- Home

- »

- Advanced Interior Materials

- »

-

Beryllium Mining Market Size, Share, Industry Report, 2033GVR Report cover

![Beryllium Mining Market Size, Share & Trends Report]()

Beryllium Mining Market (2025 - 2033) Size, Share & Trends Analysis Report By Application (Form), By End Use (Aerospace & Defense, Electronics & Telecom, Automotive, Medical & Dental), By Region, And Segment Forecasts

Market Size, 2024

$10.7MMarket Estimate, 2026

$11.0MMarket Forecast, 2033

$13.9MCAGR, 2025–2033

2.9%Beryllium Mining Market Summary

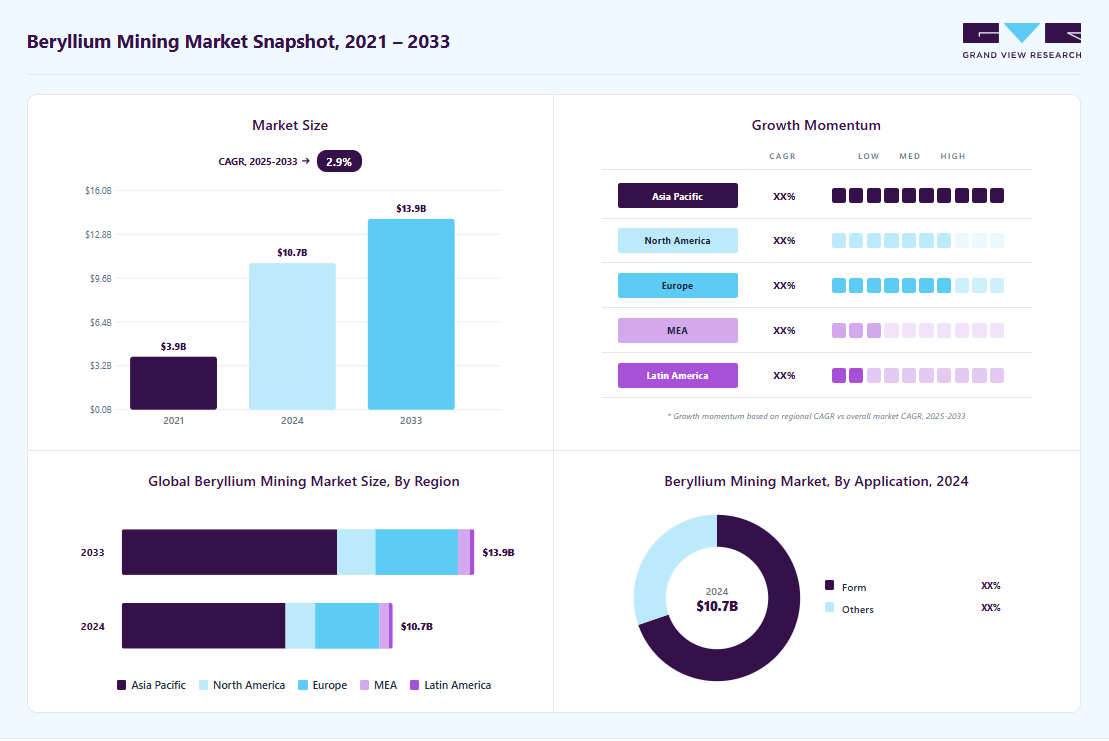

The global beryllium mining market size was estimated at USD 10.70 billion in 2024 and is projected to reach USD 13.92 billion by 2033, at a CAGR of 2.9% from 2025 to 2033. Beryllium is prized for its exceptional stiffness, light weight, and thermal stability, which keeps aerospace demand as the top growth driver for beryllium mining.

Key Market Trends & Insights

- Asia Pacific dominated the beryllium mining industry with the largest market revenue share of 60.3%.

- By application, the form segment is anticipated to register a CAGR of 2.8% from 2025 to 2033.

