- Home

- »

- Biotechnology

- »

-

Cell Analysis Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Cell Report]()

Cell Analysis Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product & Service (Reagents & Consumables, Instruments), By Technique (Flow Cytometry, Cell Microarrays), By Process, By End-use, By Region, And Segment Forecasts

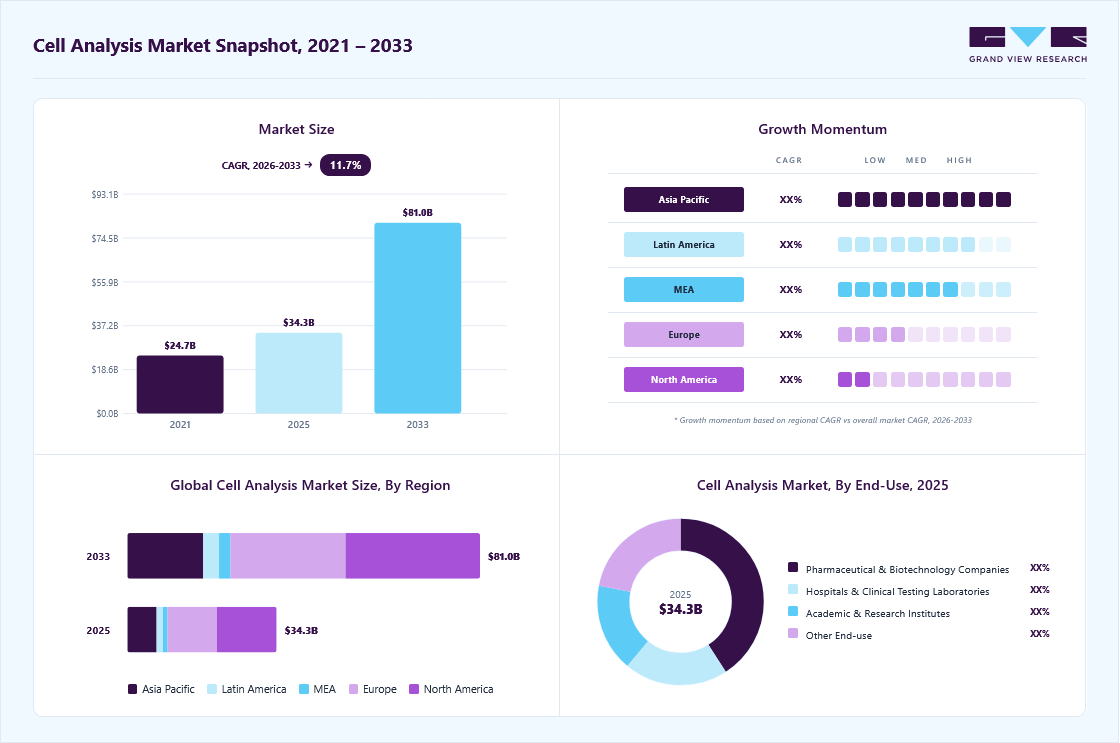

Market Size, 2025

$34.3BMarket Estimate, 2026

$37.3BMarket Forecast, 2033

$81.0BCAGR, 2026–2033

11.7%Cell Analysis Market Summary

The global cell analysis market size was valued at USD 34.3 billion in 2025 and is projected to grow from USD 37.3 billion in 2026 to USD 81.0 billion by 2033, at a CAGR of 11.7% from 2026 to 2033. North America dominated the market with the largest revenue share of 40.0% in the global market in 2025. Market growth is driven by the rising prevalence of chronic diseases, advancements in cell analysis technologies, and increasing drug discovery activities.

Key Market Trends & Insights

- By product & service: Reagents & consumables segment held the largest market share of 48.0% in 2025.

- By technique: Flow cytometry segment held the largest market share of 18.6% in 2025.

- By process: Single-cell analysis segment held the largest market share of 19.0% in 2025.

