier packaging based on product sensitivity to moisture, oxygen, light, aroma loss, contamination, and shelf-life requirements throughout storage, transportation, and retail distribution.

Barrier Packaging Penetration Layer

Where is barrier packaging utilized?

Estimate the penetration of barrier packaging relative to conventional packaging solutions across various applications and regions. Assess adoption rates of plastic films, aluminum foil, metallized films, paper & paperboard, and coated materials based on product protection requirements, shelf-life extension needs, regulatory compliance, sustainability objectives, transportation conditions, and cost-performance considerations.

Barrier Packaging Volume Layer

How much barrier packaging is consumed?

Analyze barrier packaging consumption volumes by material type, packaging format, and end-use industry. Evaluate demand for high-barrier pouches, sachets, wraps, lidding films, blister packs, bags, cartons, containers, and specialty barrier structures. Volume consumption is influenced by food production levels, pharmaceutical manufacturing output, consumer packaged goods demand, international trade activities, e-commerce growth, and packaging intensity across end-use sectors.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the sale of barrier packaging materials and solutions across diverse end-use industries. Revenue generation includes standard and customized packaging products manufactured from plastic films, aluminum foil, paper & paperboard, metallized films, and coated materials. Market growth is supported by increasing demand for shelf-life extension, product safety, contamination prevention, sustainable packaging solutions, advanced barrier technologies, recyclable structures, and value-added packaging features that enhance product performance and regulatory compliance.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation Analysis

Delivered detailed market sizing, growth forecasts, consumption trends, regulatory developments, sustainability initiatives, and end-use demand analysis across North America, Europe, Asia Pacific, Central & South America, and Middle East & Africa, including key country-level assessments within major barrier packaging markets.

Enabled identification of high-growth regions, evolving regulatory environments, packaging innovation hubs, and region-specific demand drivers to support market entry, expansion, and investment decisions.

Cross-Segmentation Analysis

Provided comprehensive analysis across Material (Plastic Films, Aluminum Foil, Paper & Paperboard, Metallized Films, Coated Materials), End Use (Food & Beverage, Pharmaceuticals, Personal Care, Industrial, Others), and Region. Assessed market size, growth potential, adoption trends, and application-level demand across each segment combination.

Delivered granular insights into the most attractive material-end use combinations, helping clients identify high-growth applications, emerging demand pockets, technology adoption trends, and portfolio optimization opportunities.

Opportunity Assessment

Identified emerging opportunities across recyclable barrier packaging solutions, mono-material structures, bio-based packaging materials, high-barrier coatings, pharmaceutical packaging expansion, sustainable food packaging, e-commerce packaging applications, and advanced shelf-life extension technologies.

Enabled prioritization of high-potential investment areas, product development initiatives, sustainability-focused innovations, and long-term growth strategies aligned with evolving customer and regulatory requirements.

Frequently Asked Questions About This Report

Food & beverages segment held the largest revenue share of 56.2 % in 2025.

The global barrier packaging market size was valued at USD 19.6 billion in 2025 and is estimated at USD 20.3 billion for 2026.

The global barrier packaging market is expected to grow at a CAGR of 4.3% from 2026 to 2033, reaching USD 27.3 billion by 2033.

Key factors driving the barrier packaging market include rising demand for packaged and convenience foods, growing pharmaceutical and healthcare production, increasing need for extended shelf-life and product protection, expanding global trade and e-commerce activities, and greater adoption of high-performance packaging solutions that provide protection against moisture, oxygen, light, and contamination.

The plastic films segment led the market with a 52.6% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players in the barrier packaging market include Amcor plc; Huhtamaki; Sealed Air; Graphic Packaging International, LLC; ProAmpac; Mondi; DS Smith; Coveris; TOPPAN Inc.; CarePac; ISOFlex Packaging; and C-P Flexible Packaging.

North America dominated the barrier packaging market with a 32.3% revenue share in 2025.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.