- By end use, electronics & telecom accounted for the largest market revenue share of over 37.5% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 10.70 Billion

- 2033 Projected Market Size: USD 13.92 Billion

- CAGR (2025-2033): 2.9%

- Asia Pacific: Largest Market in 2024

As commercial and military aircraft continue to push for lighter, stronger materials to improve fuel efficiency and performance, the need for beryllium-containing alloys and components in structural parts, satellite systems, and high-performance electronics increases. Growth in space programs and satellite constellations further amplifies demand because beryllium’s combination of mechanical and thermal properties is hard to replace in precision instruments and optics.Defense and advanced electronics represent another major source of market expansion. Beryllium’s role in guided munitions, radars, and secure communication systems makes it strategically important, prompting defense procurement programs to secure reliable supplies. Meanwhile, the miniaturization of electronics and advances in high-frequency devices boost demand for beryllium-bearing components in connectors, switches, and thermal management solutions. As military modernization and high-tech manufacturing programs progress in multiple countries, these sectors continue to create steady, high-value demand.

")

Innovation in new industrial and scientific applications is widening the beryllium market. Growth in quantum computing, precision optics, and specialized medical devices has raised interest in beryllium for niche, high-performance uses. Research into additive manufacturing and advanced alloys also creates opportunities for beryllium to be used in specialized parts where its properties enable performance that alternative materials cannot match. Expanding these high-margin applications increases mining incentives because they justify investment in secure, high-quality feedstock.

Supply-side dynamics are a powerful growth driver because beryllium production is concentrated and capital-intensive. Limited global primary deposits and the complex, regulated processing chain make supply relatively inelastic, amplifying price signals when demand rises. Geopolitical concerns and export controls on strategic materials encourage downstream users to seek vertically integrated or diversified sources, prompting investment in economically viable exploration and processing capacity. Investors view constrained supply and strategic importance as reasons to support additional mining projects and beneficiation capacity.

Environmental regulations and recycling trends influence the market by shaping lifecycle economics and social license to operate. Strict health and environmental controls around beryllium dust and processing raise compliance costs and can limit expansion in some jurisdictions, which increases the value of responsibly sourced material. At the same time, improvements in recycling beryllium-containing alloys and components alleviate some feedstock pressure, enabling secondary supply for lower-grade applications while leaving primary mined material available for the highest-performance uses. Together, these regulatory and circular-economy factors steer investment toward safer, more efficient, and higher-quality production.

Drivers, Opportunities & Restraints

The growth drivers of the beryllium mining industry largely stem from its unique physical and chemical properties, which make it essential in aerospace, defense, and advanced electronics. Increasing demand for lightweight, high-strength materials in aircraft, satellites, and precision instruments has positioned beryllium as a critical resource. Its role in national security through defense applications such as radars, missiles, and secure communication systems further strengthens mining activities. Rising adoption in medical imaging, nuclear technologies, and high-performance alloys continues to fuel demand, ensuring that beryllium remains a material of strategic importance.

Opportunities are emerging through technological advancements and the diversification of end-use industries. The rising focus on space exploration, renewable energy systems, and quantum computing is creating new avenues where beryllium’s properties are irreplaceable. The expansion of additive manufacturing and advanced alloys has provided fresh applications in industrial and scientific fields. With limited global producers, countries seeking secure supply chains may invest in exploration projects and collaborative ventures, enhancing the market outlook. Growth in recycling technologies also presents opportunities to extend the lifecycle of beryllium-containing products, reducing dependence on primary mining.

Despite its potential, the beryllium mining industry faces significant restraints. Health and environmental hazards related to beryllium exposure impose stringent regulatory frameworks that increase compliance costs. The scarcity of economically viable deposits and the concentration of production in a few regions create supply vulnerabilities and geopolitical risks. High production costs and the availability of alternative materials for certain applications can also limit widespread use.

Application Insights

Form held the revenue share of 69.8% in 2024. The growth of the form segment, which includes beryllium alloys and metal, is being fueled by rising demand in the aerospace, defense, and electronics industries. Beryllium alloys such as beryllium-copper are valued for their high strength-to-weight ratio, thermal stability, and corrosion resistance. These properties make them ideal for satellite structures, missile components, and precision instruments, where lightweight and durable materials are essential.