- By end use: Pharmaceutical & biotechnology companies segment held the largest market share of 40.8% in 2025.

Regional Highlights

- Largest regional market: North America (40.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 34.3 Billion

- Estimated market size in 2026: USD 37.3 Billion

- Projected market size by 2033: USD 81.0 Billion

- CAGR (2026-2033): 11.7%

The application of cell analysis has expanded from early-stage cancer diagnostics to the development of cancer-targeted therapies and tools, strengthening its role in oncology.")

Companies are actively investing in advanced cell analysis methods to support the development of innovative treatments. For instance, in March 2024, Serum Detect announced the launch of a T-cell analysis approach for early cancer detection at the American Association for Cancer Research (AACR). Such initiatives are expected to support market growth during the forecast period.

Advancements in Cell Analysis Technologies

Advancements in cell analysis technologies remain a key driver of market growth, with companies launching next-generation platforms that improve sensitivity, throughput, and multi-parameter data analysis. For instance, in May 2025, BD (Becton, Dickinson and Company) introduced the BD FACSDiscover A8 Cell Analyzer, which integrates spectral flow cytometry with real-time imaging to capture over 50 cellular characteristics and detailed morphological data in a single run, supporting deeper insights in drug discovery and translational research.

Key Advancements in Cell Analysis Technologies

Advancement

Description

Impact on Cell Analysis

High-Content Screening (HCS)

Combines automated microscopy with image analysis to study multiple cellular parameters simultaneously.

Enables high-throughput drug screening and detailed cellular phenotyping.

Flow Cytometry & Spectral Cytometry

Advanced cytometry techniques allowing multiparametric analysis of cells using fluorescent markers.

Improves identification of cell populations and immune profiling.

Single-Cell Analysis Technologies

Techniques such as single-cell sequencing and single-cell proteomics analyze individual cells rather than bulk samples.

Enhances understanding of cellular heterogeneity in diseases like cancer.

Microfluidics-Based Cell Analysis

Uses micro-scale fluid systems to isolate, manipulate, and analyze cells efficiently.

Enables precise cell sorting, reduced sample consumption, and rapid diagnostics.

Source: Secondary Research, Primary Interviews, Grand View Research

Technology integration isn’t limited to instruments alone; software and AI are reshaping how cellular data is processed and interpreted. New AI-driven platforms like ThinkCyte’s VisionCyte, pre-commercially launched in January 2025, exemplify how machine learning can augment sorting, classification, and analysis workflows to accelerate discovery in regenerative medicine and cell therapy development.

Increasing Prevalence of Chronic Diseases

The rising prevalence of chronic diseases such as cancer, diabetes, cardiovascular disorders, and autoimmune conditions is a major driver of the cell analysis industry. These diseases involve complex cellular changes, increasing the demand for advanced tools to study cell behavior, signaling pathways, and immune responses. Technologies such as flow cytometry, high-content imaging, and single-cell analysis are widely used to identify biomarkers, study disease progression, and evaluate therapeutic responses.

In addition, the long-term management of chronic diseases is increasing the demand for personalized and cell-based therapies. Precision medicine requires detailed cellular profiling to tailor treatments and monitor patient outcomes. As aging populations and lifestyle factors continue to raise the global burden of chronic diseases, the demand for advanced and scalable cell analysis solutions is expected to grow.

Market Dynamics

The growing number of drug discovery activities is a key driver of the cell analysis market, as cell-based technologies are increasingly central to identifying and evaluating therapeutic candidates early in development. As pharmaceutical and biotechnology companies expand R&D pipelines and invest more in high-throughput screening and phenotypic assays, cell analysis platforms, such as flow cytometers, high-content imaging systems, and single-cell analysis tools, are essential for assessing compound efficacy, toxicity, and mechanism of action in biologically relevant models.

Recent industry developments highlight how drug discovery priorities are shaping broader life sciences innovation. For instance, Illumina unveiled the Billion Cell Atlas in January 2026, a large dataset designed to accelerate AI-powered drug discovery by mapping cellular responses across hundreds of disease-relevant cell lines, supporting target identification and candidate screening at an unprecedented scale. In another strategic move reflecting the industry’s focus on therapeutic innovation, Agilent Technologies opened a new biopharma experience center in Hyderabad in 2025, aimed at accelerating life-saving drug development with integrated solutions spanning cell analysis and laboratory informatics. These examples show how heightened activity in drug discovery not only expands the use of cell analysis technologies but also drives collaboration and investment across the market..

The complexity of cell analysis techniques is a significant restraint for the cell analysis market, as many advanced methods require specialized expertise, sophisticated instrumentation, and carefully controlled workflows. Technologies such as multi-parameter flow cytometry, high-content imaging, and single-cell sequencing involve complex sample preparation, instrument calibration, and data interpretation processes. Laboratories often need highly trained personnel to operate these systems and ensure data accuracy, which can increase operational costs and limit adoption, particularly in smaller research settings or resource-constrained regions.

In addition, the large volume and high dimensionality of data generated by modern cell analysis platforms create challenges in data management, analysis, and standardization. Interpreting complex datasets often requires advanced software tools, bioinformatics capabilities, and integration across multiple experimental platforms, which can slow workflows and increase the risk of variability or errors. These technical and analytical challenges may discourage new users and extend implementation timelines, thereby restraining the broader adoption of advanced cell analysis technologies despite their scientific value.

Advancements in cell analysis technologies are a key market opportunity, with companies launching next-generation platforms that improve sensitivity, throughput, and data integration. For instance, in May 2025, BD launched the BD FACSDiscover A8 Cell Analyzer, combining spectral flow cytometry with real-time imaging to capture over 50 cellular parameters and detailed morphological data in a single run, enabling deeper insights for drug discovery and translational research. Similarly, Cytek Biosciences introduced the Cytek Muse Micro in March 2025, offering simplified flow cytometry with intuitive “Mix-and-Read” assays, expanding access to advanced cell analysis in both research and clinical settings.

Alongside hardware innovation, software and AI integration are transforming data analysis and interpretation. Platforms such as ThinkCyte’s VisionCyte, pre-commercially launched in January 2025, demonstrate how machine learning enhances cell sorting, classification, and workflow efficiency in regenerative medicine and cell therapy development. Broader trends in automation, cloud-based analytics, and high-throughput systems are further improving reproducibility and reducing manual intervention, collectively strengthening the role of cell analysis as a core enabling technology across life sciences and clinical research.

Data management and storage complexity is a significant challenge in the cell analysis market due to the massive volumes of high-dimensional data generated by technologies such as high-content imaging, flow cytometry, and single-cell analysis. These platforms produce terabytes of multi-parameter and multi-omics data per experiment, requiring robust, scalable infrastructure for storage, retrieval, and long-term archiving, which many small and mid-sized laboratories struggle to implement. The challenge is further intensified by the analytical complexity of integrating and interpreting heterogeneous datasets, which demands advanced computational tools, bioinformatics expertise, and standardized workflows. Variability in data formats, limited interoperability across platforms, and a lack of standardization hinder seamless data consolidation, leading to reduced reproducibility, inconsistent outputs, and difficulties in multi-study comparisons, ultimately constraining the efficiency and adoption of advanced cell analysis solutions.

In addition, the demand for regulatory compliance and data security adds another layer of complexity. Clinical and pharmaceutical applications of cell analysis, particularly in cell and gene therapies, require rigorous documentation, traceability, and secure storage of sensitive patient-derived information. Cloud-based solutions and AI-enabled analytics are increasingly adopted to address these issues, but implementing and maintaining such systems involves high costs, training, and IT support. Consequently, data management and storage challenges remain a critical barrier that can slow market growth and limit the full potential of advanced cell analysis technologies.