The others segment in the market is experiencing growth as industries seek advanced materials with unique thermal and electrical characteristics. Beryllium ceramics, such as semiconductor equipment, medical imaging devices, and precision optics, are particularly valuable in applications where heat dissipation, dimensional stability, and resistance to thermal shock are critical. With the ongoing expansion of semiconductor manufacturing and medical technology, demand for beryllium-based ceramics and composites is rising steadily.

End Use Insights

Electronics & telecom held a revenue share of 37.5% in 2024. The electronics and telecom segment in the market is expanding due to the increasing demand for high-performance and reliable electronic components. Beryllium copper alloys are widely used in connectors, switches, and relays because of their excellent electrical conductivity, mechanical strength, and fatigue resistance. Rapid growth in the semiconductor industry, rollout of 5G networks, and the miniaturization of electronic devices drive higher consumption of beryllium-based materials in producing precise and durable components for smartphones, computers, and telecom infrastructure.

The automotive segment is anticipated to register the fastest CAGR over the forecast period as manufacturers increasingly adopt lightweight and high-strength materials to improve fuel efficiency and meet stricter emission norms. Due to their excellent mechanical strength, electrical conductivity, and wear resistance, beryllium copper alloys are used in critical automotive components such as sensors, switches, connectors, and precision engine parts. The shift toward electric vehicles, hybrid drivetrains, and advanced electronics in modern vehicles further drives demand for beryllium-containing materials in battery connectors, braking systems, and electronic control units.

Regional Insights

Asia Pacific accounted for the largest market revenue share of 60.3% in 2024. The Asia-Pacific beryllium mining industry has become a pivotal player in the global market, primarily due to China's substantial production and consumption. In 2023, China extracted over 30,000 metric tons of beryl ore and refined approximately 28 metric tons of beryllium, solidifying its dominant force in the industry. The nation's extensive industrial base and strategic investments in electronics, aerospace, and defense have driven a steady increase in beryllium demand. This growth is further supported by China's expanding refining capabilities, which have enhanced its self-sufficiency in beryllium production.

North America Beryllium Mining Market Trends

The North America beryllium mining industry is pivotal in the global market, primarily because the U.S. produces most of the world’s refined beryllium. The U.S. operates the only commercial bertrandite mining operation in Utah, providing a consistent supply of beryllium to domestic and international markets. This mining operation forms the backbone of the region’s beryllium supply chain, supporting various industrial applications. While not as dominant in raw production, Canada contributes through refining and alloying, helping to meet specialized demands in electronics and high-tech manufacturing. The combination of U.S. production and Canadian processing ensures North America remains largely self-sufficient in meeting its critical beryllium needs.

U.S. Beryllium Mining Market Trends

The U.S. beryllium mining industry dominated the North American market in 2024, accounting for most of the region’s production. The country operates the only commercial bertrandite mine in the world, located in Utah, which serves as the primary beryllium source for domestic consumption and international supply. This mining operation underpins the U.S. beryllium supply chain, providing feedstock to industrial, aerospace, and defense manufacturers. The strategic importance of this resource has led to sustained investment in mining infrastructure and processing capabilities to ensure reliable and consistent production.

Europe Beryllium Mining Market Trends

The beryllium mining industry in Europe is growing, with Luxembourg being the only significant producer within the European Union. In 2024, Luxembourg's production reached 836 tons, accounting for most of the EU's total output of 876 tons. Despite limited local production, Europe represents a substantial consumer of beryllium, driven by aerospace, defense, electronics, and telecommunications sectors.

Latin America Beryllium Mining Market Trends

The beryllium mining industry in Latin America is still in its early stages, with no active commercial beryllium mines currently operating. The region, particularly Brazil, possesses significant geological potential with rich mineral deposits containing beryllium-bearing minerals. These resources position Latin America as a promising area for future beryllium mining projects. The governments in the region have started recognizing the strategic importance of developing their mineral sectors, which may include beryllium as part of broader rare earth initiatives.

Middle East & Africa Beryllium Mining Market Trends

The beryllium mining industry in the Middle East and Africa is currently underdeveloped, with limited commercial production and processing facilities. However, the region holds significant geological potential, particularly in countries such as Mozambique, Nigeria, and South Africa, where new beryl deposits have been identified. In 2023, Mozambique and Nigeria reported discovering new beryl deposits totaling approximately 5,000 metric tons, indicating the region's untapped resources. Despite these discoveries, the lack of refining infrastructure and export logistics poses challenges to scaling up production to meet global demand.