Market Concentration & Characteristics

The cell analysis industry is highly innovative, driven by advances in single-cell analysis, flow cytometry, and high-content imaging. Integration of automation, artificial intelligence, and advanced analytics improves accuracy, throughput, and data interpretation, supporting applications in drug discovery, precision medicine, and disease research.

The level of M&A activities in the cell analysis industry is moderate to high, as leading life sciences and biotechnology companies actively pursue acquisitions and strategic partnerships to expand their technology portfolios and strengthen their market presence. These transactions often focus on gaining access to advanced platforms such as single-cell analysis, flow cytometry, and AI-driven data analytics, enabling companies to enhance their research capabilities and accelerate innovation in drug discovery and precision medicine.

Regulations have a significant impact on the cell analysis industry, as instruments, reagents, and related technologies used in clinical and research applications must comply with strict regulatory standards set by authorities such as the U.S. Food and Drug Administration and the European Medicines Agency. These regulations ensure product safety, quality, and reliability, particularly for diagnostic and therapeutic applications. While compliance requirements can increase development timelines and costs, they also support market credibility and encourage the adoption of standardized, high-quality cell analysis technologies.

Product expansion in the cell analysis industry is significant, with companies continuously introducing advanced instruments, reagents, and software platforms to strengthen their portfolios. Key players are focusing on developing high-throughput systems, single-cell analysis tools, and integrated data analytics solutions to address the growing demand from research, drug discovery, and clinical diagnostics applications.

Regional expansion in the cell analysis industry is increasing as key companies expand their presence in emerging markets across Asia-Pacific, Latin America, and the Middle East. Growing investments in life sciences research, improvements in healthcare infrastructure, and rising biotechnology activity in these regions are encouraging companies to establish new distribution networks, research facilities, and strategic partnerships to strengthen their global footprint.

Product & Services Insights

The reagents & consumables segment led the market with the largest revenue share of 48.0% in 2025. The demand for reagents and consumables in the cell analysis market is driven by the rapid expansion of research in areas such as immunology, oncology, and stem cell biology. As laboratories and biopharma companies increasingly focus on high-throughput screening, single-cell sequencing, and complex phenotyping, there’s a growing need for specialized kits, fluorescent labels, and assay-specific reagents that can deliver reliable, reproducible results.

The services segment is anticipated to grow at the fastest CAGR during the forecast period. A major driver for services in the cell analysis market is the increasing reliance on advanced instruments that require ongoing technical support, maintenance, and calibration to perform optimally. As laboratories deploy complex platforms like high-parameter flow cytometers, live-cell imaging systems, and cell sorters, they need reliable service agreements to minimize downtime, extend equipment longevity, and ensure data accuracy

Technique Insights

The flow cytometry segment led the market with the largest revenue share of 18.6% in 2025. This can be attributed to the ability of the flow cytometry process to allow researchers to analyze many cells simultaneously with multiple parameters such as size, shape, granularity, and the presence of specific molecules in or outside the cell surface. Moreover, several market players are developing solutions to enhance the accuracy of flow cytometry results, further contributing to its growth.

The high-content screening segment is expected to grow at the fastest CAGR over the forecast period. High-content screening goes beyond traditional cell analysis techniques by leveraging automated image analysis, artificial intelligence (AI), and machine learning, enabling researchers to gain deeper insights. Moreover, the ability of high-content screening to analyze many compounds and cellular features simultaneously is anticipated to drive its demand over the forecast period.

Process Insights

The single-cell analysis segment led the market with the largest revenue share of 19.0% in 2025 and is projected to grow at the fastest CAGR during the forecast period. Single-cell analysis enables researchers to examine individual cells, revealing the remarkable heterogeneity within a seemingly homogeneous group. This hidden diversity can be crucial for cellular function, disease development, and drug response. Moreover, several market players are developing advanced solutions for single-cell analysis, further contributing to the segment growth.

The cell identification segment is expected to witness at a significant CAGR over the forecast period, driven by the increasing need for accurate characterization of heterogeneous cell populations in research and clinical applications. Techniques such as flow cytometry, immunostaining, and single-cell sequencing enable researchers to distinguish specific cell types, identify rare subpopulations, and monitor dynamic cellular changes in response to treatments. This capability is critical in fields like immunology, oncology, and stem cell research, where understanding cell-specific behavior informs drug development, biomarker discovery, and therapeutic strategies.

End Use Insights

The pharmaceutical and biotechnology companies segment led the market with the largest revenue share of 40.8% in 2025. This can be attributed to the increasing drug discovery efforts, high R&D investment capacity, and increasing focus on personalized medicine by these companies. Pharmaceutical and biotechnology companies account for a significant share of drug discovery activities. Cell analysis, a crucial part of drug discovery, is used by these companies for various purposes, thereby increasing the segment share of pharmaceutical and biotechnology companies.

The hospitals and clinical testing laboratories segment is expected to witness at the fastest CAGR from 2026 to 2033. The fast growth can be attributed to the increasing demand for biomarker identification, early disease diagnostics, and disease progression. Cell analysis can help identify specific molecules or cellular characteristics, allowing hospitals to predict a patient's response to a particular treatment. This allows healthcare providers to personalize treatment plans for each patient, improving patient outcomes. Similarly, advanced cell analysis techniques can enable healthcare providers to diagnose diseases more accurately and effectively, further underscoring their importance to hospitals and clinical testing laboratories.

Regional Insights

North America dominated the global cell analysis market with the largest revenue share of 40.0% in 2025, owing to the large number of drug discovery activities, better access to advanced cell analysis technologies, and presence of key market players, and the high prevalence of chronic diseases in the region. According to the Statistics Canada data, approximately 45.1% of Canadians in 2021 suffered from at least one major chronic disease. Such a high prevalence of chronic diseases increases the need for advanced, effective treatments, thereby driving market growth.

U.S Cell Analysis Market Trends

The cell analysis market in the U.S. accounted for the largest market revenue share in North America in 2025, driven by the presence of major market players, supportive regulations, and increasing R&D investments by pharmaceutical and biotechnology companies. The availability of advanced technologies and frequent product launches by leading companies further support the adoption of cell analysis solutions and market expansion.

Europe Cell Analysis Market Trends

The cell analysis market in Europe is supported by strong public research funding, cross-border collaboration, and a well-established pharmaceutical industry. Countries such as Germany, the UK, France, and Switzerland lead the market due to advanced research infrastructure and active biotechnology clusters, while EU and national research programs continue to promote cell-based research and translational medicine.

The UK cell analysis market is driven by life science hubs such as Cambridge, Oxford, and London, with strong competition centered around advanced translational research. Companies primarily compete by supporting complex applications, including immunophenotyping, cell therapy development, and advanced imaging, particularly for university hospitals, cell therapy centers, and contract research organizations (CROs).In November 2024, UK-based Cytomos raised USD 5 million in an oversubscribed round to scale production, commercialize its Celledonia platform, and expand global adoption of its single-cell analysis technology.

The cell analysis market in Germany is highly consolidated and innovation-driven, with competition led by global life-science instrument manufacturers and strong domestic biotechnology firms. The country’s local production base and strong R&D ecosystem drive competition in areas such as automation, single-cell analysis performance, and integration with advanced academic and pharmaceutical research workflows.

Asia Pacific Cell Analysis Market Trends

The cell analysis market in the Asia Pacific is anticipated to witness at the fastest CAGR of 13.1% from 2026 to 2033, due to increasing investments in biomedical research, expanding biopharmaceutical manufacturing, and rising adoption of advanced analytical technologies. Government funding programs and innovation policies, along with the expansion of laboratory infrastructure and industry-academic collaborations in countries such as China, Japan, India, and South Korea, are further supporting market expansion.