Key Beryllium Mining Company Insights

Some of the key players operating in the market include Materion Corporation, Ulba Metallurgical Plant, and others

-

Materion Corporation is a leading global supplier of advanced materials, with a strong presence in beryllium mining and production. The company specializes in providing high-performance beryllium and beryllium-based products for applications requiring lightweight, strong, and thermally stable materials. Its beryllium offerings are widely used in aerospace, defense, electronics, and industrial sectors, where precision and reliability are critical. Materion operates integrated mining, refining, and alloying facilities that allow for control over product quality and supply chain efficiency, ensuring consistent performance for its customers worldwide.

-

Ulba Metallurgical Plant, based in Kazakhstan, is a major producer of beryllium and beryllium compounds. The company has developed a vertically integrated operation encompassing the extraction of beryllium ores, processing, and production of beryllium metals and alloys. Ulba, leveraging its advanced metallurgical expertise, serves various high-tech industries, including aerospace, nuclear energy, and electronics. Its focus on innovation and quality control has positioned it as a reliable supplier in the global beryllium market, supporting domestic and international industrial demands.

Key Beryllium Mining Companies:

The following are the leading companies in the beryllium mining market. These companies collectively hold the largest market share and dictate industry trends.

- Materion Corporation

- Ulba Metallurgical Plant

- Xinjiang Xinxin Mining Industry Co Ltd

- China Nonferrous Metal Mining Group Co Ltd (CNMC)

- Hunan Shuikoushan Nonferrous Metals Group Co Ltd

- IBC Advanced Alloys Corp

- NGK Metals Corporation

- American Beryllia Inc

- Belmont Metals Inc

- Texas Mineral Resources Corp

Recent Development

-

In September 2025, BGV Group Management received the first draft of a preliminary feasibility study (PFS) for its flagship Ukrainian Beryllium project, prepared by SGS Canada to NI 43-101 standards. The PFS results revealed robust economic fundamentals, projecting a payback period of up to five years, substantially faster than the industry average of 8-15 years, and confirming significant reserves of beryllium and zinc as key minerals. This enhances Ukraine’s global strategic role as a prospective beryllium supplier for the EU, US, and Asian markets, especially as the demand grows in aviation, defense, nuclear energy, and electronics.

Beryllium Mining Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 11.04 billion

Revenue forecast in 2033

USD 13.92 billion

Growth rate

CAGR of 2.9% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative Units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

End use, application, region.

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Brazil; Saudi Arabia, UAE

Key companies profiled

Materion Corporation; Ulba Metallurgical Plant; Xinjiang Xinxin Mining Industry Co Ltd; China Nonferrous Metal Mining Group Co Ltd (CNMC); Hunan Shuikoushan Nonferrous Metals Group Co Ltd; IBC Advanced Alloys Corp; NGK Metals Corporation; American Beryllia Inc; Belmont Metals Inc.; Texas Mineral Resources Corp

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Beryllium Mining Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global beryllium mining market report based on application, end use, and region.

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Form

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Aerospace & Defense

-

Electronics & Telecom

-

Automotive

-

Medical and Dental

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The electronics & telecom segment dominated the market with a revenue share of 37.5% in 2024.

Some of the key players of the global beryllium mining market are Materion Corporation, Ulba Metallurgical Plant, Xinjiang Xinxin Mining Industry Co Ltd, China Nonferrous Metal Mining Group Co Ltd (CNMC), Hunan Shuikoushan Nonferrous Metals Group Co Ltd, IBC Advanced Alloys Corp, NGK Metals Corporation, American Beryllia Inc, Belmont Metals Inc, Texas Mineral Resources Corp, and others.

The key factor driving the growth of the global beryllium mining market is the rising demand for lightweight and high-performance materials across aerospace, defense, telecommunications, and electronics industries.

The global beryllium mining market size was estimated at USD 10.70 billion in 2024 and is expected to reach USD 11.04 billion in 2025.

The global beryllium mining market is expected to grow at a compound annual growth rate of 2.9% from 2025 to 2033 to reach USD 13.92 billion by 2033.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.