The China cell analysis market is anticipated to grow at a significant CAGR during the forecast period, driven by strong government initiatives supporting biotechnology innovation, precision medicine, and advanced biopharmaceutical manufacturing. Increasing investments in research infrastructure and growing activities in genomics, immunology, and stem cell research are accelerating the adoption of advanced, high-throughput cell analysis technologies across academic and commercial laboratories.

The cell analysis market in Japan is mature and innovation-driven, supported by a strong focus on biotechnology, regenerative medicine, and precision healthcare. Government funding, collaboration between academia and industry, and advanced laboratory infrastructure enable the widespread adoption of sophisticated cell analysis technologies across research and clinical laboratories.

Middle East & Africa Cell Analysis Market Trends

The cell analysis market in the Middle East & Africa is growing steadily due to increasing investments in healthcare infrastructure, precision medicine, and research activities. Governments, particularly in GCC countries, are promoting biotechnology innovation and advanced diagnostics, driving demand for technologies such as flow cytometry and molecular analysis

The Kuwait cell analysis market is experiencing steady growth, supported by increasing healthcare modernization initiatives and rising investments in advanced diagnostic infrastructure

Key Cell Analysis Company Insights

The cell analysis industry comprises global life sciences companies and specialized biotechnology firms competing through advanced analytical platforms, integrated workflow solutions, and application-specific technologies designed for cell biology, drug discovery, and clinical research.

Key players such as Thermo Fisher Scientific, Inc., Danaher (Cytiva), BD, Merck KGaA, Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., Miltenyi Biotec, Revvity, New England Biolabs, and Avantor, Inc. maintain strong market positions due to their extensive product portfolios in cell analysis instruments, reagents, and software, along with well-established global distribution networks and continuous investments in innovative life science technologies.

Key Cell Analysis Companies:

The following key companies have been profiled for this study on the cell analysis market.

- Thermo Fisher Scientific, Inc.

- Danaher (Cytiva).

- BD

- Merck KGaA

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Miltenyi Biotech

- Revvity

- New England Biolabs

- Avantor, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Thermo Fisher Scientific, Inc.

- Focus on building integrated cell analysis ecosystems combining instruments, reagents, consumables, and software platforms

- Strong emphasis on automation, high-throughput workflows, and AI-enabled data analytics for advanced cell characterization

- Strong global footprint with diversified life sciences and diagnostics portfolios

- Advanced technology platforms enabling multi-parameter, high-precision cell analysis

- High dependency on capital-intensive R&D and acquisition-led growth strategies

Emerging Players: New England Biolabs

- Focus on specialized cell analysis workflows such as flow cytometry, molecular assays, and sample preparation tools

- Emphasis on innovation in niche research applications and high-precision laboratory solutions

- Strong technical expertise in specialized cell analysis techniques and reagents

- High innovation, agility, and faster product development cycles in niche segments

- Higher vulnerability to pricing pressure from large diversified competitors

Recent Developments

-

In December 2025, BD commercially released new three‑ and four‑laser BD FACSDiscover A8 cell analyzer configurations globally from Franklin Lakes, USA, expanding access to spectral and real‑time imaging for research labs globally.

-

In July 2024, Illumina, Inc. acquired Fluent BioSciences to expand its multiomics portfolio, integrating Fluent’s scalable single-cell PIPseq V technology and accelerating accessible single-cell analysis for a broader customer base.

Cell Analysis Market Report Scope

Report Attribute

Details

Market size in 2025

USD 34.3 billion

Estimated Market size in 2026

USD 37.3 billion

Projected Market size by 2033

USD 81.0 billion

Growth rate

CAGR of 11.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product & service, technique, process, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Australia; Thailand; South Korea; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Thermo Fisher Scientific, Inc.; Danaher (Cytiva).; BD; Merck KGaA; Agilent Technologies, Inc.; Bio-Rad Laboratories, Inc.; Miltenyi Biotech; Revvity; New England Biolabs; Avantor, Inc.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Cell Analysis Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global cell analysis market report based on the product & service, technique, process, end-use, and region.

-

Product & Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Reagents & Consumables

-

Instruments

-

Accessories

-

Software

-

Service

-

-

Technique Outlook (Revenue, USD Million, 2021 - 2033)

-

Flow Cytometry

-

PCR

-

Cell Microarrays

-

Microscopy

-

Spectrophotometry

-

High Content-Screening

-

Other Techniques

-

-

Process Outlook (Revenue, USD Million, 2021 - 2033)

-

Cell Identification

-

Cell Viability

-

Cell Signaling Pathways

-

Cell Proliferation

-

Cell Counting

-

Cell Interaction

-

Cell Structure Study

-

Single-cell Analysis

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharmaceutical & Biotechnology Companies

-

Hospitals & Clinical Testing Laboratories

-

Academic & Research Institutes

-

Other

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional & Country-Level Cell Analysis Market Segmentation

Detailed breakdown of the global cell analysis market across North America, Europe, Asia Pacific, Latin America, and MEA, including key countries (U.S., China, Germany, India, Japan, etc.). Covers regional market size, growth trends, adoption of technologies like flow cytometry and single-cell analysis, and country-wise demand patterns across pharma, biotech, and clinical research ecosystems.

Identifies high-growth geographies driven by rising R&D investment, precision medicine adoption, and biopharma expansion; enables region prioritization, market entry strategy, and localization of product & commercial strategies.

Cross-Segmentation Analysis (Product × Technique × End Use × Application)

Multi-layered analysis combining product types (instruments, reagents & consumables, software, services), techniques (flow cytometry, PCR, high-content screening, microscopy), applications (oncology, immunology, drug discovery, stem cell research), and end users (pharma & biotech, hospitals, academic institutes, CROs).

Reveals high-value demand intersections (e.g., reagents in oncology research or flow cytometry in pharma), identifies niche growth pockets like single-cell analysis, and supports targeted portfolio expansion and investment prioritization.

Competitive Benchmarking & Market Opportunity Assessment

Profiling of key players such as Thermo Fisher Scientific, Danaher, BD, Merck KGaA, Bio-Rad, Agilent, and others, including product portfolios, technology leadership, geographic footprint, and innovation focus in single-cell and AI-driven cell analysis platforms.

Supports competitive positioning and gap identification in technology adoption (e.g., high-content screening vs. flow cytometry), informs partnership/M&A strategies, and highlights innovation-driven differentiation opportunities in the market.

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The reagents & consumables segment held the market with the largest revenue share of 48.0% in 2025, while services is the fastest-growing segment.

The flow cytometry segment led the market with the largest revenue share of 18.6% in 2025, while high-content screening is the fastest-growing segment.

Some of the key players operating in the market include Thermo Fisher Scientific, Inc., Danaher, BD, Merck KGaA, Agilent Technologies, Inc., Bio-Rad Laboratories, Inc., Miltenyl Biotech, Revvity, New England Biolabs, and Avantor, Inc.

The growth of the market can be attributed to the increasing prevalence of chronic diseases, advancements in cell analysis technologies, and the growing number of drug discovery activities.

The global cell analysis market size was valued at USD 34.3 billion in 2025 and is projected to reach USD 37.3 billion by 2026.

The global cell analysis market is expected to grow at a CAGR of 11.7% from 2026 to 2033, reaching USD 81.0 billion by 2033

North America dominated with a revenue share of 40.0% in 2025.

The single-cell analysis segment led the market with the largest revenue share of 19.0% in 2025, while cell identification is the fastest-growing segment.

The pharmaceutical & biotechnology companies segment led the market with the largest revenue share of 40.8% in 2025, while hospitals and clinical testing laboratories is the fastest-growing segment.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.